Key Takeaways

- A TIN is any tax ID used for individuals or businesses.

- An EIN is a type of TIN used to identify businesses.

- Sole props and single-member LLCs may use an SSN as a TIN.

- Most LLCs need an EIN to bank, file taxes, or get licenses.

- The IRS issues EINs, ITINs, ATINs, and PTINs; the SSA issues SSNs.

- You can apply for an EIN free on the IRS site.

- TINs appear on tax forms, ID letters, and official records.

- TINs are private, but some EINs show up in public filings.

In business, we throw a lot of acronyms around: LLC, SIC, KPI… TIN and EIN are two acronyms that look similar and are often confused, but they refer to different things.

A TIN is a broad term, while an EIN is one specific type of TIN used for business purposes. Here, you’ll learn the key differences between the two as well as when and why you need a TIN vs. EIN.

This is what’s in store:

- What is a TIN vs. EIN?

- Do You Need a TIN for Your LLC?

- Where to Find Your Tax ID Number

- Frequently Asked Questions

- Final Takeaway

Now, let’s learn!

What is a TIN vs. EIN?

In short, a TIN is a “Tax Identification Number,” and an EIN is an “Employer Identification Number.” Both are issued by U.S. federal agencies to individuals or businesses for tax purposes. Let’s take a closer look at each.

Disclaimer: This article is for general information only and isn’t tax advice. For help with your specific situation, talk to a qualified tax professional or accountant.

What is a TIN?

A Tax Identification Number (TIN) is a unique number the Internal Revenue Service (IRS) uses to identify individuals or businesses for tax purposes. It can refer to a Social Security Number (SSN), an Employer Identification Number (EIN), or an Individual Taxpayer Identification Number (ITIN), depending on the situation.

A TIN may be issued by the Social Security Administration (SSA) or the IRS.

| Type of TIN | Issued By | Used For |

| Social Security Number (SSN) | SSA | Identifying U.S. citizens and eligible residents for tax and employment. |

| Employer Identification Number (EIN) | IRS | Identifying businesses, estates, and trusts for tax filing and reporting. |

| Individual Taxpayer Identification Number (ITIN) | IRS | Identifying individuals not eligible for an SSN, often nonresident aliens. |

| Adoption Taxpayer Identification Number (ATIN) | IRS | Temporary ID for adopted children until an SSN is assigned. |

| Preparer Tax Identification Number (PTIN) | IRS | Required for paid tax return preparers. |

You might also like: Sole Proprietorship VS LLC: How to Choose Your Entity Wisely

What is an EIN?

An EIN is a type of TIN that the IRS assigns to businesses. It’s used to identify a business entity. So, an EIN isn’t a separate concept from a TIN. It’s actually one specific type of TIN used for identifying businesses.

Businesses may use an EIN when they:

- File tax returns

- Open a business bank account

- Apply for licenses and permits

Many business formation services offer EIN application services. I rarely recommend that you take advantage of this because you can apply for an EIN on the IRS website. It’s free and only takes a few minutes. The only catch is that online EIN applications are only available during IRS business hours, Monday through Friday.

You might also like: Can (and Should) You Be Your Own Registered Agent?

Do You Need a TIN for Your LLC?

If your business will open a bank account or file taxes, yes, you need a TIN. Every LLC needs a TIN for tax and business purposes. In most cases, this means getting an EIN from the IRS—even if your LLC doesn’t have employees.

If you’re a single-member LLC or sole proprietorship with no employees, the IRS may, in some cases, allow you to use your SSN instead of an EIN.

Your business might not need an EIN if it meets all of the following conditions:

- It’s a sole proprietorship or single-member LLC.

- It has no employees.

- It does not file any excise taxes (like fuel or alcohol taxes).

- It does not withhold taxes for non-resident aliens.

- It does not have a Keogh retirement plan.

- It does not need to file employment, excise, or alcohol/tobacco/firearms tax returns.

In this case, the owner may be able to use their SSN as the business’s TIN for tax purposes. However, most banks and agencies still ask for an EIN. Some business owners co-mingle their personal and business finances, but this can lead to problems. Plus, when you manage business finances through a personal account, you aren’t generally eligible for business credit.

You might also like: No-Doc Business Loans with EIN Only: Get Funds Without Proof of Income

Where to Find Your Tax ID Number

Where you find your Tax ID Number (TIN) depends on the type of TIN you’re looking for.

The most common places to find your TIN are:

- SSN → On your Social Security card, on tax documents like W-2s or past tax returns, and through the SSA. If you’ve lost it, you can request a replacement Social Security card.

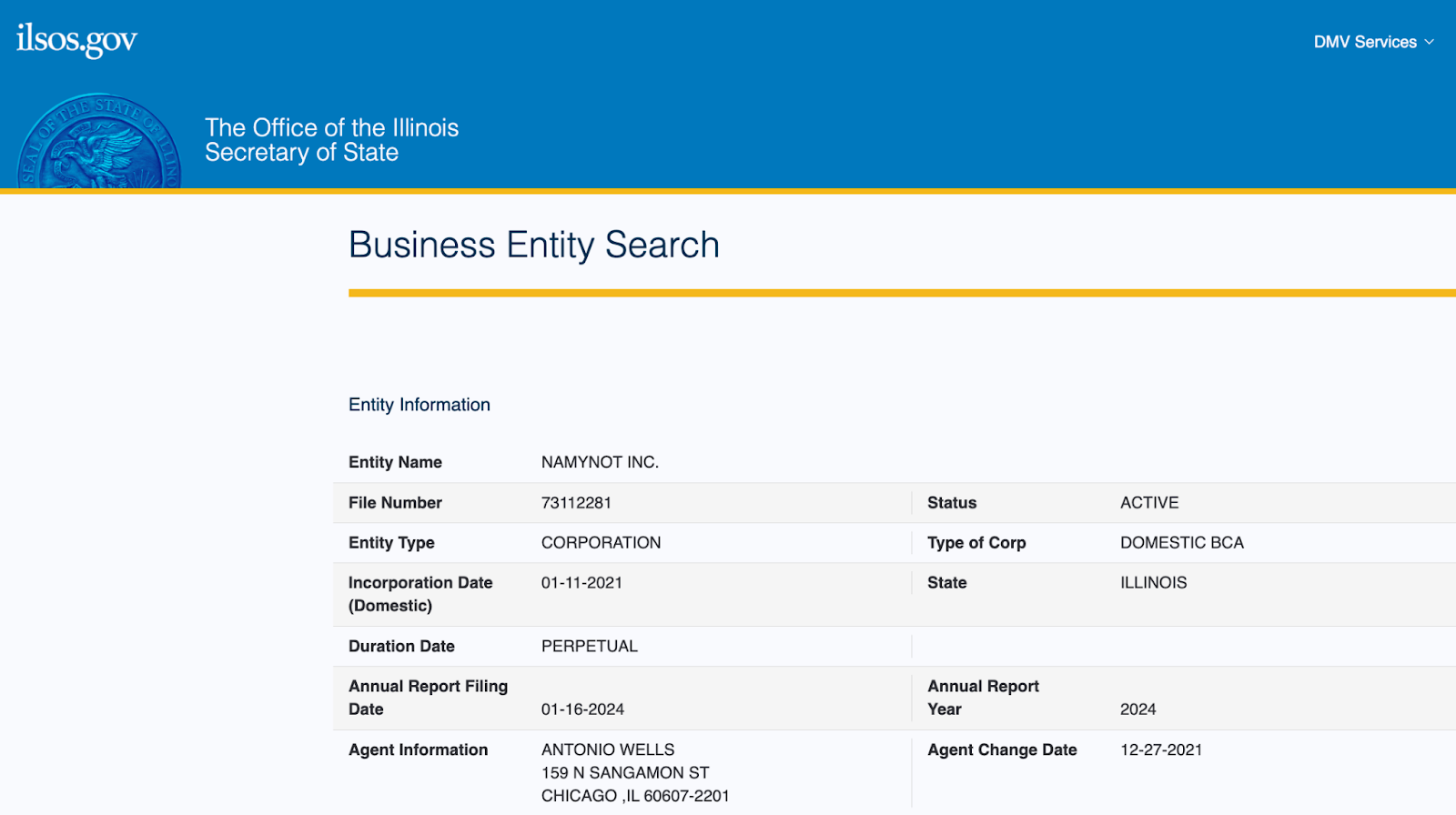

- EIN → On your EIN confirmation letter from the IRS (Form CP 575), on tax forms like your 1120, 1065, or payroll filings, and on business bank account documents or loan applications. If you can’t find it, call the IRS Business & Specialty Tax Line at 1-800-829-4933.

- ITIN → On your IRS ITIN assignment letter and on tax returns you’ve filed with the ITIN.

To look up someone else’s EIN (like a nonprofit), it may be listed on public records like Form 990s.

You might also like: InDinero Unveiled: A Detailed Accounting & Tax Platform Review

Frequently Asked Questions

Can I use my SSN as my TIN?

When filing taxes as an individual, yes. As a business, maybe. If you’re a sole proprietor or single-member LLC with no employees, your SSN can serve as your TIN. But you’ll need an EIN to hire, open a business bank account, or get licenses.

How do I know if I have an EIN or TIN?

If you applied for an EIN from the IRS, you have one. An EIN is a type of TIN. If you use your SSN for taxes, that’s your TIN. Check past tax forms or your EIN confirmation letter to be sure.

How can I get an ITIN?

To get an ITIN, file Form W-7 with the IRS, along with your federal tax return and proof of identity.

Is there a difference between EIN and ITIN?

Yes, an EIN is for businesses, while an ITIN is for individuals who can’t get an SSN, like some nonresident aliens.

How do I find out who a TIN belongs to?

You usually can’t because TINs are private. But, EINs for nonprofits or public businesses might appear on public tax documents like Form 990.

Final Takeaway

TINs and EINs might look similar, but they serve different roles in the world of taxes and business. A TIN is any tax ID used to track individuals or entities, while an EIN is the go-to ID for businesses.

Whether you’re just starting out or growing your LLC, knowing which number you need—and how to get it—can help keep your finances legit, organized, and ready for whatever comes next.

Ready to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!