In today’s competitive business landscape, a strong brand identity is paramount to stand out from the crowd. An effective way to showcase your company’s image and values is through custom apparel and swag. Shirtsy, a popular business t-shirt club, offers a wide range of high-quality print-on-demand t-shirts that can elevate your brand and leave a lasting impression.

The reason I take an interest is because of the net 30 offer, which is a key element in building a strong business credit profile.

In this full review, I’ll delve into Shirtsy’s full print-on-demand offer (the range of products, available designs, customization options, and dropshipping offer) and explore my favorite parts of the offer (net 30 accounts, credit reporting, and credit bureaus).

But, is this the best offer for your business, or can you find one that’s better suited?

This is what’s in store:

- Meet Shirtsy — The Business T-Shirt Club That Can Help You Build Business Credit

- More Net 30 Options to Build Business Credit

- Final Thoughts

Now, let’s get the ball rolling!

Meet Shirtsy — The Business T-Shirt Club That Can Help You Build Business Credit

Shirtsy offers a wide range of print-on-demand products for businesses to build their brand. From apparel like hoodies, shirts, and activewear for both men and women to home items like candles and wall art, Shirtsy has customizable options to suit various needs.

They also provide promotional items like magnets and postcards, as well as specialized merchandise for restaurants and professionals (i.e. chefs and skateboarders). With their print-on-demand services, businesses can create personalized items that showcase their brand identity and leave a lasting impression.

Whether it’s clothing, accessories, or promotional merch, Shirtsy offers a diverse selection to help businesses enhance their brand visibility and engage with their target audience effectively.

Product categories include Apparel, Home (candles, wall art, and frames), Promotional (magnets & postcards), Restaurant Merch, Office (business cards, mugs, and mouse pads), Create (puzzles and stickers), Portraits, and Drinkables (bagged coffee).

Shirtsy Company Overview

Shirtsy is a fashion apparel company based in Dania Beach, FL, dedicated to creating and selling unique and funny shirts. With a diverse collection of creative designs, they offer high-quality and distinctive shirts and other products that cater to various styles and preferences.

I didn’t know this before I went down the rabbit hole, but Shirtsy is managed by the same person as Crown Office Supplies, Dana Angelino. Angelino is also responsible for a few other up-and-coming Florida companies like Coconut Bikinis and Greentees and a handful of other businesses.

Shirtsy’s Net 30 Payment Terms

When considering signing up for Shirtsy’s Net 30 account, you need to understand the terms and how they will impact you. With this account, you have 30 days after each billing cycle to pay your balance. Shirtsy offers a 0% Annual Percentage Rate (APR) for purchases, based on your creditworthiness — This means you won’t be charged interest on your purchases if you pay off your entire balance by the due date each month.

But, there are other fees associated with the account.

Shirtsy charges an annual fee of $99.

The annual membership fee is non-refundable. However, as a gesture of goodwill, Shirtsy claims that they will report the fee to the credit bureaus as your initial credit payment — This should allow your business to begin building credit immediately, regardless of whether you utilize the services.

And, there are late fees depending on your balance:

- $2 minimum finance charge

- $15 for balances up to $100

- $29 for balances from $100 up to $250

- $39 for balances of $250 and over.

In addition, a returned payment fee of $39 may apply if your payment cannot be processed.

If you decide to sign up for the Shirtsy Net 30 Account, keep in mind that Shirtsy has the discretion to apply your payments in a way that benefits them the most — This means they may choose to pay off lower APR balances before the higher ones.

And, Shirtsy can change the rates, fees, and terms of the card agreement at any time, but they will provide you with advance notice of any rate or fee increases…If you don’t agree with the changes, you have the right to opt-out, but this may result in the closure of your account. You can continue paying the remaining balance under the old rates, fees, and terms.

Signing up for the Shirtsy Net 30 Account may affect your credit report. Shirtsy reports credit information to the credit bureaus, and they may request commercial reports and other information about your business. It’s crucial to provide accurate information and be aware of how your creditworthiness can be impacted.

To summarize the costs, you can expect to pay an annual fee of $99 and potential late fees and returned payment fees. However, if you manage your payments responsibly and pay off your balance each month, you can avoid interest charges.

Review the terms and conditions carefully before making a decision, and if you have any questions, reach out to Shirtsy for clarification.

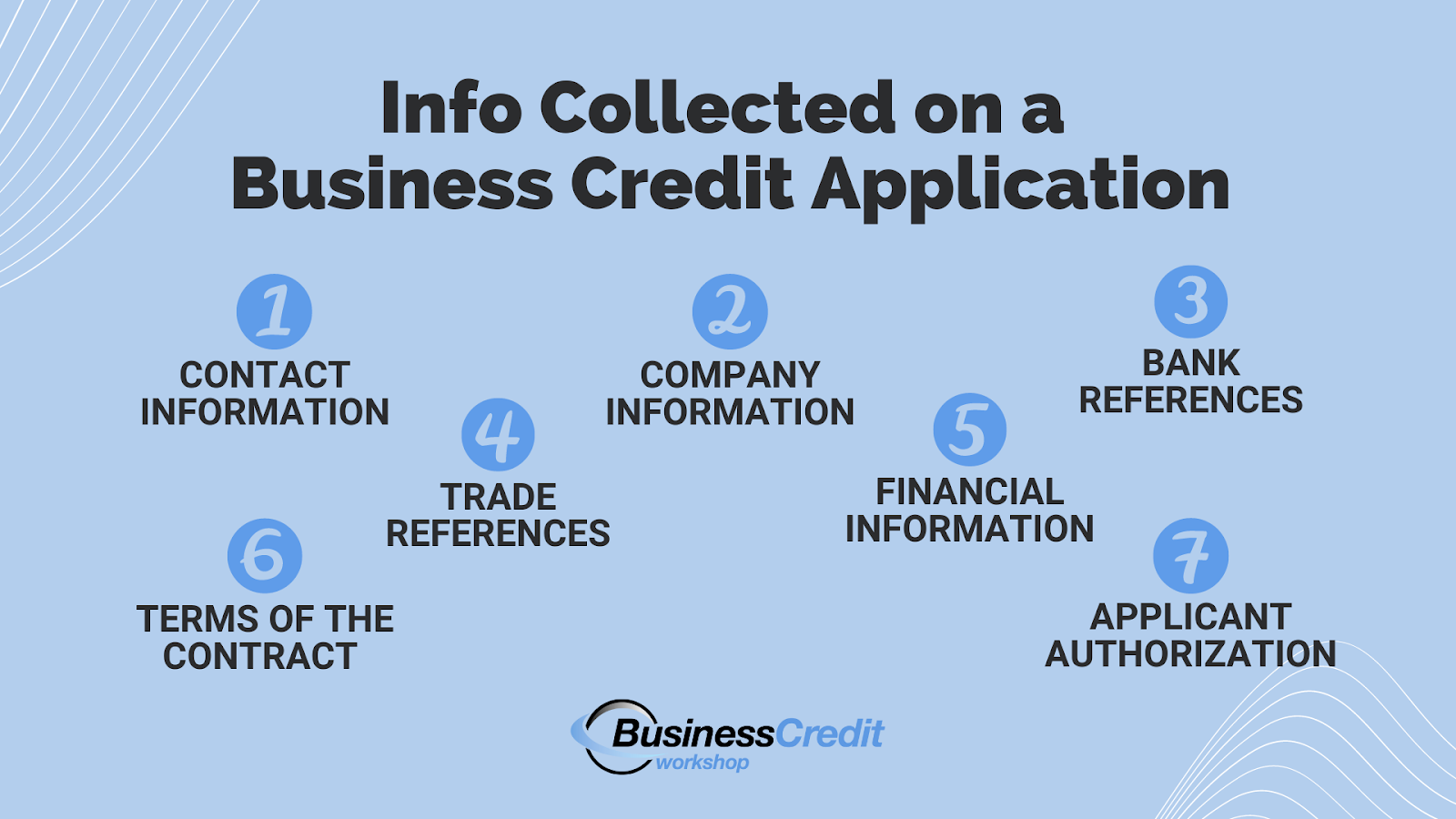

What to Expect When You Apply for Shirtsy’s Net 30 Terms

Before applying for Shirtsy’s Net 30 account, make sure you meet the following requirements:

- 25% or more ownership of the company

- Accurate details about your company, including its legal name, website, EIN, and DUNS number

- Your full name, email address, password, phone number, and date of birth

- Your company’s complete address

- Ability to receive account status notifications via email, SMS, and phone

Approval is contingent on commercial data reports, and commercial debt servicing and collections may be provided by a third-party financial institution — the application does not result in a hard credit inquiry and will not affect your personal credit score.

To apply for Shirtsy’s Net 30 account, follow these simple steps:

- Visit Shirtsy’s NET 30 Application page

- Fill in the required information in the application form, including:

- First Name

- Last Name

- Password

- Company Name

- Website (optional)

- EIN

- DUNS (optional)

- Address (Street, Suite, City, State, Zip)

- Phone Number

- Date of Birth (Month, Day, Year)

- Read and agree to the terms and conditions (and that the information is truthful and accurate)

- Review the application details and click the Submit button to complete the application process.

That’s it!… You’ll receive further updates about your application status and instructions via the email you provide when you apply.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

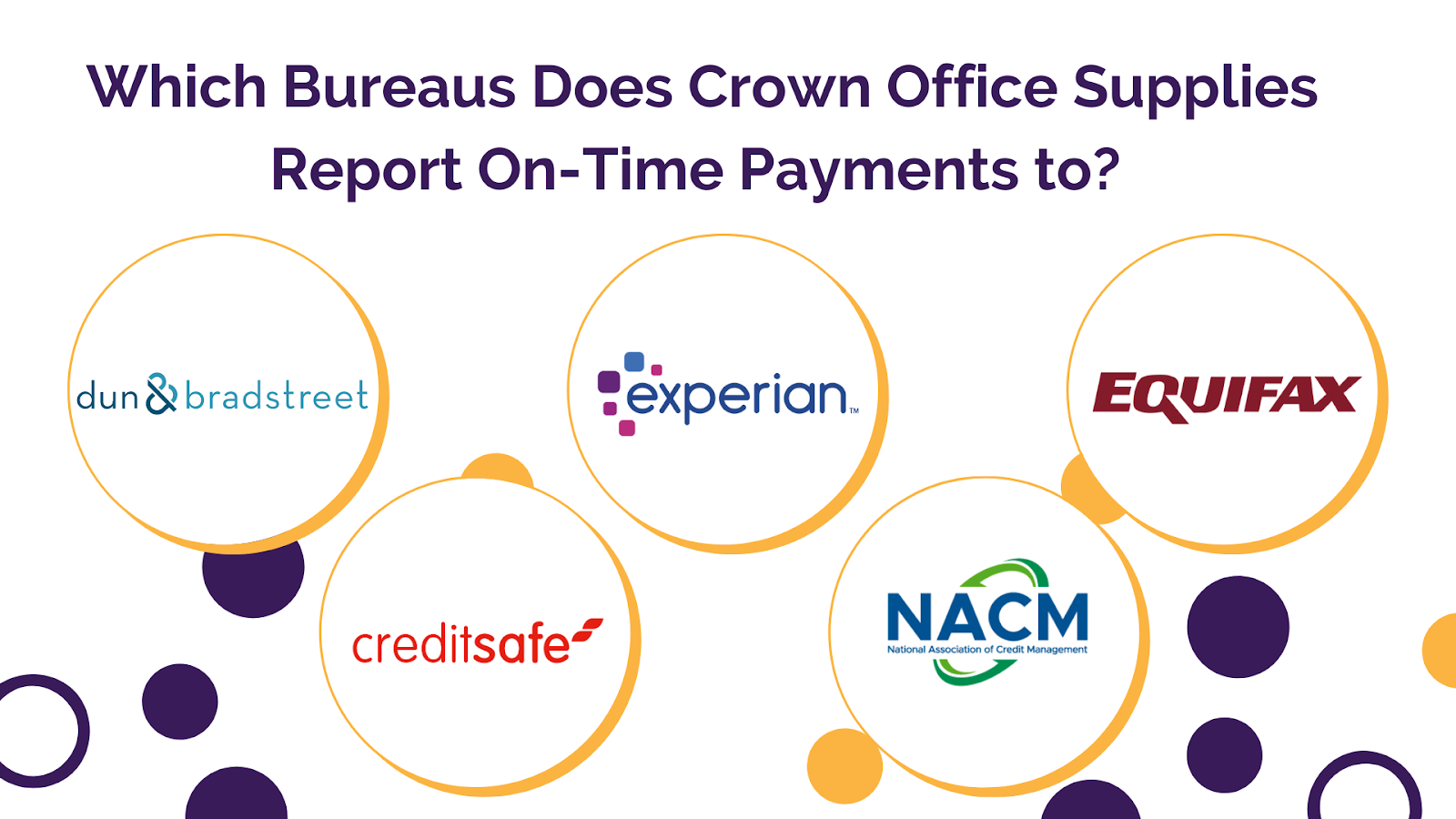

Does Shirtsy Report to Dun & Bradstreet?

According to their customer support, Shirtsy reports to Dun & Bradstreet and other credit bureaus such as Equifax, Credit Safe, NACM, LexisNexis, and Ansonia. Shirtsy reports to these credit bureaus for any purchase with a minimum amount of $30.

They require that you make the payment 2 to 3 days before your invoice due date for the payment to be reported. Still, they report your net 30 membership fee as a courtesy, even if no order is placed.

Shirtsy reports on the 15th of each month for on-time payments made the previous month. For instance, if you place an order in February but pay for it on March 1st, the payment will be considered a March payment and reported on April 15th.

However, if the payment is made on February 27th or 28th, before the end of the month, it will be considered a February payment and reported on March 15th.

It’s important to note that while some credit bureaus report accurately within 30 days, others have the discretion to delay reporting for a period ranging from 45 to 90 days.

More Net 30 Options to Build Business Credit

An annual fee is not typical with a net 30 offer. And, several other net 30 offers report on-time payments to business credit bureaus.

Using Net 30 vendors is a smart way to build your business credit score. These vendors offer payment terms where you pay the amount owed within 30 days. By choosing vendors that report to business credit bureaus, like Quill, you can establish trade lines and build credit.

Other vendors, such as BP Gas, Valero Gas, Advance Auto Parts, Gemplers, Supplyworks, Business T-Shirt Club, and Lowe’s, provide similar opportunities.

Recommended: Using 30-Day Net Vendors to Build Your Business Credit Score

Final Thoughts

In this review, we’ve explored Shirtsy’s collection of custom swag and its knack for personalization. Then, we touched on the story behind the brand. We’ve also looked at the details of their net 30 payment terms (including the infamous $99 annual membership fee and potential late payment fees that could whack your credit score).

While Shirtsy has its charm, it’s a good idea to at least consider other net 30 account options without an annual fee. Just like mixing and matching outfits, exploring various vendors can help you find the perfect credit-building ensemble for your business.

Ready to discover the best net 30 vendors to level up your credit journey and obtain up to 100K in business credit in as little as 30 days? Join Business Credit Workshop today.