Key Takeaways

- Kabbage became Amex Business Blueprint, from lending to a full financial platform.

- Blueprint combines banking, lending, and cash flow insights in one dashboard.

- Amex Lines of Credit have lower fees than Kabbage (0.95% to 27%, depending on the term).

- Business Checking offers higher (1.3%) APY, no fees, and a rewards debit card.

- The iOS app is highly rated, but Android users report issues and bugs.

- Payment Accept replaced Kabbage Payments, but new customer availability is unclear.

- The Resource Center provides business insights and financial tools.

Kabbage was once a popular online lender and one of the SBA’s approved PPP loan providers. American Express quietly acquired Kabbage’s platform in 2020, and reworked it to create Business Blueprint—a comprehensive business cashflow dashboard.

So, what’s changed? And, is American Express Business Blueprint worth checking out? Here, we’ll take a quick peek at why Kabbage might have exited from their operations and learn everything you need to know about the new and expanded offer from Amex.

This is what’s in store:

- What Was Kabbage?

- What is American Express Business Blueprint?

- How Does American Express Business Blueprint Work?

- Frequently Asked Questions

- Final Takeaway

Now, let’s dive in!

What Was Kabbage?

Kabbage, founded in 2009, was an automated lending platform offering quick loans up to $250K for small businesses. Known for convenience but high fees, it paused lending during COVID-19 to focus on PPP loans, earning mostly low ratings.

Later, a few years after the purchase by American Express, it transitioned into Amex Business Blueprint, discontinuing its original offer.

Near the end, Kabbage offered tools like:

- Kabbage Checking (competitive APY)

- Kabbage Payments (low invoicing fees)

- Kabbage Insights (cash flow tracking)

While useful, these services faced some technical issues before the transition. The hiccups near the end may have made selling the company the wise choice.

You might also like: No-Doc Business Loans: Get Funds Without Proof of Income

What is American Express Business Blueprint?

When I first heard that Amex had acquired Kabbage (whose lending funds used to come from Celtic Bank), I said, “If the brand does bring back working capital in the future, it will most likely come directly from Amex itself. We’ll just have to wait around to see.”

Well, that future is now.

American Express Business Blueprint is a free platform positioned to help small businesses manage their cash flow. It lets you view your American Express business products and linked external accounts in one place. Then, it provides personalized insights to help you make informed financial decisions.

With the tool, you can access features like a 30-day bank account balance projection, which uses data from your linked accounts to help you anticipate future balances. In a nutshell, business Blueprint aims to simplify financial management for small business owners.

Moreover, Amex is offering a Business Line of Credit up to $250K (same as Kabbage), with no mention of Celtic Bank. Today, these loans are serviced directly by American Express National Bank.

Recommended: Amex Business Checking Review: What You Need to Know…Really

Company Overview

American Express, aka Amex, is a global financial services company with roots dating back to 1850. Founded by Henry Wells, John Butterfield, and William Fargo—names you might recognize from Wells Fargo—Amex has built a reputation for reliability and innovation in finance.

Initially known for credit cards, charge cards, and traveler’s checks, the company has since expanded its offerings to include business checking accounts (and, now working capital) further solidifying its leading position in the financial world.

Headquartered in New York and led by CEO Stephen Squeri, Amex stands out as a trusted name in American finance. It’s publicly traded and has endured as a stable force in a fast-evolving industry.

You might also like: A Complete, Unfiltered Amex Business Gold Card Review

How Does American Express Business Blueprint Work?

As I said before, American Express Business Blueprint is free. And, you can log in with existing credentials, if you’re already an American Express member, or create an account.

Once you’re in, you’ll have access to a lot of the same features and services that were available with Kabbage, but with some notable improvements.

1. Business Lines of Credit

Kabbage’s fixed-rate loan fees were steep, ranging from 24-99% APR, with no savings for early repayment, no long-term options, and approval limited to businesses with online checking or PayPal.

In contrast, Amex Business Lines of Credit offer a more affordable alternative, with funding from $2K to $250K secured by business assets and personal guarantees.

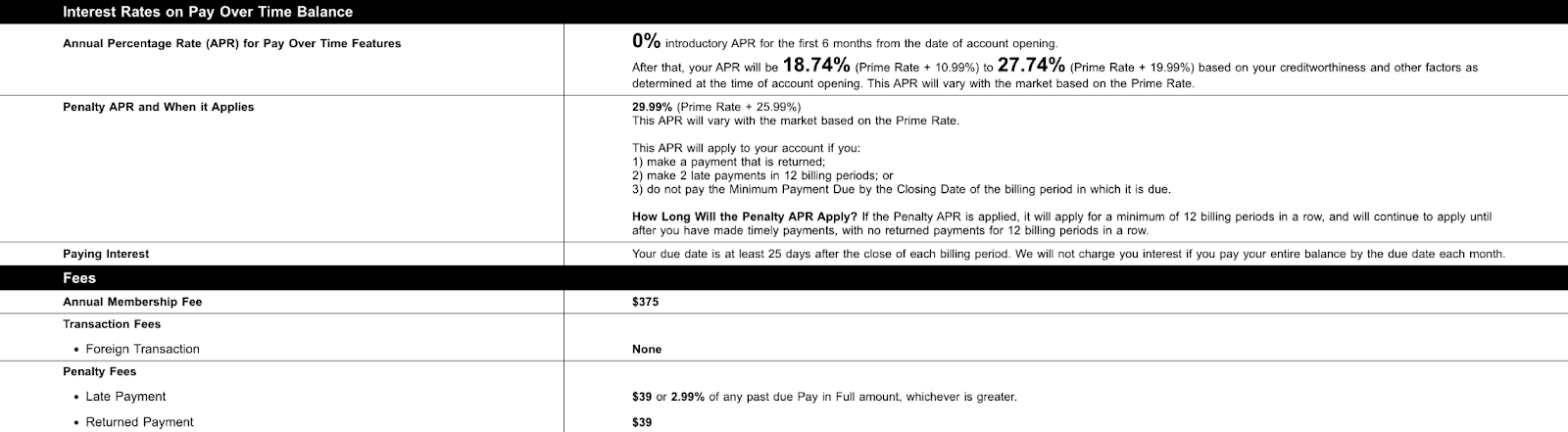

Amex’s fees range from:

- 0.95% to 6.05% for single repayment loans (1 to 3 months)

- 3% to 27% for installment loans (6 to 24 months)

So, Amex offers a much less expensive business lending option than Kabbage was able to. They also offer reduced costs with early repayment on installment plans. However, you must be an Amex cardholder to apply.

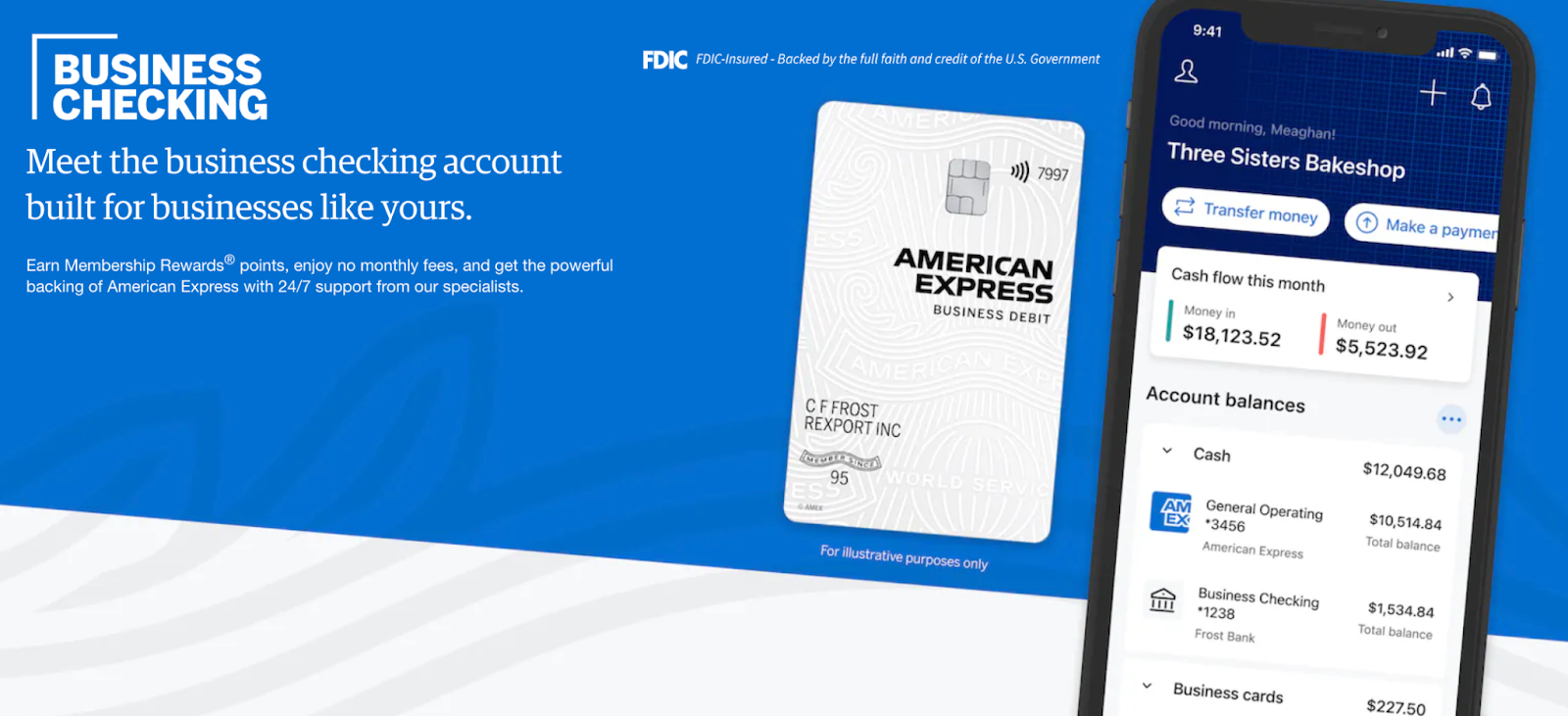

2. Business Banking Accounts

Before the transition, there was no such thing as a Kabbage business savings account. Likewise, there is no American Express business savings account (though they do have a consumer savings option).

Kabbage Checking offered FDIC-insured banking with 1.10% APY earned on funds, which they declared was the best deal you’ll find. This wasn’t true with 2% earnings from Bluevine and varying larger amounts from several credit unions.

Today, American Express Business Checking is worth taking a look at. Their business checking account earns 1.3% APY on balances up to $500K and charges no monthly maintenance fee—They also offer a rewards debit card that earns 1 point with every $2 spent, and their high deposit limits can house balances up to $5 million.

However, they lack integrations for tools like QuickBooks and don’t accommodate cash deposits (despite free MoneyPass™ ATM access). Currently, they don’t offer virtual cards, either.

Recommended: Best Business Bank Accounts: 5 Top Picks for Small Businesses

3. American Express Business Blueprint Cashflow Management

Kabbage Insights, in my opinion, was comparable to Quickbooks. While it did deliver visual reports, it was basically an accounting platform. Theoretically, it allowed users to view all their accounts in one place for a clearer picture of cash flow and revenue.

Users could link the system to various banks, including smaller credit unions. PayPal and Stripe integrations were unavailable when I reviewed Kabbage, despite being advertised.

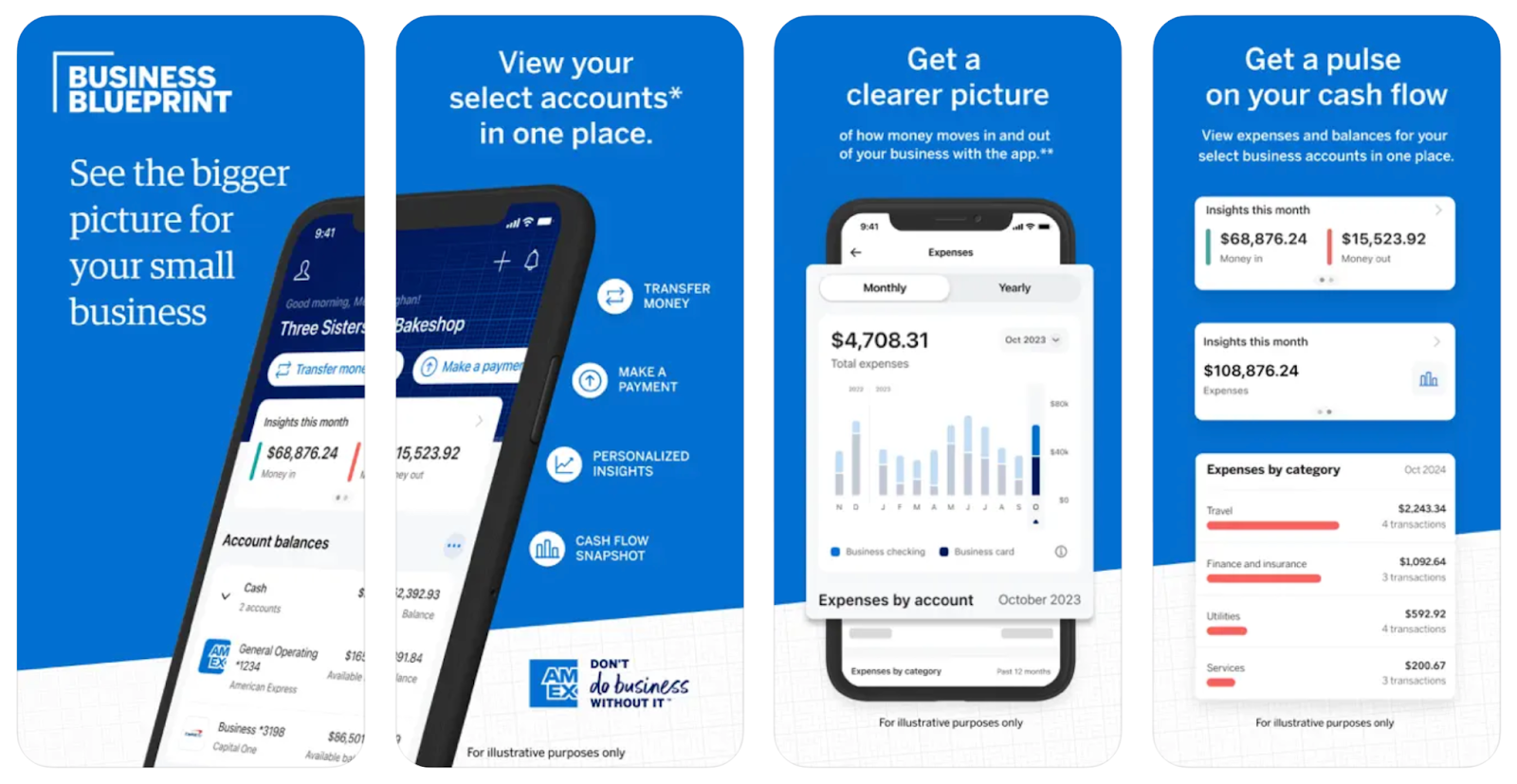

Today, Business Blueprint™ is the core of Amex’s small business offer, with a real-time financial dashboard that consolidates Amex business products and linked external accounts.

It offers:

- Personalized cash flow insights

- Business income and expense tracking

- 30-day balance projections

- A bird’s-eye view of your financial health

You can get all of this in one place. It’s designed to help you focus on growth instead of spreadsheets. The platform is free, but individual Amex financial products have their own fees and eligibility requirements.

You might also like: Plastiq Review: Can Plastiq Really Simplify Your Finances?

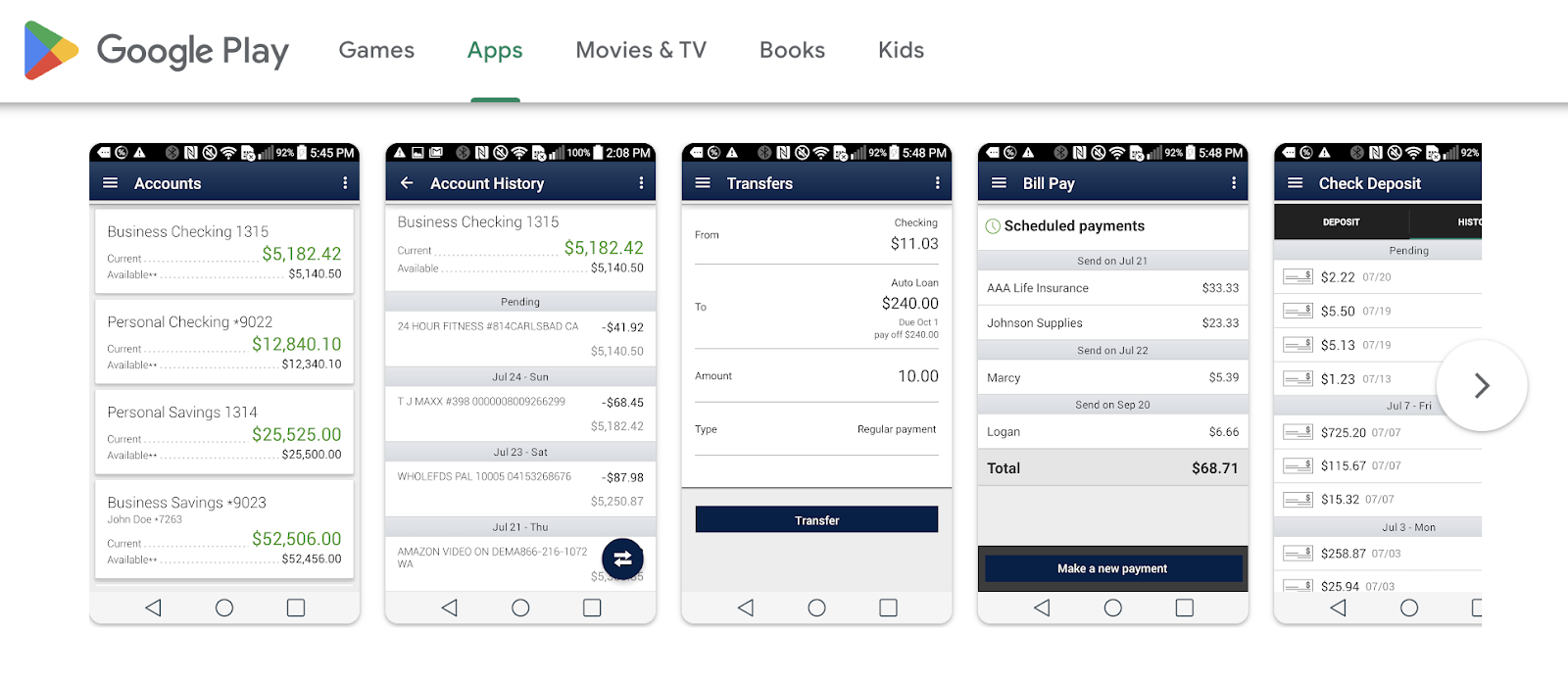

4. American Express Business Blueprint App

Back in September 2020, I noted that Kabbage’s web app and mobile app both seemed a little wonky. I assumed this was because they had recently furloughed staff and cut back on their service offer for the time being.

Today, the American Express Business Blueprint app, available on both iOS and Google Play marketplaces, seems upgraded.

Apple users give The Amex Business Blueprint™ app a 4.8 out of 5 rating, based on 8,500 reviews. Users appreciate its convenience and ease of use. However, some have reported limitations in banking functionalities, like viewing canceled checks and scheduling payments.

However, most Android users seem find the Amex Business Blueprint app frustrating due to:

- Persistent login issues

- Slow transfers

- Frequent glitches

- Poor support

Many of them prefer using the web instead.

You might also like: What is the Best Personal Finance Software? Free and Paid Options

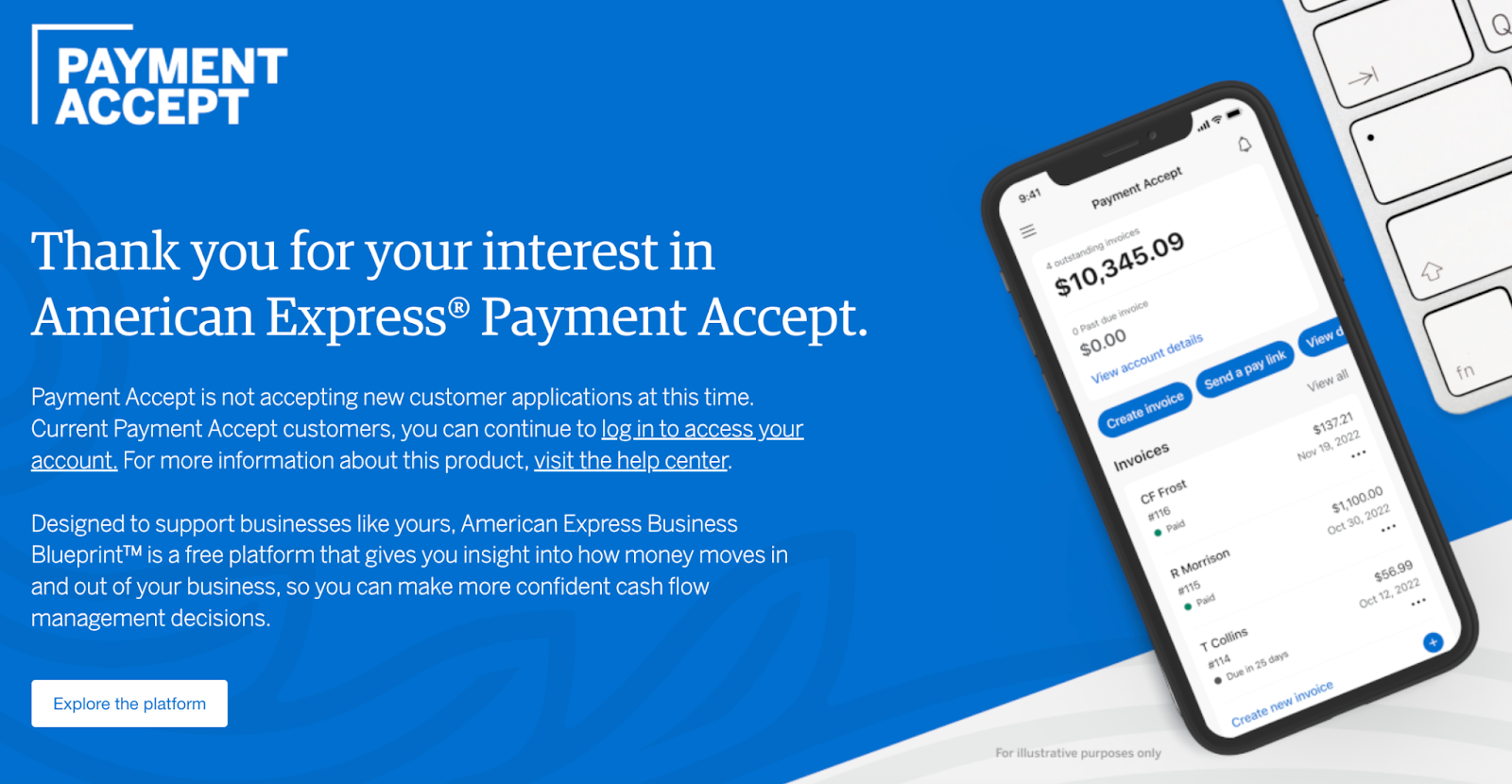

5. American Express Invoicing & Payments

Kabbage Payments was an online invoicing platform with competitive rates at 2.9% + $0.25 per transaction, slightly lower than most major competitors. It supported email and web link billing, with next-day deposits for transactions processed before 5 PM.

Users could also create a unique URL to sell gift certificates ranging from $15 to $500.

Today, American Express Payment Accept is a service designed to help small businesses process card payments online efficiently. It offers a straightforward solution with transparent pricing, aiming to make payment processing simple and quick.

*But, they may not be accepting new customer applications at this time—Check with Amex for Updated info.

You might also like: Melio Payments Review: Can It Make Business Payments and Getting Paid Easier?

6. American Express Financial Resources

Kabbage’s “Resource Center” was a blog dedicated to financial advice for business owners. I found the articles to be pretty useful, easy-to-understand, and worth a look.

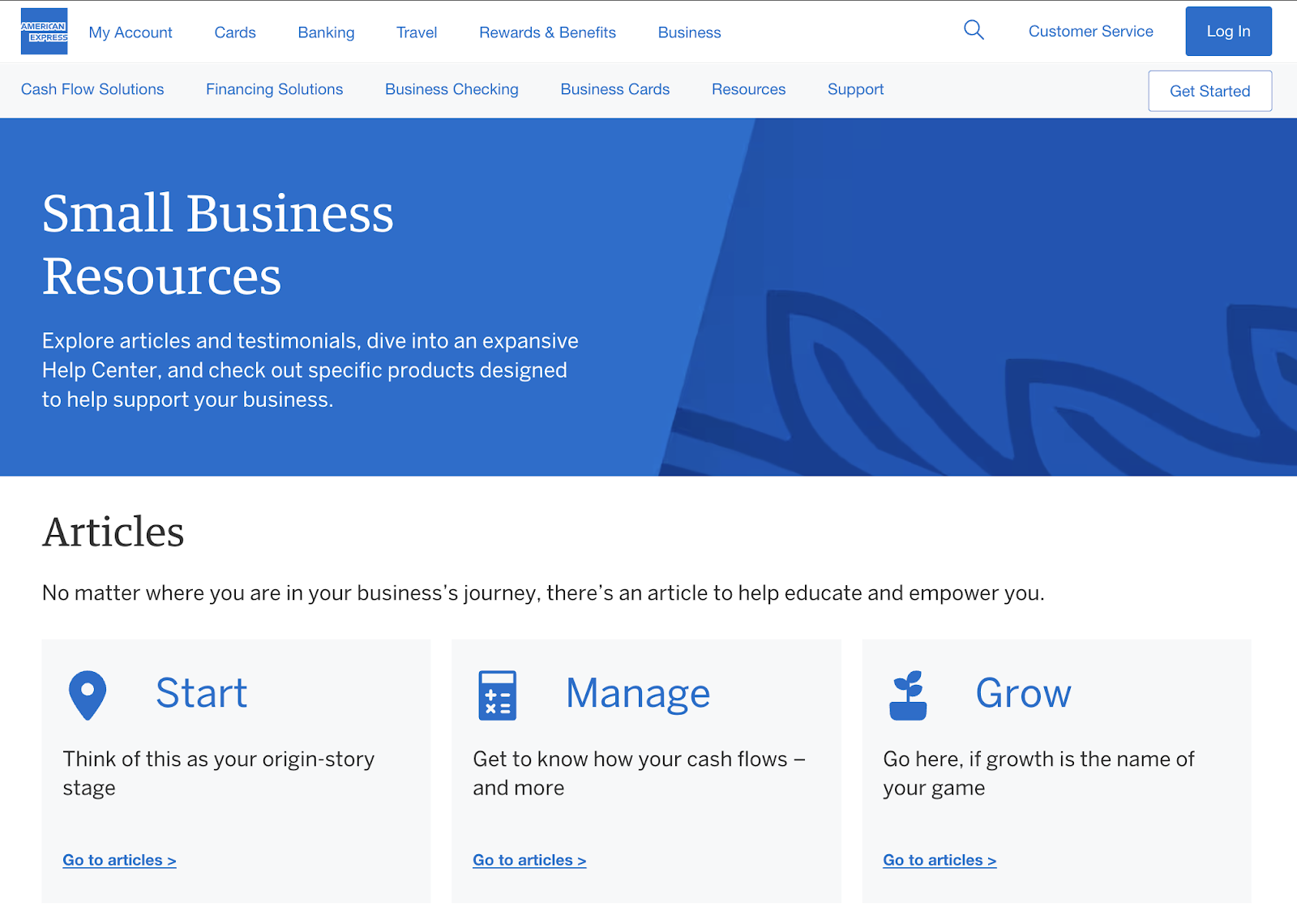

American Express, on the other hand, has a full suite of resources for small business owners through its Business Blueprint™ platform.

This includes a Resource Center featuring:

- Articles on various small business topics

- Customer success stories

- A massive help center

It provides not just articles but also tools, customer success stories, and guided resources to help business owners manage and grow their finances more effectively.

You might also like: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

Frequently Asked Questions

Is it hard to get an American Express business line of credit?

Approval for an Amex business line of credit depends on factors like your business’s financial health, credit score, and cash flow. While the process isn’t overly difficult for well-qualified applicants, Amex does require a personal guarantee and evaluates your business assets carefully.

Does Amex business report to Dun & Bradstreet?

Yes, American Express reports business credit activity to Dun & Bradstreet as well as other major credit bureaus, helping you build your business credit profile.

Why do so many businesses refuse Amex?

Some businesses avoid accepting Amex due to higher transaction fees compared to other credit card providers. These fees can cut into profit margins, especially for small businesses.

Is American Express business hard to get?

Obtaining an Amex business card or account generally requires a good to excellent credit score and stable business finances. While not excessively hard, it may be challenging for newer businesses or those with weaker credit profiles.

What is the minimum income for Amex Business Platinum?

American Express doesn’t specify a minimum income requirement for the Business Platinum Card. But, MyFico forums have a lot of anecdotal stories that suggest that they expect applicants to demonstrate significant income or business revenue to justify approval.

Final Takeaway

American Express Business Blueprint took what Kabbage started and expanded it into a full-scale financial platform. With better lending terms, a solid business checking account, and improved cash flow tools, it’s a clear upgrade.

However, some drawbacks remain, like limited integrations and an inconsistent mobile app experience. If you’re an Amex cardholder looking for streamlined business banking and financing, it’s worth considering—just be aware of its gaps.

Are you ready to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!