In the past, we’ve reviewed business funding offers from Fundbox, Lendio, and Kabbage. Until now, OnDeck (a company with a similar offer) has somehow slipped through the cracks. It’s vital for business owners who seek funding to know about all of their options. So, I want to provide a breakdown of OnDeck’s business lines of credit and term loans.

Here, I’ll share everything you need to know about the offers from OnDeck so that you can decide if this is the right option for your business funding needs.

Here’s what’s “in the hole:”

Now, batter up!

What is OnDeck?

OnDeck is a small business lending company that promises to make the process fast and easy. The company has an A+ BBB rating, and has funded $14 billion to small business owners in the U.S., and they have a 4.8 TrustScore on TrustPilot. In a nutshell, they provide what seem like trusted term loans and lines of credit.

So, are they legit? Let’s find out!

OnDeck Term Loans

OnDeck’s core offer is a term loan for small businesses. Term loans are set-amount, fixed-rate, loans with specific repayment schedules.

Here, you can get $5K to $250K loans with up to 24-month repayment terms. Automatic payments for an OnDeck term loan will be made daily or weekly.

OnDeck Lines of Credit

The secondary offer from OnDeck is a line of credit. Lines of credit are a pre-set borrowing limit with revolving terms that can be used at any time.

Here, you can get $6K to $100K lines of credit with 12-month repayment terms. Automatic payments for an OnDeck line of credit will be made weekly.

OnDeck Requirements

As with most business funding options, you will need to meet minimum requirements to successfully obtain funding. With OnDeck, you must have at least one year in business, a consumer FICO score of at least 625, $100K annual business revenue, and a business bank account.

Next, you must also operate outside of OnDeck’s list of restricted industries. Any business in the following industries are prohibited from obtaining funding through the platform:

- Adult entertainment

- Drug dispensaries

- Firearms vendors

- Government

- Non-profit and civic organizations

- Public administration

- Horoscopes and fortune telling

- Lotteries, casinos, and gambling

- Gaming

- Money service businesses

- Rooming and boarding houses

Finally, funding through OnDeck is unavailable in Nevada, North Dakota, or South Dakota.

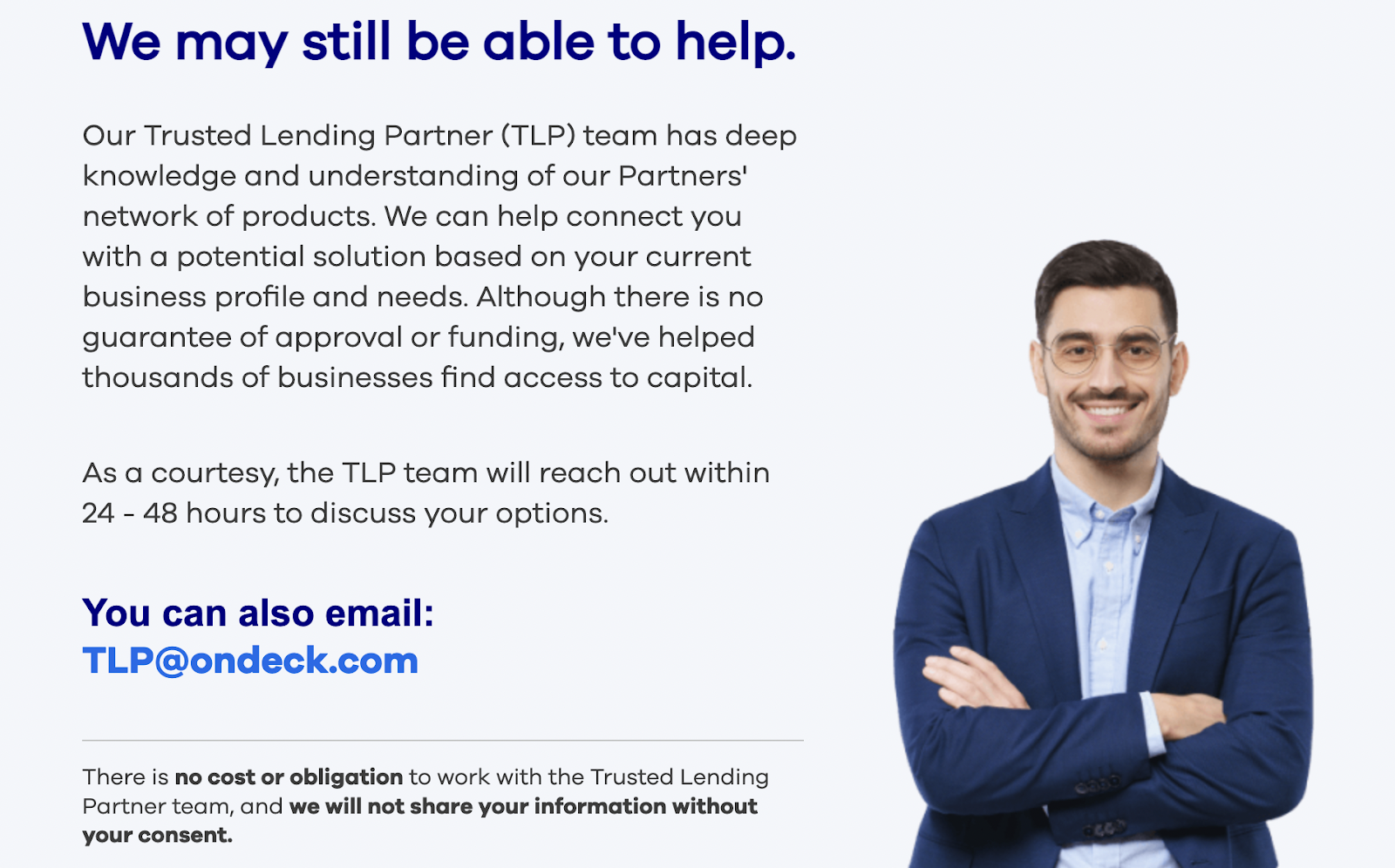

When the minimum requirements are not met, anyone who applies through the platform will be referred out to OnDeck’s Trusted Lending Partner team.

OnDeck Interest Rates & Fees

I have said this before, but I can’t say it enough. ALWAYS read the fine print.

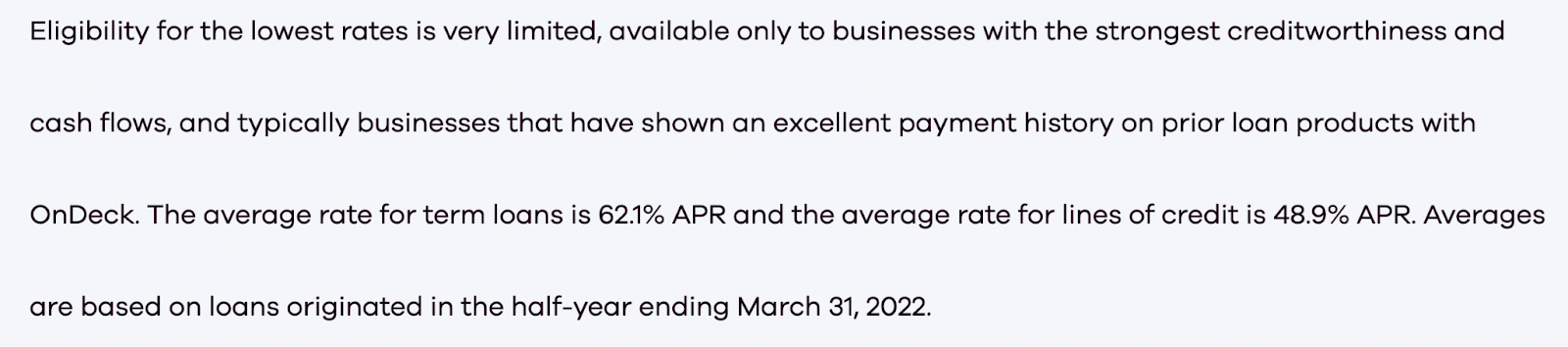

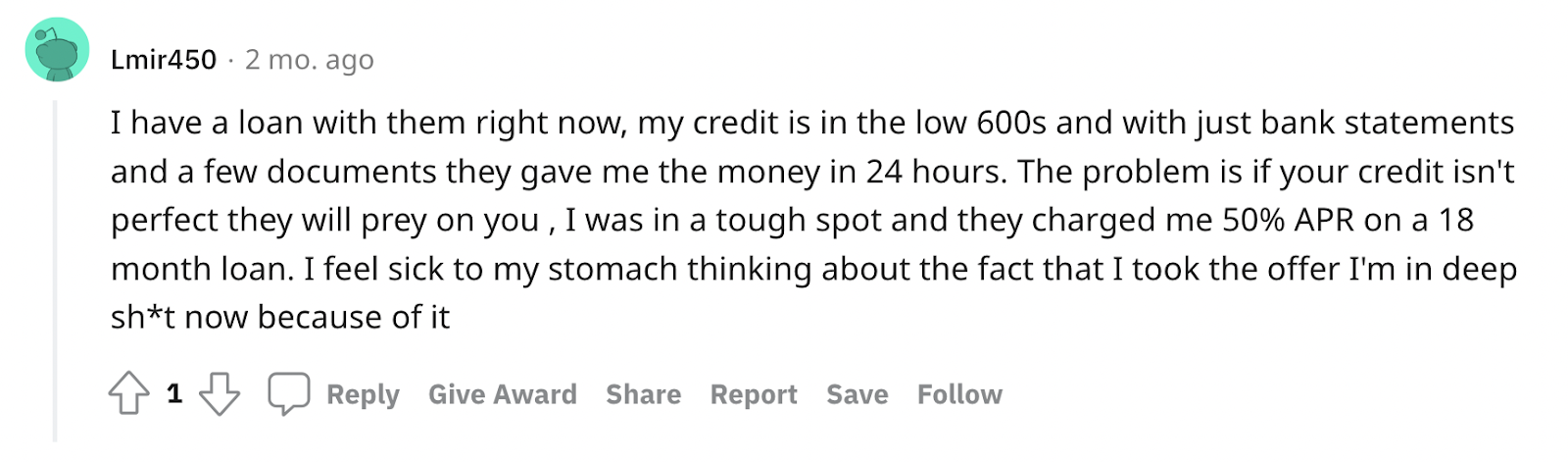

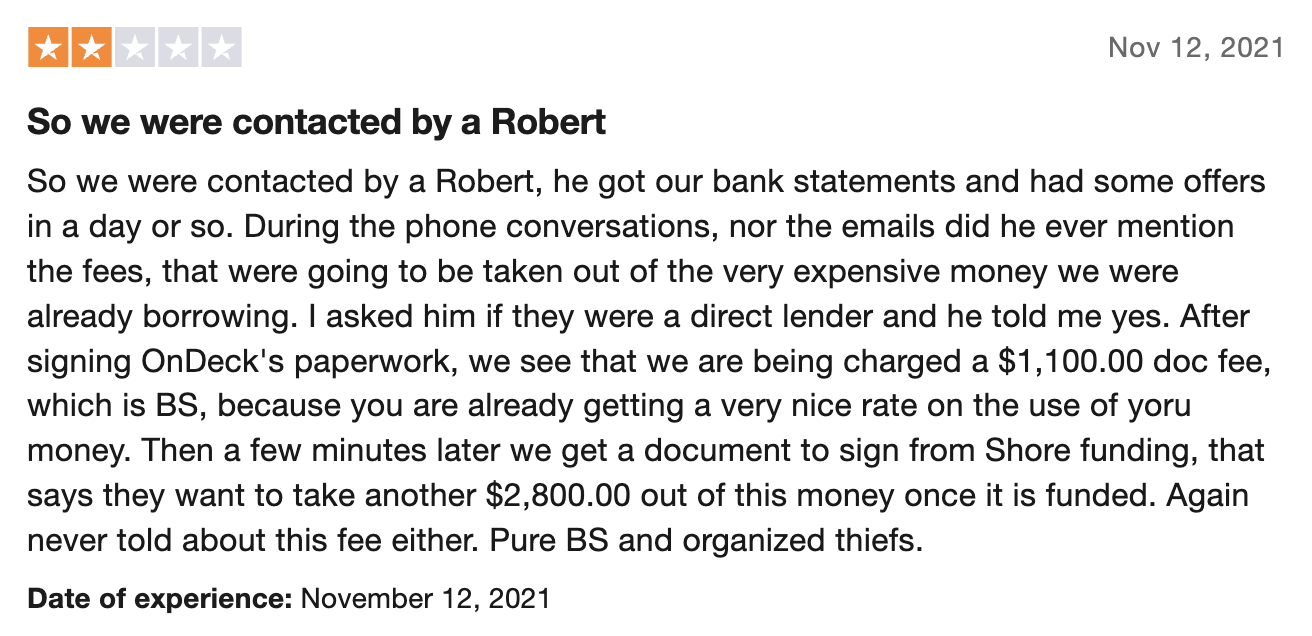

The average rate for OnDeck’s term loans is 62.1% APR and 48.9% APR for lines of credit (ouch!). This means that if you carry a balance, you’ll be paying a ton of interest, and could get yourself into trouble if you’re not careful.

Let me break this down assuming 50% interest on a $100K, 12-month OnDeck loan: Your monthly payment would be approximately $10,309.82 and your total interest would be $23,717.90 at the end of the year.

This is without considering fees, which, according to several sources, are not disclosed until closing, and can run in the thousands of dollars.

I think that if you have the revenue to qualify, you would be much better off looking into a free corporate credit card from Stripe, Torpago, Ramp, Divy, or Brex. And, if you aren’t there yet, you would do well to build your business credit.

Recommended: 41 Companies That Help Build Business Credit

What to Expect When You Apply with OnDeck

If you choose to apply for funding with OnDeck, the first thing you’ll be asked is how much funding you think you need. If your needs fall within the $5K to $250K range, there might be an offer for you here.

Next, they want to know how soon you need the funding. If you have 72 hours or you are looking for funding a month out, this will help determine how the company proceeds with your application.

Then, they need to know what you need the money for. You’ll be provided with a space to describe how you will use any funds you obtain.

From there, you’ll share your contact information with OnDeck and choose a password to create an account. You may be asked to enter a referral code (this will ensure that the person who referred you gets any bonus or incentive that they’re entitled to). So far in the process, the application process is simple.

After that, you will need to share information about your business: legal entity name, address, phone number, EIN, gross annual revenue, and average bank balance. Finally, you will be asked to enter identifiable info about yourself, including your social security number (which lets me know they may do a hard pull to your personal credit. Update: We have been told by OnDeck that they do soft pulls, even after approval, but please verify this information).

When you submit your application, OnDeck will immediately analyze the information you submitted, and attempt to make a pre-approval decision.

Once pre-approved, be prepared to submit documentation to complete the loan process. Then, you can receive your funds or credit line within as few as 24 hours. Then, after 6 months or so of on-time payments, you may be able to refinance your loan for a lower rate.

And, if you run into financial troubles, you will be required to pay your loan, possibly without much flexibility (this should be expected with most business financial offers, though some lenders will give you some grace).

OnDeck Partners

The OnDeck Trusted Lending Partner team can be reached via email at tlp@ondeck.com at any time. But, an unsuccessful applicant will be contacted within 48 hours with offers from partners. OnDeck promises that they do not share your information with partners before asking for your consent.

So, who is in the partner lineup?

OnDeck has two types of partners: editorial and financial.

Editorial partners are essentially affiliates. Anyone with a captive small business audience that might benefit from OnDeck’s offer may inquire.

Financial partners are sales organizations or direct lenders who want to receive customer referrals from OnDeck. In exchange, OnDeck receives a referral fee. Lending partners must have been in business for at least two years, offer at least $1M in monthly business funding, have a functional, encrypted website, active business insurance, and be based in the United States.

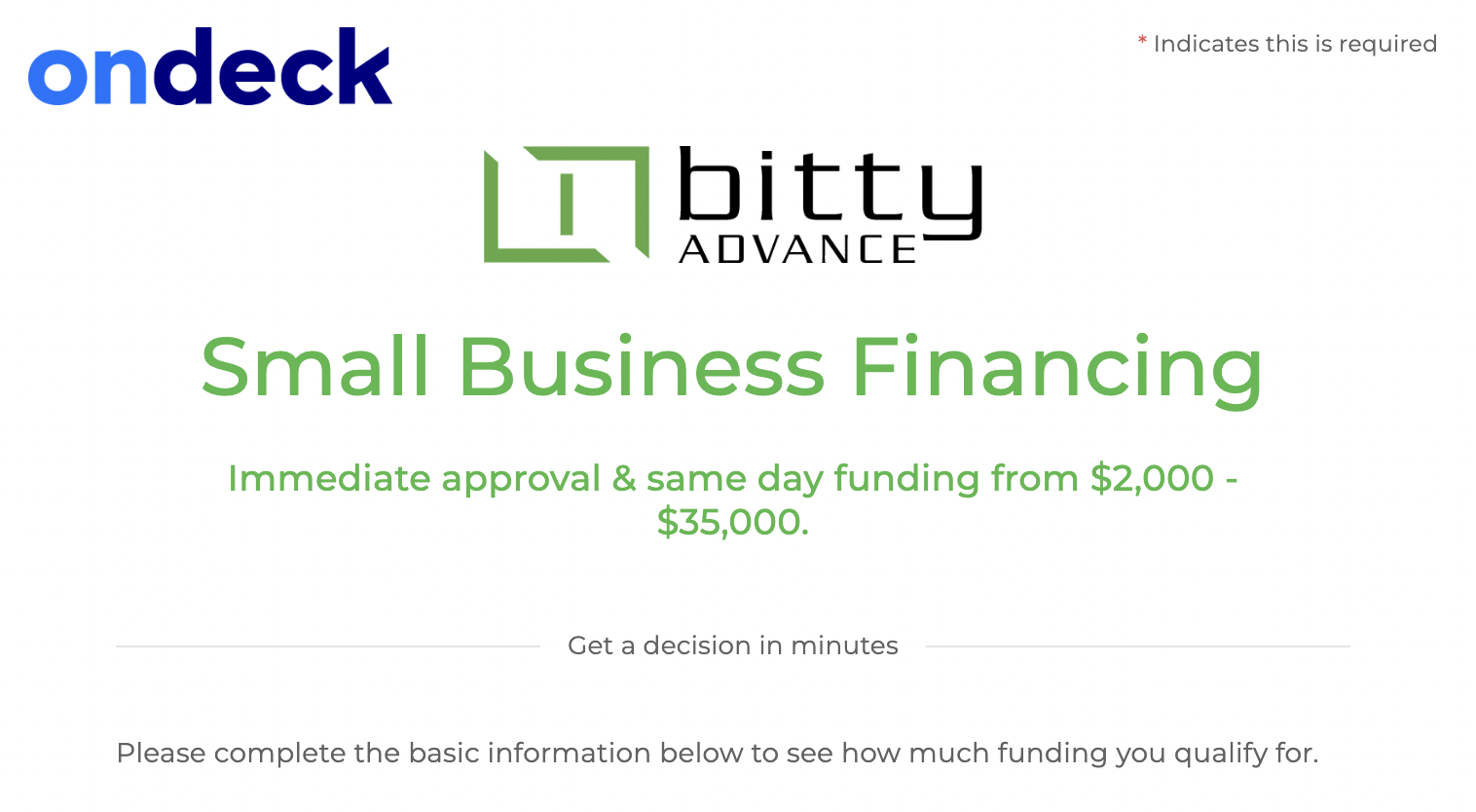

Currently, OnDeck is referring applicants whose businesses are too young for internal financing to BitttyAdvance, who works with businesses as young as 6 months. They do require at least 3 months of business bank statements, a personal credit score of 450 or higher, and at least $5K in monthly business revenue.

BittyAdvance offers instant approval and next-day funding, and they have a good TrustPilot score. Before you apply, please do your due diligence — I haven’t had the chance to fully explore this offer yet, and can’t say whether or not I recommend it.

Note: OnDeck also has programs in Australia and Canada.

OnDeck Company Overview

Originally located in the greater New York area, OnDeck Capital Inc. was founded in 2006 by Mitch Jacobs, the founder and current CEO of Plink.

In July 2020, the OnDeck was acquired by Enova International, the company that purchased Pangea Monay Transfer in 2021. OnDeck’s home base is now in Chicago. The current CEO is Joe Coughlin.

OnDeck is a publicly-traded company, and they’ve received a total of $1.2 billion in funding since launch. I would say they are here to stay.

Frequently Asked Questions

Is OnDeck still in business?

Yes, OnDeck was acquired in 2020, and they are still very much in business.

Who owns OnDeck?

OnDeck is now owned by Enova International and is publicly traded.

Is there a minimum credit score for OnDeck?

Yes, OnDeck requires a minimum FICO score of 625.

What is the maximum amount you can borrow from OnDeck?

The most you can borrow from OnDeck at one time is $250K, in the form of a term loan.

What type of loan is OnDeck?

OnDeck offers both term loans and lines of revolving credit.

What are the terms for OnDeck?

OnDeck’s lines of credit should be paid in full within 12 months, while their term loans vary with repayment terms of up to 24 months.

How does OnDeck make their money?

OnDeck makes money by charging loan fees and interest, with early rates in the 50% range.

For a borrower, what are the benefits of choosing OnDeck?

OnDeck offers fast cash, with funds received within 24 hours. The catch is in the cost.

Does OnDeck conduct credit checks?

Yes, OnDeck asks for a social security number in the loan application and requires a minimum personal FICO score (625) to approve funding.

Does OnDeck require a personal guarantee?

Yes, OnDeck required a personal guarantee. Both the business and the owner are liable for any debts incurred.

Does OnDeck use Plaid?

Yes, OnDeck uses Plaid for read-only access to business bank account information.

The Verdict

Is OnDeck the home run you’re looking for?

To be fair here, OnDeck is a legitimate company that seems to have a ton of happy borrowers — in fact, I know some of them personally. They are transparent with their offer, and they seem to be honest lenders (that in itself is a breath of fresh air). I am not one to turn people away from an offer like this… unless something better is available — in this case, better options might be available.

However, if you won’t qualify for other, more feature-rich business funding options, OnDeck could be exactly what you need to get fast cash flow that helps you grow your business. Just make sure to explore competitors. And, no matter which platform you choose to obtain funding, be sure to do the math before you apply (i.e. How much will a loan actually cost, and can you afford it?).

If you’re interested in learning how you can obtain up to $100K in business credit in as few as 30 days, join Business Credit Workshop today.