You already know that real estate investing is a surefire way to generate a substantial income. And, you’ve been wondering how you can start building a real estate portfolio now so that you can reap the rewards and retire early. Maybe the BRRRR Method is just the springboard you need to reach your goals.

When I first published this post, mortgage rates were at a historical low, and it was one of the best times since the 70’s to hold real estate with financing. Now, we’re faced with much higher rates (though they are decreasing 🎉). So, I’ve updated this post to reflect how to successfully break into real estate investing given the current associated costs.

Today, find out whether BRRRR (Buy, Renovate, Rent, Refinance, Repeat) is the right real estate investment strategy for you, and get ideas to help you profit in today’s market.

Here’s what you’ll learn:

- What is the BRRRR Method?

- Does the BRRRR Method Work?

- This is How to Do the BRRRR Method

- Frequently Asked Questions

- Final Thoughts

Are you intrigued? Good — you should be. Now, keep reading.

What is the BRRRR Method?

Despite how it may sound, the BRRR strategy has nothing to do with the weather – It is an acronym that breaks down a complex real estate investment strategy into five easy-to-digest steps.

- Buy – Purchase a home at a price below market value.

- Renovate – Make renovations to repair or upgrade the home.

- Rent – Rent out the home to establish cash flow/income.

- Refinance – Refinance the home for capital to purchase more property.

- Repeat – Find another home to buy and repeat the process.

Using this method, investors can purchase real estate to build out their investment portfolios. Here’s everything you need to know to implement the system for yourself.

You might also like: Can You Pay a Mortgage with a Credit Card?

Does the BRRRR Method Work?

Yes, the buy, renovate, rent, refinance, and repeat strategy is a legitimate and lucrative way to invest in and profit from the real estate market. Many people use it to start or expand their holding portfolio or to generate cash flow.

In fact, BRRRR has been used since before there was an acronym for it. And, if you check out Reddit or Quora, you’ll find countless anecdotes from countless investors who have successfully used the method to generate cash flow.

However, don’t expect thousands in monthly profits for a single property. After the cost of repairs and considering vacancy rates, you are more likely to be looking at $100 to $300 per month in profits per unit or property.

How Does the BRRRR Method Work?

The BRRRR method works by enabling you to leverage property you purchase to pay for new real estate and grow your portfolio.

Moreover, this strategy can be altered based on your financial situation and personal preferences. Moreover, rather than buy, renovate, rent, refinance, then repeat, you may choose to go another route.

Some investors opt for slightly different strategies:

- BRRSR (buy, renovate, rent, sell, repeat) or “buy and sell”

- BRRHR (buy, renovate, rent, hold, repeat) or “buy and hold”

These systems can help you generate hefty returns on your investment, sometimes more profitable over time as you hold.

Furthermore, BRRRR doesn’t only work for residential homes – You may opt to buy single or multi-family homes, but commercial real estate is another option. You might even consider investing in land that can be rented for livestock, farming, RV parking, or recreation.

In sum, you can alter the strategy to your liking.

BRRRR Method Risks

As with all investment opportunities, there are perils with the BRRRR method. Costs, value, timeframes, and refinancing details are constantly fluctuating in real estate.

The BRRRR method comes with all of the usual real estate investment risks:

- Financing shortfall on first property

- Unanticipated renovation problems

- Difficulty finding reliable contractors

- Tenant issues or difficulty renting (factor in a 5% vacancy rate when calculating)

- Refinancing falls short of funding next property

- Market fluctuations

- Interest rate changes

- Regulatory changes

- Construction and renovation delays

- Overestimating after repair valueM (ARV)

- Unexpected expenses

- Property management challenges

- Economic downturn

- Liquidity risks

- Market saturation

You need to be aware of and address these risks when implementing the BRRRR method. But, you may have a smooth experience and be impacted by none of these issues. And, the more you understand about the process, the more likely you are to succeed.

Now, let’s take a more in-depth look at each step of the process so you can learn to implement the BRRRR method process.

Recommended: This is How to Leverage Business Credit to Transform Your Life

This is How to Do the BRRRR Method

You already have the basic idea, but real estate investing is not a simple process. Let me give you my best advice for every step of the BRRRR process.

Learn where to find money to purchase property, how to find the best properties, and considerations to make with renovations and renting.

Step 1: Buy a Home at a Price Below Market Value

Before you start on this journey, you need to set your budget. How much money can you invest into your first property? And, this means more than

Keep in mind that you’ll need funding for a handful of items:

- The full cost of the property (for cash payment) or about 20% for a down payment (for a traditional mortgage)

- Closing costs and fees associated with title transfer

- Homeowner insurance and property taxes

- Renovations to the home

- Travel costs if purchasing out of state

- An emergency fund for future home repairs

In determining your budget, here’s where you might be able to get funds:

- Mortgage (most traditional option)

- Personal loans

- Personal savings

- Partnerships

- Private investors

- Seller financing

- Business credit cards

- Self-directed IRA withdrawal

- Government grants or programs (rare)

- Home Equity Investment Platforms

- Crowdfunding platforms

If you already own property, you could consider Home Equity Line of Credit (HELOC) aka ”home equity loan”, real estate investor line of credit or a cash-out refinance. Since this is your first purchase, I’m assuming you don’t have this option.

Carefully assess risks to choose the most suitable funding option for your BRRRR project, then research market trends to get an understanding of the current market.

You can’t typically just shop Zillow or Trulia and purchase any home to implement this strategy – The key is to purchase property at a price below market value. This means that you need to get a good deal so that you can turn a profit.

So some home purchase situations that might help you get your foot in the door include:

- Auctions and government repossessions

- Bank foreclosures

- Unlisted opportunities

You’ll hear stories of people purchasing homes for as little as $15K. When these anecdotes are sometimes true, any property priced this low was likely picked up at an auction. You never know what the prices will be on these properties. While this is usually where investors find the best deals, auctions are usually cash-only, so you can’t use a mortgage to bid.

| Log in to your Business Credit Workshop account to access a list of five legitimate real estate auction websites. |

Now, the median cost of a foreclosed home is about 15% less than market value, according to Money.com. So, while you may pick up a home for 40-50% less than the average traditional listing (this is a diamond in the rough), foreclosed homes are typically on the lower end of the value scale to start with.

This doesn’t mean foreclosures aren’t worth looking into. Search bank websites for “Real Estate Owned (REO)” pages. Some REO properties are available on conventional listing sites like Zillow®, Trulia®, and Realtor.com®, but the comprehensive lists are more likely to be found with the banks.

And, you’re only going to hear about unlisted opportunities if you get out there and network. Some people think of these as unicorn investments, but they’re very real. Make friends with real estate professionals and stay open to opportunities.

Here are the places you can look to find legitimate real estate auctions:

[Login to your Business Credit Workshop account for a directory of legitimate real estate auction websites in the US.]

Recommended: How to Raise Money for Real Estate Investment: A Beginner’s Guide

Step 2: Renovate to Make Repairs or Update the Home

Once you’ve purchased a home and it’s in your possession, it’s time to renovate. You will take a chunk of cash, say $10-20K, and put it back into the home. If the home needs repairs, start there.

You need the house to be “habitable” according to the state’s housing standards. And, some updates can instantly increase the value of the home, giving you a chance to rent it for a higher price.

Here are some of the most valuable uses of your money:

- Increase curb appeal with landscaping

- Fence in the yard or update the fencing

- Upgrade the front door

- Paint the exterior and interior

- Add new carpet or refinish flooring

- Update fixtures, switches, and outlets

- Add shutters or curtains or replace windows

- Get a new garage door

- Replace old countertops

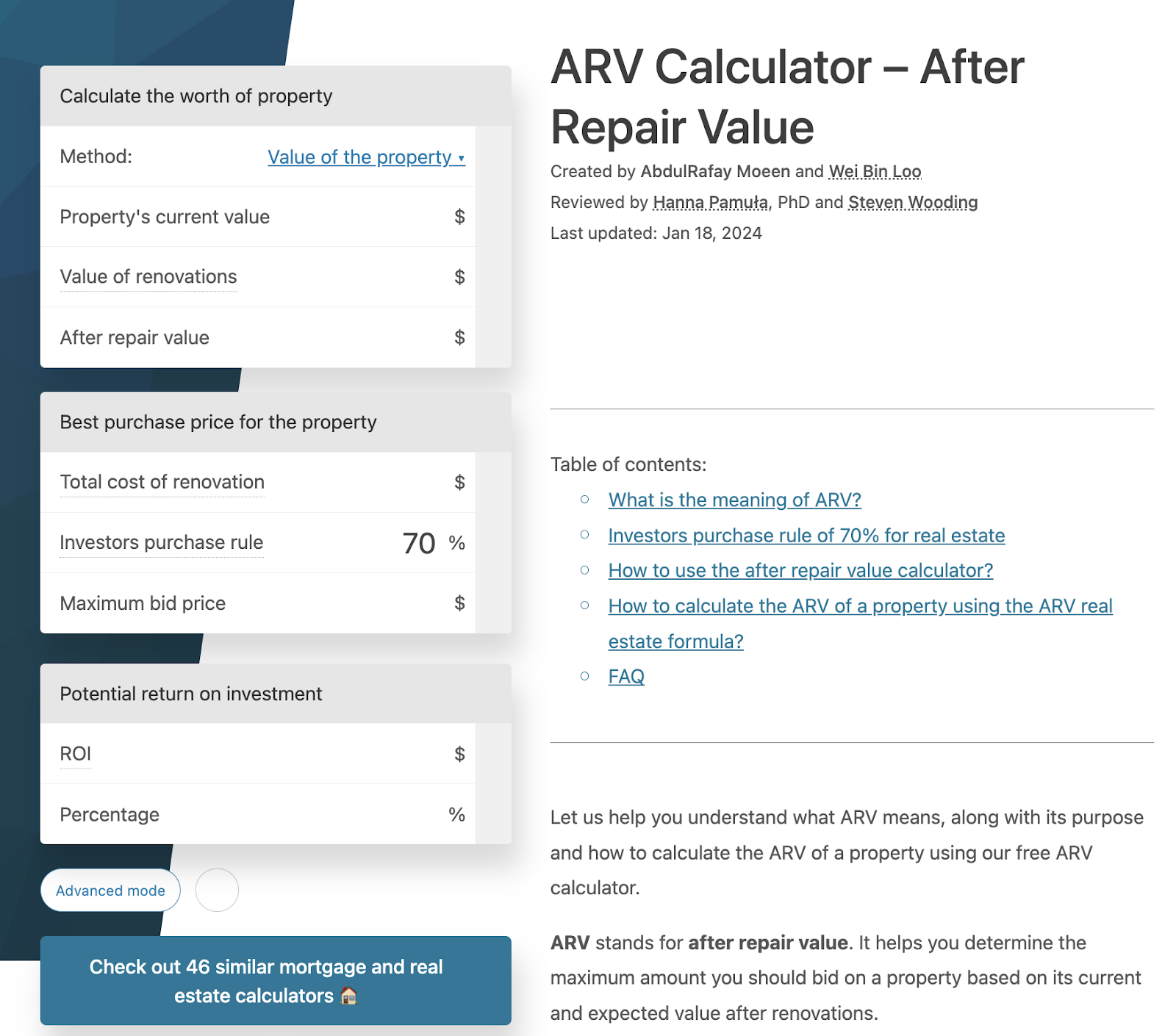

Omnicalculator® has a handy after-renovation value (ARV) calculator that might help you determine which repairs or updates can help you get the most bang for your buck.

If the home you purchase is already in excellent condition, you could get into some eco-friendly updates like alternative energy or luxury add-ons like jacuzzi bathtubs. But, keep in mind that you will not be living in the home and the more you provide, the more you will be required to help maintain.

And, sometimes the simplest fixes (painting the cabinets or the bathroom tile) can have the most impact on home value for the lowest cost. So, as a landlord, it’s typically best to keep it simple.

You might also like: Best Credit Cards for House Flippers: The Ultimate Guide

Step 3: Rent Out Your Property to Generate Cash Flow

Now, you have another decision to make: Will you act as a landlord or hire a property management company to rent your home? Depending on where you live, property management might cost $100-150 or around 10% of the monthly rental price.

For this monthly fee, someone else will do the following tasks:

- Price your rent

- Advertise your home

- Find a tenant to live in your home

- Protect you from lawsuits

- Manage emergency repairs

- Provide tax documents

- Create income and expenditure reports

- Perform house visits/ inspections

You need to rent your home at a price that generates enough cash flow to enable you to easily get refinanced — you must show a profit. So, if the fees associated with outsourcing property management take up most of your cash flow, you may want to manage the home yourself.

If you decide to take matters into your own hands, first and foremost, be sure to update yourself on the landlord-tenant laws in your state – The last thing you want is to end up in a courtroom over a dispute because you’re ill-informed.

Here are some resources to help you learn the ropes:

- State Landlord-Tenant Laws | Nolo

- How Much Should I Charge for Rent? | Zillow

- Advertise Your Rental Property | RentPrep

- How to Screen Potential Tenants | Money Crashers

- How Quickly Must Landlords Make Repairs? | The Balance SMB

- Tips on Rental Real Estate Income, Deductions, and Record-Keeping | IRS

If you make it through the reading list above and you’re still interested in managing your own rentals, then you’re probably good to go. If you decide to hire out, many people consider $100 or 10% of the total home price to be a great deal with everything that goes into the job of managing property.

Recommended: Buildium Property Management Software: An Extensive Review

Step 4: Refinance to Get Funds for Your Next Investment

Now, it’s time for you to get the home refinanced so you can do it again. You want some money for a down payment on your next home. In addition, refinancing can help you out in a couple of other ways. For example, if you already have traditional financing, you may be able to move from a variable to a fixed interest rate. And, you may get rid of an existing PMI for a lower monthly payment. These details should be discussed with your mortgage broker or lender.

If you used low or zero-interest credit cards to fund the home purchase, refinancing can give you the ability to pay them off before your interest rates spike at the end of the introductory period.

Ultimately, to qualify for refinancing, you’ll need to be in a good financial situation and have the documents to prove it. Before you submit an application for refinancing on your rental, you need to be able to show that you have the ability to pay back the new loan.

You will be asked to prove the following:

- A steady income

- Positive credit standing and FICO score above 620

- At least 25% equity in the home or a 75% loan to value (LTV) ratio

- The payment will be less than 30% of your monthly income

- Your total household debt is less than 40% of your income

In the case that you purchase and refinance the home as a business, the lender may consider your business credit profile.

Once it’s time to apply, you will want to gather the appropriate documents in advance for a quick and smooth process. Your lender will want to see the following:

- Rental lease and proof of rent deposit paid by the tenant

- HOA agreement and payment amount (if applicable)

- Proof of homeowner’s insurance

- Two months of recent pay stubs (if applicable) and bank statements

- Investment and retirement account statements (if applicable)

- Two years of tax returns

- Your current mortgage statement with payment information

- An official payoff amount from your original lender

- Property appraisal documentation

If you gather all of the required documents in advance, you’ll streamline the process. In the instance of any obstacles, your lender or broker will help you learn how to remedy them.

You might also like: Should You Use a Real Estate Investor Line of Credit to Buy or Renovate Property?

Step 5: Repeat the Process!

Now that you’ve made it this far, you’re ready to do it again. When refinancing is complete, you should have enough money to reinvest in a down payment on your second home. Rinse, repeat, then do it a third time. Eventually, you could have enough rental cash flow to live on and even retire early.

Frequently Asked Questions

What is the 70% rule for BRRRR?

The 70% rule in BRRRR suggests that you should aim to buy a property for 70% of its after-repair value (ARV), factoring in purchase, renovation, and holding costs. This leaves room for a profitable exit.

What is the 1% rule in BRRRR?

The 1% rule is a quick guideline in BRRRR, stating that your monthly rental income should ideally be at least 1% of the property’s total cost. It helps assess whether the property has income potential.

Is BRRRR better than flipping?

It depends on your goals. BRRRR focuses on long-term wealth through rental income and appreciation, while flipping aims for quick profits by buying, renovating, and selling. Choose based on your preferences and risk tolerance.

What are the disadvantages of BRRRR?

BRRRR risks include potential financing challenges, renovation setbacks, finding reliable contractors, tenant issues, market fluctuations, and uncertainties in refinancing. Thorough research and planning are crucial.

How many times can you BRRRR in a year?

There’s no strict limit on how many times you can BRRRR in a year. It depends on factors like market conditions, financing availability, and your ability to manage multiple projects efficiently. Quality over quantity is key.

Final Thoughts

The BRRRR method is not a new strategy – it’s simply a way to break down real estate investing into a system that’s easy to remember. As you can see, there’s a lot that goes into investing in real property, and it’s not for the faint of heart.

There are many things that can go wrong, but that goes for all things in life. If you go into it with an optimistic mindset and the commitment to learn, real estate investing can be one of the most viable ventures you’ll ever partake in…Plus, you can start investing with business credit and lay the first brick to build your empire.

Ready to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!