Key Takeaways

- Giggle Finance provides up to $5K in fast funding for gig workers.

- Giggle requires no credit checks,= and uses bank account activity to assess eligibility.

- You can set up income-based, automatic repayment for flexible loan management.

- Customer service is digital-only, with mixed reviews on responsiveness.

- Accusations of predatory practices and unauthorized transactions raise red flags.

- Some users value Giggle’s speed and simplicity for emergency financial needs.

Giggle Finance offers something a little different than what we usually review here, but maybe not as different as you might think. Before you apply, you’ll want to know what it is you’re signing up for.

Here, explore what Giggle Finance is, learn more about the company, and understand key features of the offer.

This is what’s in store:

- What is Giggle Finance?

- How Does Giggle Finance Work?

- Frequently Asked Questions

- Conclusion: Is Giggle Finance Legit?

Now, let’s dive in!

What is Giggle Finance?

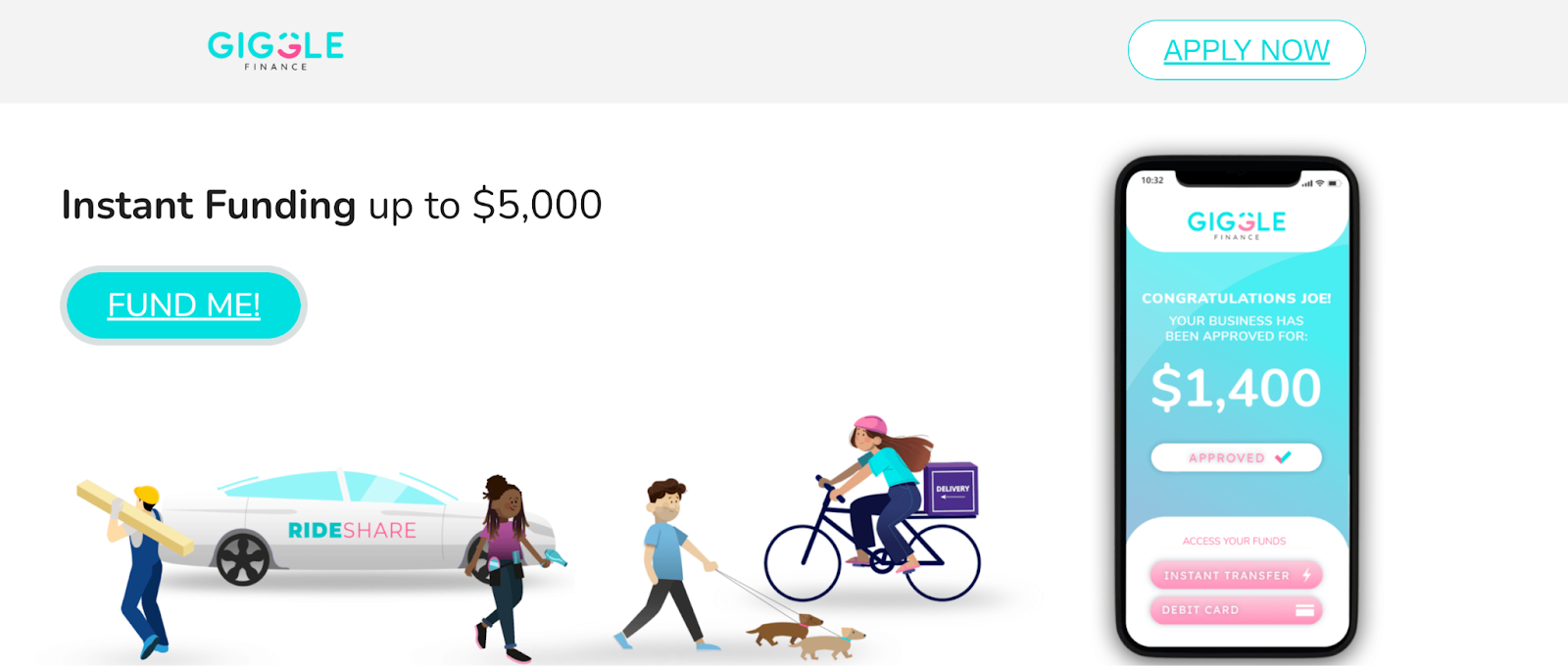

Giggle Finance provides fast and convenient funding solutions designed specifically for:

- Gig workers

- Independent contractors

- Self-employed individuals

They offer up to $5K in instant funding, their platform is fully automated, available 24/7, and requires no credit checks or lengthy application processes.

The idea is that borrowers can access cash quickly to manage unexpected expenses or invest in opportunities. In theory, this can make it a flexible option for those in the gig economy who need immediate financial support.

You might also like: Torro Business Funding Review: Is This “Zero Hassle” Offer Legit?

Company Overview

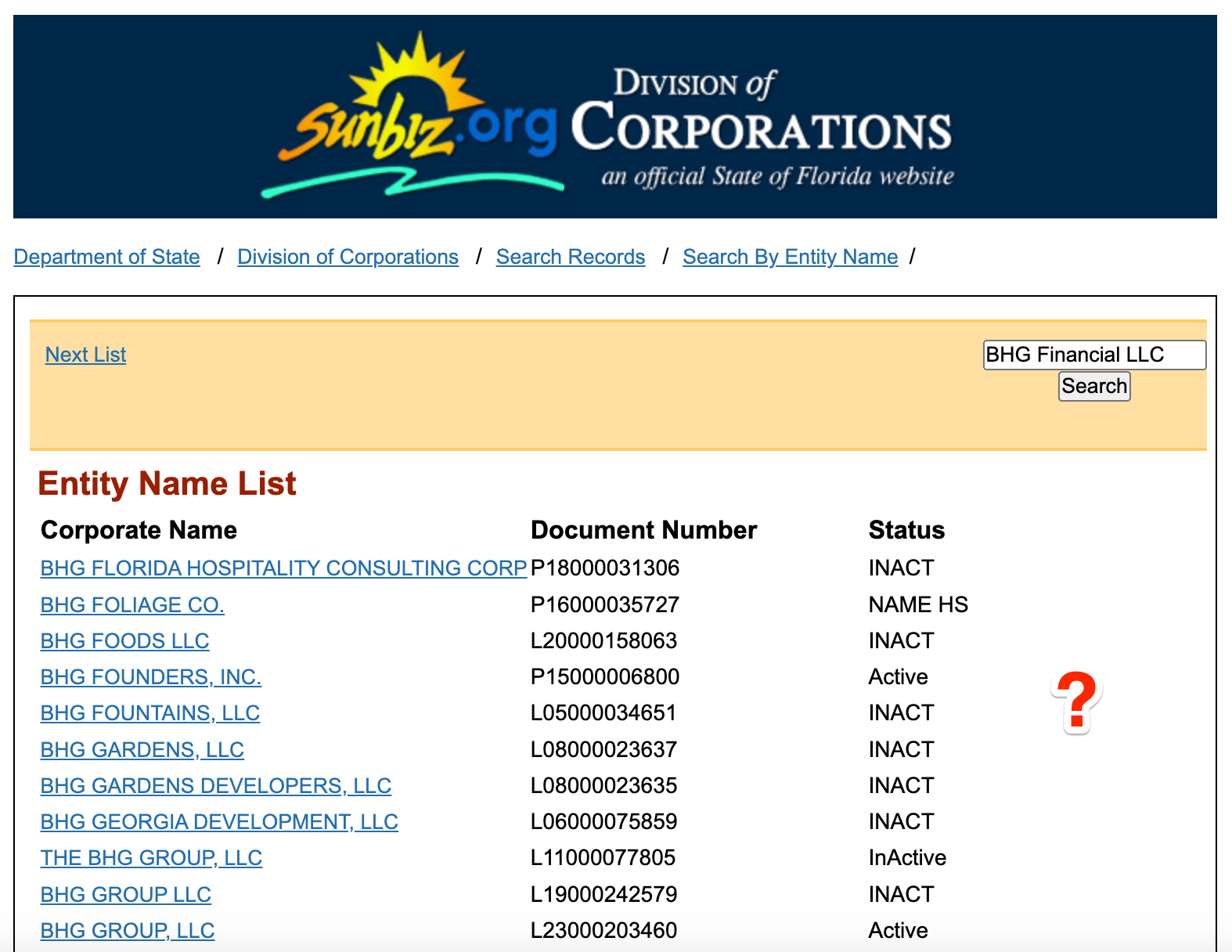

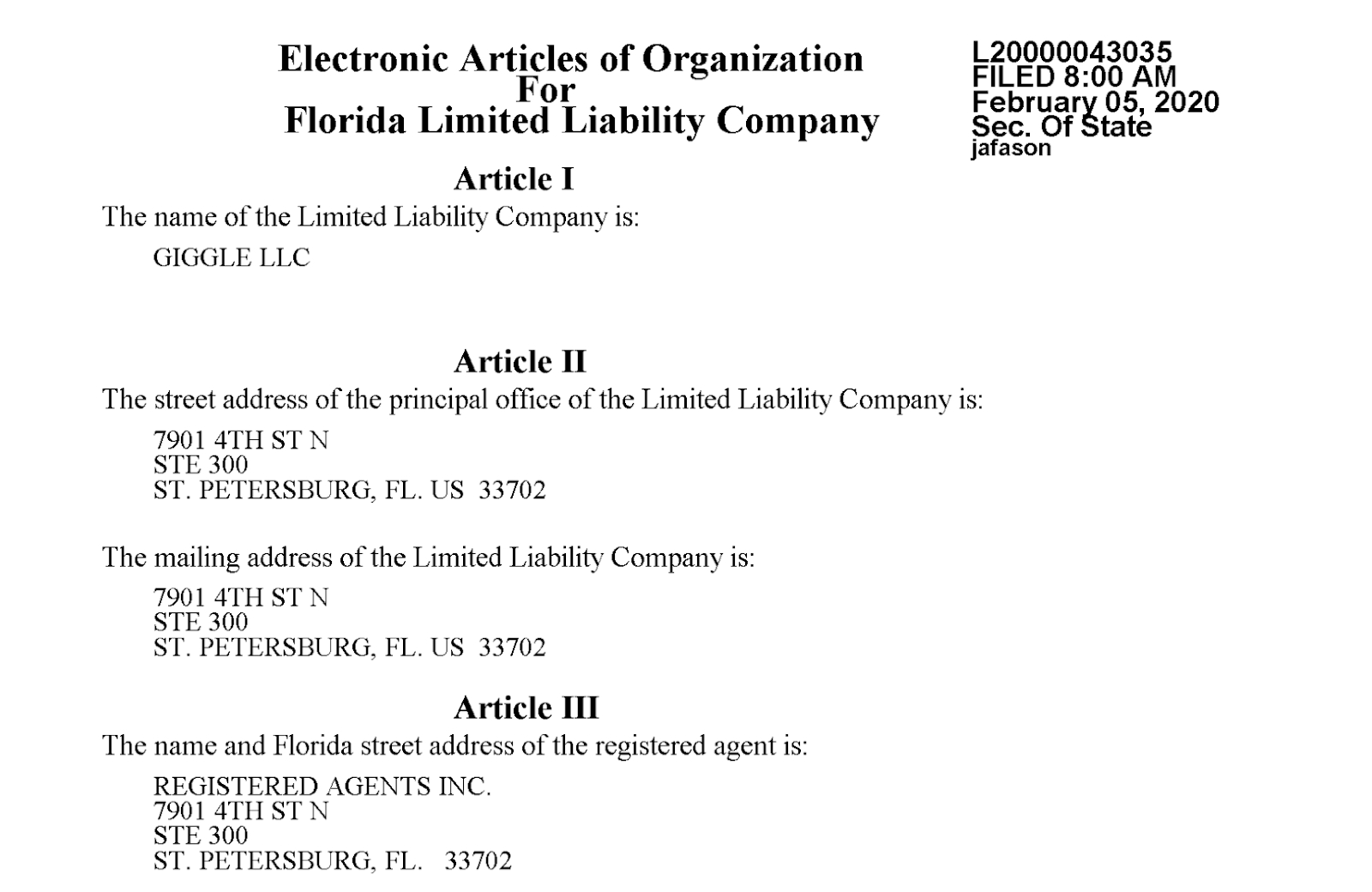

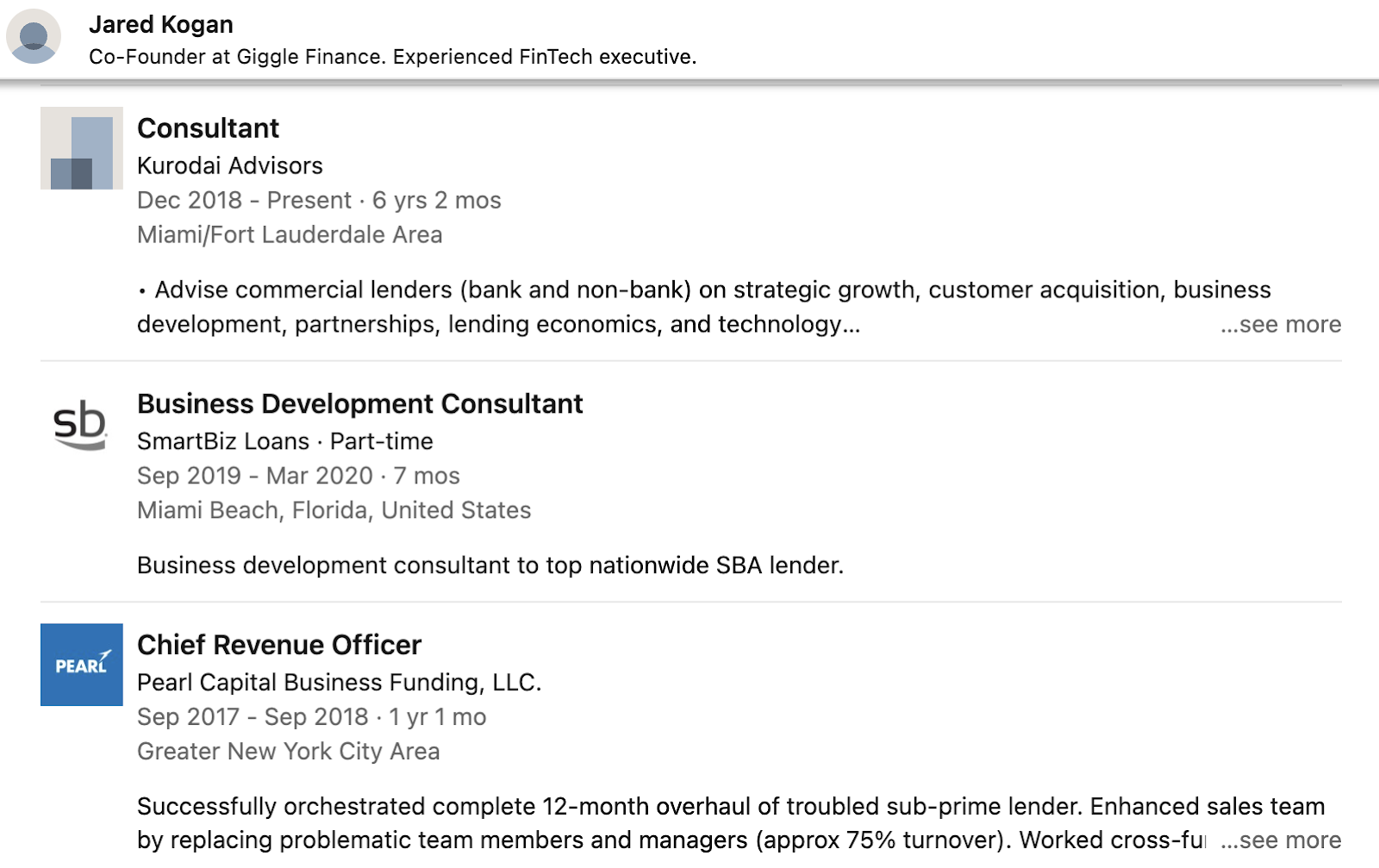

Giggle Finance, aka, Giggle LLC is a Florida-based, private, for-profit financial services entity that was founded in 2020 by Jared Kogan and Michael Zevallos. According to Florida’s SunBiz, the company is active, in good standing, and up-to-date with all their required filings with the state.

Kogen previously spent 5+ years with OnDeck, as the Director of External Sales, and has held several high-level business consulting positions. Zavallos was the Manager of External Sales at OnDeck when Kogen was with the company, and he was the Co-Founder and COO at Idea Financial before the team launched Giggle.

In short, the leadership seems to be solid. However, it’s important to know what borrowers have to say.

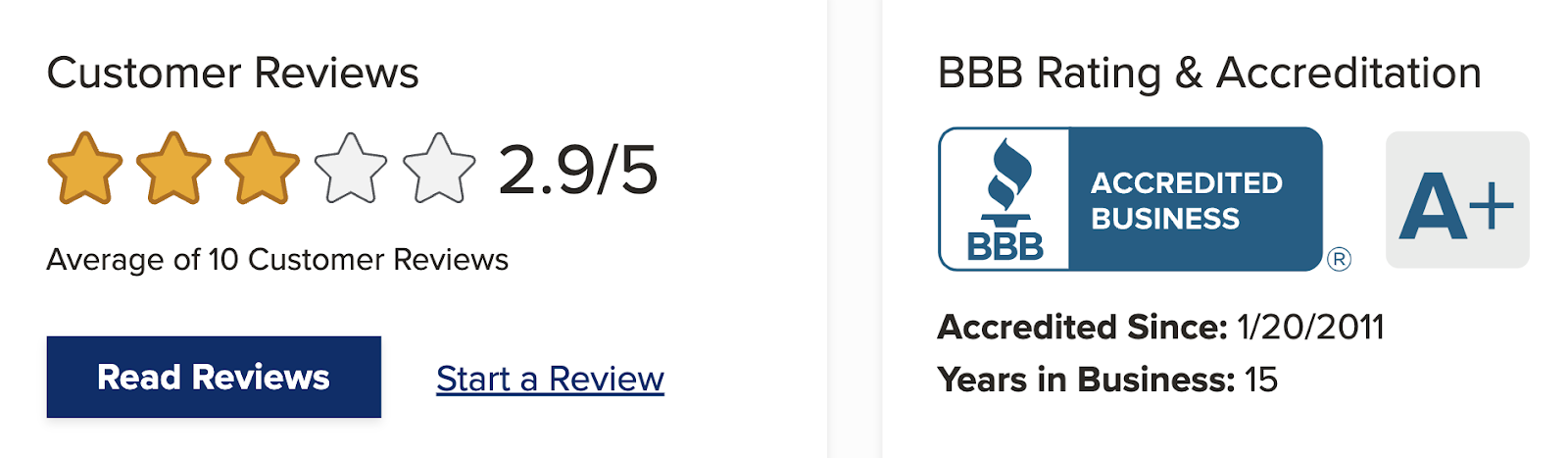

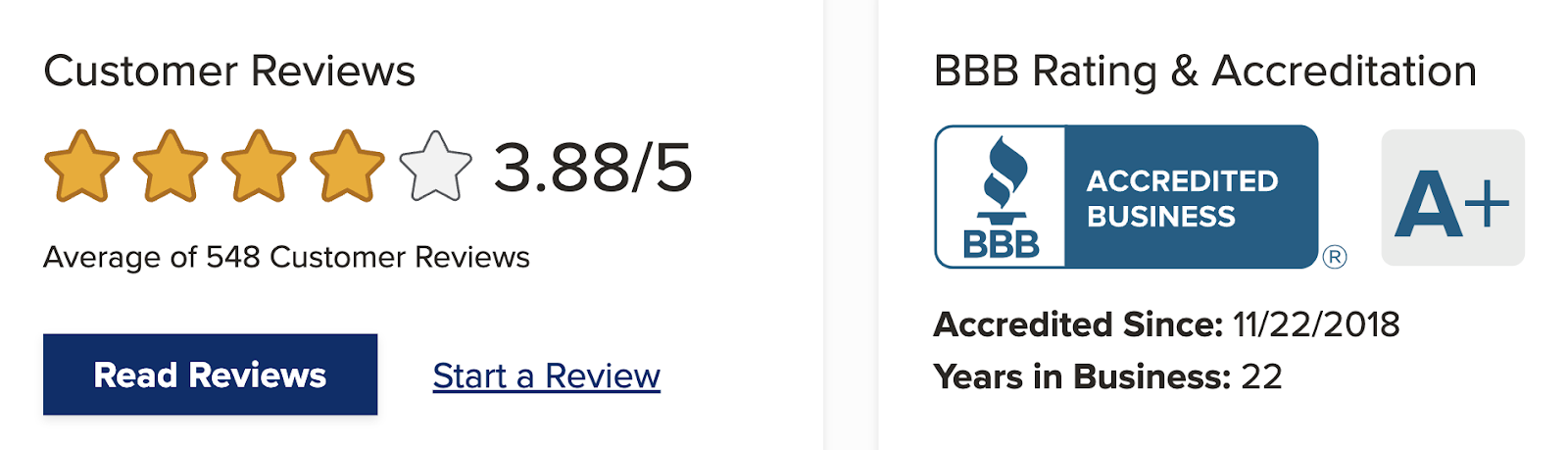

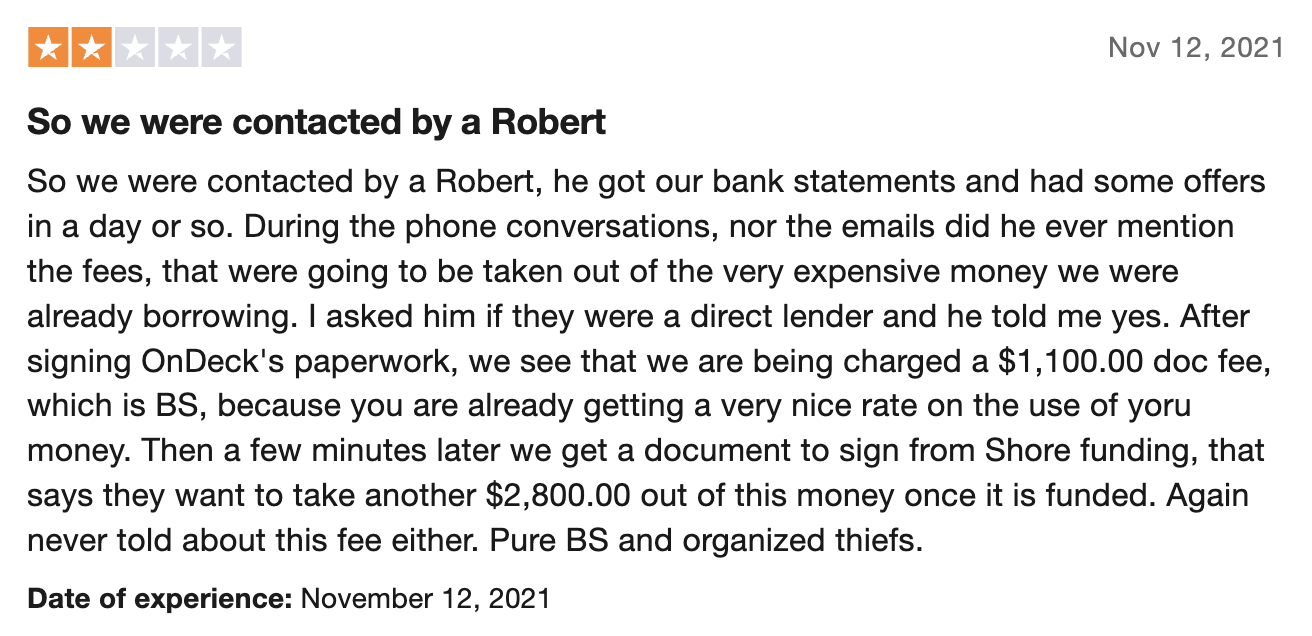

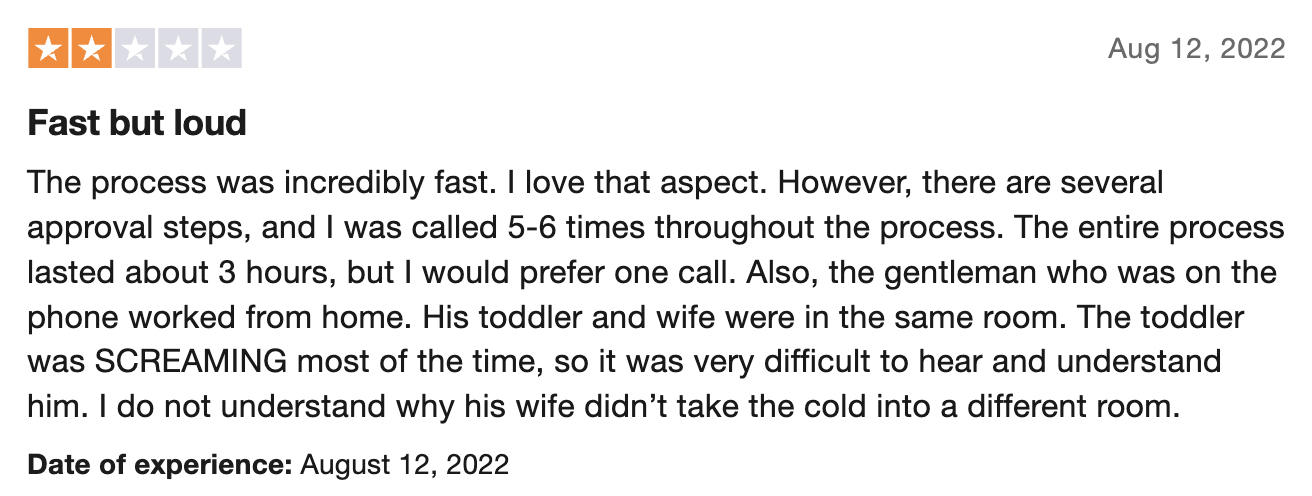

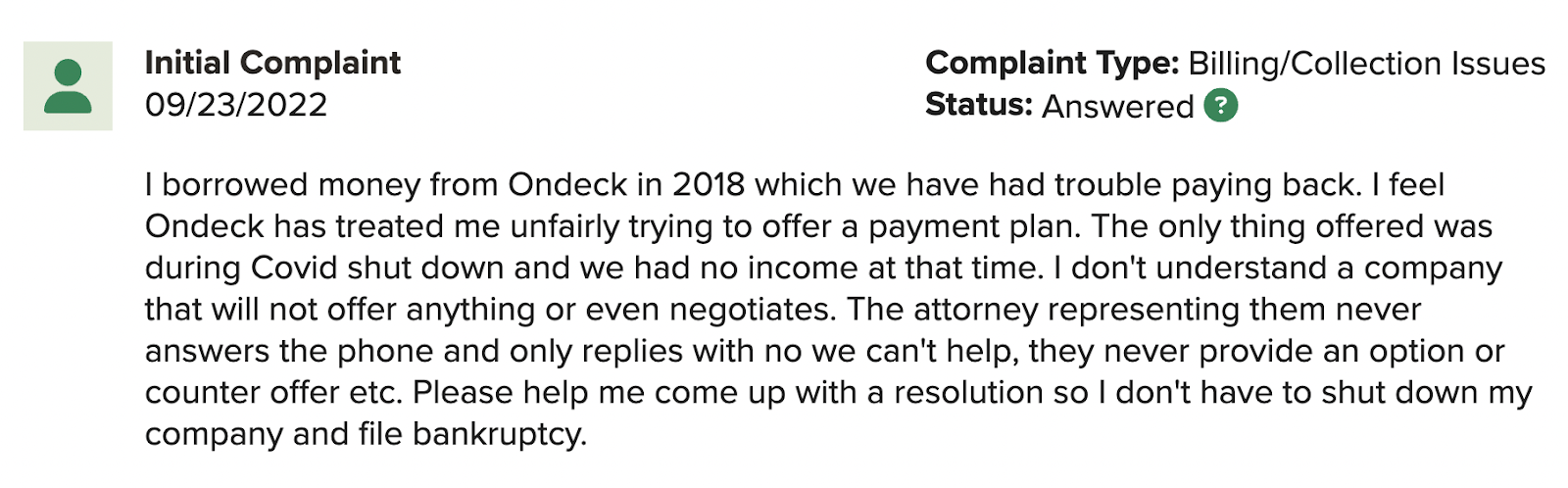

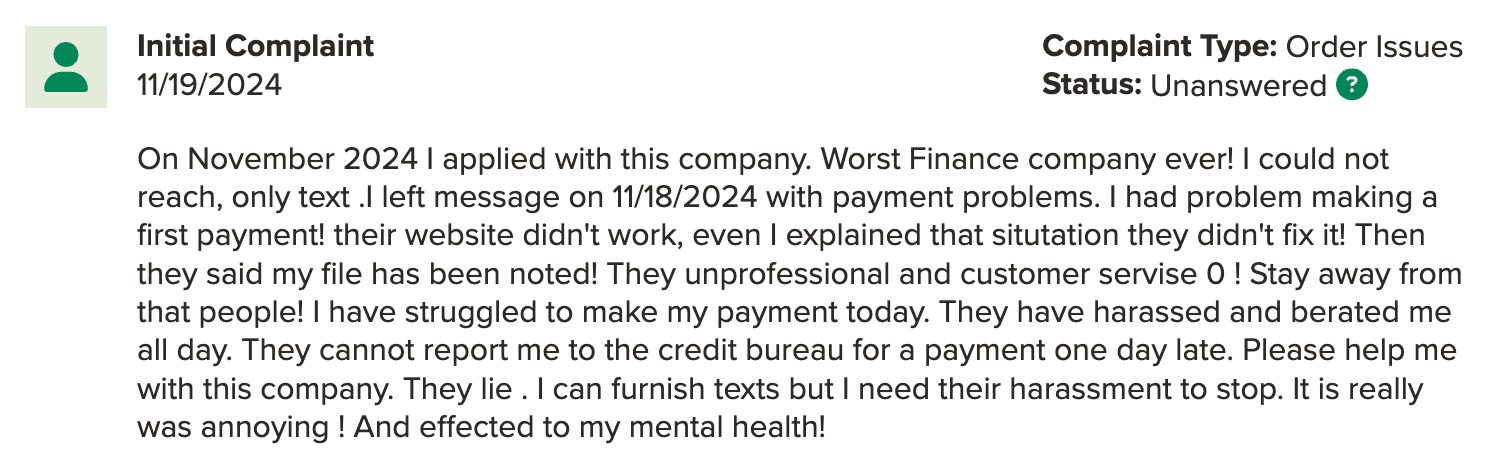

Currently, Giggle isn’t accredited with the Better Business Bureau (BBB), which I would almost let slide—not every legitimate business is accredited. But, they currently have an “F” BBB-rating and have failed to respond to 32 complaints filed on the platform.

Overall, TrustPilot reviews are a little more optimistic, with a 4.0 (out of 5.0) TrustScore.™ Even so, the 1-star reviews are pretty brutal.

All in all, borrowers largely view Giggle Finance as an “unethical” lender, citing:

- Unauthorized transactions

- Predatory practices

- Poor customer service

Though, some people appreciate its fast funding for emergency needs.

These are some pretty weighty accusations, so I wanted to verify whether or not there are any open lawsuits against the company. And, I couldn’t find any current legal issues.

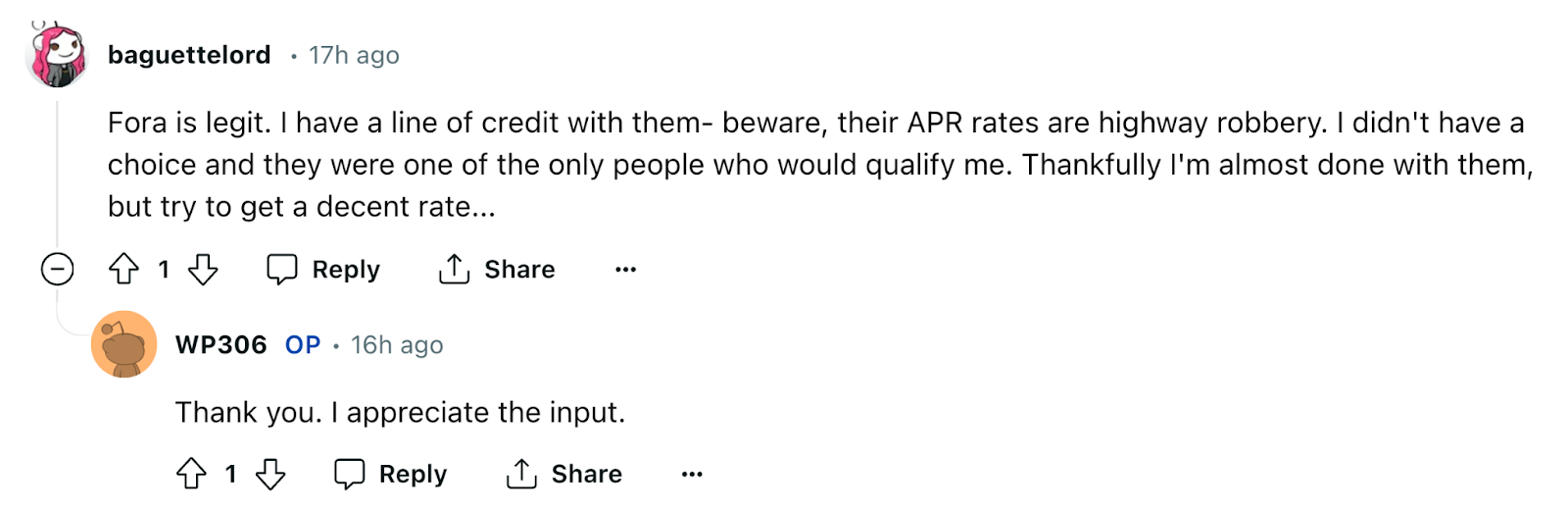

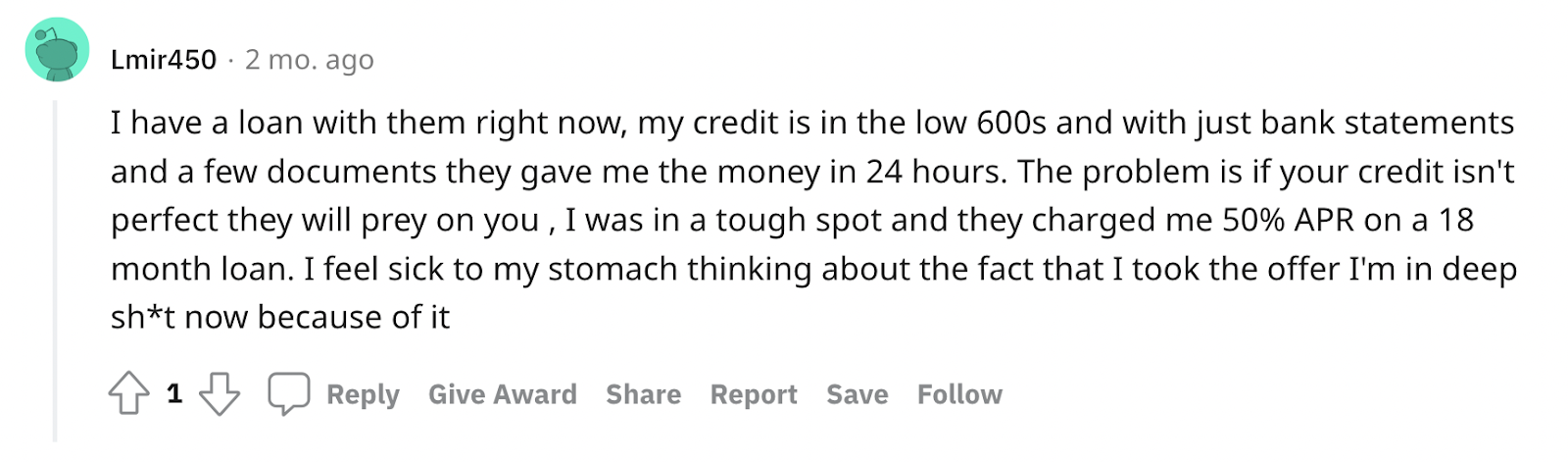

However, Redditors also criticize Giggle Finance as deceptive, warning that its loans involve hidden fees and misrepresented terms, which has caused financial strain for gig workers.

Having no experience borrowing from the company myself, I would have to take others’ word. On one hand, Giggle Finance offers fast funding that some borrowers find helpful in emergencies, while on the other, reviews raise significant red flags.

You might also like: How to Get a Business Credit Card – The Ultimate Guide

How Does Giggle Finance Work?

Giggle Finance offers gig workers and self-employed individuals fast funding options, but borrowers should weigh the potential risks. Here’s how it works.

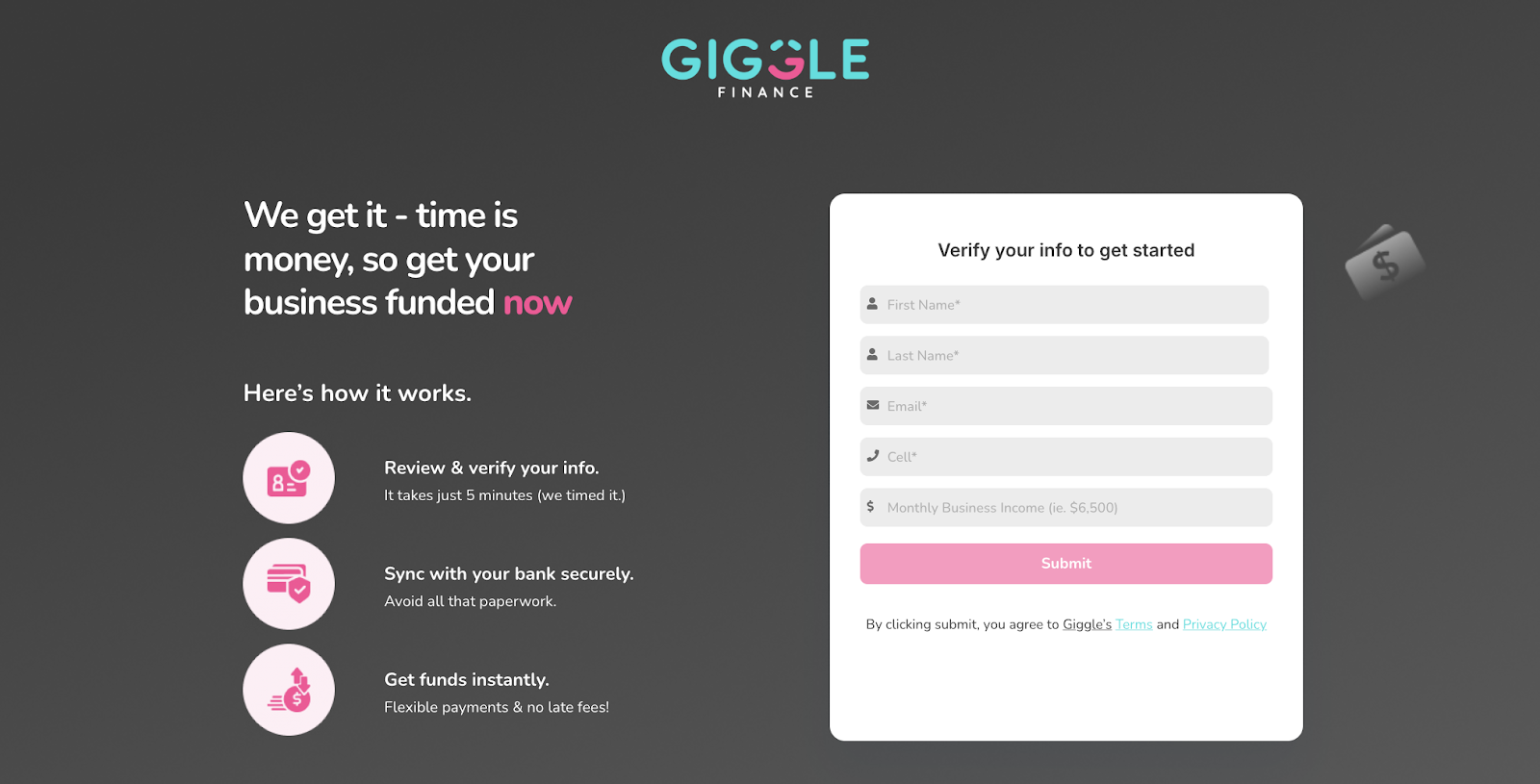

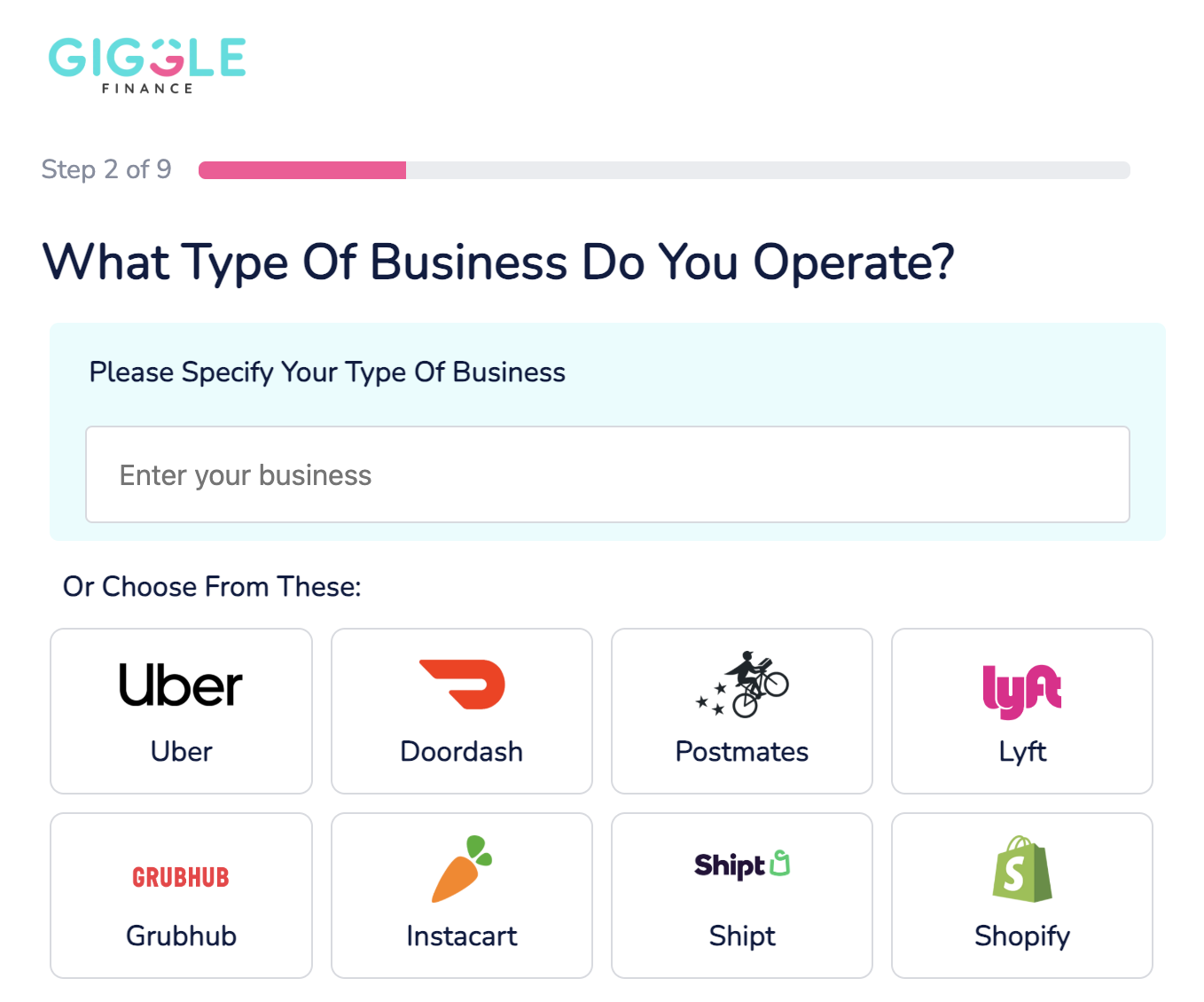

1. Apply Easily Online

The process begins with a quick online application that takes just minutes to complete. By connecting your bank account, Giggle evaluates your eligibility based on income and account activity instead of credit scores.

While convenient, some users have expressed concerns about privacy and the security of their financial data. I know that they work with Plain, which I know to be a secure technology.

If you’re working for a popular delivery service or selling on Shopify, you may be able to connect your account for immediate revenue info (this may be where the data security issue comes in).

You might also like: No-Doc Business Loans: Get Funds Without Proof of Income

2. Get Instant Funding Anytime

Once your application is submitted, the automated system processes approvals in real time, with funds often deposited within minutes. This 24/7 availability is ideal for emergencies.

However, some borrowers have reported delays or discrepancies in the amount funded compared to what was expected.

Recommended: Net 30 for New Business: 13 Vendors +Credit Building Insights

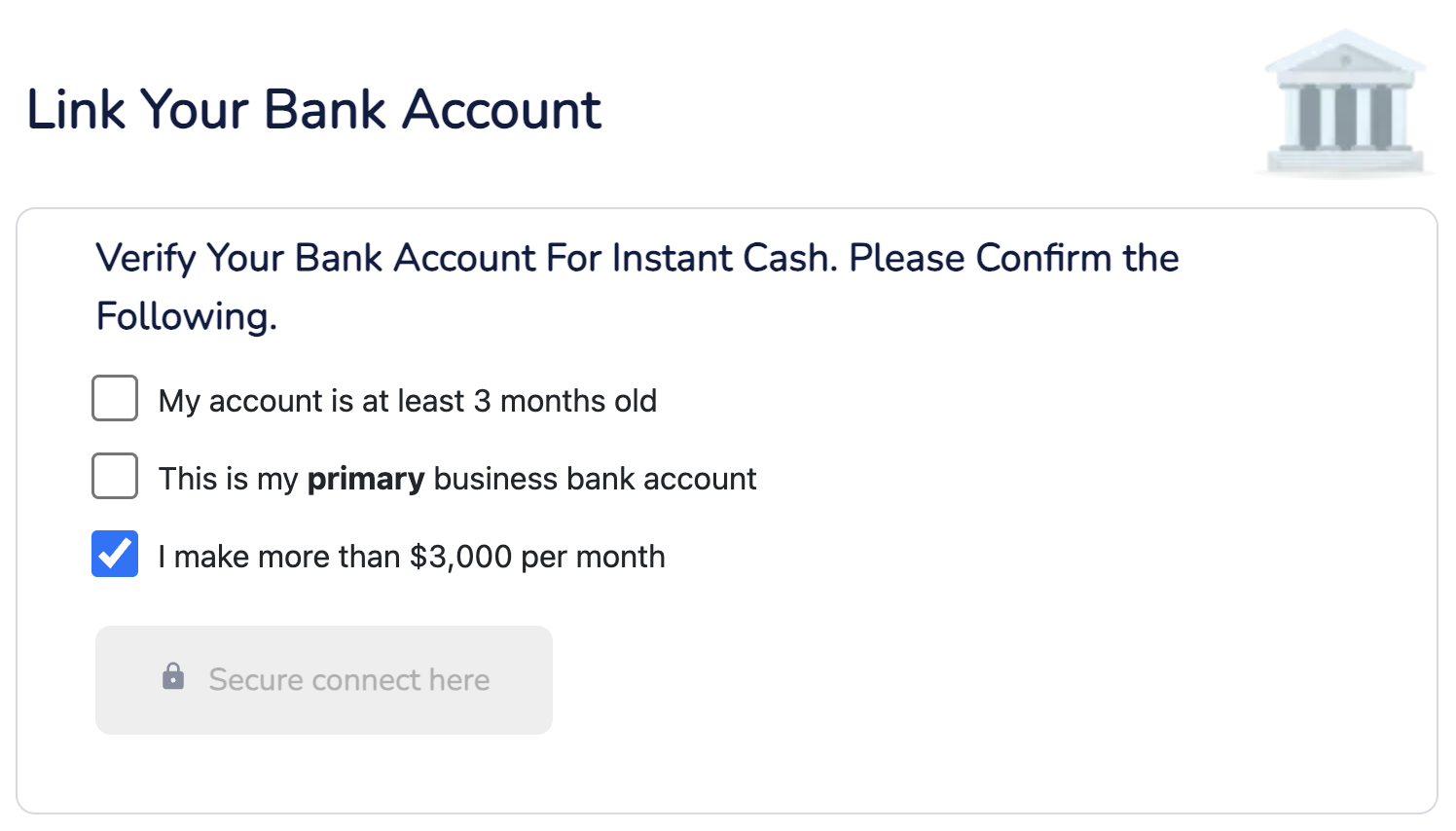

3. Repay Based on Your Income

Repayments are automatically deducted in line with your earnings, offering flexibility for those with variable incomes. Giggle also allows early payoffs to save on fees. Despite this, some users have faced challenges with rigid payment schedules and unexpected deductions.

With this said, you will need to connect the platform to your primary business bank account. They’ll use it for income verification AND repayment.

You might also like: 11 Alternate Ways for Entrepreneurs to Raise Capital with Online Lenders

4. Access Funding Without a Credit Check

Giggle Finance caters specifically to gig workers, freelancers, and independent contractors who may struggle to qualify for traditional loans.

The no-credit-check feature makes the service widely accessible, but the high fees and unclear repayment terms reported by some borrowers warrant a careful review.

You might also like: A Full Skip Review: Business Grants, Funding, and More

5. Know Your Terms Before You Borrow

Giggle Finance determines its fees and repayment terms based on the amount borrowed and the borrower’s risk profile. The company claims to maintain transparency to make sure borrowers understand the total cost before agreeing to the terms, with no hidden fees.

However, some users report higher-than-average fees.

Keep in mind, Giggle calculates repayment amounts using a factor rate, which is a multiplier applied to the borrowed amount. For instance, a $5,000 loan with a factor rate of 1.5 would require $7,500 in total repayment. And, Giggle Finance doesn’t advertise their factor rates (I wish they did).

You might also like: Clover Capital Review: Read This Before You Accept an Offer

6. Be Ready for SMS-Only Customer Support

To verify what some borrowers had said, I tried calling the phone number listed on the website and was redirected by a pre-recorded message instructing me to send a text.

Customer service is entirely digital, with interactions through text or email. Some users have described their experiences as unprofessional or unhelpful, particularly when resolving disputes or addressing errors. But, depending on your preferences, this might be convenient.

Frequently Asked Questions

What credit score do you need for Giggle Finance?

You don’t need a specific credit score to qualify for Giggle Finance. The platform does not rely on traditional credit checks and instead evaluates your eligibility based on your bank account activity and income.

What is the maximum loan amount for Giggle Finance?

The maximum loan amount offered by Giggle Finance is $5K— Your approved amount will depend on your verified income and banking activity.

Does Giggle Finance report to credit bureaus?

Yes, Giggle Finance does report to credit bureaus. This means your repayment activity (including any missed or late payments) can impact your credit score and appear on your credit report. Be mindful of this when you apply for a loan.

Conclusion: Is Giggle Finance Legit?

Giggle Finance provides quick, easy access to cash, which can be invaluable in a pinch. However, recurring complaints (with no responses from the company) about aggressive practices, high costs, and poor communication highlight the importance of understanding the risks before borrowing.

If you carefully review the terms, you can make an informed decision about whether Giggle Finance is the right solution for your needs.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!