If your debt is stressing you out, you’re not alone. According to Forbes, 54% of Americans are stressed about their debt. And, if you’re in this boat, you may have come across National Debt Relief – which sounds almost like a way to eliminate debt altogether.

As with any offer that affects your finances, you need to know whether this is a legitimate offer before you sign up. So, I’m going to share everything I know. We’ll look at what National Debt Relief is, what they can do for you, and the services they offer. By the end, you should know if this is the right offer for you.

This is what’s in store:

- What is National Debt Relief?

- What Does National Debt Relief Do?

- Frequently Asked Questions

- Conclusion: Is National Debt Relief Legit?

Now, let’s set sail!

What is National Debt Relief?

National Debt Relief is a company that helps people tackle their debt through various debt relief services.

Depending on your situation, services might include:

- Negotiation with creditors

- Debt consolidation loans

- Credit counseling services

- Bankruptcy referrals

They provide a free consultation where you can discuss your financial situation and explore your options…allegedly without any obligation.

While they don’t offer tax debt relief or any government loans, they cover nearly every other type of debt you can think of.

This includes relief from:

- Credit card debt

- Personal loans

- Bad credit debt

- Medical debt

- Unemployment debt

- Retirement debt

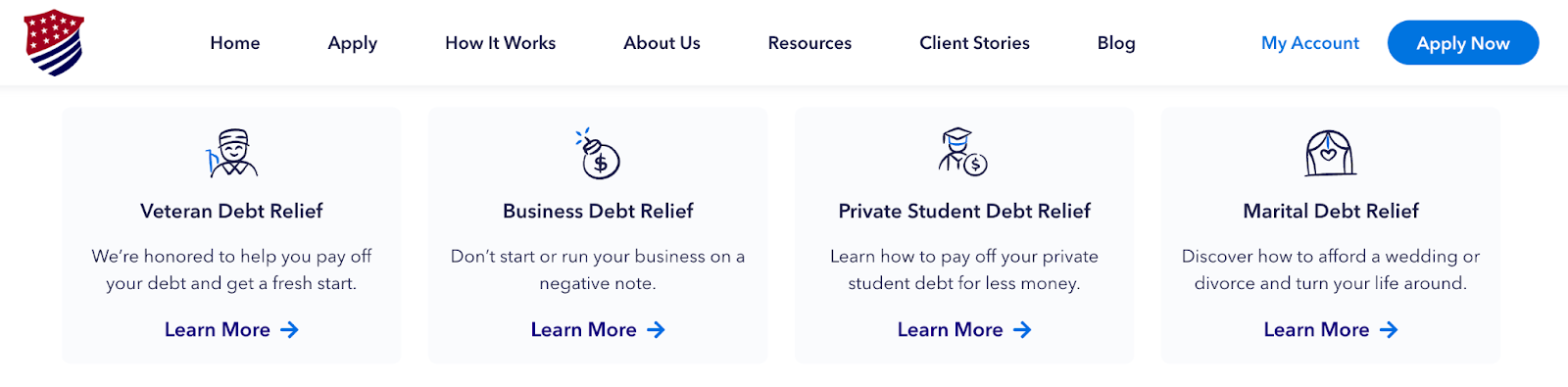

- Veteran debt

- Business debt

- Private student loans

- Marital debt (wedding or divorce)

Ultimately, National Debt Relief aims to help you become debt-free within a reasonable timeframe, typically within 24-48 months. They emphasize affordability and customization, ensuring that their solutions align with your budget and financial goals.

Recommended: Credit Secrets Book Review: Can You Erase Bad Credit History?

Where Does National Debt Relief Operate?

As of March, 2024, and despite what the brand’s name implies, National Debt Relief doesn’t operate in all 50 states (I wouldn’t have known this if I didn’t call in to ask a few questions about pricing). When I asked which states they do operate in, the rep advised that I do a search for debt relief specifically in my state so I didn’t get a straight answer…not right away.

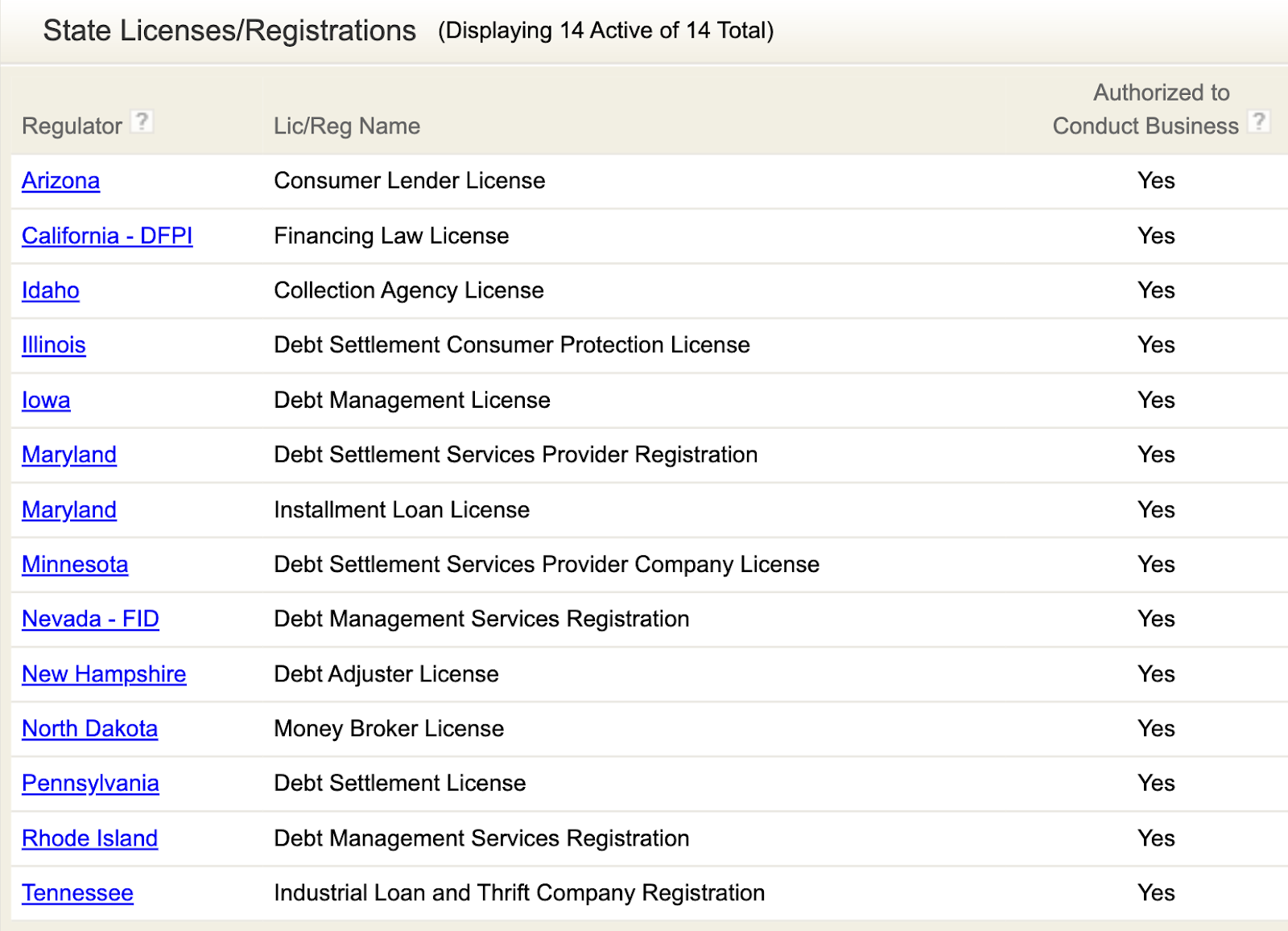

So, after the call, I put my research cap back on and checked with the Nationwide Multistate Licensing System. I found that National Debt Relief holds 14 state licenses in 13 states.

I can verify that they do legally operate in:

- Arizona

- California

- Idaho

- Illinois

- Iowa

- Maryland

- Minnesota

- Nevada

- New Hampshire

- North Dakota

- Pennsylvania

- Rhode Island

- Tennessee

And, in Illinois, Iowa, Maryland, Minnesota, New Hampshire, Pennsylvania, and Rhode Island, the company actively holds debt-specific licensing.

While you can apply for a consultation regardless of your location, you may be limited in the scope of services offered if you live outside of the states where they maintain licensure.

How Does National Debt Relief Work?

At first glance, it may seem like you’ll sign up to have your debt reduced without any work. But, that is not how these programs work.

So, here’s how national debt relief really works…

…First of all, their approach starts with a personalized debt relief plan tailored to your unique circumstances.

This might include negotiating with creditors to reduce the amount you owe and setting up a dedicated savings account where you make monthly deposits. These funds are then used to pay off your creditors at the negotiated reduced amounts.

Some participants might be offered a debt consolidation loan. The idea is that you would consolidate your high-interest debts into a new loan with a lower interest rate and pay less over time.

While the company boasts that you can be back to financial freedom and living your life within 24-48 months, that doesn’t mean you will be out of debt within 4 years. For example, a consolidation loan might take 7 years to pay off, but your payments or interest would hopefully be lowered.

There’s even a chance you’ll be referred to a bankruptcy attorney. In this case, some or all of your debt may be wiped out, but this could have a negative impact on your credit score for several years.

Keep in mind, debt relief is not the same as credit repair, and may have a negative impact on your credit score (many so-called credit repair programs can have a negative impact on your credit as well). And, you will need at least $7.5K in debt to qualify for their services.

You might also like: Superior Tradelines Review: Is it a Scam or Legit Way to Build Credit?

How Much Does National Debt Relief Get Paid?

National Debt Relief charges a fee for their services, which is typically based on a percentage of the enrolled debt. This fee can vary depending on factors such as the state you reside in and the total amount of debt you owe.

On average, the fee usually falls within the range of 15% to 25% of the total enrolled debt. For example, if you enroll $10,000 in debt and the fee is 20%, then the fee would amount to $2,000.

Now, when I called in and asked specifics about the costs, the rep that I spoke with only disclosed that the fee is “built-in” to the plan and no services are rendered until all fees are agreed to.

So, if you make it to the proposal stage, do your own math before you sign up — Make sure that the amount you pay will in-fact be less than the interest and principal you would otherwise pay on your debts. And, keep in mind that debt settlement often has a negative impact on your credit report, and negative marks can remain for up to seven years.

It’s important to note that National Debt Relief operates on a performance-based fee structure – This means they are only supposed to collect their fee after they successfully negotiate a settlement with your creditors. Again, you will have the chance to approve the cost and the savings.

You might also like: A Credit Stacking Breakdown: What it is & How it Works

Company Overview

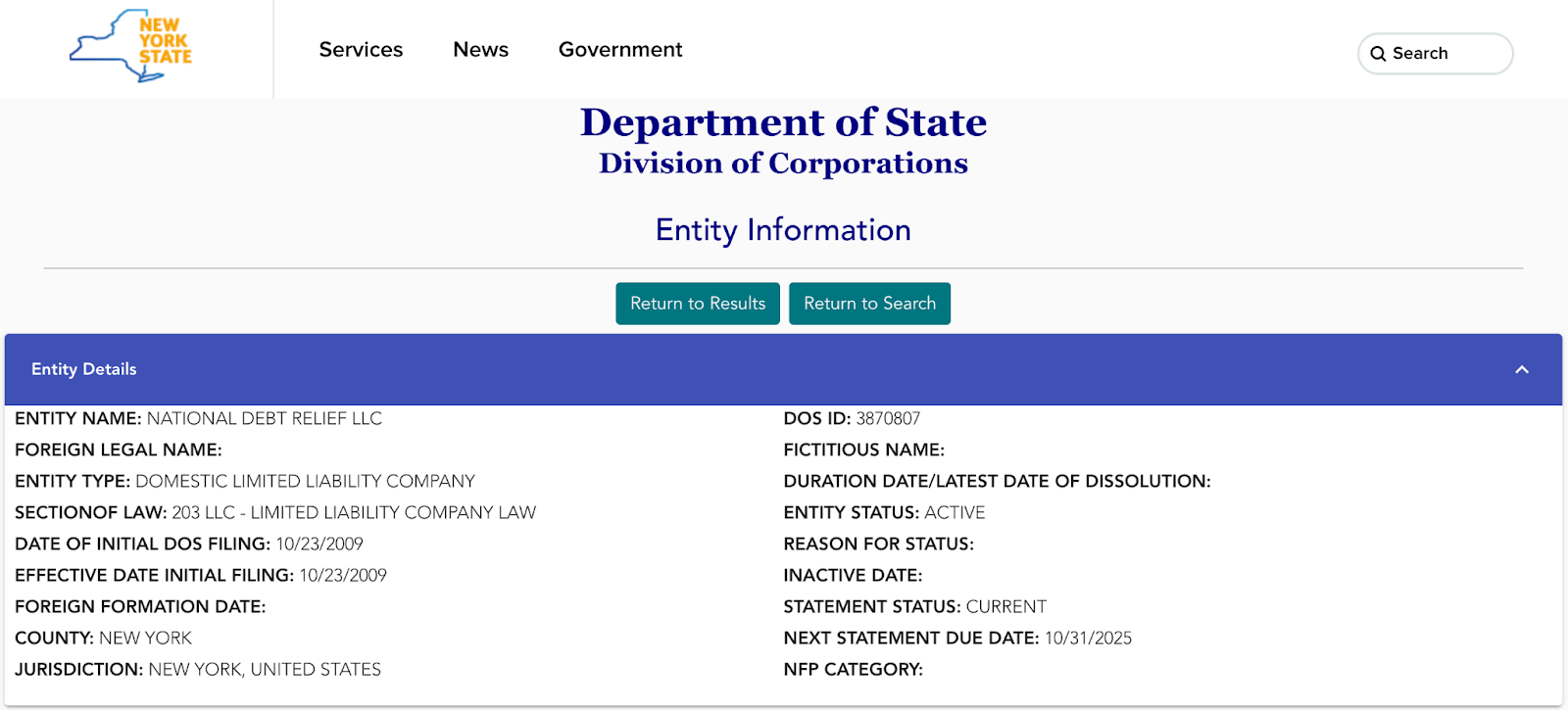

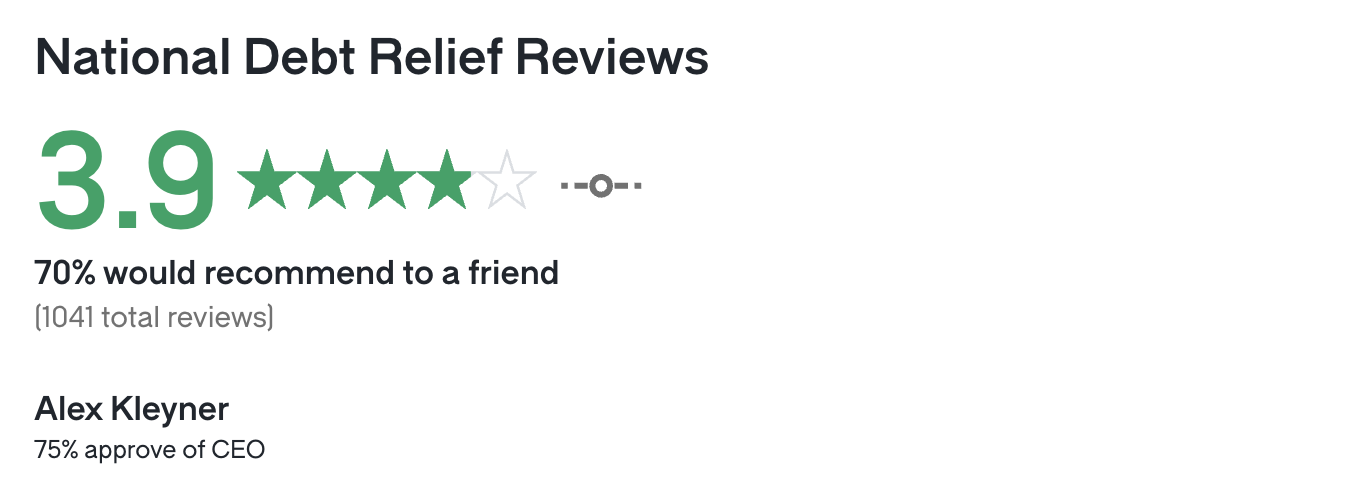

National Debt Relief LLC is a New York-based company that was founded in 2009 by Alex Kleyner, Daniel Tilipman, Tom Leydiker. Kleyner is the current CEO, where he’s been full-time for the past 15+ years.

Prior to launching the company, Kleyner received a Bachelor’s degree from Pace University

Tilipman remains on National Debt Relief’s executive board, and went on to found Reach Financial — a debt consolidation loan provider — in 2022. This makes me wonder if National Debt Relief offers consolidation loans in partnership with Reach.

Leydiker is also still with the company. Before co-founding the company, he was a branch manager at Citibank and President and CEO of Continental Funding, LLC.

The leadership seems strong, especially considering that most employees (according to Glassdoor) would recommend the company to a friend in need of a job. What staff thinks of a company speaks volumes, and 75% of National Debt Relief’s Workers approve of the CEO.

With that said, you also have to look at what clients think of a company before you can really judge. Like all financial offers, National Debt Relief gets mixed reviews.

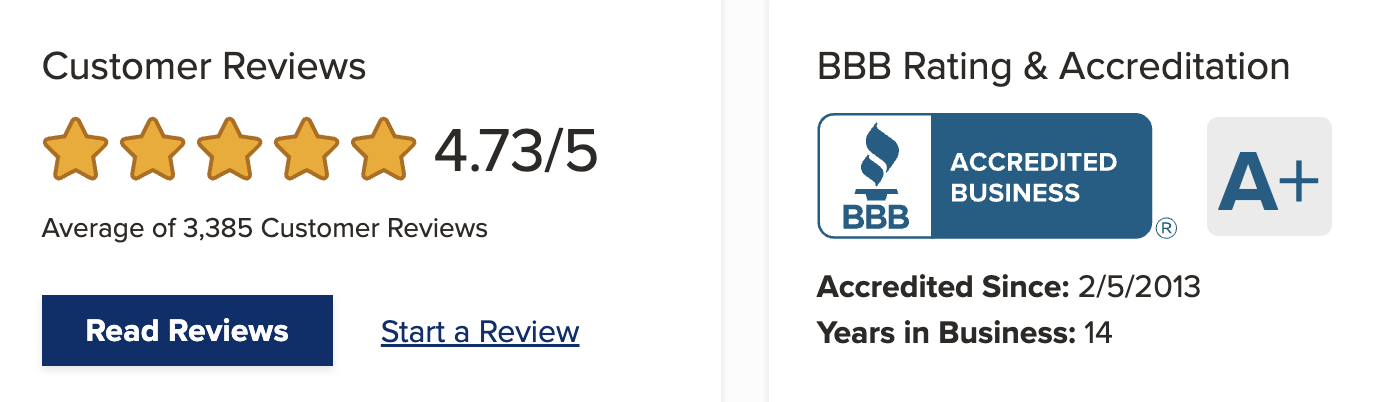

They are A+ rated and accredited with the Better Business Bureau (BBB), but this is despite 124 complaints in the past year. Still, 3,385 customers give them a 4.73-star rating. I do like these numbers.

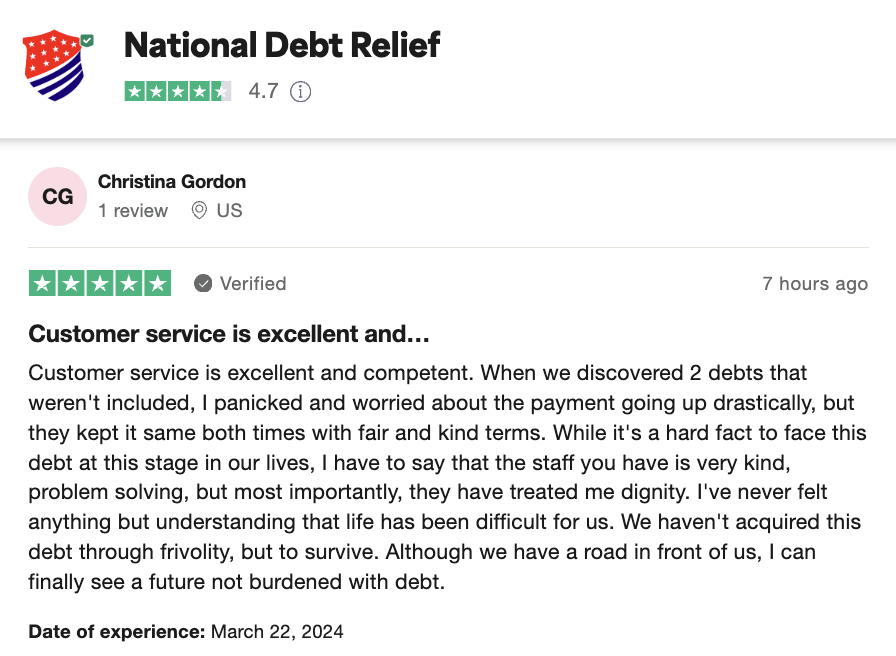

National Debt Relief is rated nearly as high on Trustpilot (4.7 stars) and platform reviewers are mostly very satisfied with the services they receive.

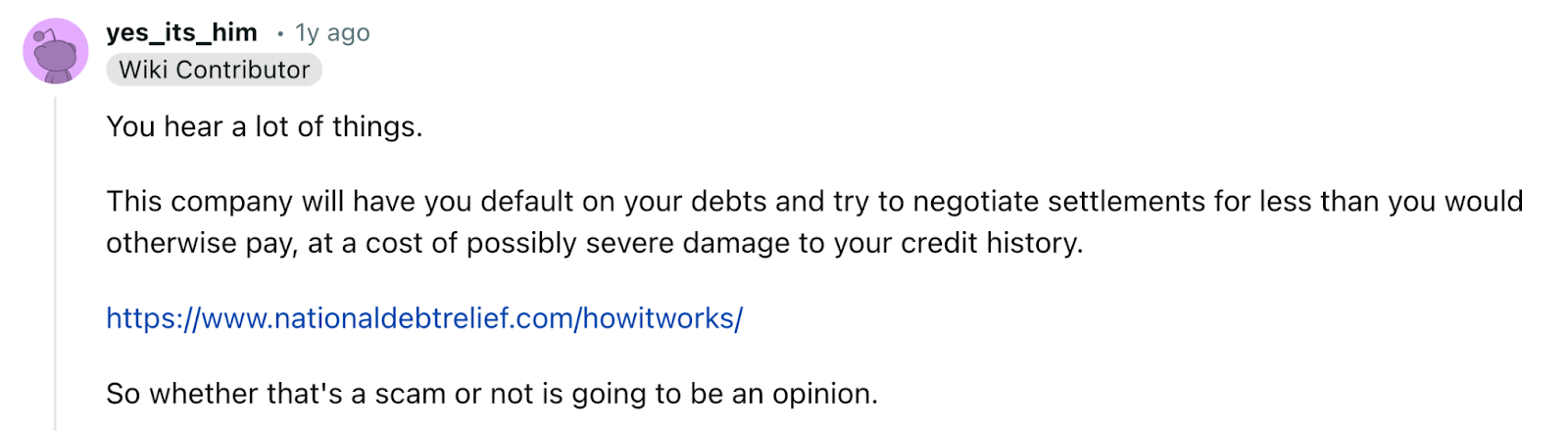

Plus, even Redditors have generally objective opinions about the company – they are typically the toughest crowd on the internet to impress.

Note that some anonymous commenters do recommend you side-step these guys and go straight to a government agency or attorney for your own protection (which are definitely avenues worth exploring).

Now, there is a new class action lawsuit against National Debt Relief that claims they collect users’ IP addresses without consent – note, this has nothing to do with the way they handle clients’ finances. And, keep in mind, the jury is still out…literally.

Before you decide if this is the offer for you, find out exactly what National Debt Relief can do to help provide relief from debt.

You might also like: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

What Does National Debt Relief Do?

Some of National Debt Relief’s services are offered in-house and other advertised relief solutions are made by referral. Now, I didn’t see any affiliate links or affiliate disclosures on their site – this could mean that they will refer you out to someone without earning any commission, but I can’t be sure.

Here’s what you might expect if you sign up.

You might also like: No-Doc Business Loans: Get Funds Without Proof of Income

1. Free Consultation

If you reach out and apply for services from National Debt Relief, the first thing you can expect is a call from a rep who will listen to your situation, ask questions and start to formulate a plan.

At this stage, I only recommend you watch out for high-pressure sales tactics. This is always a bad sign. But, a phone call is a low-risk way to explore whether an offer is going to be a good fit for you. Your mantra for any sales call should be, “I’m in the driver’s seat.”

2. Personalized Debt Relief Plan

National Debt Relief will need to know about all of your debts before they can make a recommendation on how to tackle them.

So, list out all of your debts:

- Credit cards

- Lines of credit

- Personal loans

- Medical bills

- Collections

- Repossessions

- Student loans

- Business debts

And, be prepared to let the rep take some time to come up with a tailored plan.

3. Credit Counseling & Education

Credit counseling might be beneficial if you are able to make monthly payments, but struggle with debt management. It’s ideal if you’re seeking a structured plan to handle debt effectively, negotiate lower interest rates, and consolidate payments.

Additionally, counseling offers valuable financial education on budgeting and responsible credit use. Credit counseling might be suitable if you want to avoid bankruptcy and are willing to actively participate in the counseling process to achieve financial stability.

In addition to the counseling services they offer, National Debt Relief offers quite a few educational resources – primarily a comprehensive blog that discusses all matters debt, lifestyle, and financial wellness-related. If you want to learn about debt consolidation, or bankruptcy, their blog is full of useful information.

Plus, their articles are laid out in a way that’s simple to navigate and written in an easy-to-understand tone.

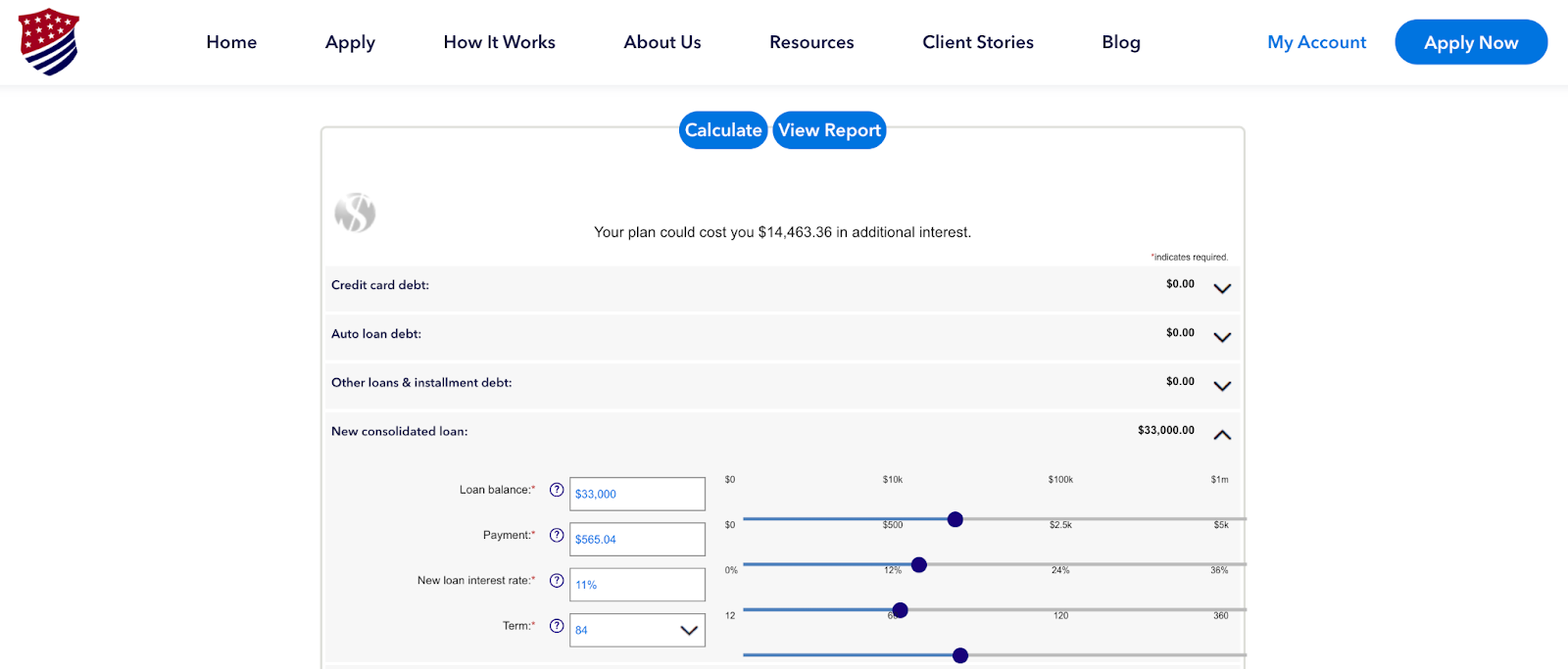

Moreover, they have quite a few calculators to help you figure out your situation.

Calculators include accelerated debt payoff, consolidation loan investment, cost of debt, credit card minimum payment, and more.

If you decide to take a DIY approach, or even if you choose another service, I do recommend you peek in at National Debt Relief’s resources. They share most of the basics of debt and finances – And, I think this is a great knowledge base for anyone looking to sharpen their debt and financial wellness chops.

4. Debt Negotiation With Creditors

Debt negotiation, or debt settlement, might be a good fit if you have significant unsecured debt you can’t fully repay – this could be due to financial hardship like job loss or medical emergencies. It’s suitable for those unable to qualify for consolidation loans or facing collections or legal action.

Debt negotiation provides an alternative to bankruptcy, helping stop collection calls and lawsuits by reaching settlements with creditors. However, it’s not ideal for everyone, and careful evaluation of your financial situation is essential before pursuing this option.

5. Debt Consolidation Loans

Debt consolidation can be a suitable option if you have multiple debts, such as credit card balances, personal loans, or medical bills…and are looking for a more manageable way to repay them. It might be beneficial if you want to streamline your debt by combining multiple payments into a single monthly payment (usually at a lower interest rate).

This type of debt relief can help you simplify your finances and potentially save money on interest payments over time. And, it’s a good fit if you have a steady income and can afford to make consistent monthly payments towards your consolidated debt.

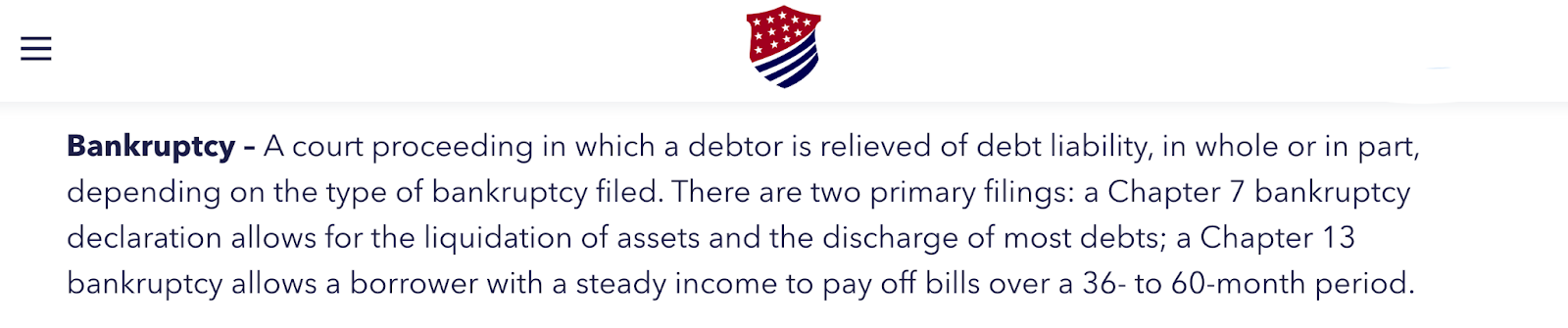

6. Bankruptcy Referrals

Bankruptcy might be a viable option if you’re facing overwhelming debt that you cannot repay, even with debt management strategies like credit counseling or debt negotiation. It might also be good if you’re experiencing severe financial hardship, such as job loss, medical expenses, or divorce. Sometimes, these situations can make it impossible to meet debt obligations.

Bankruptcy provides a legal process for individuals to eliminate or restructure debts and obtain a fresh financial start. It may also be appropriate if you’re at risk of foreclosure or wage garnishment. However, bankruptcy has long-term consequences, including a negative impact on your credit score and potential loss of assets. So, it’s essential to carefully consider the decision and seek legal advice before filing.

You might also like: Cred AI Review: Are You Really Better Than Your Bank?

Frequently Asked Questions

Can you cancel National Debt Relief?

Yes, you can cancel your enrollment with National Debt Relief at any time. They understand that circumstances may change, and you have the right to discontinue their services if you wish.

How can you cancel National Debt Relief?

To cancel National Debt Relief, you can contact their customer service team either by phone or email. They will guide you through the cancellation process and provide any necessary documentation or instructions.

Do I get my money back if I cancel National Debt Relief?

If you cancel National Debt Relief, you may be entitled to a refund of funds you’ve deposited into your dedicated savings/escrow account, minus any fees earned for services rendered up to that point. The specific refund policy may vary depending on the terms outlined in your agreement.

Does National Debt Relief hurt your credit?

When you stop making payments to creditors and enter into negotiations for debt settlement, it can be reflected on your credit report. The long-term effects of debt settlement on your credit score can vary depending on your circumstances. Discuss the potential impact with a legal and financial professional and consider all your options before enrolling.

Conclusion: Is National Debt Relief Legit?

The percentage-based pricing model seems higher than what you might expect from a debt relief program. If you paid a separate credit repair company to clean up your report for, say, $170 per month, the cost could add up fast. But, if you save 25% off your debt, and National Debt Relief charges you 20% of your enrolled debt to do it, is it really worth it?

In the case that you’ll save 50%, a 25% fee might make sense. Be sure to read the fine print before you make any commitments. I don’t know whether National Debt Relief charges before or after debt is negotiated, which could vary on a case-by-case basis.

If you’ve got a lot of collections that you want to clear up or negative items you need removed from your report, a credit repair company, an attorney, or a DIY approach might be cheaper alternatives.

In all, though, I like this offer. The company seems to be legit, they’ve been in business long enough to be reputable, and the BBB likes them. Other than the potential expense, I don’t see any glaring red flags that would make me tell you to run for the hills.

My only advice is to do your research. Learn about all of your options before you apply for relief from debt. And, if you don’t have at least $7.5K in debt, you will need to look elsewhere. Good luck on your journey to financial freedom.

Do you want to learn how to obtain up to $100K in business credit that won’t impact your personal credit, in as few as 30 days? If so, join Business Credit Workshop today!