You’ve got a business, and you’re at least somewhat interested in leasing a car. So, why not lease on behalf of your business? Well, as with all things, there are pros and cons.

Here, I’ll cover everything you need to know about business car leasing, the benefits, potential tax breaks, and answer some of the most commonly asked questions.

Find out how you can lease a car with your EIN and learn to take advantage of all the benefits.

This is what’s in store:

- What is Leasing a Car?

- How to Lease a Car With Your EIN

- Business Car Lease Requirements

- Frequently Asked Questions

- Final Thoughts

Now, let’s hit the road!

What is Leasing a Car?

Leasing a car is kinda like renting it for a longer stretch, usually a few years. Instead of paying the full price, you’re basically paying for the time you’ll be driving it and how much it’s expected to depreciate (lose value) during that time.

When you lease, you agree to make monthly payments, kinda like paying rent on an apartment. You also might have to put down a chunk of money upfront, which is called a “down payment” or “cap cost reduction.”

Leasing can be a good option if you like driving newer cars and don’t wanna deal with selling or trading in your ride every few years—But it’s not for everyone, ’cause you don’t actually own the car at the end, and the costs can add up if you go over the mileage limit or damage the car.

So, it’s worth doing some math and thinking about your driving habits before diving into a lease.

You might also like: How to Start a Trucking Company From Start to Finish

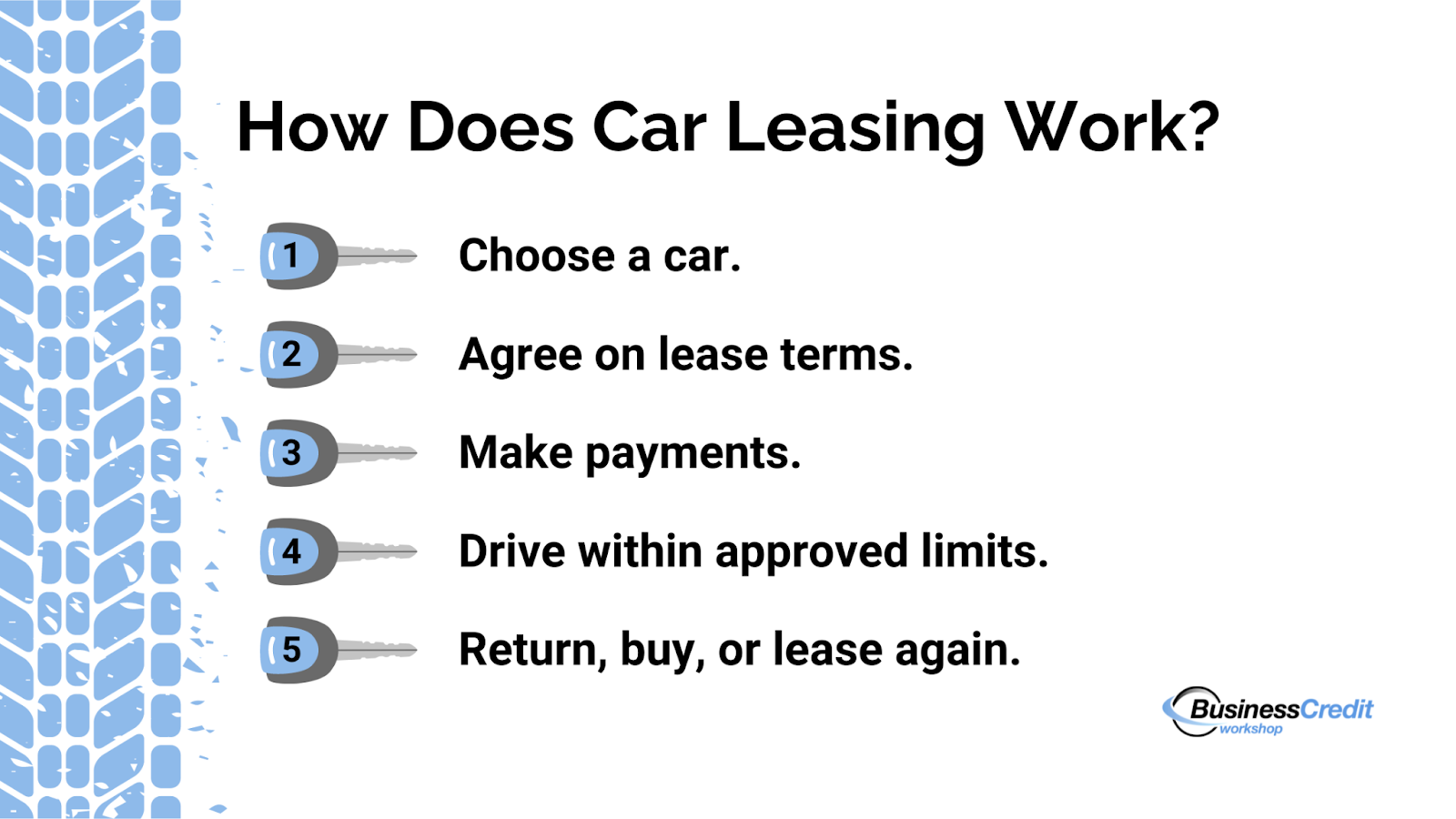

How Does Car Leasing Work?

The process for car leasing is somewhere in between the process for buying a car and renting one.

Here’s the lowdown on how it usually goes:

- You pick the car you wanna lease—This could be a brand new one from a dealership or a used one from a leasing company.

- You and the leasing company (or dealership) agree on how long you’ll lease the car for, usually 2 to 4 years, and how many miles you can drive each year. There might also be other terms like the down payment and monthly payment amount.

- Once you sign on the dotted line, you start making monthly payments, kinda like paying rent on an apartment. These payments cover the depreciation of the car during the lease period, plus any fees and taxes.

- During the lease, you’re responsible to keep the car in good shape and maintain it according to the leasing company’s requirements. You also gotta stick to the mileage limit, ’cause going over it can result in extra fees.

- When the lease term is up, you’ve got choices to make. You can return the car and walk away, buy it outright for a pre-agreed price (called the “residual value”), or lease a new car.

If you decide to return the car, you’ll need to get it inspected to check for any excess wear and tear or mileage overage. Depending on the condition, you might have to pay some extra charges.

After all that, you either say goodbye to the car or hop into a new lease and start the process all over again—That’s the basic rundown.

A lease can be a pretty sweet deal if you like driving newer cars and don’t mind not owning them outright. But like anything, it’s got its pros and cons, so weigh your options before you dive in.

You might also like: The Best Credit Cards for Truckers: Save Big on the Road!

Why Lease a Car for Business?

Leasing a car for business purposes can be a strategic move for several reasons. Firstly, opting for a lease often translates to lower monthly expenses compared to purchasing a vehicle outright through a loan.

And, there are potential tax benefits associated with leasing—lease payments can typically be deducted as a business expense. You can potentially write-off the entire payment if the car is used solely for business purposes.

Moreover, leasing enables you to regularly upgrade to newer models, helping to maintain a professional image and take advantage of the latest tech and safety features. Some lease agreements include maintenance packages, which eases the burden of routine upkeep and repairs.

The flexibility of lease terms further enhances its appeal. It can enable you to tailor agreements to your specific needs in terms of lease duration and mileage allowances.

By leasing, you can:

- Preserve capital

- Enjoy predictable costs

- Drive newer vehicles without long-term commitment

- Mitigate potential depreciation associated with ownership

However, carefully evaluate your needs and thoroughly review lease terms to make sure leasing is the right fit for your particular circumstances.

You might also like: How a Trucking Company in Snellville, GA Got Over $200K in Business Credit

Can You Write-Off a Car Lease for Business?

A car lease can be written off on your taxes, but the way you write it off isn’t cut and dry. With that said, how is leasing a car a tax write off?

To write off a car lease for tax purposes, you typically have a few options depending on your business’s circumstances and tax strategy:

- Section 179 deduction – If the leased vehicle qualifies under Section 179, you can deduct the full cost of the lease as a business expense, up to the annual limit set by the IRS. To qualify, the vehicle must be used for business purposes at least 50% of the time and meet other criteria—This deduction can provide significant tax benefits, especially if you need to deduct a large portion of the lease cost upfront.

- Standard depreciation – If the vehicle doesn’t qualify for Section 179 or if you’ve reached the deduction limit, you can depreciate the lease payments over the vehicle’s useful life using standard depreciation methods like Modified Accelerated Cost Recovery System (MACRS)—This method spreads the lease cost over several years, allowing you to deduct a portion of the expense annually based on the depreciation schedule provided by the IRS.

- Actual expenses deduction – Alternatively, you can deduct the actual expenses related to the business use of the leased vehicle. This includes costs like fuel, maintenance, insurance, and lease payments. To claim this deduction, you’ll need to keep detailed records of all business-related expenses and ensure you can substantiate them.

- Mileage Deduction – If you prefer a simpler method, you can deduct the business-related mileage driven using the leased vehicle. The IRS allows a standard mileage rate deduction for qualifying business miles driven, which accounts for depreciation, maintenance, insurance, and other vehicle expenses. Keep accurate records of your business mileage to support your deduction claim.

And, not every business can automatically write off a vehicle for business—So, consult with a tax professional to ensure you meet all the requirements and properly claim deductions for leased vehicles.

You might also like: Is Carputty Legit? A Complete Auto Financing Review

How to Lease a Car With Your EIN

Leasing a car using your Employer Identification Number (EIN) for business purposes involves similar steps to leasing a car with your personal information, but with some differences.

Here’s a general guide on how to lease a car with your EIN.

You might also like: Here’s How to [Actually] Get Business Credit With Just an EIN

1. Establish Business Credit

Before applying for a car lease with your Employer Identification Number (EIN), it’s crucial to establish credit in your business’s name—This can be achieved by opening a business credit card, obtaining a business loan, or establishing trade lines with suppliers.

Building a solid credit history for your business will increase your chances of getting approved for a car lease and securing favorable lease terms.

Recommended: Business Credit Workshop’s Official Business Credit Building Checklist

2. Research Lease Options

Take the time to explore different leasing companies and dealerships to find the best lease terms that align with your business needs.

Consider factors such as:

- Lease duration

- Mileage limits

- Upfront costs

- Monthly payments

Compare offers from multiple sources to ensure you’re getting the most competitive deal available.

You might also like: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

3. Gather Required Documents

Prepare all the necessary documentation to support your lease application.

This typically includes:

- Your business’s EIN

- Possibly your DUNS number

- Business registration documents

- Financial statements

- Personal guarantors or business credit references

If you don’t already have established business credit, you’ll want to make sure your business is registered in an appropriate structure and that you’ve chosen a low-risk NAICS or SIC code.

Any additional docs you will need depends on the leasing company’s requirements. Having your documentation ready ahead of time will streamline the application process.

You might also like: Free, Printable Business Credit Application Template (+How to Use it)

4. Apply for the Lease

Submit your lease application to the leasing company or dealership. Provide accurate information about your business, including its financial standing and credit history—Be prepared for the leasing company to conduct a credit check on your business to assess its creditworthiness.

Some companies may also require additional documentation or information during the application process.

Recommended: No-Doc Business Loans: Get Funds Without Proof of Income

5. Negotiate Terms

Review the lease offers you receive and negotiate terms if necessary.

Pay close attention to factors like:

- Lease duration

- Mileage allowance

- Interest rates

- Additional fees

Don’t hesitate to ask for modifications or concessions that better suit your business’s needs. Negotiating favorable terms upfront can save you money and ensure a more favorable leasing experience.

Recommended: Should You Hire a Business Credit Consultant?

6. Sign the Lease Agreement

If you’re satisfied with the terms offered, sign the lease agreement using your business’s legal name and EIN. Take the time to carefully review all the terms and conditions outlined in the contract before signing.

Make sure you understand your obligations, rights, and any penalties for early termination or excessive mileage.

7. Take Possession of the Vehicle

Once the lease agreement is signed, you can accept delivery of the leased vehicle. Before taking possession of the vehicle, inspect it thoroughly. Make sure it meets your expectations and that there are no damages or defects.

⚠️ Document any issues and notify the leasing company or dealership promptly to avoid disputes later on.

8. Make Your Payments as Agreed

Make timely lease payments according to the terms outlined in the lease agreement. It’s essential to adhere to the payment schedule to maintain a positive relationship with the leasing company and avoid late fees or penalties.

Maintain the leased vehicle in good condition and adhere to any maintenance requirements specified by the leasing company—this ensures compliance with your lease agreement.

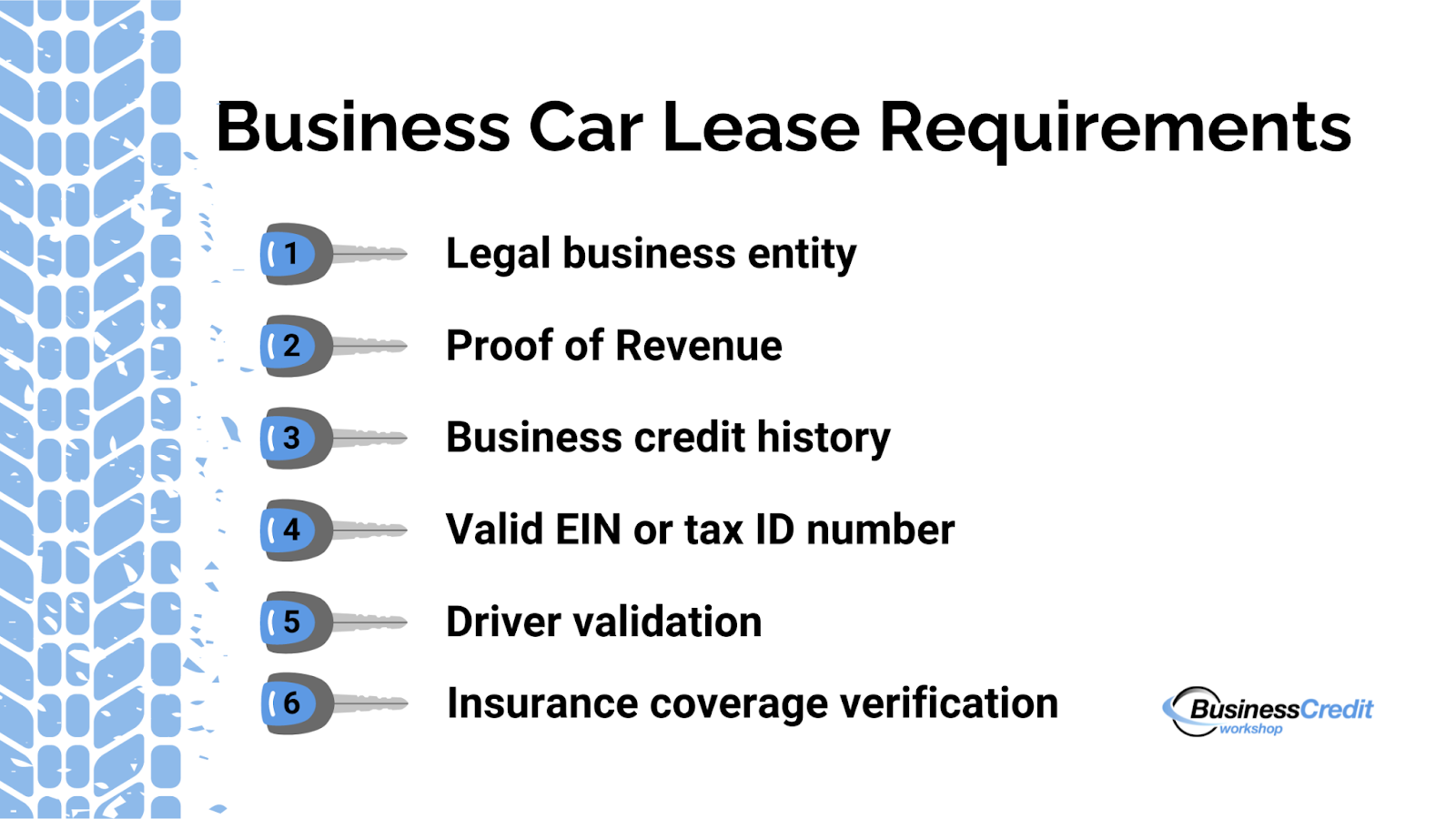

Business Car Lease Requirements

Business car lease requirements can vary depending on the leasing company and the specific terms of the lease agreement.

Here are some common requirements that businesses typically need to meet when leasing a car:

- You must operate as a legal business entity.

- Provide a valid Employer Identification Number (EIN) or Business Tax ID.

- A solid business credit history demonstrates your ability to manage financial obligations.

- Provide proof of your business’s financial stability.

- Designate authorized drivers with valid licenses.

- Maintain adequate insurance coverage for the leased vehicle.

You will also need to adhere to mileage restrictions and usage limitations as well as follow all terms and conditions outlined in the lease agreement.

⚠️ Be sure to carefully review all lease terms and conditions before signing the agreement to ensure that you understand your obligations and rights as a lessee.

You might also like: Here’s How to Check Your Business Credit Score, Step-by-Step

Frequently Asked Questions

How do I lease a car with my EIN number?

To lease a car using your Employer Identification Number (EIN), establish business credit, gather required documentation, submit a lease application with accurate business details, and sign the lease agreement using your EIN.

Is it better to lease a car as a business owner?

Leasing may be advantageous for business owners due to lower upfront costs, potential tax benefits, and access to newer vehicles without long-term ownership commitments. However, it involves ongoing payments and mileage restrictions.

What are the disadvantages of leasing a vehicle for business?

Drawbacks of leasing include no ownership at the end of the term, mileage limitations, continuous lease payments without equity buildup, and potential fees for early termination.

Can you write off car payments for an LLC?

Yes, LLCs can typically deduct car lease payments as a business expense if the vehicle is used for business purposes, following IRS guidelines. Consult a tax professional to see if this applies to you.

Is it better to lease or buy a car for business tax write off?

The decision depends on factors like usage, budget, and preferences. Leasing offers immediate tax benefits with deductible lease payments, while buying provides long-term ownership and potential depreciation deductions. Consult a tax advisor for personalized advice.

Final Thoughts

Business car leasing can offer a flexible and cost-effective way to meet your company’s transportation needs—By using your EIN to lease a vehicle, you can access newer models with lower upfront costs and potential tax benefits. However, leasing involves ongoing payments and there are mileage restrictions to consider.

Now, you should understand essential aspects of business car leasing, including the process, tax implications, and considerations. By taking it all into account and weighing the pros and cons, you can make an informed decision that aligns with your business goals.

Consult financial advisors or tax professionals to tailor leasing decisions to your circumstances and maximize benefits. With this knowledge, you can leverage business car leasing to optimize your transportation strategy efficiently.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!