You’re looking for a way to get fast cash flow. If you haven’t invested in building your business credit or your have a low personal FICO score, your options could be limited. Enter LendingPoint, a lender that caters to people with less than ideal credit, offering personal loans for various uses.

Furthermore, this lender provides an option for merchants to extend financing to their customers and clients, which sounds awesome. So, are they legit?

Here’s what’s in store:

- What is LendingPoint?

- LendingPoint Loan Overview

- LendingPoint Merchant Solutions Overview

- Conclusion

So, keep reading to learn more.

What is LendingPoint?

Founded July 2014, LendingPoint is positioned as a lender for those with lower credit scores who can prove their dependability in other ways: income, credit behavior, job history. LendingPoint’s core offer includes personal loans up to $25K. The company is based in Kannesaw, Georgia. Tom Burnside is the CEO and co-founder.

Before founding LendingPoint, according to his LinkedIn profile, Burnside spent 13 years as the President and Chief Operating Officer (COO) of Capital Access Network (now known as CAN Capital). There, he was responsible for design, development, and implementation of their unique credit scoring model.

LendingPoint’s loans are designed for multiple uses, such as unexpected urgent expenses, debt consolidation, medical or dental costss, home improvement, travel, taxes, wedding, or other personal financial reasons. And, to date, the company has loaned over $1.8 billion in the United States.

| Note: Some people get LendingPoint confused with Lending Club. A few years back, the CEO of the latter was involved in a scandal, which discredited the company’s trustworthiness to investors. These two businesses are unrelated. |

LendingPoint Loan Overview

As a funding solution, LendingPoint gets some pretty rave reviews. On the other hand, there are naysayers. So, what can you expect from personal loans? Here’s everything you need to know, including costs, requirements, and a quick look at competitors.

First, LendingPoint is a direct lender in certain states, meaning they sometimes use their own, private funds to finance borrowers. In other cases, they may offer financing extended from another source like FinWise Bank.

LendingPoint Pricing

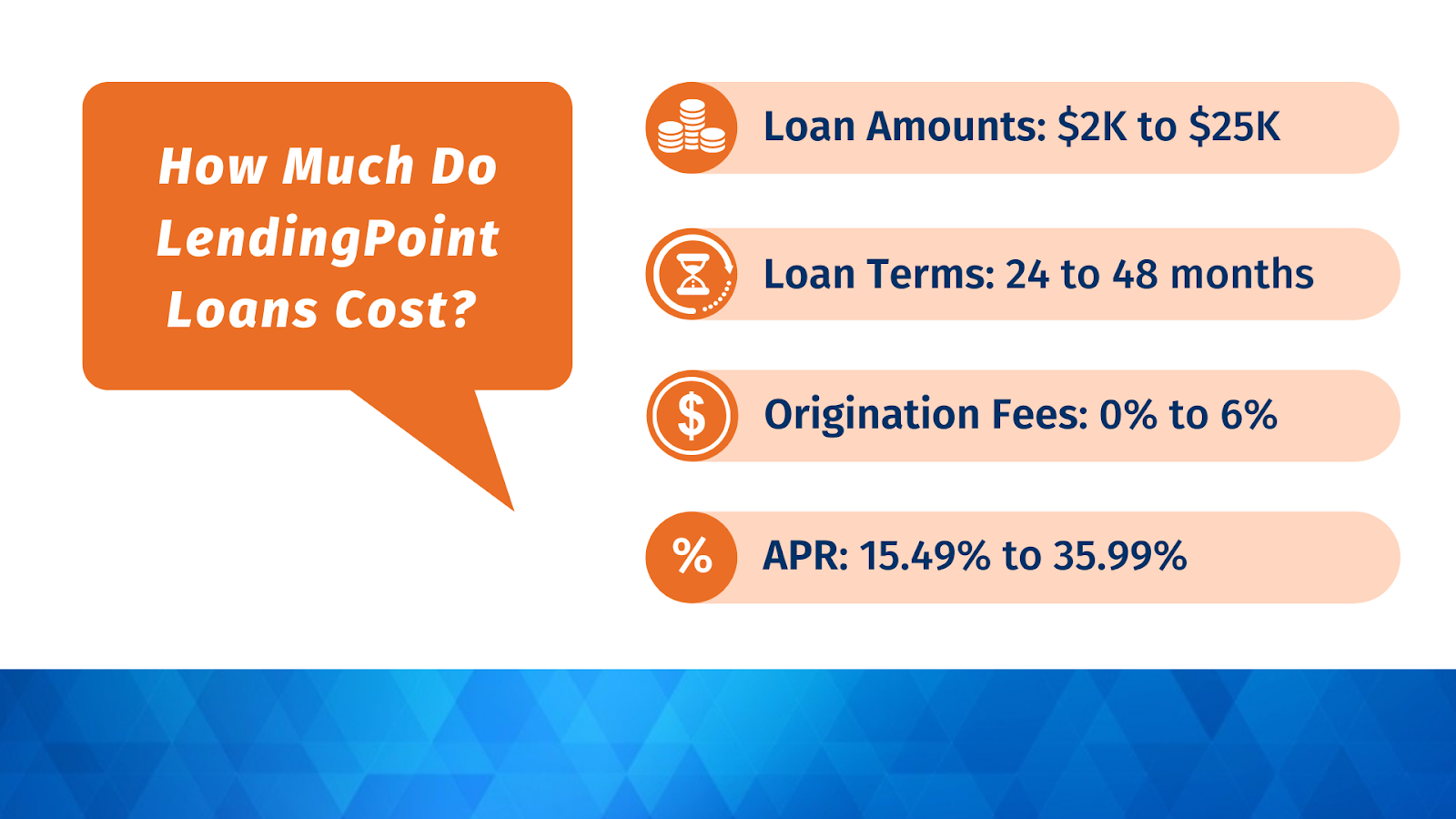

As with all funding providers, there are layers to LendingPoint’s pricing. Let’s take a examine the costs of their funding. Loan amounts range from $2K to $25K with terms from 24 to 48 months. Origination fees range from 0% to 6% with interest rates between 15.49% and 35.99%.

So, if you take out a $10K loan with a 6% interest rate, the total amount owed with fees might be $12,700. In this scenario, monthly payments at 24.098% APR with 24-month terms should be around $530 per month. You could be offered the option to deduct the origination fee from the dispersed amount if desired.

You might also like: Torro Business Funding Review: Is This “Zero Hassle” Offer Legit?

Does LendingPoint Report to Credit Bureaus?

According to Experian, LendingPoint promises to report to one or more personal credit bureau(s), not all three. So, on-time payments toward a LendingPoint loan can essentially help you improve or maintain your personal credit with at least one bureau. Furthermore, they do not report payments to business credit bureaus.

How to Qualify for a LendingPoint Loan

While LendingPoint is positioned as a funding option for those with “fair credit,” not just anyone will qualify. As stated previously, you will need to prove your creditworthiness through other means.

A credit score of at least 585 is a must for LendingPoint. So, if your score is lower than this, you’ll need to look elsewhere for funding. Furthermore, the lender will take into account your income, the intended use of funds, and other details to get a clear picture of your ability to repay the funds.

Bankruptcy within the last 12 months could disqualify you, but older bankruptcies may be okay. Other immediate edisqualifying factors could be too many recent credit inquiries, annual income lower than $35K, and the inability to verify income or identity.

Related Reading: Credit Secrets Book Review: Can You Erase Bad Credit History?

LendingPoint does not do a hard inquiry on your credit when prequalifying borrowers. Instead, they do a soft-pull. So, checking out what you might qualify for will not impact your credit score and other potential lenders will not see that you applied for funding.

How Long Does LendingPoint Take to Approve?

After you apply for a loan through LendingPoint, you’ll be asked to share documentation that proves your ability to repay the loan and your identity.

- Your social security number

- A federal, state, or local government-issued photo ID

- A verifiable personal bank account

- Proof of annual income of $35K or more

Once your full application is complete, you will know within a week and in ass little as 24-hours if you have been approved. Then, your funds should be dispersed by the next business day.

LendingPoint Merchant Solutions Overview

If you’re a business owner interested in working with LendingPoint, their merchant solutions offer might be right up your alley. Through the platform, you may be able to offer financing to your clients and customers.

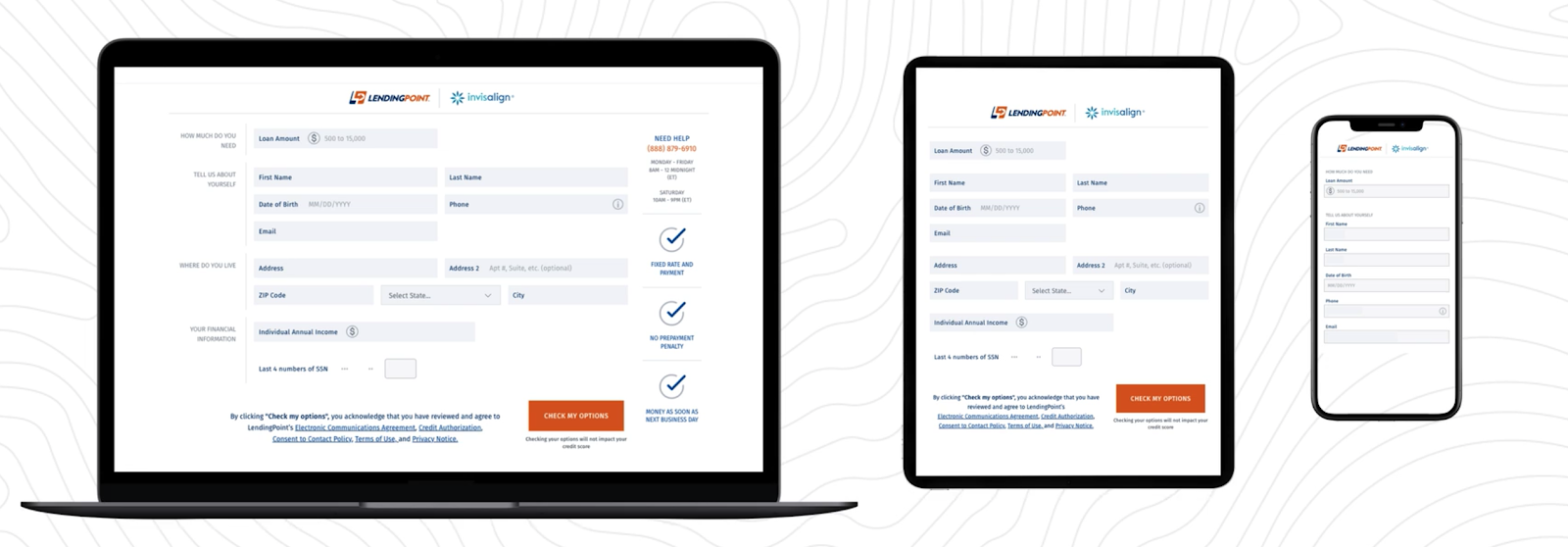

For example, one of the most popular LendignPoint partnerships is with Invisalign. Patients seeking clear teeth aligners without the cash to pay upfront can access LendingPoint’s offer from Invisalign’s brand website. As of August, 2020, eBay has partnered with the lender to bring a new “buy now, pay later” solution to their shoppers.

Instead of a $5,000 pricetag, your offer could instead be ~$250 per month. To consumers, sometimes a smaller monthly payment is a better deal. So, this might make sense when you’re trying to grow, scale, and just increase your sales.

The Benefits of Merchant Solutions

If you opt to add financing to your offer, LendingPoint Merchant Solutions can make it simple. First, applicants can apply from any device, including their own phone or a tablet that you provide in-office.

Next, the qualification terms are pretty easy. The brand marketing materials boast “more approvals” for consumers.

And, your clients and customers can check their rate (prequalify) before applying. So, there’s minimal risk to them.

LendingPoint Alternatives for Merchants

Before you dive into a commitment, it’s smart to explore your options. Here are a couple of choices to explore (there are many other solutions out there). Side-by-side, this is what your customers might expect from each:

| Loan Amounts | Loan Terms | Origination Fees | Interest Rates | |

| LendingPoint Merchant Solutions | $2K to $25K | 24 to 48 months | 0% to 6% | 15.49% to 35.99% |

| Acima Credit | $500 to $5K | 90 days, 12, 18, or 24 months | $25+ | Unlisted |

| FinanceIt | Up to $60K | Varies | $0 | 6.99% to 14.99% |

Conclusion

So, is LendingPoint good for funding? If it’s the only lender you might be able to qualify with and you’re in need of quick cash, sure. LendingPoint offers a competitive personal loan offer for consumers with fair credit.

Now, you if you’re looking for a way to provide your clients and customers with financing between $2K and $25K to purchase your products and services now and pay over time, LendingPoint Merchant Solutions could be an excellent source. I do recommend you explore further.

And, if you want to learn how to obtain no-doc lines of credit up to $100K for your company, join Business Credit Workshop today.