As you build your business credit, you’ll start to see the Small Business Financial Exchange (SBFE) mentioned here and there. It’s probably immediately apparent that they’re involved in business credit data. But, how does this apply to you, as a small business owner?

Here, I’ll break down what the SBFE is, what they do, who they are affiliated with, and how this applies to small business and business credit. And, I’ll answer a couple of the most common questions I hear about the SBFE.

This is what’s in store:

- What is the Small Business Financial Exchange?

- What Companies are Affiliated with the SBFE?

- Frequently Asked Questions

- Conclusion

Now, let’s roll!

What is the Small Business Financial Exchange?

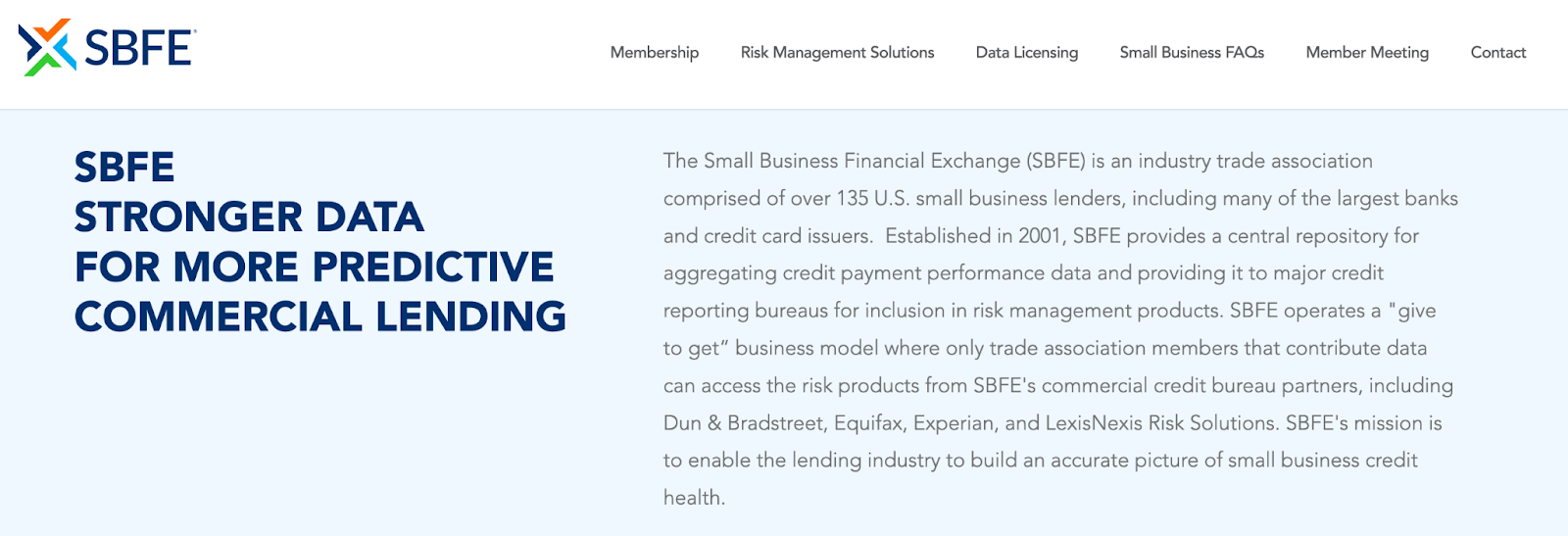

The SBFE is like a guild for over 135 U.S. small business lenders, including big banks, merchant acquirers, and credit card companies. It started in 2001 and gathers info about how businesses pay their bills—This info goes to the major credit reporting companies, helping them figure out how risky it is to lend to businesses.

The goal is to make sure lenders have accurate insights into business’ credit health. However, it’s not a commercial credit reporting agency. Instead, it collects payment history from its member lenders and provides that data to the credit reporting agencies.

Here’s how it works:

- SBFE member lenders report business payment history to SBFE.

- SBFE shares the data with commercial credit reporting agencies.

- The agencies use this data – along with information from other sources – to create credit reports and scores.

Payments to suppliers, loan payments, commercial lease payments, and auto payments are examples of payment experiences that can end up on your business credit file via the SBFE. They collect and share both positive and negative payment information, which includes on-time payments as well as late payments.

And, unlike personal credit data, business credit data is not protected under the Fair Credit Reporting Act FCRA, which means that anyone can access your business’s credit information without your permission. However, SBFE data is available only to SBFE members for credit risk assessment purposes, not for marketing.

As for membership, small businesses can’t join SBFE or report payment history directly to it (the reason they don’t allow you to submit your own trade references is to prevent duplicate account reporting). SBFE membership is open to those who originate small business financing.

Recommended: 41 Companies That Help Small Businesses Build Business Credit

What You Need to Know About the SBFE Score

The SBFE maintains independence from business credit reporting bureaus, which enables bureaus to set their own criteria for data sharing. Meanwhile their regulations help make sure the data remains unaltered once bureaus incorporate it into their systems. So, commercial credit reporting agencies come up with their own SBFE scores based on (accurate) information obtained from the SBFE as well as other sources.

For example, Dun & Bradstreet’s (D&B’s) SBFE Score predicts how likely a business is to have financial problems like severe delinquency, charge-offs, or bankruptcy within the next year—It ranges from 706 to 999, with higher scores meaning lower risk.

The score is based on data from SBFE and other sources, including tradelines that report directly to D&B. D&B’s SBFE score available for most U.S. businesses, except for some with missing info or those flagged as high risk. The score is used to help lenders determine a business’ credit risk and optimize profitability.

So, what is a good SBFE score for a business? Well, typically one on the higher end of the scale, which indicates lower risk for financial issues.

Experian, Equifax, and Lexis Nexis have their own, comparable business credit scoring models. I am most familiar with D&B’s scoring models, since it’s the business credit bureau that I primarily work with (in my experience, it has the greatest breadth).

Recommended: Everything You Need to Know About a DUNS Number – and Why You Should Care

Company Overview

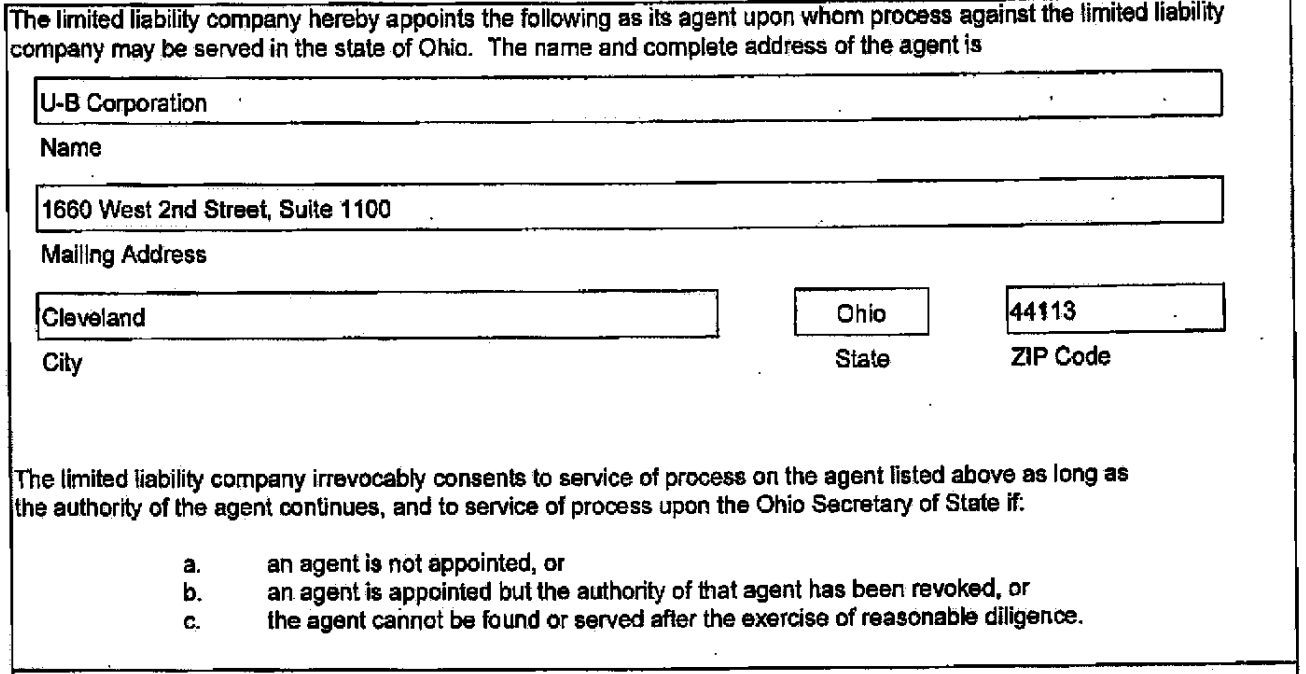

Small Business Financial Exchange Inc. (SBFE, LLC) is a trade association that was founded in 2001 to support the safe and secure growth of small businesses. According to Crunchbase, they’re based in Illinois, but the Ohio Secretary of State’s Website lists them as an actively-registered, foreign (registered in Delaware) Limited Liability Company headquartered in Cleveland. Their LinkedIn profile lists them in Shaker Heights, Ohio.

The organization has raised a total of $15.8 million in funding from investors, and recently made headlines with their efforts to strengthen small business credit decisions.

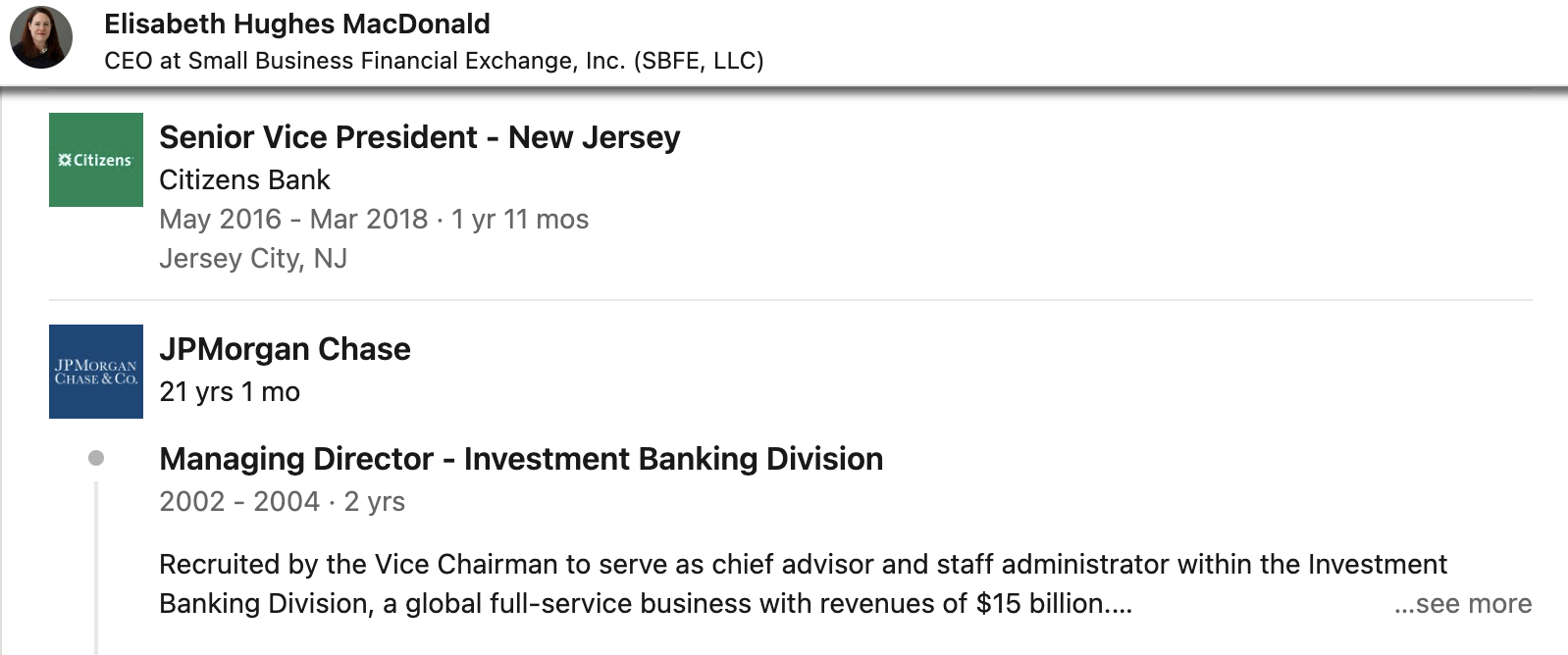

Prior to taking her role as the current CEO of SBFE, Elisabeth Hughes Macdonald (New York) was the Managing Director of Investment Banking at Chase and the Senior Vice President at Citizens Bank. She’s also served as a board member at Lafayette College and Impact 100 Garden State.

The SBFE apparently doesn’t have a lot of employees, so they don’t have a presence on Glassdoor or Indeed. As a result, we don’t know what employees think about working there or whether they approve of company leadership. And, you won’t find user reviews on Trustpilot or complaints with the Better Business Bureau because they’re not a consumer or small business-facing institution.

What Companies are Affiliated with the SBFE?

The SBFE collaborates with various entities that can significantly impact small businesses’ financial health and creditworthiness. While SBFE doesn’t publicly disclose its entire list of members, here are some key entities they work with that small businesses should be aware of.

By understanding SBFE’s partnerships with these entities, you can gain insights into the credit ecosystem and make informed decisions about their financing options and credit management strategies.

Recommended: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

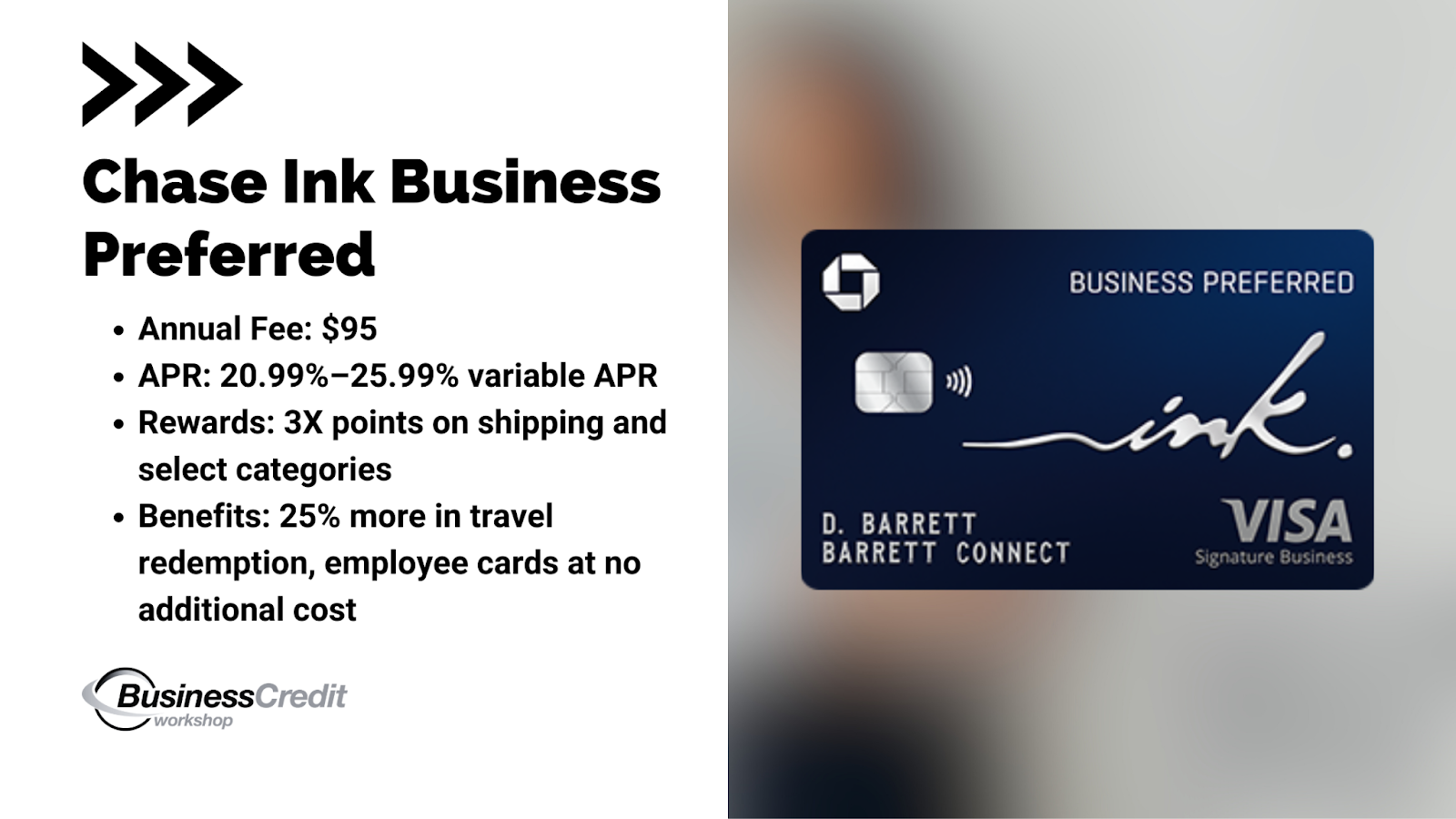

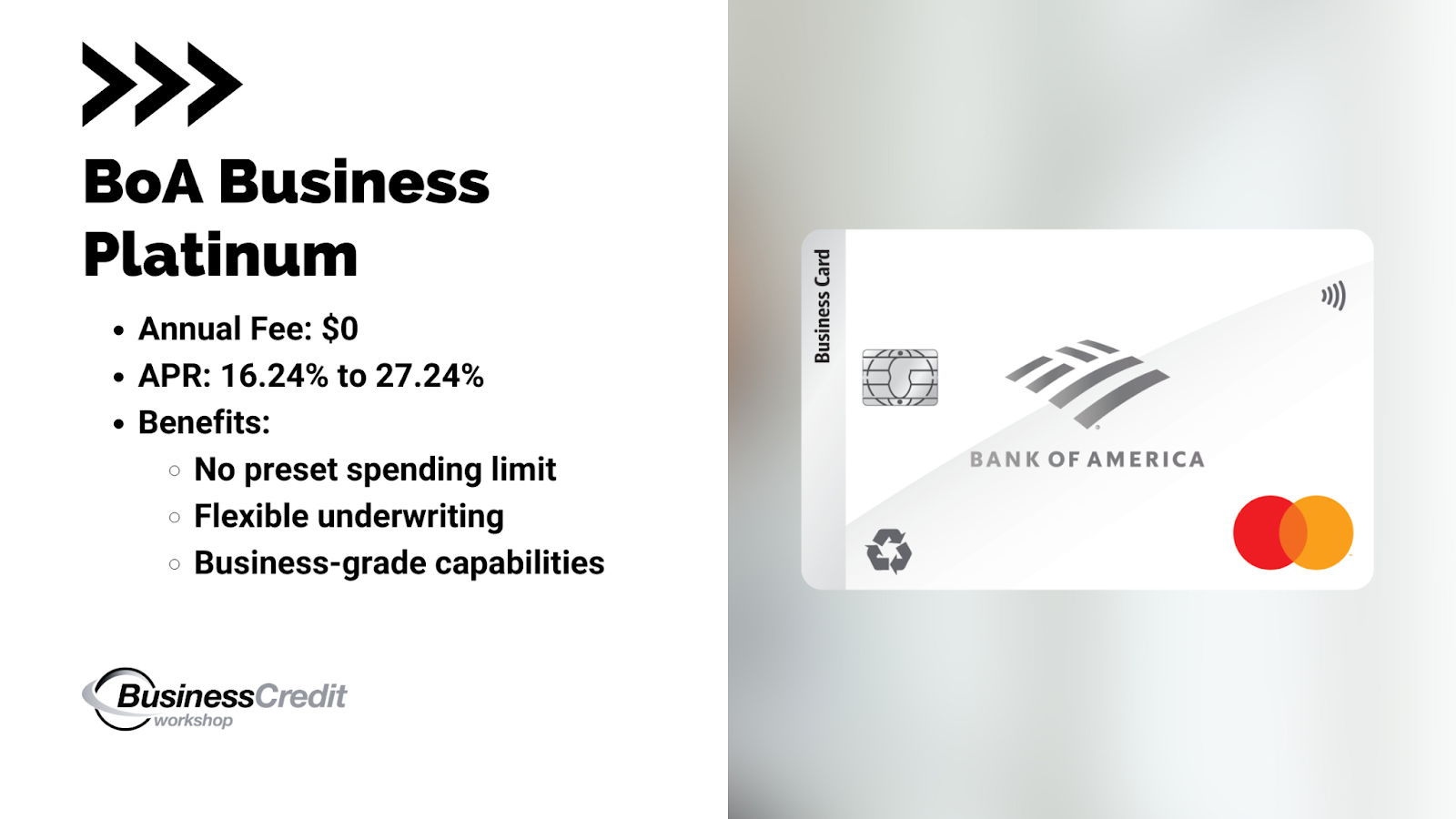

1. Major Banks

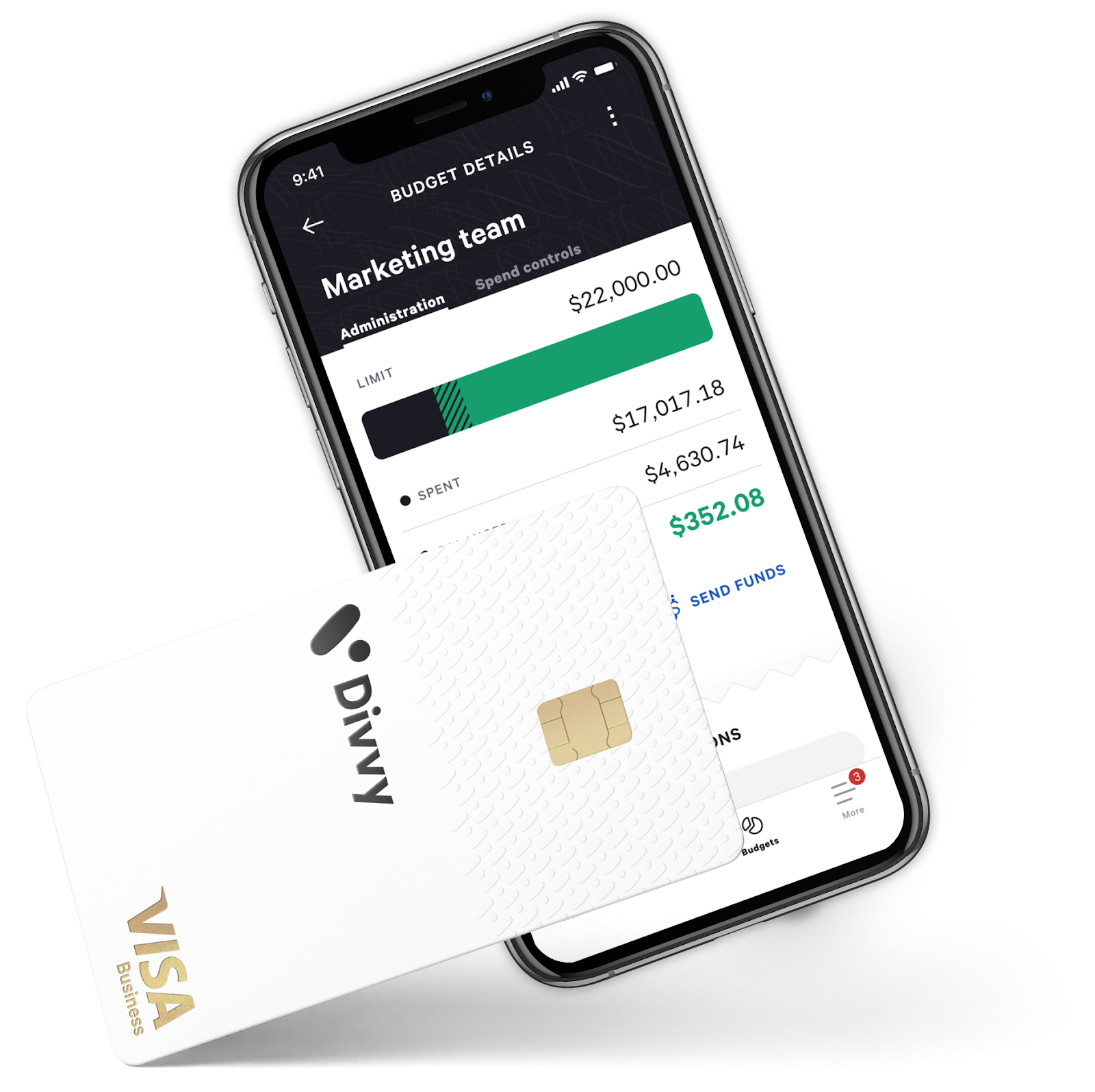

Many of the largest banks in the United States are members of SBFE. These banks often offer a wide range of financial products and services to small businesses, including loans, lines of credit, and business credit cards.

You might also like: Chase Ink Business Preferred Credit Card: A Deep Dive Analysis

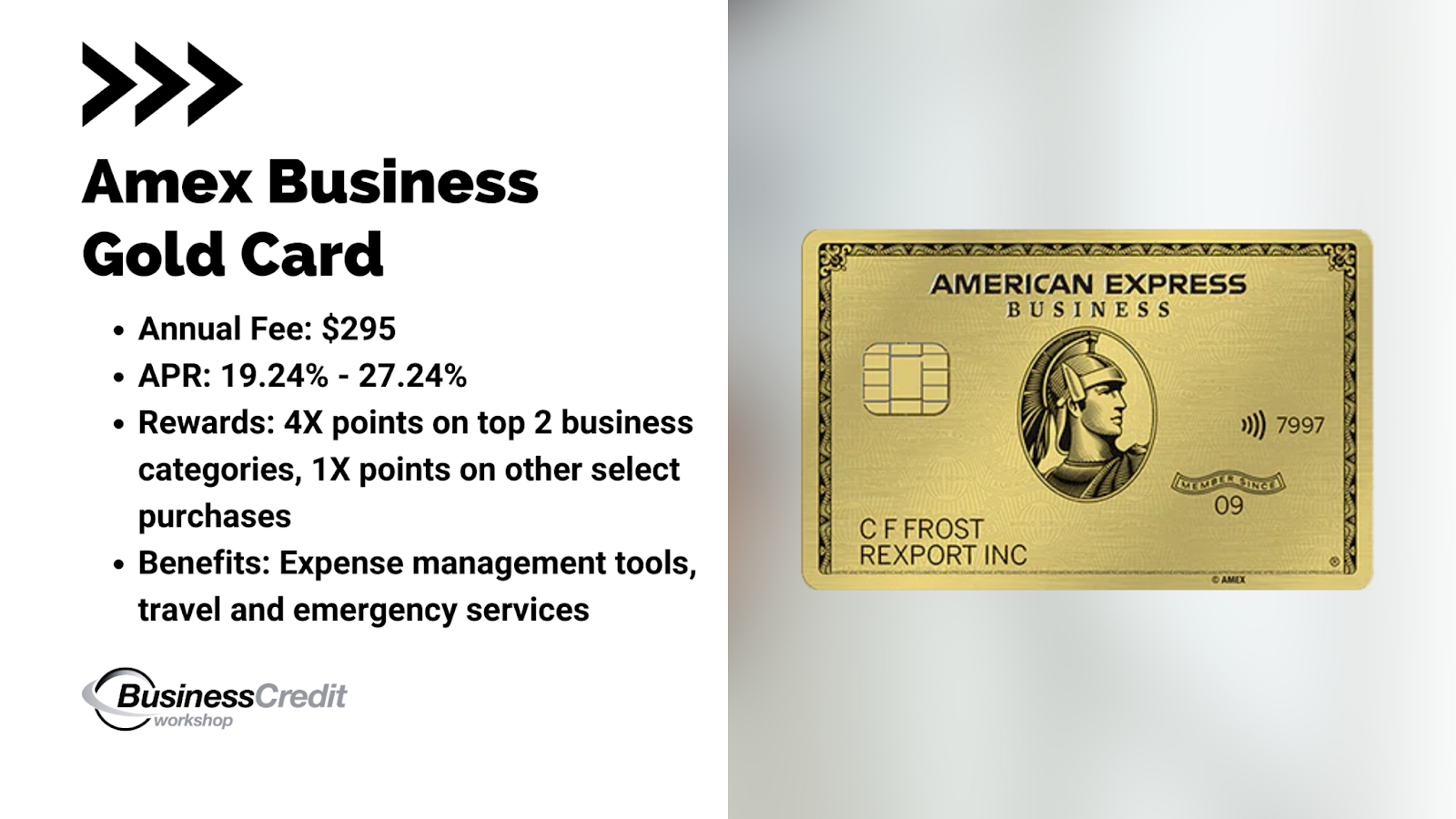

2. Credit Card Issuers

SBFE partners with credit card issuers who provide small businesses with credit cards tailored to their needs. These issuers play a crucial role in helping small businesses manage cash flow and access credit for various business expenses.

Recommended: What are the Best Unsecured Business Credit Cards for Startups?

3. Alternative Lenders

In addition to traditional banks and credit card issuers, SBFE may also work with alternative lenders such as online lenders and fintech companies. These lenders often provide innovative financing solutions to small businesses that may not qualify for traditional bank loans.

You might also like: No-Doc Business Loans: Get Funds Without Proof of Income

4. Business Credit Bureaus

SBFE shares data with four major commercial credit reporting bureaus:

- Dun & Bradstreet

- Equifax

- Experian

- LexisNexis Risk Solutions

These bureaus compile and analyze small business payment data to create credit reports and scores used by lenders to assess creditworthiness.

Recommended: Dun and Bradstreet / How to get a DUNS Number

Frequently Asked Questions

How do I find out my business credit score?

You can find out your business credit score by contacting commercial credit bureaus like Dun & Bradstreet, Equifax, Experian, or LexisNexis Risk Solutions. They can provide you with your commercial credit report, which includes your business credit score.

What is a small business as defined by the US SBA?

According to the US Small Business Administration (SBA), a small business is typically one that has fewer than 500 employees for most industries—The definition can vary based on industry and other factors.

Conclusion

In sum, the SBFE isn’t super transparent with small businesses when it comes to how they operate and what information they report to bureaus. They’re primarily a lender-facing institution. So, when you have questions about your business credit as it relates to SBFE reporting, it’s best to go straight to the business credit bureaus that they report to (D&B, Experian, Equifax, or Lexis Nexis).

If you’re unsure whether or not your lender is an SBFE member, you can ask them directly.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!