Credit stacking is one of the latest catchphrases in the credit card realm. Naturally, as a business credit coach and expert, I had to check it out. I did a ton of research into the system (everything shy of hopping on a strategy call and joining the community) to see what I could find out.

As usual, I want to share what I’ve learned with you.

At first glance, credit stacking seemed a lot like what we teach at Business Credit Workshop…but it’s not — there are some fundamental differences. I’ll summarize the most glaring distinctions before I wrap up.

If you’re thinking about hopping on a call with the Credit Stacking team to become a member, read this first.

Here’s what’s in store:

- What is Credit Stacking, Exactly?

- Frequently Asked Questions

- The Credit Stacking Book by Jack McColl

- The Takeaway — Is Credit Stacking Legit?

Now, let’s hop to it!

What is Credit Stacking, Exactly?

When I first heard the expression, I thought credit stacking might be akin to credit piggybacking, but I was wrong.

Credit stacking is a popular buzz phrase (pretty catchy, really!) coined by Jack McColl — it refers to building multiple lines of credit in an alleged specific order to obtain large lines of credit. Essentially, it is a framework to apply for multiple cards at once with the least negative impact on your credit.

With credit stacking, you can get up to hundreds of thousands of dollars in funding by applying for multiple credit cards and taking advantage of business credit (which is separate from personal credit).

McColl teaches about the system through a credit stacking course, online membership, and a Facebook group. Through these channels, members allegedly learn how to maximize their credit limits to grow businesses from the ground up with tens of thousands of dollars in credit.

The application process to join is simple and seems to help gauge where potential members are on their credit journey — which is helpful for a customized strategy.

🚩 The company doesn’t display the cost of membership anywhere on its website and some sources say that it costs $4,500 or more to join.

What is the Credit Card Stacking Strategy?

With the Credit Stacking system, essentially, you want to apply for cards in a specific order that might improve your odds of successful funding…this requires that you aren’t over-leveraged in the way that you have too many inquiries showing on your credit profile.

To do this, you need to know which banks pull your info from which credit bureaus, and apply in such an order that all of your inquiries hit your report with minimal negative impact on your score.

And, since Chase Bank is more strict about how many credit inquiries you can have to qualify, you should apply for credit with them first.

Frequently Asked Questions

Why is credit stacking effective?

Credit card “stacking” is effective because it ideally maximizes the amount of credit you’re able to obtain by minimizing the impact of inquiries on your consumer credit report.

What is the credit stacking analogy?

Think of credit stacking as building a tower out of blocks. You start with a solid foundation, like a base of small credit lines, and then add more blocks (larger lines of credit) on top in a specific order. This way, you can build a strong and stable tower of credit that allows you to access more funding opportunities over time. It’s like playing Jenga, but instead of removing blocks, you’re carefully adding them to build something bigger and better!

What are the effects of credit stacking?

Credit stacking can help you spread out your balances, increase your credit limits, and minimize the negative impact of too many inquiries. However, this can lead to high interest charges if you can’t keep up with payments, so it’s important to be mindful when using this technique.

The Credit Stacking Book by Jack McColl

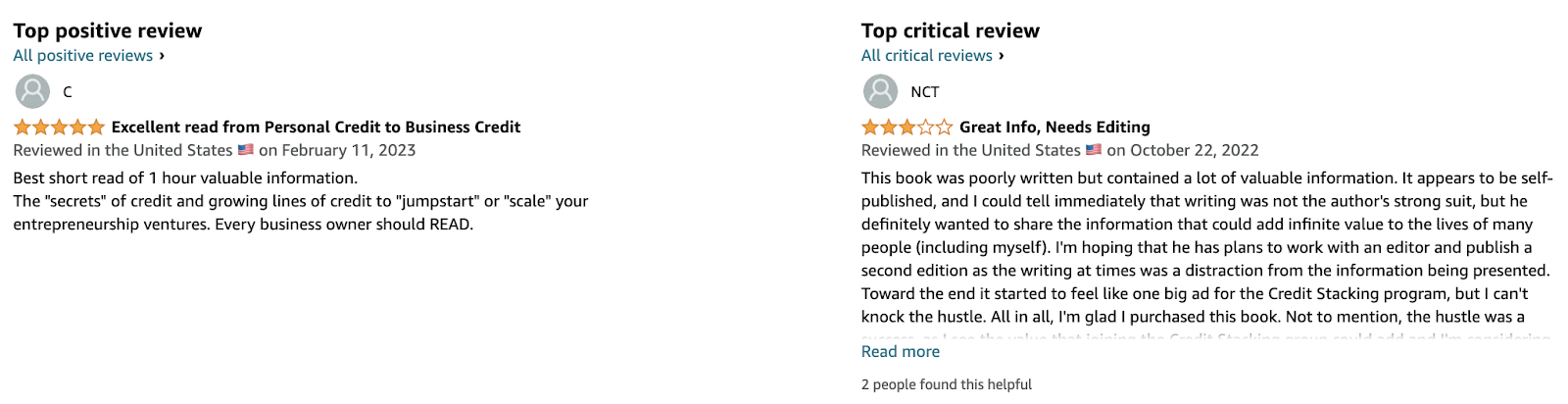

I already told you that I didn’t hop on a strategy call or join the Credit Stacking group…what I did is read Jack McColl’s book, Credit Stacking: Accelerate Financial Freedom With Business Credit.

I’ll tell you that it seems to be self-published. It could have used an editor to help condense some of the information (which is absolutely valuable nonetheless).

And, while I can’t shame the hustle, the book was pretty promo-heavy, leading readers into the Credit Stacking program by teasing some of the resources that are exclusive to members.

With that said, I was taking notes the entire time, and here’s what I got from it.

→ If you don’t want to read the entire synopsis, you can skip to the final takeaway.

Chapter 1: Where Do You Want to Go?

The first chapter of the book is all about mindset and vision — this is probably my favorite chapter because it’s so interactive. Before you implement the steps to stack credit and build your dream business, you need a vision.

McColl leads into the book with questions such as, “Where do you want to live?” “What relationship do you want to have?” and “What career do you want?” He recommends you get a clear vision by answering all of the questions in his sequence before you move forward.

Next, he shares his framework for daily journaling, recommending that you do something similar. Every day, you should write about the following:

- What you’re grateful for

- Affirmations for yourself

- A recent win

- Desires for yourself

- A power list of needle-moving tasks you can accomplish today

With a clear vision and daily check-ins with yourself, you can take an honest look at your discipline, resilience, and environment to determine what you need to do to make your business strategies work.

Before wrapping up, the first chapter looks at good debt vs bad debt. In a nutshell, good debt is invested in assets that generate cash flow or equity and bad debt is costing you money… think of it as assets = good debt, liabilities = bad debt.

Chapter 2: Personal Credit

The second chapter is all about consumer credit. Good personal credit gives you access to rewards cards as well as low-interest auto and home loans. And, according to McColl, better access to 0% interest business capital.

This is where the book starts to talk about the technical aspects of credit stacking like awareness of the three consumer credit bureaus, VantageScore vs FICO, credit score factors, and credit repair.

When speaking on the three major credit bureaus, McColl mentions a specific template that Credit Stacking members use to analyze their credit profiles but doesn’t offer the template in the book.

Vantage scores are more readily available for free (via Credit Karma, for example), but lenders typically pull FICO scores. McColl recommends myscoreiq.com, which costs $35.99 per month, to monitor your FICO score. There’s a gray area between scores of 500 to 700, but below 500 typically means that a borrower is high-risk, and above 700 usually signals that a borrower is low-risk.

Naturally, lenders like higher credit scores.

But, if you have a low score, don’t let it discourage you, because, as McColl states, this can always be fixed.

This chapter also breaks down the factors of a credit score and what you might do to maintain or improve each factor — this information is typically available with any credit monitoring system, but it’s good for beginners to understand:

Payment history and amount of debt have the highest impact while credit mix and new credit are important too. After explaining each factor in more detail, this chapter goes on to share a few case examples of individuals who used the credit stacking strategy.

One Credit Stacking member was able to obtain a $50K line of business credit from Chase Bank. McColl claims that this was 0% interest capital. In the case of this borrower, they had a strong personal credit profile, and their business entity was established properly…they also had a checking account and a connection with the relationship manager at the bank where they applied for the loan.

Here, McColl mentions an important fact: You don’t necessarily have to have a large, established business to obtain large lines of credit. Small, new businesses can obtain credit too.

Many business owners who started out with poor credit were able to obtain large lines of credit after implementing a credit repair system. McColl mentions that this process starts by disputing anything negative that might be holding your score down. He mentions that the Fair Credit Reporting Act (FCRA) has laws in place that protect consumers and enables them to dispute anything that is unfair or inaccurate and that the burden of proof is on the creditors.

McColl mentions a credit repair partner that Credit Stacking members can be connected with and cites some happy endings after working with these programs.

⚠️ I do not ever recommend unethical exploitation of laws or institutions that are in place to protect you. I do recommend educating yourself on the regulations and strategies to repair your consumer credit profile.

Recommended: Credit Secrets Book Review: Can You Erase Bad Credit History?

Chapter 3: Credit Cards and Calculated Risk

The third chapter of the book starts with a pretty long intro to the story of Amazon. Then, it talks about why you should use credit cards instead of other types of capital to fund a business: protection, rewards, card benefits, and relationship building.

Here, the book fails to mention freedom (this is why I like business credit over other funding types). Traditionally, when a company gets funding, it might have to rely on personal capital or investors who want control — with business credit, the business owner maintains control and freedom to make their own choices for their company.

Recommended: How Business Credit Can Transform Your Life (Really)

Next, McColl recommends some credit cards you should apply for, and ones that you shouldn’t. He says that he doesn’t recommend that anyone apply with Capital One because they pull from all three bureaus, creating a ding on all three consumer credit reports. This is true, but he doesn’t mention that these “dings” last two years — they’re temporary.

Then, McColl recommends some questions to ask yourself when applying, such as, “Do you have a travel card yet?” and, “Which bank are you looking to build a relationship with?”

Before he moves on, he covers when to apply, how to apply, and how to request reconsideration on a failed application.

Chapter 4: Using Business Credit to Gain Momentum

According to McColl, the key to business success is momentum — the value of your company has a direct impact on momentum.

The fourth and most extensive chapter covers the different ways you can fund your business to create momentum:

- Your own cash (personal capital) — with this, you’ll foot 100% of the risk

- Business loan — lofty interest rates on a non-transferable lump sum of debt

- Get a partner — you’ll have to share control of business decisions

- 0% interest business credit card — if you keep your relationship with the bank in good standing, you’ll keep yourself “just one application away” from more business credit

Note: McColl doesn’t mention all of the ways to fund a business like Y Combinator, seed funding, MCAs, nor the many, many others.

Next, he explains that business credit won’t impact your FICO score, which is mostly true…if you apply for the business credit cards that are reported to D&B and not the three consumer credit bureaus.

He then shares the process for setting your business up for business credit.

This section discusses business SIC codes, and the fact that some are considered higher risk than others — General businesses such as “consulting” and “management” are best and may get better business credit results than “credit coach” or “real estate agent.”

In a nutshell, you need a NAICS code that fits your business narrative in a low-risk category.

McColl recommends that you look up your business on D&B to see if you have a DUNS number. If you don’t, create a profile with D&B…and make sure your NAICS code is the same with your bank, D&B, and your state business registry.

Recommended: Everything You Need to Know About a DUNS Number

McColl strongly recommends that you use Chase Bank for your business checking, as he’s seen the most business credit success with Chase, however, he cites other major banks like BoA and US Bank and claims that you should have similar results.

Basically, he says that you should only build a relationship with a bank that offers 0% interest business credit cards. And, he shares his framework for building your business credit:

- Open a business checking account with the main (big) bank

- Open a business checking account with a regional bank or credit union

- If you already have an account with a regional bank, move some of your capital to a big bank

- Get your FICO score above 780

- No derogatory marks

- No more than one late payment

- 4-5 accounts that are at least three months old

The framework we teach at Business Credit Workshop is quite a bit different.

Recommended: This is How to Build Business Credit Fast [Step-by-Step Guide]

Next, McColl covers each of the four funding types from the beginning of the chapter (personal capital, business loan, equity partner, and business credit) in detail before he starts elaborating on business credit.

Business credit is a way for you to finance business ops by borrowing from banks using your EIN rather than your SSN. McColl says you should have an LLC or a Corporation rather than a sole proprietorship, and I agree… 💯

After this, he lists a handful of the benefits of business credit, such as the fact that business credit bureaus don’t include opening dates on their reports and you can go through rounds of applications (“credit stacks”) without harming your credit score.

Then, McColl lists some ideas for ways to use business credit to grow your business (invest in equipment, rent office space, hire a mentor, etc.) and lists new business ideas for entrepreneurs:

- Start a trucking business

- Start an Airbnb

- Launch an eCommerce store

- Buy a rental property with the BRRRR method

- Fix & Flip a property

He mentions that there are ways to liquidate credit cards into cash, but doesn’t mention what they are.

Recommended Resources:

- How to Convert Credit Cards Into Cash

- How to Pay Rent With a Credit Card

- Can You Pay Your Mortgage With a Credit Card?

This chapter also mentions business credit requirements such as on-time payment history on your personal credit profile, a variety of accounts, and sizable limits on your consumer cards. Here, it starts to feel like the book exerts excessive information about consumer credit.

McColl shares the difference between revolving credit cards — with and without interest — and charge cards (Capital on Tap, Divvy, and Amex) are discussed… he recommends that you max out your Amex cards and pay them off in full to get your limit increased.

There are companies that will apply for business credit for you, but McColl recommends DIY credit applications. The companies that offer services like this aren’t always thinking in your best interest where high card limits and the number of hard inquiries are concerned. Plus, you have to pay fees for these services.

The book then mentions that 0% interest credit cards aren’t necessarily easy to find (there was no database that houses all of the banks’ current promotions, so McColl built one…though, it’s only available for Credit Stacking members).

In place of a database of cards with 0% introductory rates, you can use McColl’s recommended searches:

“[your state] 0% interest business credit cards”

As he wraps up, McColl summarizes inquiry stacking. “Stacking” credit inquiries can allow you to maximize your business credit. When you know which banks pull from which bureau, not all of your inquiries will show up when you apply for multiple cards.

And, Chase is stricter about maximum credit inquiries, so McColl recommends you apply for any Chase business credit cards first.

Tip: If you submit your applications in the branch, your applications won’t be flagged for technical issues like invalid IP, flagged VPN, or grammar mistakes. McColl suggests that you submit your application through a relationship manager for the best results (they work directly with the underwriting team, so they know what you need to get credit and can help you with your applications).

The book then states that it is difficult to find a bank’s relationship manager to submit your applications and that Credit Stacking members are introduced to relationship managers as part of their membership.

Finally, McColl shares his advice for filling out credit applications accurately.

Chapter 5: Money

In the fifth chapter, wealth accumulation and money are covered.

The first principle of wealth that McColl covers is compound interest. For example, you have $100 growing at 10%, and you earn $10 the first year. So, the next year, you have $110, and your earnings are $11. As this continues, your annual growth grows.

And, if you have $250K to invest initially, with a 10% growth rate, you would have $11M after 40 years.

There is a lot more information in this section about investing — buying low and selling high, dollar cost averages, etc — including examples of billionaires who invested wisely.

The key takeaway is that you need to invest wisely in facets of your business that produce income and wealth.

McColl then covers the importance of educating yourself — both about money and about your industry. Essentially, if you learn specific skills from experts in a niche, you save yourself the time and heartache of learning through trial and error.

Likewise, it’s important to join networks of successful people who you can piggyback from their knowledge. McColl recommends in-person mastermind events in particular.

Next, he covers Roth IRAs and the “infinite banking” concept.

Roth IRAs allow you to invest, tax-free, if you keep your money in the account until you’re 59.5 years old and at a 10% fee if you withdraw sooner. The maximum you can invest in a Roth IRA is $6K per year. There are also exceptions to the 10% fee, such as withdrawing $10K to put down on your first home.

This is an excellent investment opportunity, especially for young people looking to the future, especially since these accounts compound *see above.*

The infinite banking concept is essentially the idea of an Indexed Whole Life Insurance Policy (not all life insurance policies are equal). With this type of life insurance, you get most of the benefits of building your net worth without triggering an MEC through the IRS…in a nutshell, it maximizes the cash value of your policy without negating the tax benefits.

Plus, nobody can come after money in an Indexed Whole Life Insurance Policy — not the courts, ex business partners, or spouses…nobody. And, all the while, it will accrue interest of about 5.5% while any loan repayment to the account will cost about 5%.

The rest of this chapter covers the fundamentals of cryptocurrency, centralized exchanges, and crypto hedge funds; these are pretty extensive explanations and I recommend you read the book if you’re interested to learn more.

Chapter 6: Traveling on Credit

The sixth chapter covers how travel creates work-life harmony and how this can be achieved with business credit.

If you opt to travel while working, you need to be sure you can have a consistent, reliable WiFi connection — a fast one — anywhere you go (this is especially true if you opt to travel full time). McColl also recommends that you make sure you’re close to a gym, beach, or hiking trails to stay in shape.

Basically, you can travel on credit by maximizing the use of your credit card travel rewards and points.

The final section of this chapter covers credit card points accumulation and redemption strategies, how to gain status with hotels (Hilton and Marriott), and credit card travel benefits.

Chapter 7: The Road to Independence

The seventh chapter wraps up the book — it starts with some motivational ideas about maintaining freedom and reaching goals, with the thought that independence, once earned, is hard to keep.

McColl concludes by inviting readers to take advantage of a free “strategy session” with the Credit Stacking team, followed by lots of testimonials and case examples of what members have achieved.

The Takeaway — Is Credit Stacking Legit?

In a word, yes, Credit Stacking is a legitimate technique and sort of mastermind group that has helped people obtain substantial lines of credit…tens of thousands of dollars, in fact.

I don’t believe they’re going to steal your money if you sign up — these guys seem to be for real and their members are getting some great results.

With that said, I have a few conflicting ideals with the Credit Stacking system:

- First of all, at Business Credit Workshop, we don’t teach members to give big banks precedence over smaller community banks and credit unions.

- Next, we share a lot more information upfront about the steps to obtain business credit, including establishing the right number of reporting tradelines to achieve a perfect business credit score.

- Finally, my focus is on helping people learn how to build their business credit fast and have a long term strategy working with local banks to get funding…not just applying for as many credit cards from big banks as they can.

If you’re looking to obtain $100K in business credit in as few as 30 days (even if you have a new business), join Business Credit Workshop today.