In the realm of business banking, Apple Federal Credit Union (Apple FCU) is a local cooperative institution that caters to the needs of small businesses in Northern Virginia—Unlike traditional big banks, credit unions like Apple FCU operate as member-owned entities that prioritize personalized service and community engagement over profit margins.

Here, we’ll delve into Apple FCU’s array of business banking solutions, including their credit card, loans, and other tailored products. Learn about their commitment to supporting local businesses while providing competitive financial offerings to decide if this is the place to do your business banking.

This is what’s in store:

- What is Apple Federal Credit Union?

- Business Financial Products & Services

- Apple FCU Customer Service

- Apple FCU Community Involvement

- Frequently Asked Questions

- Conclusion

Now, let’s roll!

What is Apple Federal Credit Union?

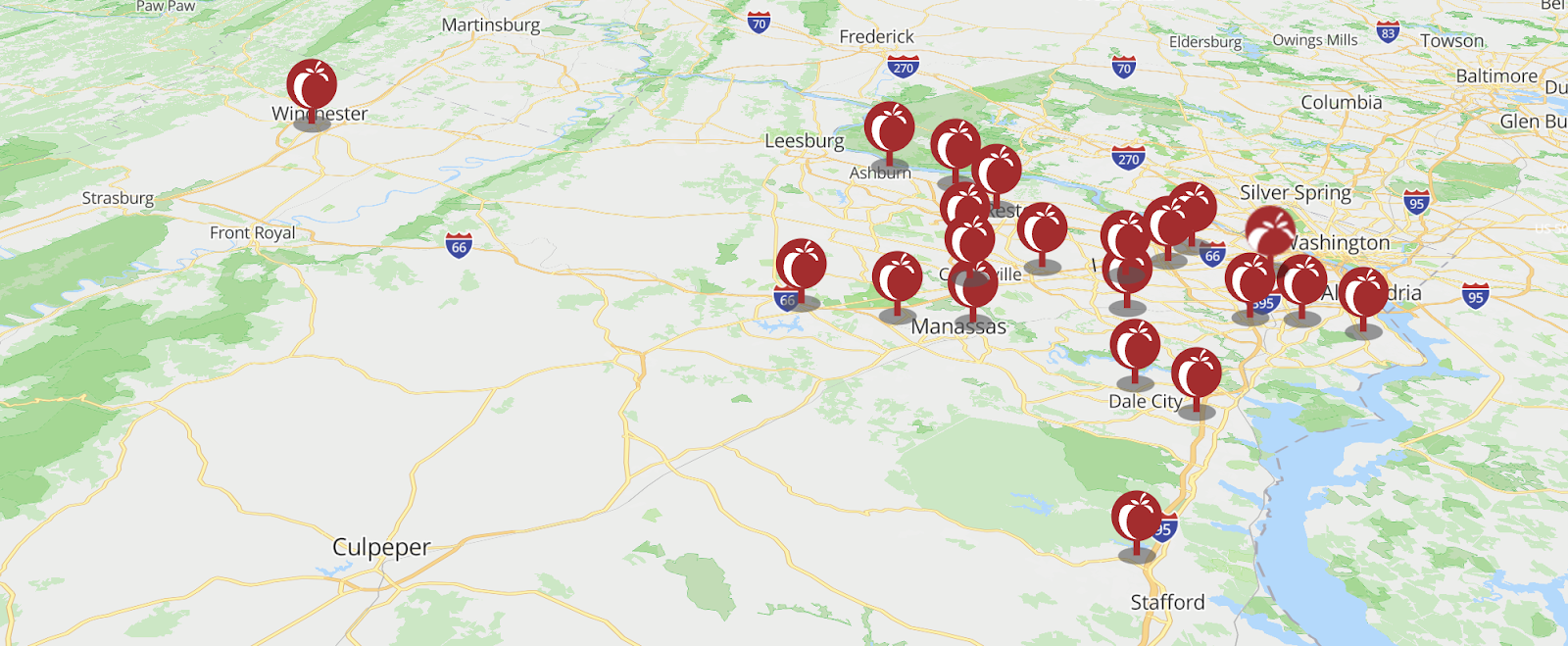

Apple FCU is a member-owned financial cooperative located in Fairfax, Virginia. It started in 1956, initially serving educators, and has since grown to include a broader membership. With 21 branches in Northern Virginia and access to over 33,000 ATMs nationwide, Apple FCU aims to make banking convenient for its members.

Apple FCU is particularly dedicated to supporting small businesses—They offer a range of services designed to meet the needs of business owners, including various types of loans, checking accounts, and financial planning resources.

The credit union understands the challenges small businesses face and provides products to help manage finances effectively:

- Apple FCU offers competitive rates on business loans, which can help you fund growth or manage day-to-day operations.

- Their business checking accounts are designed to meet different business needs, often with no monthly fees and easy access through online and mobile banking.

- You can find resources and tools to help manage your business’s cash flow, ensuring financial stability.

- Apple FCU provides articles and seminars on important financial topics, helping you make informed decisions for your business.

As a business member, you’ll get personalized service, with professionals available to guide you through your financial decisions and help optimize your operations.

They aim to positively impact the communities they serve and make their products and services easy to understand and use. Whether you’re looking to manage your personal finances or support your small business, Apple FCU offers resources and support to help you achieve your financial goals.

Recommended: 3 Best Credit Unions for Small Business Banking in 2024

Apple FCU Locations Served

Apple Federal Credit Union (Apple FCU) serves businesses primarily in Northern Virginia, where it has 21 local branches. The branches are strategically located in various communities to ensure easy access for members. You can find branches in cities such as Ashburn, Falls Church, Burke, Centreville, Chantilly, Fairfax, Gainesville, Herndon, Alexandria, Woodbridge, Manassas, Springfield, Stafford, Sterling, and Winchester.

Despite its focus on Northern Virginia, Apple FCU offers online services that provide broader, nationwide accessibility. Through their online and mobile banking platforms, you can manage your accounts, make transactions, and access a wide array of financial tools and resources from anywhere in the country. Additionally, Apple FCU is part of a nationwide fee-free ATM network, which allows you to withdraw cash and manage your accounts without incurring extra fees, even if you are outside Northern Virginia.

By combining local branch access with comprehensive online services, Apple FCU ensures that both local businesses and those operating on a broader scale can benefit from their financial products and personalized service.

You might also like: Should You Open a Navy Federal Credit Union Business Account?

Apple FCU Membership & Eligibility

Apple FCU offers membership to a wide range of individuals and businesses—To become a business member, there are several eligibility criteria you can meet:

- First, you can qualify based on your location if you live, work, worship, volunteer, or attend school in specific areas of Northern Virginia, including Fairfax County, Prince William County, the City of Fairfax, and several others.

- Second, you can join if you are affiliated with various school systems or educational institutions. This includes faculty, staff, students, and immediate families of schools such as Fairfax County Public Schools and universities like George Mason University.

- Third, relationship-based eligibility allows immediate family members of existing members to join, as well as household members living with a current member. Additionally, joining certain associations, like the Friends of the W&OD Trail, can also make you eligible.

- Lastly, employment at one of the numerous partnered businesses or organizations can qualify you for membership. This includes a wide range of companies and associations, from Alexandria Bar Association to Costco Sterling.

To join Apple FCU, you need to complete an online application, which takes less than five minutes. You start by choosing a Checking account (which includes Regular Savings) or just a Regular Savings account—Once you’re a member, you can open business accounts or apply for loans through Apple FCU Online or the Mobile App.

Now, let’s dive into the specific business banking and loan features Apple FCU offers. These include a variety of commercial loans, credit cards, and other services designed to help your business manage finances and grow effectively.

Business Financial Products & Services

Apple FCU offers a comprehensive suite of services to support business members, including a variety of banking options, credit cards, and loan products. They provide several types of checking and money market accounts designed for different business needs, such as Core, Core Plus, Core Advantage, Core Corporate, and Money Market accounts.

Their credit card offerings come with flexible spending limits and rewards, while their merchant services help manage transactions efficiently. Moreover, they offer advanced business management systems, including retail POS and mobile solutions, cash management tools, payment acceptance and processing, and fraud prevention measures.

Here, we’ll dive into the specific features of their business banking services and loan products—explore how Apple FCU can support your business operations and growth!

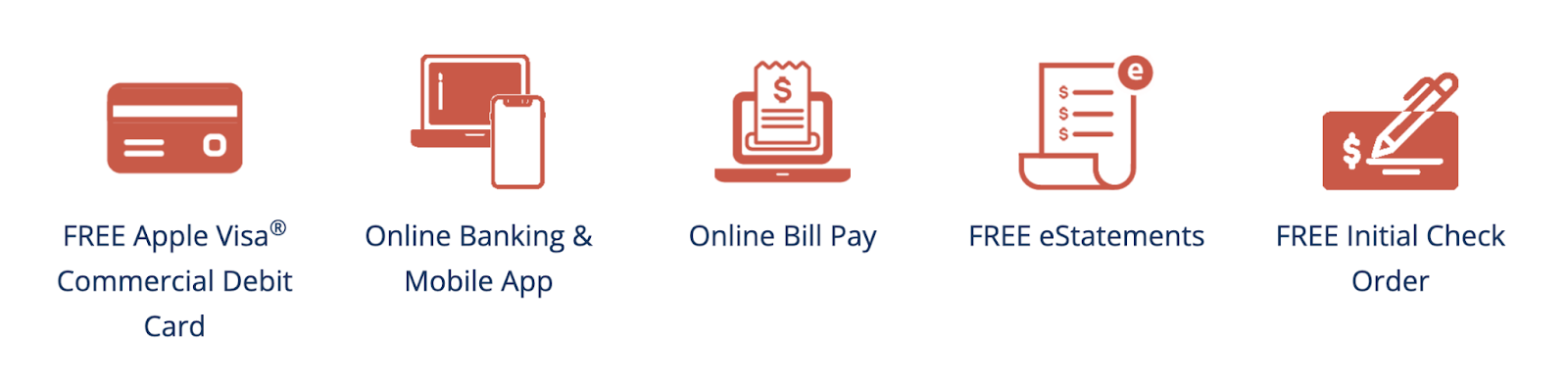

1. Apple FCU Business Checking Accounts

Apple Federal Credit Union (Apple FCU) offers a variety of business checking accounts designed to meet the needs of businesses of different sizes and transaction volumes. Here’s an overview of what they offer and how they support small business growth.

All business checking accounts come with several key features: a free Apple Visa® Commercial Debit Card, online banking and mobile app access, online bill pay, free eStatements, and a free initial check order:

- Core checking account

- Core Plus checking account

- Core Advantage checking account

- Core Corporate checking account

The Core checking account is perfect for small businesses looking for a simple, cost-effective option. It requires no monthly maintenance fee and has a $50 minimum opening deposit. You’ll get 200 free items per month, including paid checks, items deposited, deposit tickets, and ACH credits/debits received. If you go over 200 items, there’s a fee of $0.30 per item. Cash deposits and withdrawals over $5K cost $2 per $1K.

For businesses with moderate transaction activity, the Core Plus checking account is ideal. It also has a $50 minimum opening deposit and offers 300 free items per month. If you exceed 300 items, there’s a $0.30 per item fee. This account has a monthly maintenance fee of $15 if the average daily balance falls below $2,500. Cash deposits and withdrawals over $5K also cost $2 per $1K.

The Core Advantage checking account is designed for larger businesses with higher transaction volumes. It requires a $5K minimum opening balance and pays dividends monthly at an APY of 0.05%. You get 500 free items per month, with a $0.30 fee for each additional item. The monthly maintenance fee is $25 if the average daily balance falls below $5K. Cash deposits and withdrawals over $5K cost $2 per $1K.

For businesses with substantial balances and transaction needs, the Core Corporate checking account is the best option. It requires a $15K minimum opening balance and pays dividends monthly at an APY of 0.40%. The monthly maintenance fee is $25 if the average daily balance falls below $15K. The excessive items fee is $0.15 per debit, $0.30 per credit, and $0.10 per item deposited. Cash deposits and withdrawals over $5K cost $2 per $1K.

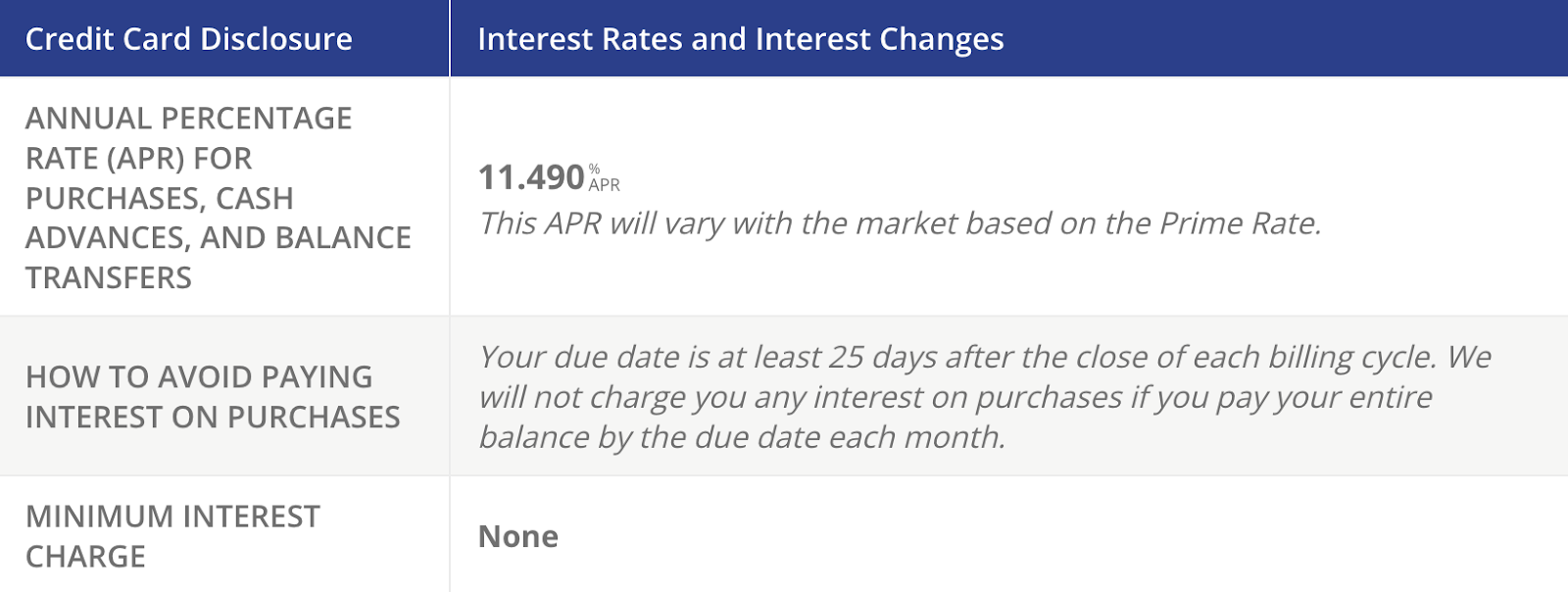

2. Apple FCU Visa® Business Rewards Credit Card

Apple FCU offers the Visa® Business Rewards Credit Card, which provides robust spending power, rewards, and features to streamline expense management.

The Visa® Business Rewards Credit Card has credit lines up to $50K, which caters to businesses with varying credit needs. One of its key advantages is the absence of an annual fee, combined with a competitive, variable interest rate (13.24% to 18%)—This makes it an affordable option to manage business expenses.

Cardholders can earn points for every purchase, which can be redeemed for:

- Cash

- Gift cards

- Other rewards.

Additionally, the card includes Visa’s Zero Liability policy – protection against unauthorized charges – and 24/7 account screening to help prevent fraud.

The card also offers several tools to make managing business finances easier. You can track expenses online or through the mobile app, reconcile accounts, and set up multiple users with “sub-accounts.” These features help streamline daily cash management and provide detailed tracking and reports.

Recommended: Corporate vs Business Credit Card: What’s the Difference?

3. Apple FCU Business Loans

Apple FCU offers a wide array of business loan options to support different financial needs. As with their other products, the rates are competitive and tend to be lower than what you would expect from a big bank.

Their business loan options include:

- Term loans

- Equipment financing

- Working capital loans

- Real estate loans

- SBA 504 loans

- SBA 7(a) loans

- Vehicle loans

Term loans provide funding for long-term investments or purchases, while equipment financing helps businesses acquire necessary equipment. Working capital loans assist with managing cash flow and covering operational expenses. Real estate loans support businesses in purchasing, refinancing, or renovating commercial properties.

SBA loans, including 504 and 7(a) options, offer government-backed financing for various business purposes. Additionally, vehicle loans are available to assist with purchasing business vehicles.

Recommended: How to Get Money for Real Estate Investing: 18 Practical Ideas

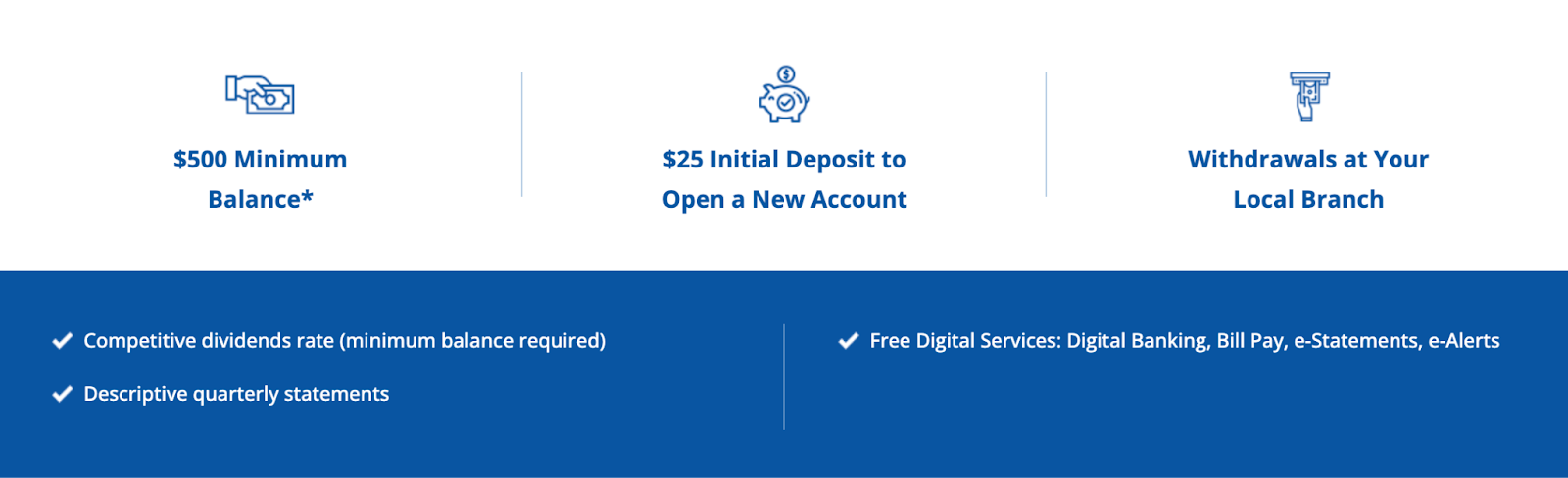

4. Apple FCU Business Savings & Investment Opportunities

Apple FCU doesn’t have a “regular” share for business—Instead, they offer a couple of other savings options as ways to manage your excess cash:

- Business “Sweep” Accounts

- Business Money Market Accounts (MMAs)

Both the Business Sweep Account and the Money Market account offer secure and NCUA-insured options to help your business manage and grow its funds with peace of mind.

The Business Sweep Account provides a convenient way to maximize the potential of profits—With no transaction limit, you can seamlessly manage your funds while earning tiered dividends. By setting a target balance for your checking account, any excess funds are automatically transferred into an interest-bearing account each night.

This streamlined approach allows you to focus on running your business while Apple FCU helps your money work harder for you. With a minimum balance requirement of $25K, the Business Sweep Account offers a cost-effective solution to grow your business’s funds.

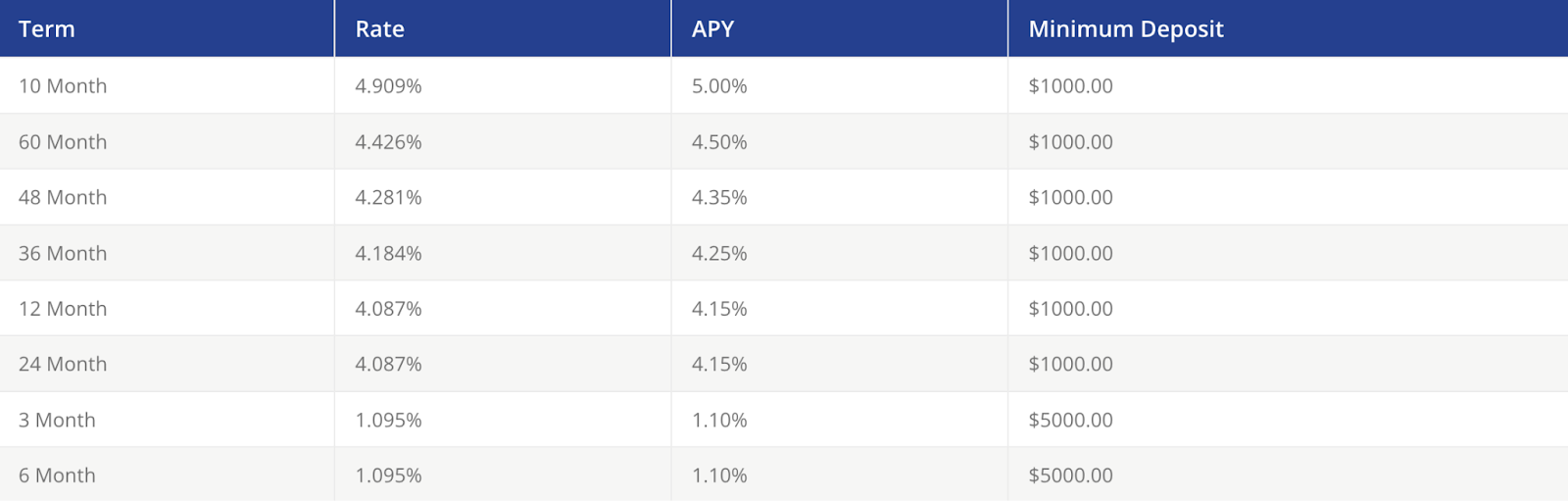

Next, the MMA offers a premium rate of up to 5.00% APY, allowing you to put your capital to work for your business. With no monthly maintenance fees or ongoing balance requirements, this account provides flexibility and accessibility to your savings.

You can make deposits into your business MMA in any amount at any time, and dividends are compounded daily and paid monthly, helping your funds grow steadily over time. With a minimum opening deposit of $1 million, this account is designed to support your business’s savings goals effectively.

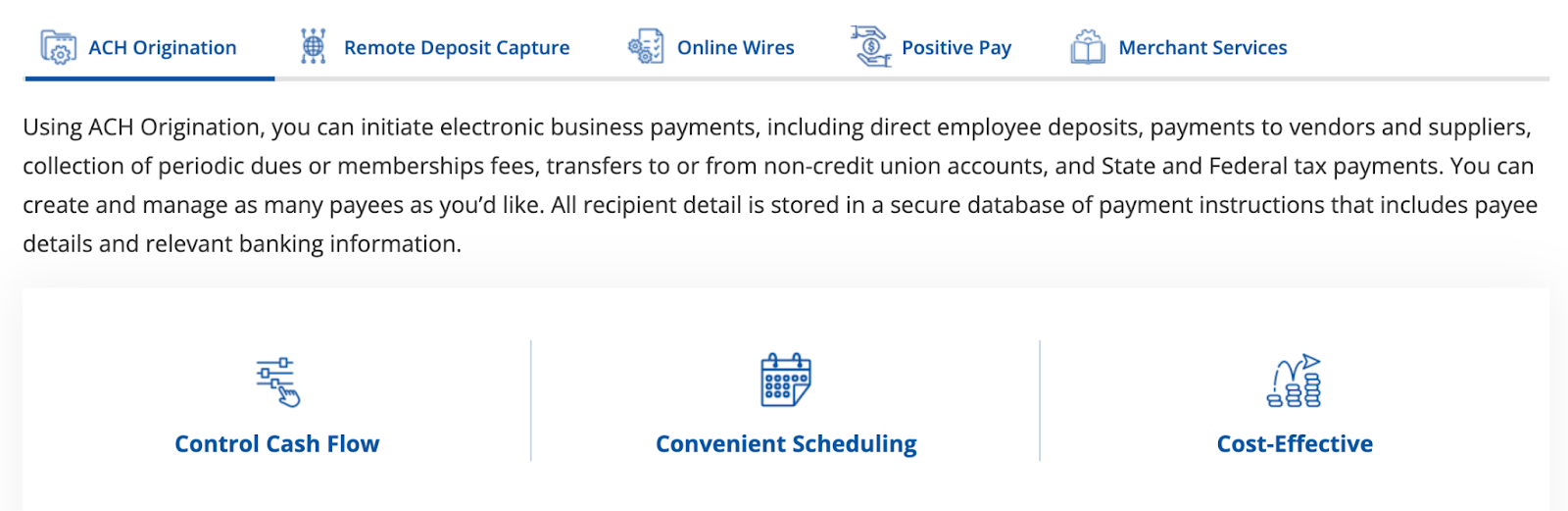

5. Apple FCU Business Treasury Services

Apple FCU offers a comprehensive range of business treasury services designed to help businesses manage their finances efficiently and effectively.

Apple FCU provides payment processing solutions tailored to businesses’ needs, with competitive rates, personalized customer service, and the latest technology to streamline transactions. The credit union offers a suite of tools and services to manage business operations seamlessly, including POS systems, back-office solutions, industry-specific products, and more.

Smart POS systems provide customizable and integrated transaction experiences, offering options like:

- Clover Station Duo

- Clover Station Solo

- Clover Flex

- Clover Mini

Advanced payment terminals boast speed, versatility, and integration with back-office devices like:

- Desk/3500

- Move/5000

- Lane/3000

They also offer a range of additional services, including software integration, website development, municipal invoicing, donation management, check services, gift/loyalty cards, and property management tools.

Overall, Apple FCU’s business treasury services aim to provide businesses with efficient, secure, and customizable solutions to manage their finances, streamline operations, and drive growth.

Recommended: What’s the Best Payment Processor for a Small Business? Really

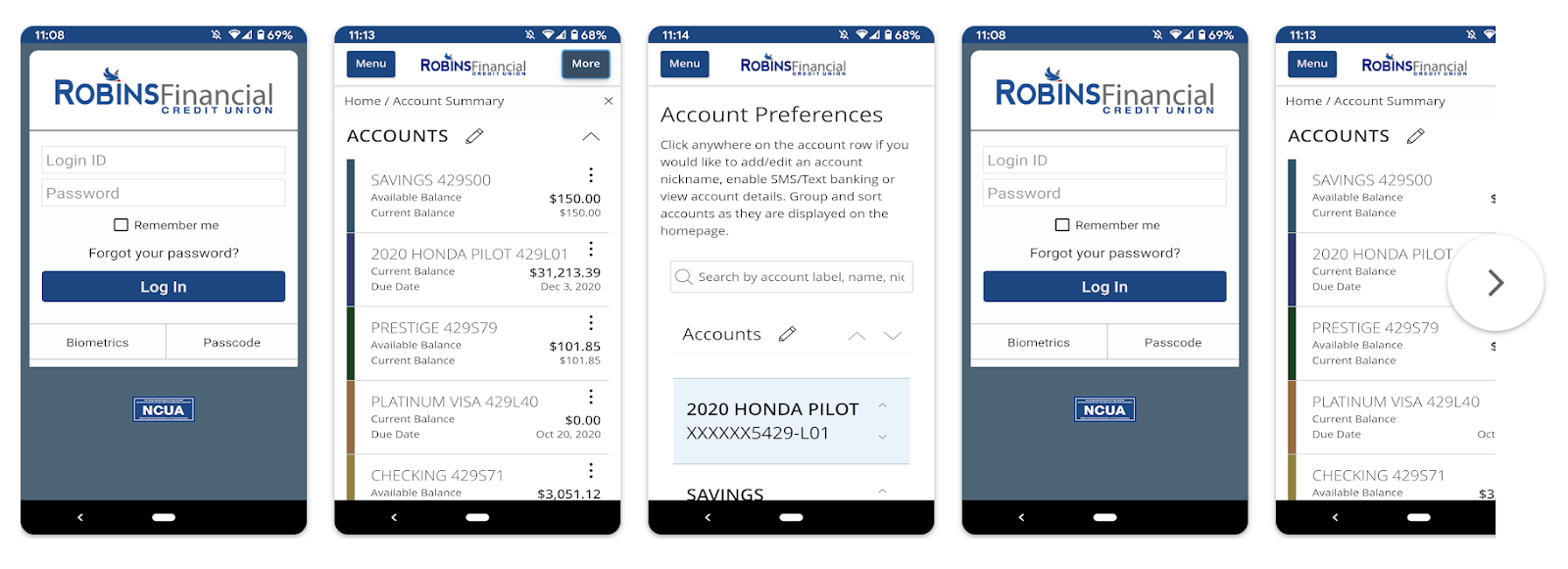

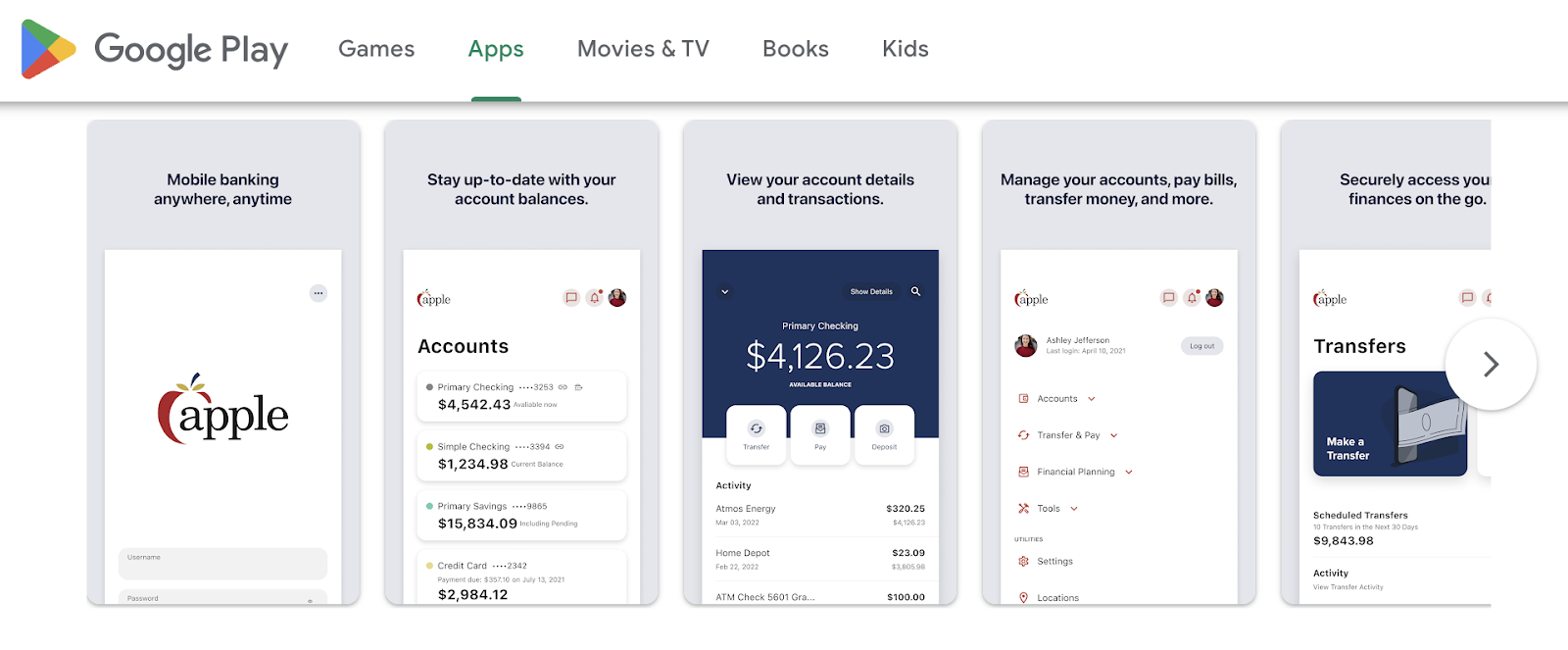

6. The Apple FCU Mobile App

As a business member, Apple Federal Credit Union’s mobile app is gonna be your go-to tool for managing your personal and business finances on the fly.

Here’s what you can expect:

- Check your balances, transfer funds between accounts, view your loan and credit card history, make payments, and even deposit checks—all from the convenience of your phone.

- Say goodbye to the hassle of paper bills. With the app, you can pay your bills with just a few taps, making it super easy to stay on top of your finances.

- Set up alerts and notifications based on your account activity. Whether it’s a low balance alert or a payment confirmation, you’ll always be in the know.

Some users mention occasional login glitches, such as difficulties with Face ID or biometric authentication, and slower performance compared to other banking apps. There are also requests for additional features like a dark mode for users with visual impairments.

However, many users appreciate the app’s modern interface and ease of use, acknowledging the improvements made over previous versions. Overall, while there are some minor issues, Apple FCU seems committed to addressing user feedback and enhancing the app’s functionality for its members.

You might also like: Meet the Emburse Card: An Inclusive Cash Back Corporate Card

Apple FCU Customer Service

Apple FCU offers dedicated customer service for business members, providing support via:

- Phone

- Secure email

- Live chat

- In-person at branches (during business hours)

Business members can contact representatives Monday through Friday from 8 a.m. to 6 p.m., and on Saturdays from 9 a.m. to 1 p.m.

And, there are specific contact channels for Visa card inquiries, mortgage questions, and even the option for virtual appointments via Video Banking to discuss financial goals. This array of communication options ensures that you’ll have access to assistance tailored to your needs, whether you prefer online, phone, or face-to-face interactions.

Apple FCU in the Community

In all, Apple FCU demonstrates a strong commitment to community initiatives and social responsibility, particularly through its Apple FCU Education Foundation—The foundation awards college scholarships to high school seniors who have shown dedication to their schools and communities.

Plus, Apple FCU recognizes educators like Jeffrey “JJ” Kuchan, who received the New Educator of the Year award for his exceptional contributions to Osbourn Park High School. Through volunteerism and philanthropy, Apple FCU supports various causes, including scholarship programs and COVID-19 relief efforts, with employees contributing over 1,000 hours annually.

However, it’s important to mention recent criticism, including a class action lawsuit alleging unlawful overdraft fee practices, which may impact the credit union’s reputation among its members.

Frequently Asked Questions

How to use Zelle with Apple Federal Credit Union?

To use Zelle with Apple Federal Credit Union, you can access Zelle directly through the credit union’s mobile app or online banking platform. Simply log in to your account, navigate to the transfer or payments section, and select Zelle. Follow the prompts to enroll and start sending or receiving money with Zelle.

How to find account number on Apple Federal Credit Union app?

To find your account number on the Apple Federal Credit Union app, log in to your account and navigate to the account details section. Your account number should be listed there along with other account information such as balance and transaction history.

What time does Apple Federal Credit Union close?

Apple Federal Credit Union typically closes at 6 p.m. on weekdays and 1 p.m. on Saturdays. However, it’s always a good idea to check the specific branch hours on the credit union’s website or contact them directly for the most accurate information.

What time does Apple Federal Credit Union open?

Apple Federal Credit Union typically opens in the morning on weekdays, but the exact opening time may vary depending on the branch location. It’s best to check the specific branch hours on the credit union’s website or contact them directly for the most accurate information.

Is Apple Federal Credit Union owned by Apple?

No, Apple Federal Credit Union is not owned by Apple Inc. Despite sharing a similar name, Apple FCU is a separate financial institution that operates independently, providing banking services to its members.

Conclusion

Apple FCU offers a range of financial solutions tailored to the needs of small businesses in Northern Virginia—With competitive rates on loans, diverse checking account options, and a Visa Business Rewards Credit Card, Apple FCU provides valuable tools for business growth.

However, recent criticism, including a class action lawsuit alleging unlawful overdraft fee practices, raises concerns about the credit union’s transparency and adherence to fair banking practices.

Despite these challenges, Apple FCU remains committed to addressing user feedback and enhancing its services, aiming to provide comprehensive support for business members while maintaining a strong community focus.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!