A couple of my Business Credit Workshop students were recently approved for business auto financing through Carputty. So, naturally, I wanted to do a deep dive into the offer to give you a full Carputty review. By the end, you should know if this is the right offer for you.

Here, we’ll look at the auto loans, the requirements, the company, and all of Carputty’s features. Along the way, I’ll make sure to answer any questions you might have the best I can.

This is what’s in store:

- What is Carputty?

- What Does Carputty Do?

- Frequently Asked Questions

- Conclusion: Is Carputty Worth it?

Now, let’s get the show on the road!

What is Carputty?

Carputty offers a new approach to auto financing that can change how you manage your vehicles (as investments)—Instead of traditional auto loans, Carputty provides a Flexline™, which is a flexible line of credit.

You can use it repeatedly for various automotive transactions like:

- Buying out a lease

- Refinancing

- Purchasing eligible vehicles

You can use it for both new and used vehicles, and the interest rate remains the same regardless of the vehicle’s make, model, year, or transaction type. As you pay down your balance, the funds become available again for other vehicle purchases, which makes it super convenient.

You might also like: How a Trucking Company in Snellville, GA Got Over $200K in Business Credit

Carputty Credit Score Requirements

Carputty generally requires individuals to have good-to-excellent credit scores to qualify for their Flexline™ of credit. You need a FICO score of at least 680, though exact requirements vary based on other factors such as income, debt-to-income ratio, and other considerations.

If you’re considering applying for Carputty’s Flexline™, check your credit score beforehand and make sure it falls within or exceeds the range required for approval.

You might also like: Here’s How to Check Your Business Credit Score, Step-by-Step

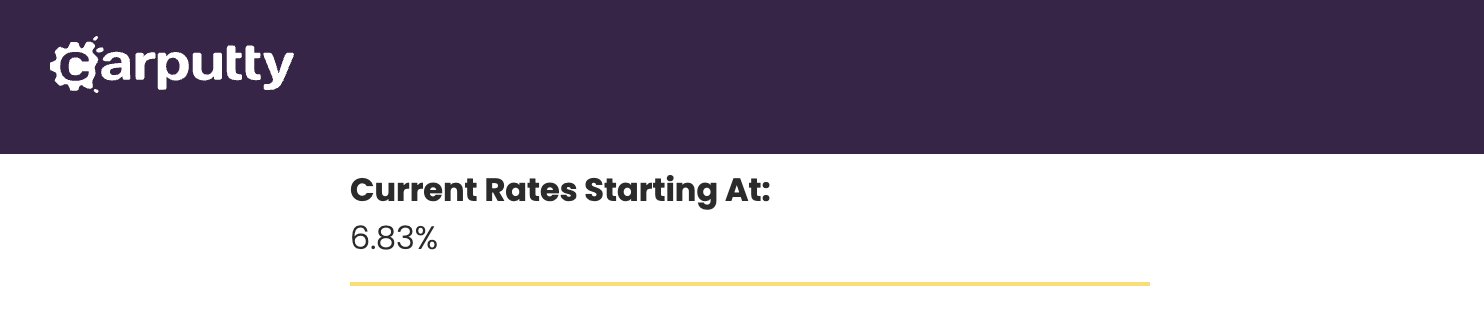

Carputty Interest Rates

Right now, Carputty rates start at 6.83%. Compared to the national average – currently 9.56% – this may seem low. But, if you look at some of the top auto lenders right now, their rates may start lower. For example, Toyota auto financing starts at 3.75%.

The difference is that the traditional auto lenders aren’t offering revolving loans for cars and their limits usually max out around $75K to $100K—you can get a much higher limit with Carputty.

You might also like: Business Car Leasing 101: How to Lease a Vehicle With Your EIN

Company Overview

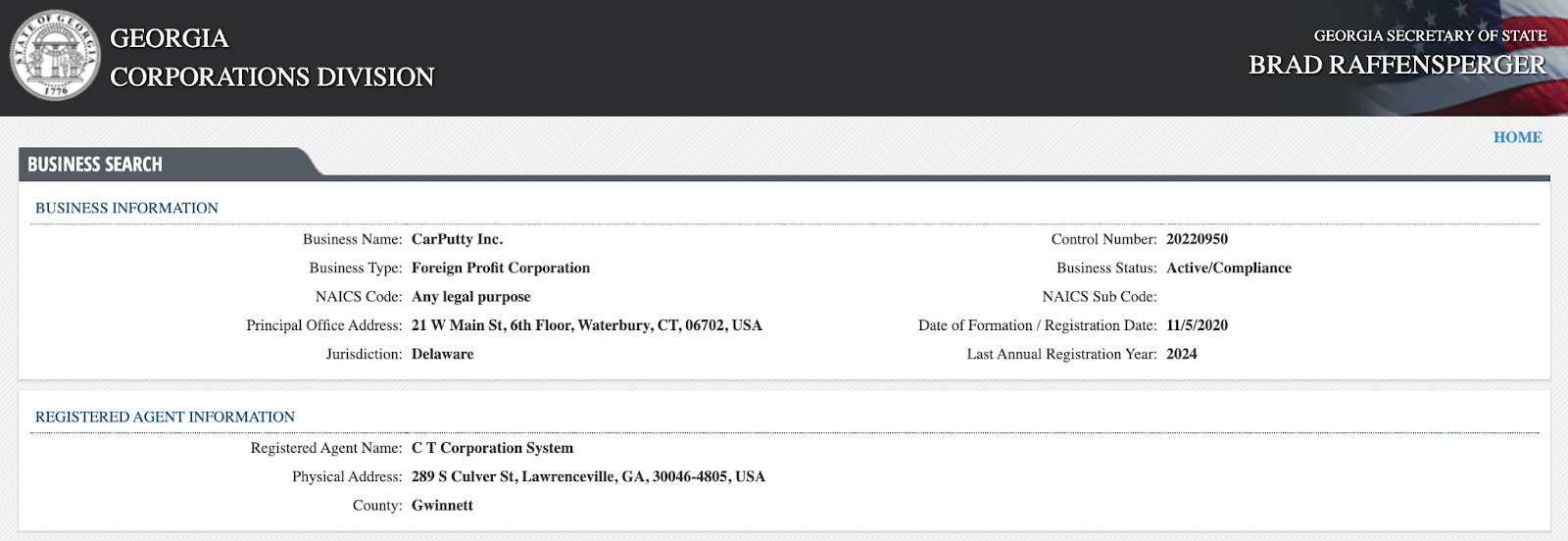

Carputty Inc. is an Atlanta, Georgia-based, private, for-profit company that was founded in 2020 by Joshua Tatum and Patrick Bayliss. According to the Geoigia Corporations Division, the company is active and in good standing.

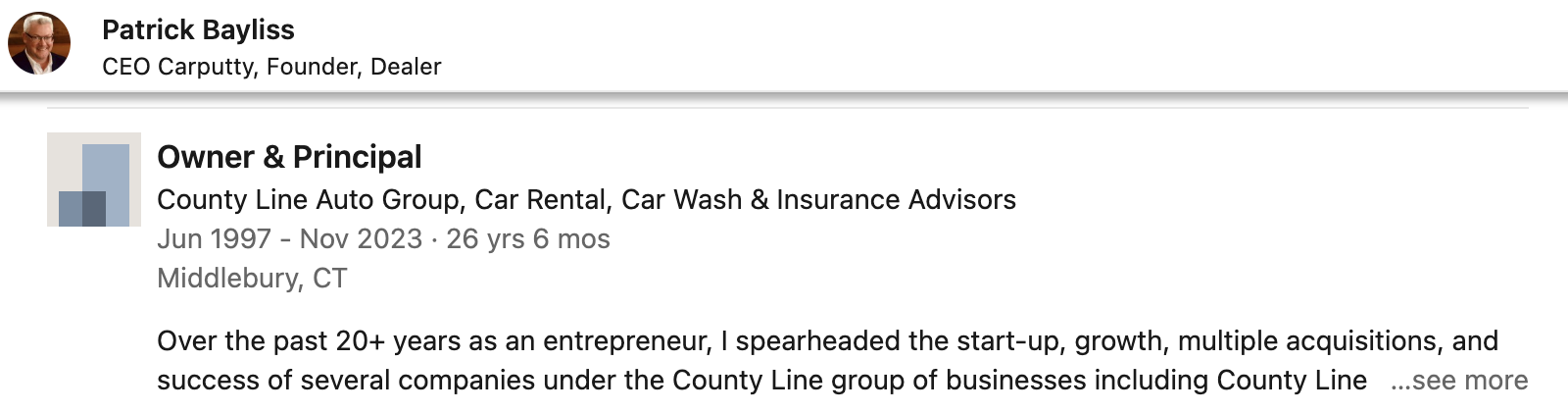

Before launching Carputty, Bayliss (the current CEO) was the owner of County Line Auto Group – a business specialized in car rental, car wash, and insurance – for over 26 years. I would wager he knows his cars.

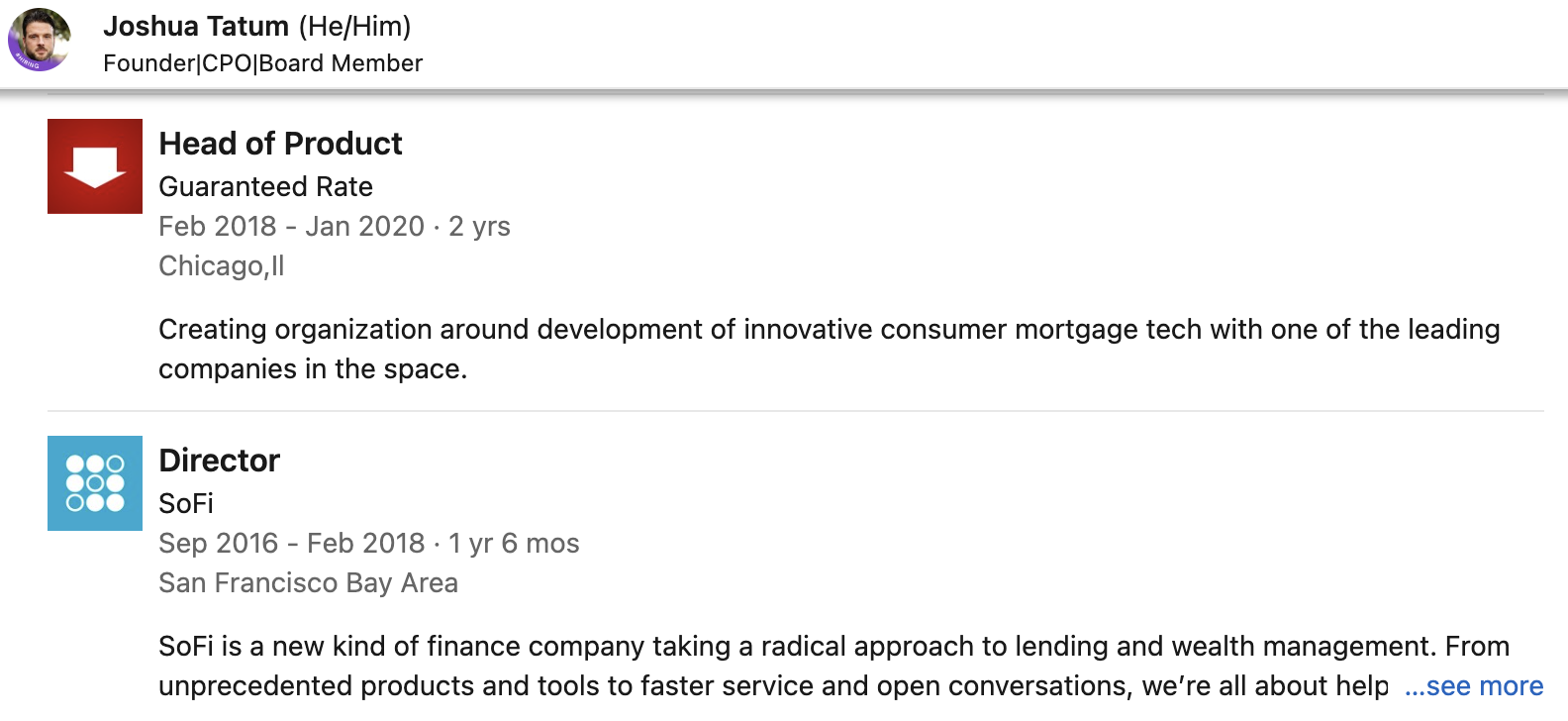

And, Tatum (now CPO) held leadership positions with SoFi® and Guaranteed Rate® before he launched his own technology consulting business around the same time Carputty was born.

In all, the company leadership seems like it would be strong. According to Glassdoor, over half of Carputty’s staff agree—50% would recommend the company to a friend and 66% approve of Bayliss as the CEO.

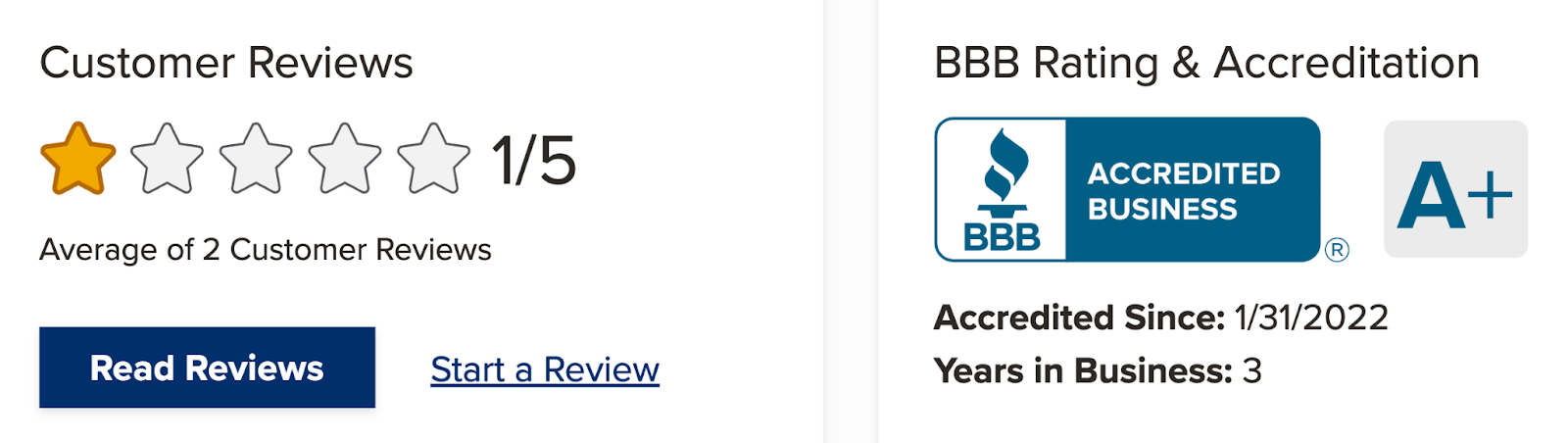

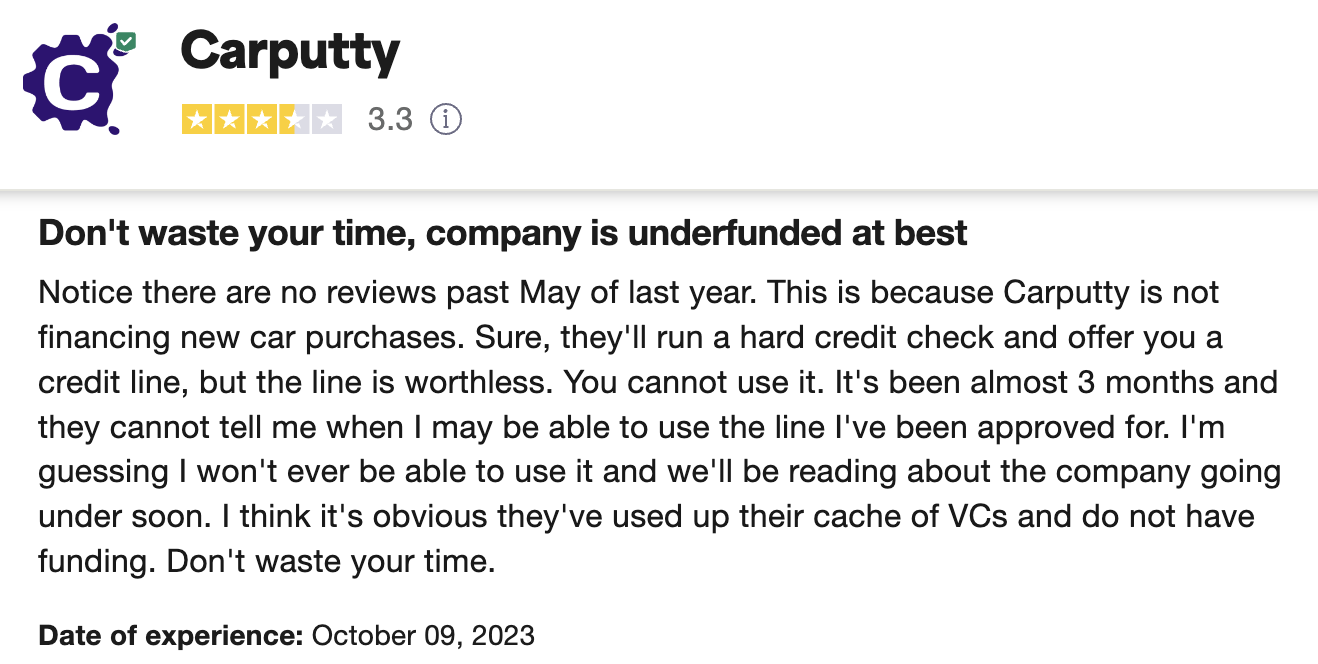

Despite their 1-star rating with the Better Business Bureau (BBB), Carputty is accredited and maintains an A+ rating on the platform. In three years, they’ve had no formal complaints filed with the BBB.

And, Carputty has received mixed Trustpilot reviews—While some customers praise its efficiency and great rates, others have expressed dissatisfaction with issues like delayed processing, excessive fees, and difficulties with the credit line as well as concerns about the company’s funding status. Positive reviewers seem to love their smooth transactions, prompt customer service, and favorable rates.

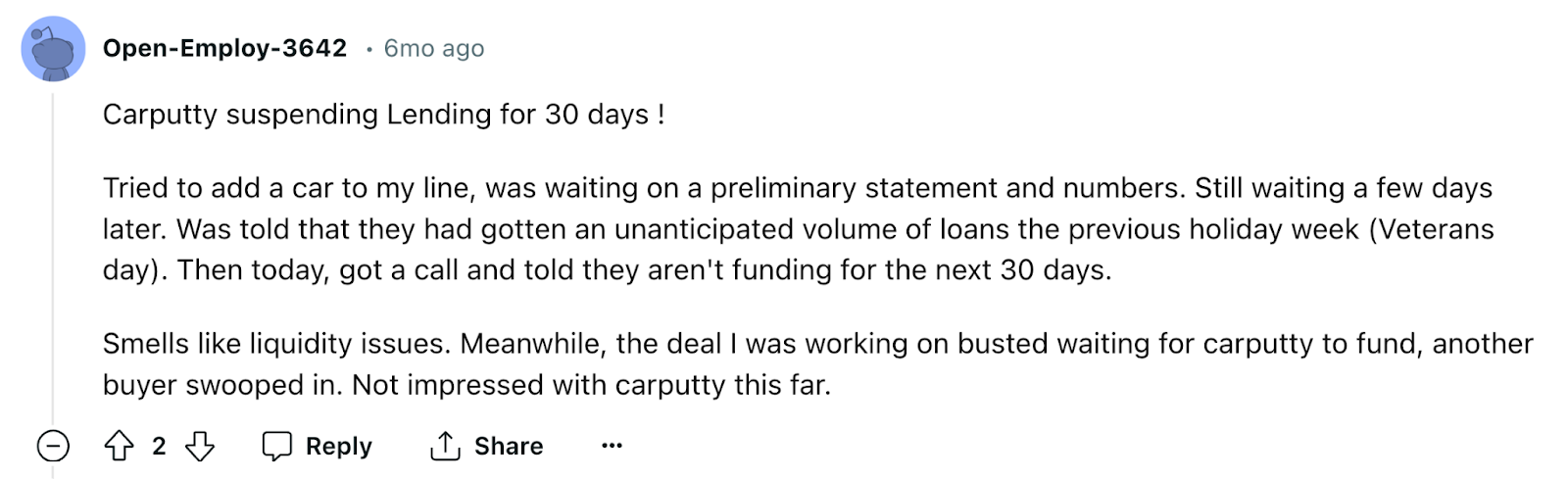

In line with funding status concerns, last year, several borrowers reported that Carputty had temporarily suspended lending. They weren’t able to use their funds to purchase or refinance their loans—-This points to a lack of reliability, and while I can’t speak to the reason why, it could be that they weren’t managing their funds very well at the time.

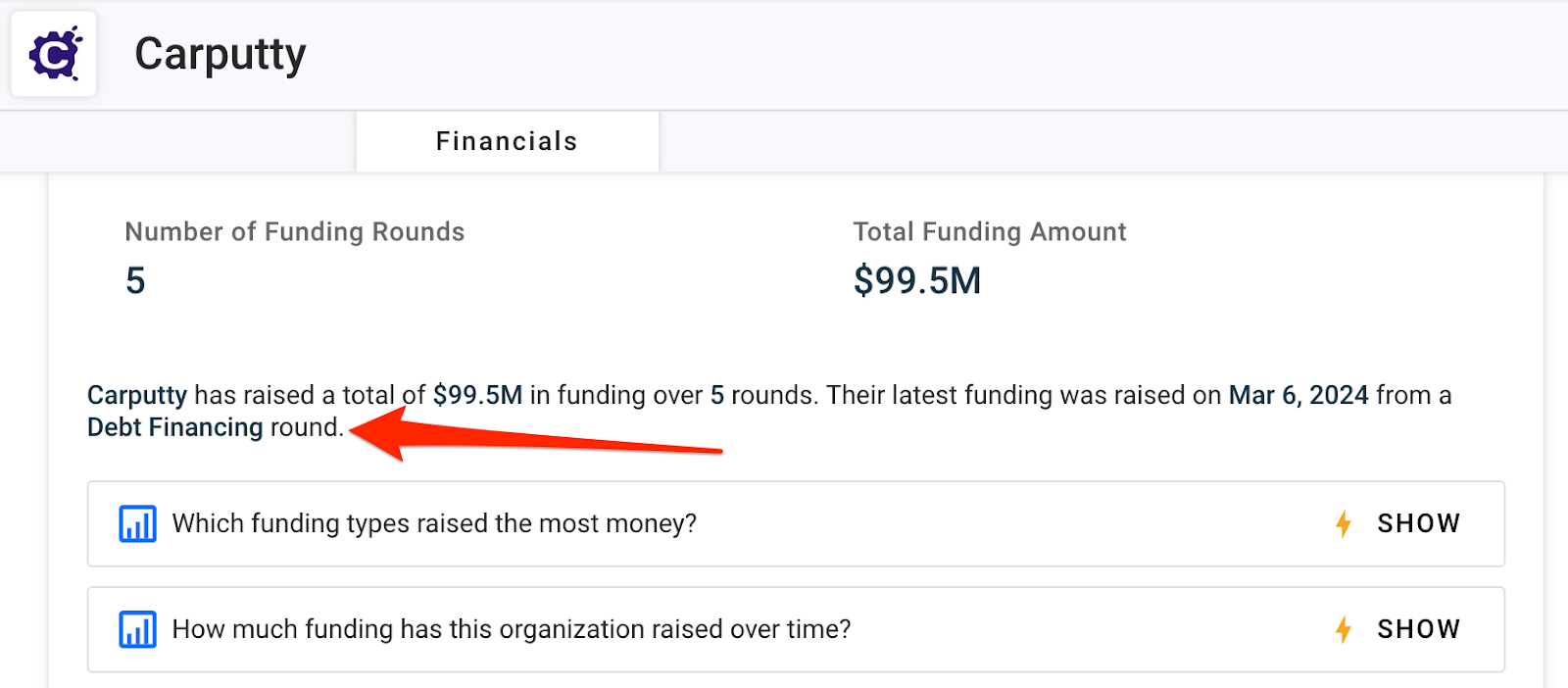

As far as I know, lending is back on track. And, in March 2024, Carputty received a couple rounds of funding from at least eight investors—This brings the total funding amount to $99.5 million.

Now, it may seem like the fact that they received more funding puts them in a financially-healthy position. But, if you look closely, this was debt financing. So, this means that the company obtained a loan from investors in return for a predetermined interest rate, and promised to repay both the loan and interest. If Carputty Inc. fails to meet its repayment obligations, the investors can seize any collateral provided.

I didn’t find any open lawsuits against the company, which is a good sign.

What Does Carputty Do?

Now, take a closer look at exactly what you get with a Carputty account.

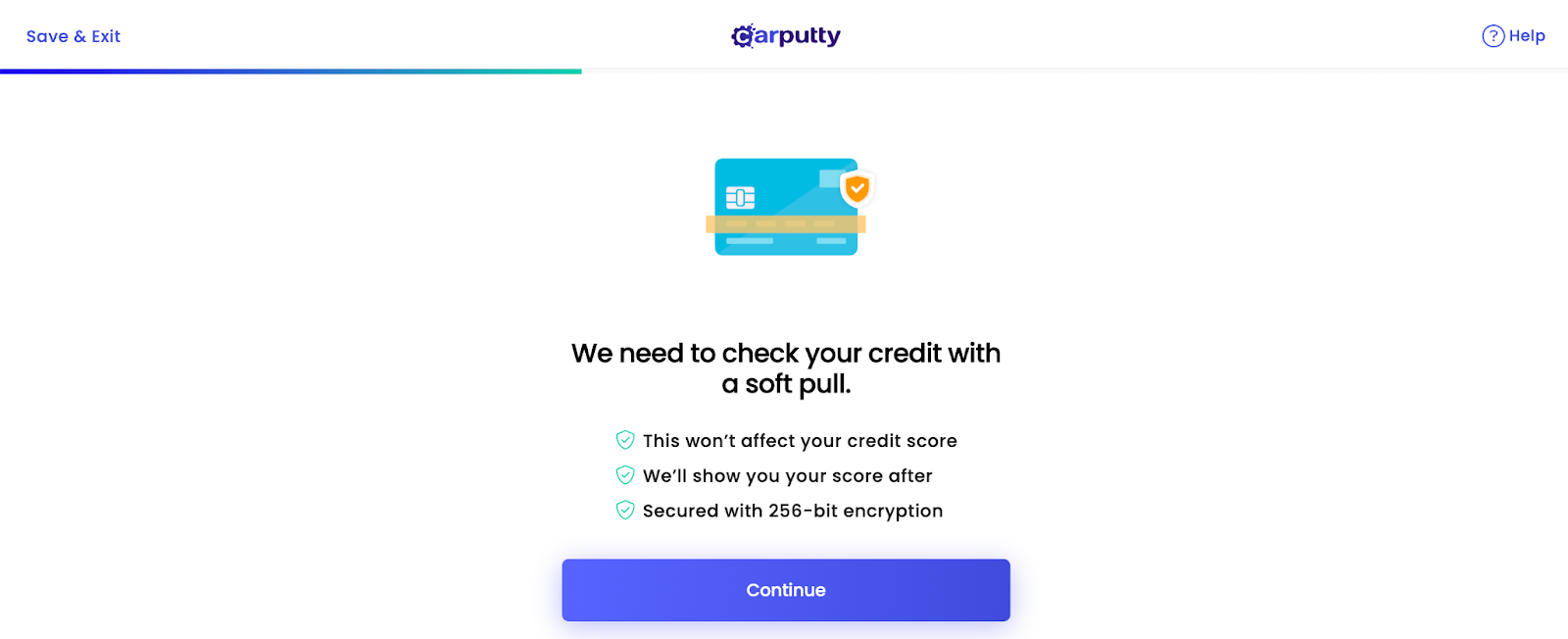

1. Soft Pull for Pre-Approval

Even if you apply as a business (LLC), Carputty will ask for your SSN – this means that they’ll look at your personal credit history. They do not ask for your EIN or DUNS number, which indicates that they aren’t looking at your business credit report or business credit score.

And, while it’s a soft pull, they do ask for proof of income. Plaid is compatible with the platform, but seems like it’s optional. The main benefit to applying as a business will be the higher possible credit limit ($800K) vs lower limit as an individual.

One of my students saw the pre-approval process as a good way to see what type of financials are picked up by tools like Plaid and had a lot of fun with the application process.

There should be no impact to your consumer credit from the initial soft pull—a hard pull will usually dock a few points from your score, but the effects are typically temporary.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

2. Loan Offer & Terms Acceptance

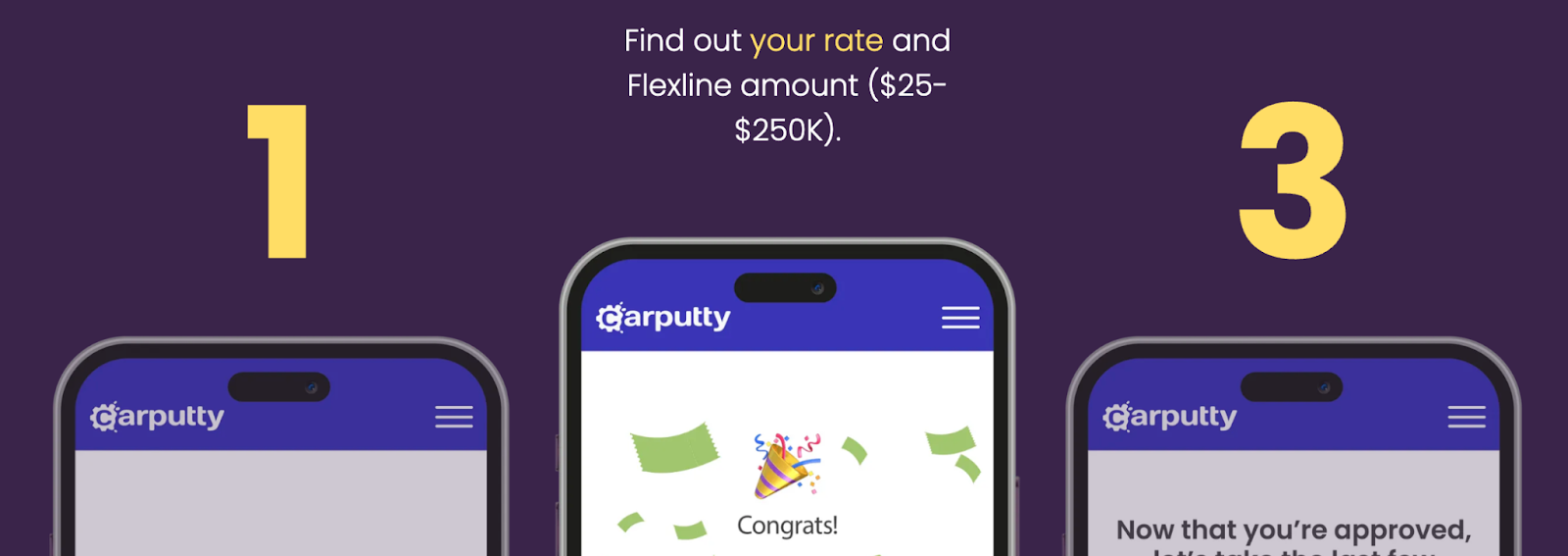

After your application is pre-approved, you’ll be offered a (fixed) rate and Flexline™ amount, from $25K to $250K—And, you don’t have to accept the loan; you can save it for later if you like.

Once you accept a loan offer, Carputty will do a hard pull to your consumer credit. The fixed interest is nice because you will know what you can expect to pay.

Remember: rates start at almost 7%, so it’s a good idea to explore all of your options to see if you might be able to get a better rate from another lender.

You might also like: Is LendingPoint Any Good for Financing? [Lender Review]

3. Online Loan & Vehicle Management

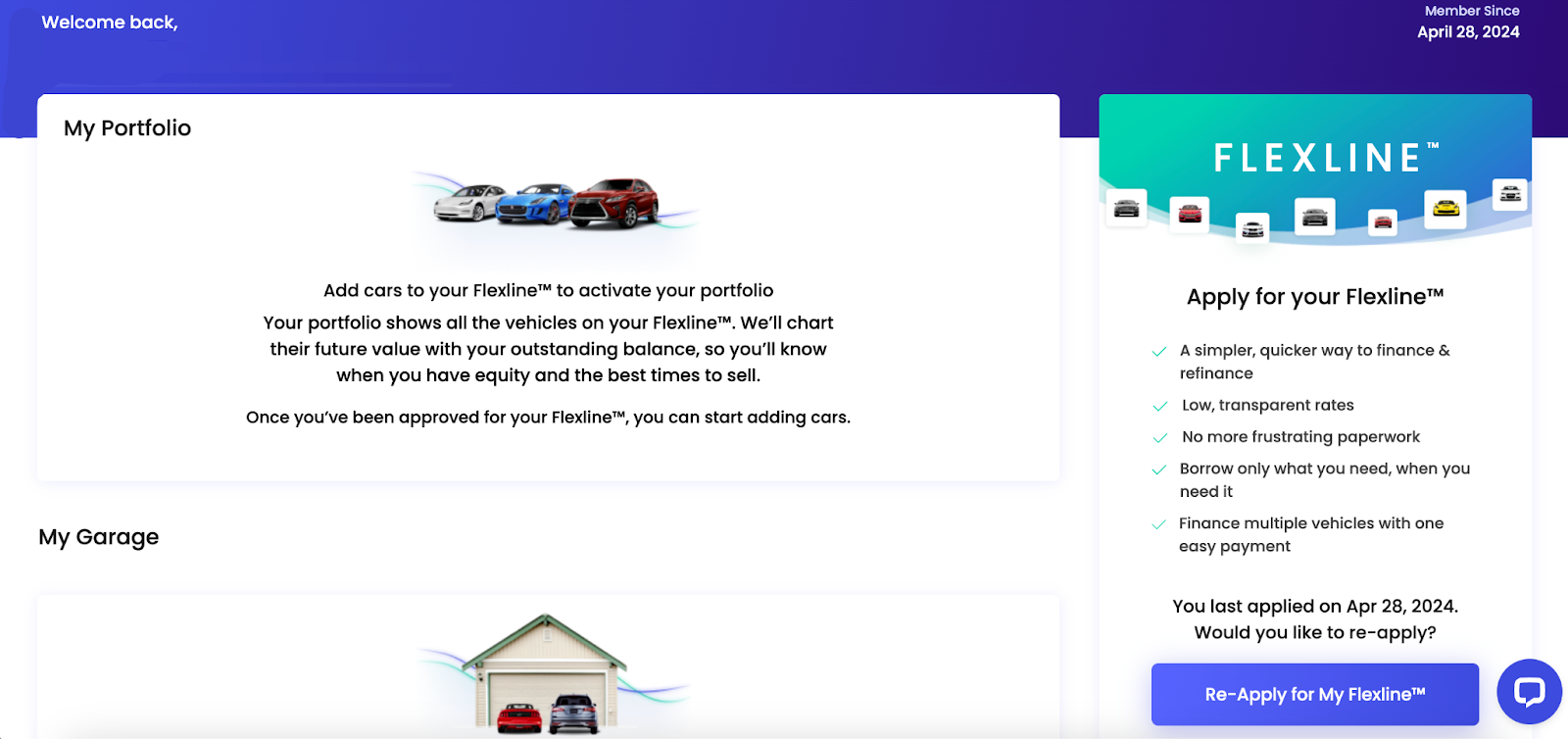

The Flexline™ offers a continuous line of credit of up to $250K for individuals and up to $800K for businesses. Once approved, you won’t need to apply for auto loans again, but you can reapply from your dashboard.

Keep in mind, the Flexline™ is tied to you or your business, not a specific car.

You can manage your vehicles and your loan from one dashboard, which is super convenient and informative.

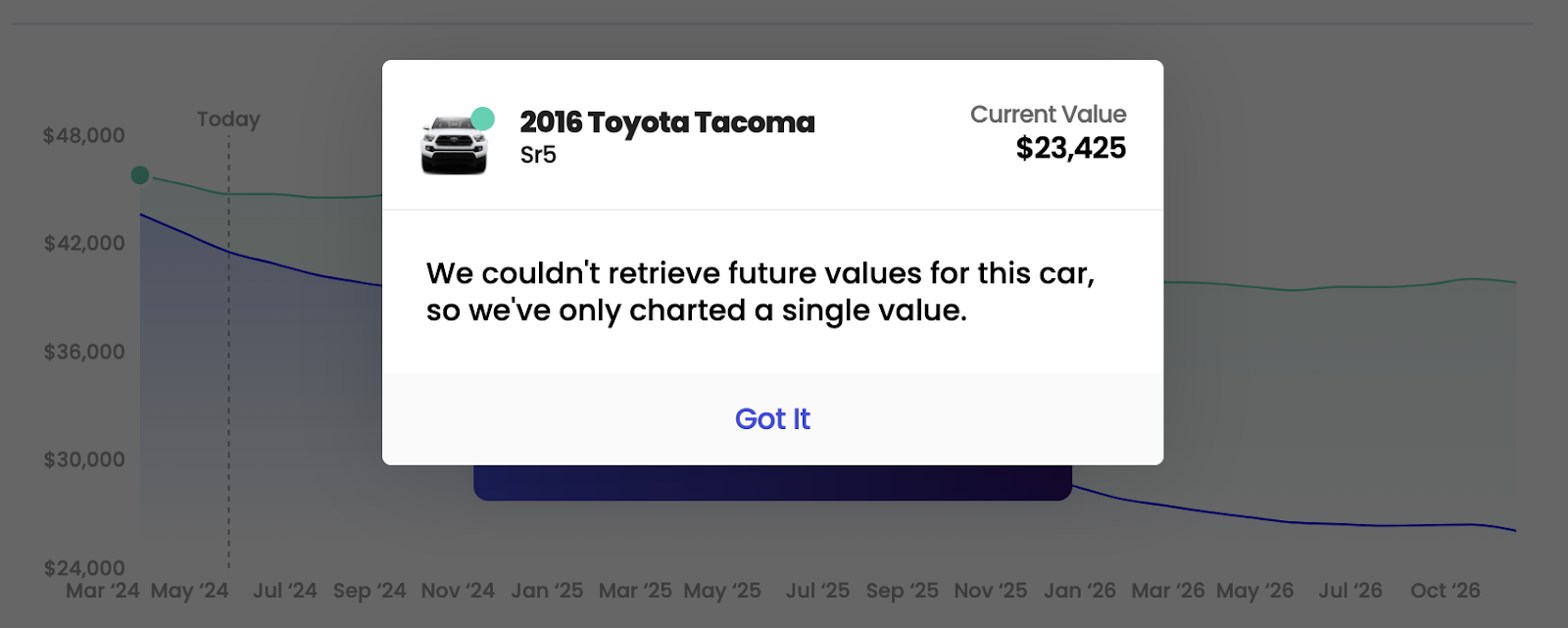

4. Automotive Value Tracking

In your Carputty dashboard, you can input your vehicle’s VIN and mileage for long-term value tracking. Similar offers are available with popular consumer financial tools like Credit Karma® and Rocket Money®. Here, it’s even more relevant and adds a nice touch—plus the algorithm is original.

The V³ Valuation™ tool should reveal upcoming shifts in your vehicle’s worth to give you insights to make informed and optimal buying and selling decisions. By analyzing over a million data points sourced from auctions, dealerships, and private sales, they try to provide precise and impartial valuations.

Historical values aren’t available for all vehicles.

I think this feature would be particularly helpful for a small car dealership, but I can also see how it would be beneficial in any type of fleet management. Plus, you can take advantage of the valuation tool even if you haven’t qualified for the loan.

5. Make Informed Purchases or Refinance Old Loans

Once you’ve selected the desired car, add it to your dashboard to initiate a new purchase or refinance. Follow the prompts on the screen, and the platform will guide you through the process. “Member success agents” are available to help you with the process and they oversee every step, from document submission to fund transfer and title transfer.

Please be aware that presently, Carputty exclusively facilitates used car purchases through authorized dealerships. A Carputty Flexline™ cannot be used for private sales.

You might also like: Is Dell Business Credit Worth Your Time?

Frequently Asked Questions

What states does Carputty operate in?

Carputty currently operates in Alaska, Alabama, Arkansas, Arizona, Colorado, Connecticut, Washington D.C., Delaware, Florida, Georgia, Hawaii, Iowa, Idaho, Illinois, Indiana, Kansas, Kentucky, Louisiana, Massachusetts, Maryland, Maine, Michigan, Minnesota, Missouri, Montana, North Carolina, North Dakota, Nebraska, New Hampshire, New Jersey, New Mexico, New York, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, Vermont, Wisconsin, West Virginia, and Wyoming.

Does Carputty do a hard pull?

Carputty does not perform a hard credit pull during the pre-approval process. They use a soft credit inquiry, which does not impact your credit score. However, final approval does involve a hard credit pull.

Conclusion: Is Carputty Worth it?

Carputty offers a unique approach to auto financing with its Flexline™ product. It provides a flexible line of credit that can be used for various automotive transactions. You can buy out a lease, refinance, or purchase eligible vehicles. The interest rates start at 6.83%, which may be competitive compared to other lenders.

The company has received mixed reviews, with some customers praising its efficiency and rates, while others have expressed concerns about delayed processing and difficulties with the credit line. Carputty operates in a wide range of states and does not perform a hard credit pull during the pre-approval process.

Overall, whether Carputty is worth it depends on your circumstances, including credit score, financial needs, and preferences. My advice is to carefully review the terms, rates, and customer feedback before deciding if Carputty is the right fit for you.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!