→ Download the Business Credit Checklist PDF

As an entrepreneur looking to build credit for your small business, you’ve probably realized how important it is to establish creditworthiness. Building credit for your business is crucial to secure start-up funds, get financed for operating costs, or expand your offer.

Establishing business credit can be challenging, but by following this checklist, you can get your business on the right track. Here’s a comprehensive business credit checklist with nine essential steps to help you build and maintain business credit. From getting your personal credit in check to applying for business credit, we’ll walk you through each step to help you establish a strong credit profile for your small business.

Here’s everything covered in this checklist:

- 1. Get Your Personal Credit In Check

- 2. Establish Your Business for “Credit Readiness”

- 3. Open a Business Bank Account

- 4. Establish Relationships at the Bank

- 5. Make Sure You Have a DUNS Number

- 6. Establish Your First Trade Lines of Credit

- 7. Pay Your Accounts at the Right Time

- 8. Check and Monitor Your Business Credit

- 9. Apply for Business Credit

- Final Thoughts

Now, let’s get to it!

1. Get Your Personal Credit In Check

Before you start building business credit, you need to get your personal credit in check. It doesn’t necessarily have to be perfect, but most business credit lenders require a “personal guarantee” (PG). This means your personal credit can impact your ability to obtain funds for your business.

If you don’t know without a doubt that your personal credit is excellent, here’s what you need to do:

- Obtain a copy of your credit report from each of the three major credit bureaus – Equifax, Experian, and TransUnion — You can do this through AnnualCreditReport.com or individual credit bureaus’ websites.

- Review your credit reports carefully and dispute any errors or inaccuracies with the credit bureau(s) reporting it.

- Pay down any outstanding balances on loans, credit cards, or lines of credit to decrease the size of outstanding debt in proportion to your available credit. This will lower your credit utilization ratio, which can boost your credit score over time.

- Make timely payments on all current and prior debt obligations and avoid negative marks by paying your bills on time.

- Try to increase the average length of your credit history by keeping your oldest credit card account(s) open and active (closing them can reduce your credit history and negatively affect your credit score).

- Avoid opening multiple new credit card accounts or loans at once, as it can impact your credit score negatively in the short term.

- Monitor your credit reports regularly to ensure that they reflect your current creditworthiness.

Your personal credit score can impact your ability to secure business credit, so it’s crucial to maintain healthy financial habits like making timely payments and keeping credit balances low. Improving and maintaining your personal credit score is an investment in the future of your business.

Recommended: Credit Secrets Book Review: Can You Erase Bad Credit History?

2. Establish Your Business for “Credit Readiness”

Whether your business is established or brand new, there are several items you need to be “credit ready.” Go through this list and make sure you’ve done everything you need to make your business seem credible to lenders.

Note that you need to choose a consistent business name and address, and a start date, get a business phone number, and create a legal entity for your business. If your business has a physical location, determining an address is easy. If not, you can use a virtual address or shared office space. And, use a consistent date for your business start date.

Here’s how to properly set up and establish your business:

- Register your business with the appropriate authorities and file state and federal paperwork as required.

See: Sole Proprietorship VS LLC: How to Choose Your Entity Wisely

- Apply for an Employer Identification Number (EIN) from the IRS in the company’s name.

- Set up a dedicated business phone line and list it on 411 under the exact business name used on your registration.

- Create a professional business website and email address.

- Ensure credibility by meeting the following requirements for business credit approval:

- Use the full legal name, including DBAs, and ensure it matches the corporation records for the business name.

- Obtain necessary business licenses required by your industry and state.

- Make sure your EIN matches exactly with your state filing.

- Have a physical business address and avoid using P.O. box. If you use your home office address, establish a suite number.

- Use a real business or VOIP number instead of your mobile or home phone — for a free or low-cost option, look into Google Voice.

- Have a business fax number — you can use an online service for this, if you don’t want to mess with a fax machine.

- Ensure there are no liens, judgments, or lis pendens exist against the business in public records.

By following these steps, your business can establish good business credit, which is necessary for obtaining business credit approval.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

3. Open a Business Bank Account

You need a business bank account to get business credit because it helps lenders verify your financial stability and separate your business and personal finances. Without one, you may not be able to provide the necessary information to apply for business credit, and it can harm your chances of approval.

Here’s how to open a business bank account:

- Research and identify a suitable bank or credit union for your business needs. Small community banks and credit unions are often a great option for businesses.

See: 3 Best Credit Unions for Small Business Banking

→ Interested in online banking? See our full write-ups on Novo Bank, Amex Business Checking, Bluevine, and NorthOne.

- Gather your business’s legal documents such as your state and local business license, Articles of Incorporation or Organization, and the employer identification number (EIN) issued by the IRS.

- Schedule an appointment with the bank and bring the business documents, along with the personal identification documents of anyone authorized to make transactions on the account.

- Choose the type of account you need, such as a checking or savings account, and ensure that it meets the requirements of your business.

- Provide the bank with the business’s address, phone number, and tax/EIN number to set up the account.

- Ask about any fees, minimum balance requirements, and transaction limits associated with the account and make sure you understand the terms and conditions.

- Commit to using this account for all business expenses and avoid using it for personal expenses. Mixing business and personal transactions can make it difficult to track expenses, which can lead to complications come tax season.

Opening a business bank account is essential for establishing financial credibility for your business. By choosing the right account and keeping personal and business expenses separate, you can effectively manage your business finances, and build a positive relationship with your bank or credit union.

4. Establish Relationships at the Bank

Establishing a good relationship with your bank provides several benefits, including quicker loan processing, more flexibility, access to financing, personalized services, and financial expertise. It lays a strong foundation of mutual understanding, trust, and communication, which can help your business grow and succeed.

Here are some steps you can take to establish rapport at your bank:

- Schedule a meeting with a business banker at your bank to introduce yourself and your business. Use this opportunity to learn more about the bank’s lending policies and requirements.

- Use your bank account regularly for all business transactions. This can help you establish a positive payment history and build trust.

- Avoid overdrafts and NSFs from your bank account.

- If your business needs a loan, consider applying for a small business loan through your bank rather than going to alternative lenders like online lenders or credit cards. This can help you establish a credit history with the bank and show that you are committed to building a relationship with them.

- Attend local business events and network with other entrepreneurs and business professionals. Building these relationships can help entrepreneurs gain referrals and make useful connections.

- Be open and honest with the bank about your business’s financial situation, plans, and goals. Honesty can help build trust.

- Regularly communicate with the bank to nurture the relationship and ensure that they are aware of your business’s successes and challenges.

Taking these steps can help you establish strong relationships with your bank and increase your odds of obtaining business credit. Building a relationship with your bank is important in establishing financial credibility and creating a successful business.

Recommended: This is How to Leverage Business Credit to Transform Your Life

5. Make Sure You Have a DUNS Number

A business needs a DUNS number to establish a credit file, enhance credibility, access loans and credit, and increase visibility. It’s a unique identifier assigned by Dun & Bradstreet (the leading business credit bureau) that allows for easy tracking and reporting of credit history, and it’s free and easy to obtain online.

Here’s how to make sure your business has a DUNS number:

- Check if your business is listed with the major business credit reporting agencies, including Dun & Bradstreet, Equifax, and Experian. You can search for your business on their website or through a free Nav account.

- Apply for a free D-U-N-S number from Dun & Bradstreet, which is required to create a business credit profile in their system. It can take 4-6 weeks to process.

When you take these steps, you can properly build business credit. It’s important to stay on top of your payments and ask others to report on your payments as well to ensure you build a positive credit history.

Recommended: Everything You Need to Know About a DUNS Number – and Why You Should Care

6. Establish Your First Trade Lines of Credit

Establishing the first tradelines (credit accounts) for your business is crucial to building and improving your business credit score. It involves paying on time and generating a positive payment history with suppliers or vendors that report to credit reporting agencies. By doing this, you increase your chances of obtaining financing and credit on favorable terms for your business.

To obtain vendor credit, follow these steps:

- Locate 3-5 vendors who report to business credit reporting agencies.

See: Using 30-Day Net Vendors to Build Your Business Credit Score

- Ask all vendors, suppliers, and service providers to report on your payments to improve your score — your CPA and attorney might be able to report on your payments as well.

- Apply for vendor credit using your EIN without revealing your SSN.

- Purchase products from these vendors, following their reporting terms.

- Use the newly approved credit to buy over $50 worth of items.

- Pay your accounts on time, preferably early in the billing cycle.

You can build business credit and establish a positive payment history by following these steps — this will allow you to access credit and better financing options in the future.

Recommended: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

7. Pay Your Accounts at the Right Time

Paying business tradeline accounts on time is crucial to maintain a positive payment history, improve your business credit score, and build positive supplier/vendor relationships. Late payments can harm your credit score, trigger fees, and damage your reputation, making it harder to obtain financing and business opportunities in the future.

Here’s how to build business credit by paying on time:

- Set up reminders, alerts, or auto payments to pay business accounts on time.

- Pay your bills early to further improve your credit score, (this also helps you take advantage of discounts with suppliers).

- Proactively contact suppliers to avoid late fees or negative reports if you can’t make a payment on schedule.

- Connect the tradeline to your business account and use it to pay the credit card bill to establish a good payment history.

*By connecting your tradeline to your business bank account and using it to pay your invoices, you establish a good payment history and keep cash flowing through your account.

Recommended: eCredable: A Deep Dive Into the Business Credit Reporting Platform

8. Check and Monitor Your Business Credit

Reviewing business credit reports often, promptly correcting any errors, and taking action if fraudulent activity occurs can protect you from business credit fraud and identity theft.

Here are some action steps to monitor your business credit effectively:

- Understand the number of payment experiences required to qualify for different types of business credit — as a rule, you should gather at least 3 payment experiences on your business credit report.

- Obtain credit reports from business reporting agencies such as D&B, Experian, and Equifax by obtaining a DUNS number for free from D&B and enrolling for reporting agencies.

- Check credit reports every month to monitor for unfamiliar inquiries or accounts you didn’t authorize.

- Review reports from all agencies quarterly, correct errors promptly, and take action if any fraudulent activity occurs.

- Use a monitoring service to stay informed of any changes.

When you have three reporting payments, this gives you an 80 Paydex score, which is the ideal business credit score. However, specific lenders may have unique qualifying requirements.

Recommended: Nav Review: A Tool that Helps Build Up Your Business Credit Score

9. Apply for Business Credit

When you have your perfect Paydex score (80), you’re ready to apply for business credit. You can start with store cards, revolving cash credit, or credit cards. Let’s take a quick look at each.

How to apply for business store credit:

- To obtain revolving credit at popular stores like Best Buy, Amazon, Walmart, Target, and Staples, establish a business credit profile with at least a D&B and Experian score and at least five reported payment experiences.

- Contact the store directly to learn how to apply, research their approval requirements, and complete the application without including your social security number.

- Use your newly established business credit accounts to purchase products and timely pay bills while monitoring your credit reports.

- Establish at least ten reported payment experiences, including vendor and revolving credit, to start getting approved for more cash credit.

How to secure revolving cash credit:

- Establish a business credit profile with at least a D&B and Experian score and at least ten payment experiences, including at least one reported account with a $10,000 high limit.

- Locate cash credit sources and complete the business application form without including your social security number.

- Use your new credit to purchase items and timely pay bills to increase your business credit score.

- Monitor your credit reports to ensure your new accounts are reporting.

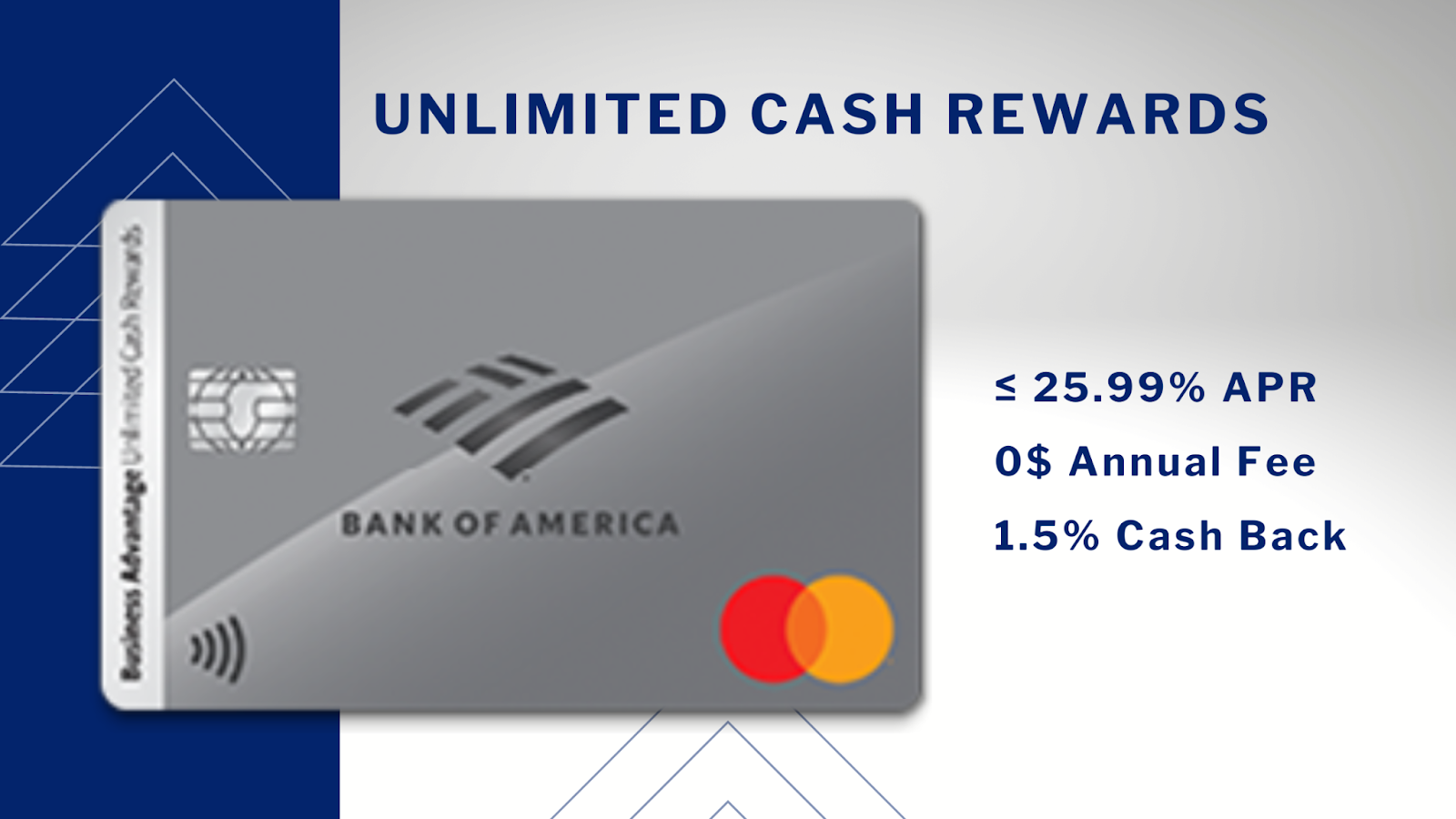

How to use a business credit card:

- Pay your business credit card on time to boost your business credit scores and improve overall creditworthiness.

- Note that some business credit cards may report to the owner’s personal credit reports with all activity or just negative activity in the case of unpaid bills.

- Before applying for a small business credit card, ensure you have good personal credit scores and sufficient income from all sources.

- Review credit card offers carefully as terms and rewards vary widely.

- Determine whether to issue business credit cards to employees to help with expense reporting and segregating business expenses.

- Connect the tradeline to your business account and use it to pay the credit card bill.

By following these steps, businesses can establish a credit profile and obtain business credit. Establishing payment experiences for revolving and cash credit, researching approval requirements, and monitoring credit reports regularly are key to building and maintaining business credit. Using a business credit card can also be an effective tool to manage expenses and improve credit scores.

Recommended: What are the Best Unsecured Business Credit Cards for Startups?

Asking for Help is Not a Sign of Weakness

Building business credit can be complex and overwhelming, but it’s essential for the success of your business. Remember that asking for help is not a sign of weakness. Resources and experts are available to guide you through the process and help you establish strong credit for your business. With guidance from people with experience, you can navigate the complexities of building business credit and take your business to the next level.

If you want to learn how to obtain up to $100K in business credit in as few as 30 days, join Business Credit Workshop today.