A lot of my students at Business Credit Workshop have been approved for the Truist business credit card recently. After hearing their stories, I want to share everything I know about the offer and what I’ve learned (including whether the rewards are worth it if you don’t have a Truist checking account).

There are three Truist business credit cards currently available, each with their own unique set of features. We’ll explore them here, along with more info about Truist bank and how well they cater to small businesses. Find out if the card is worthwhile in your situation.

This is what’s in store:

- What is a Truist Business Credit Card?

- The 3 Truist Business Credit Cards

- More Truist Small Business Products

- Frequently Asked Questions

- Conclusion

Now, let’s roll!

What is a Truist Business Credit Card?

A Truist business credit card is designed to meet the credit needs of small businesses. It offers various benefits tailored to business spending, like cash back rewards on purchases. Plus, you’ll get a Loyalty Cash Bonus when you deposit your cash rewards into an eligible Truist business checking, savings, or money market account.

Truist has three business credit cards for varying needs—there’s a card for:

- Cash rewards

- Travel rewards

- General business expenses

Each card has its own set of features, fees, and rewards structure. So you’ll want to compare them to find the best fit for your business (which we’ll do below).

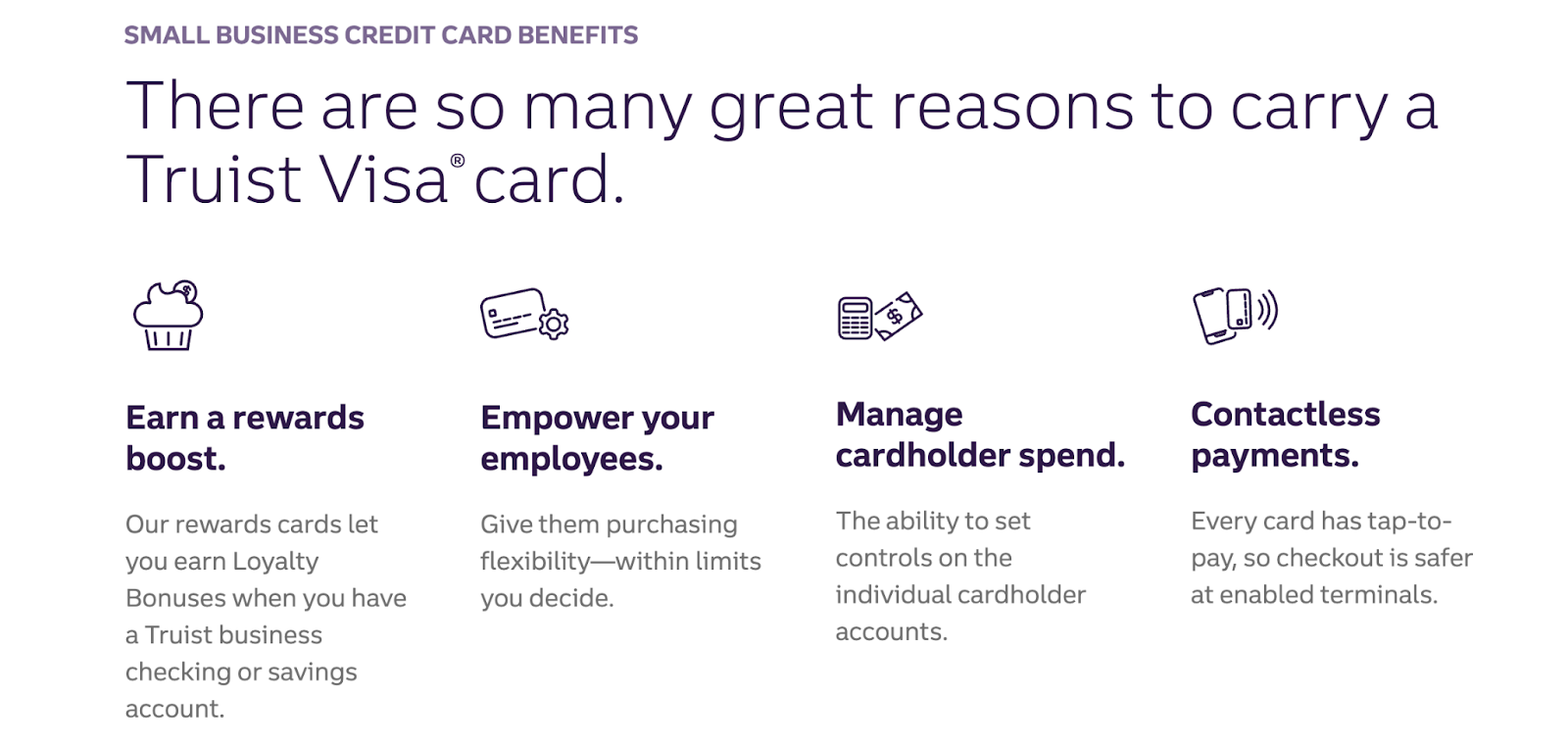

These cards also provide flexibility for your employees with customizable spending limits and controls on individual cardholder accounts. And, they come with contactless payment options for added convenience and security at enabled terminals.

You can manage your Truist business credit card online to access your account, redeem rewards, view transactions, and set up alerts. You can also manage employee cards, integrate with accounting software, and get resources for better business strategies.

You might also like: 6 Best 0% APR Business Credit Cards to Check Out

Truist Business Credit Card Pre-Approval

At some point, Truist had a pre-qualification page for business owners to see if they could obtain credit through Truist—This apparently triggered a soft pull, which would protect your credit from the ding on your credit report.

But, does Truist still have pre-approval? Today, I can’t find any sign of such a page on the company website. Instead, I do see a disclaimer that by applying, you give Truist permission to access and update your credit report. So, when you apply, it will likely have a slight impact on your credit score.

Truist evaluates both personal and business credit. When considering business cards, Truist utilizes Equifax personal credit reports, but claims to prioritize business credit scores over personal credit scores on applications for business products.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

Truist Business Credit Card Requirements

Before you move forward and learn more, you should know what you need to Apply for a Truist business credit card.

Note: Truist does offer secured cards, so a low credit score (below 640) won’t necessarily disqualify you from obtaining credit through the bank…you will just have to work toward it.

To qualify, Truist wants you to have excellent personal and business credit—you’ll need:

- Basic details about your business

- Business Tax ID

- Your personal street address

- Phone number

- Social Security number

- Names and emails of people involved in the application

You can apply online with electronic signatures and email communication or visit a branch to complete the Truist business credit card application. For-profit businesses will need at least one Guarantor. And, nonprofits don’t need a Guarantor.

You might also like: Everything You Need to Know About a DUNS Number +Why You Should Care

Company Overview

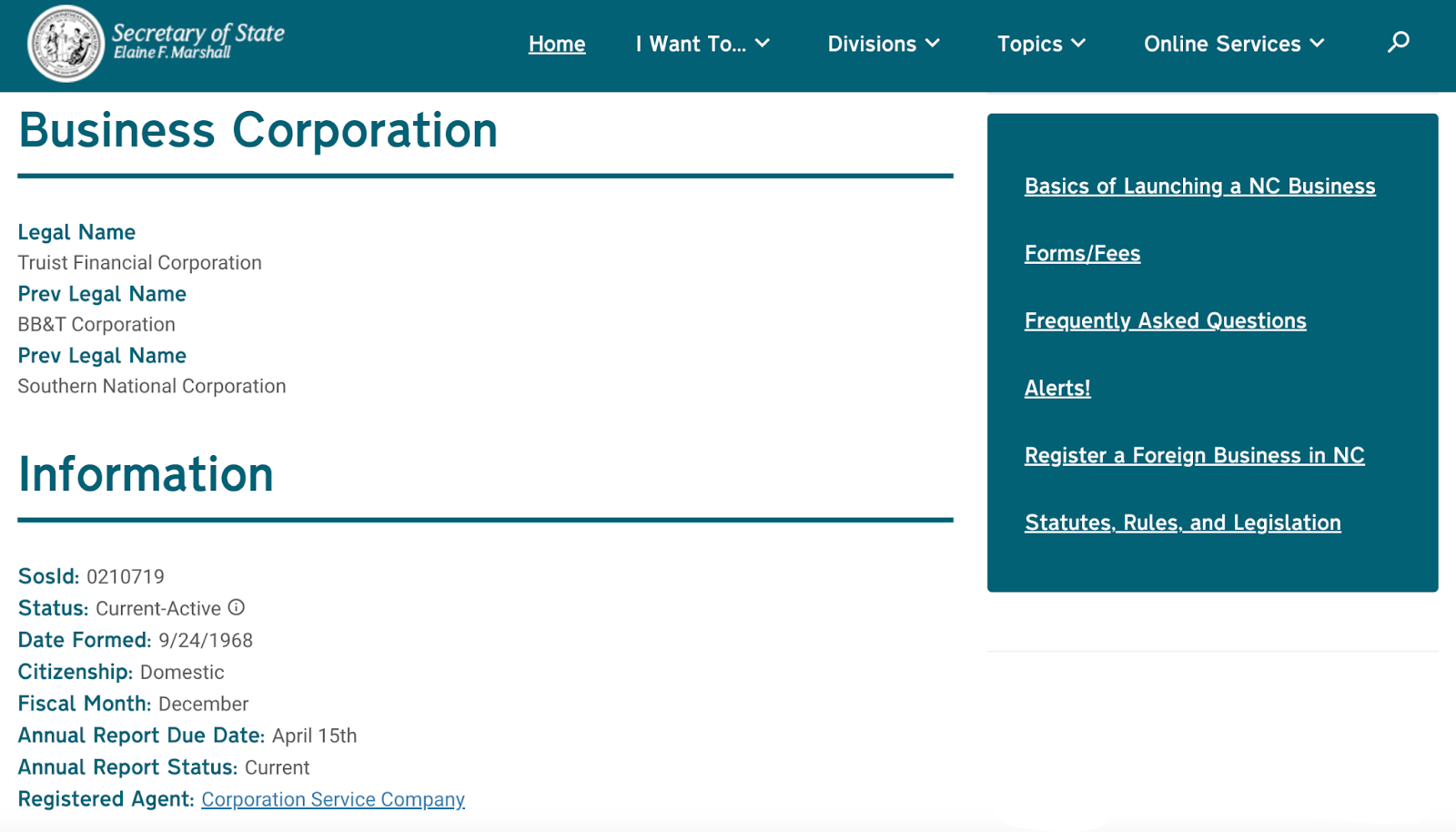

Truist Financial, or Truist Financial Corporation, is a Charlotte North Carolina-based, for-profit investment bank. In 2019, Truist Financial was formed from the merger of BB&T and SunTrust. With a combined history spanning 275 years, Truist serves approximately 12 million households, holding significant market share in key growth regions across the country.

Their diverse range of services includes:

- Retail, small business, and commercial banking

- Asset and wealth management

- Capital markets

- Real estate

- Insurance

- Mortgage

- Payments

- Specialized lending

Truist apparently ranks as the sixth-largest commercial bank in the United States, operating as “Truist Bank” under FDIC membership.

According to the North Carolina Secretary of State, the company is active and in good standing—they’re current with their annual reporting.

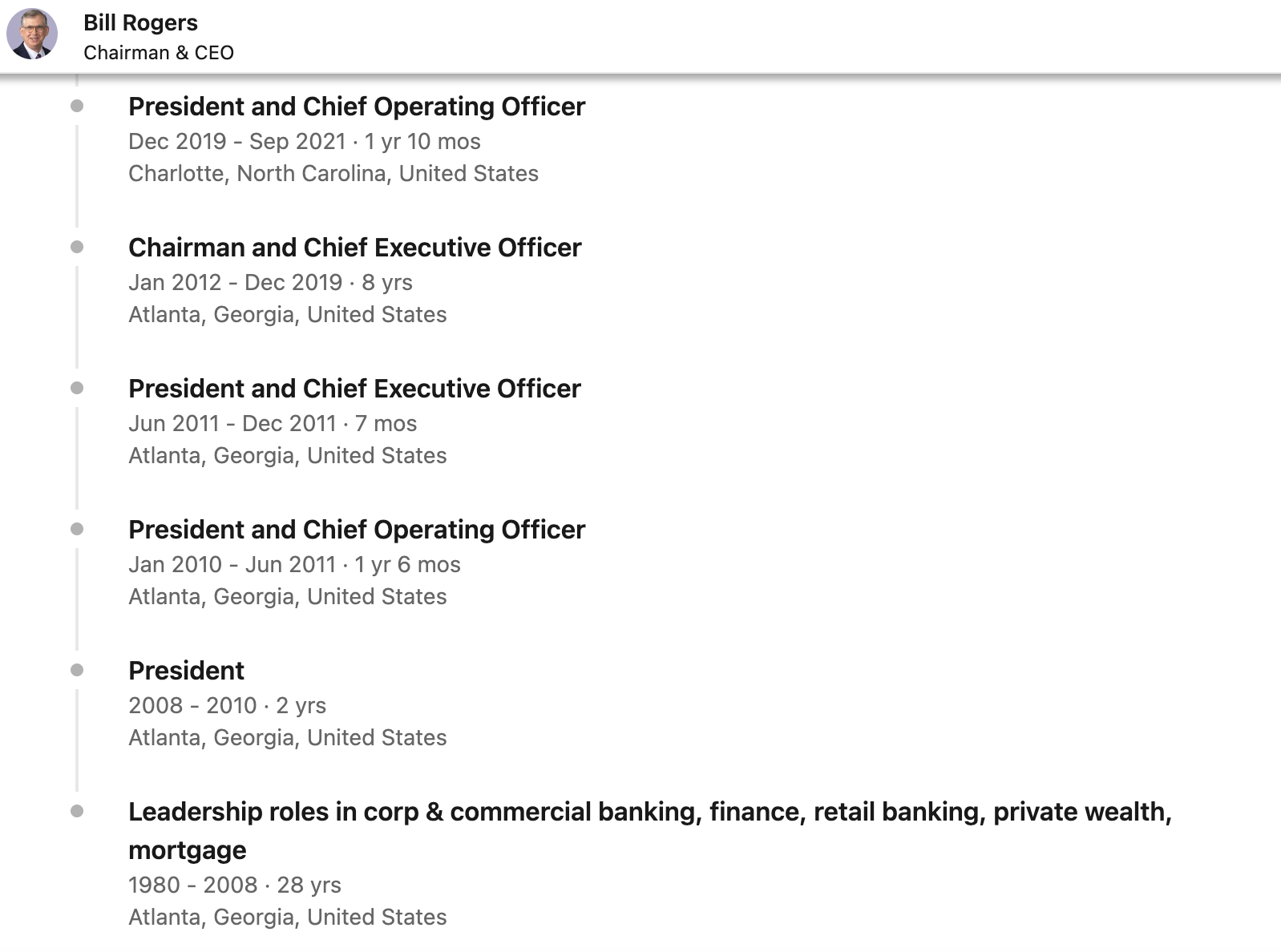

Truist Financial’s current CEO is William H. Rogers Jr., aka “Bill” Rogers. Bill has led the company, in one position or another, since 1980. It’s safe to say, he’s been a decision maker since at least 2008, when he took the role of President.

According to Glassdoor, less than half of employees would recommend a job at the company with a friend. And, about half approve of Rogers as CEO. So, while some people love working here, others aren’t so fond of the company, which speaks to their internal ethics.

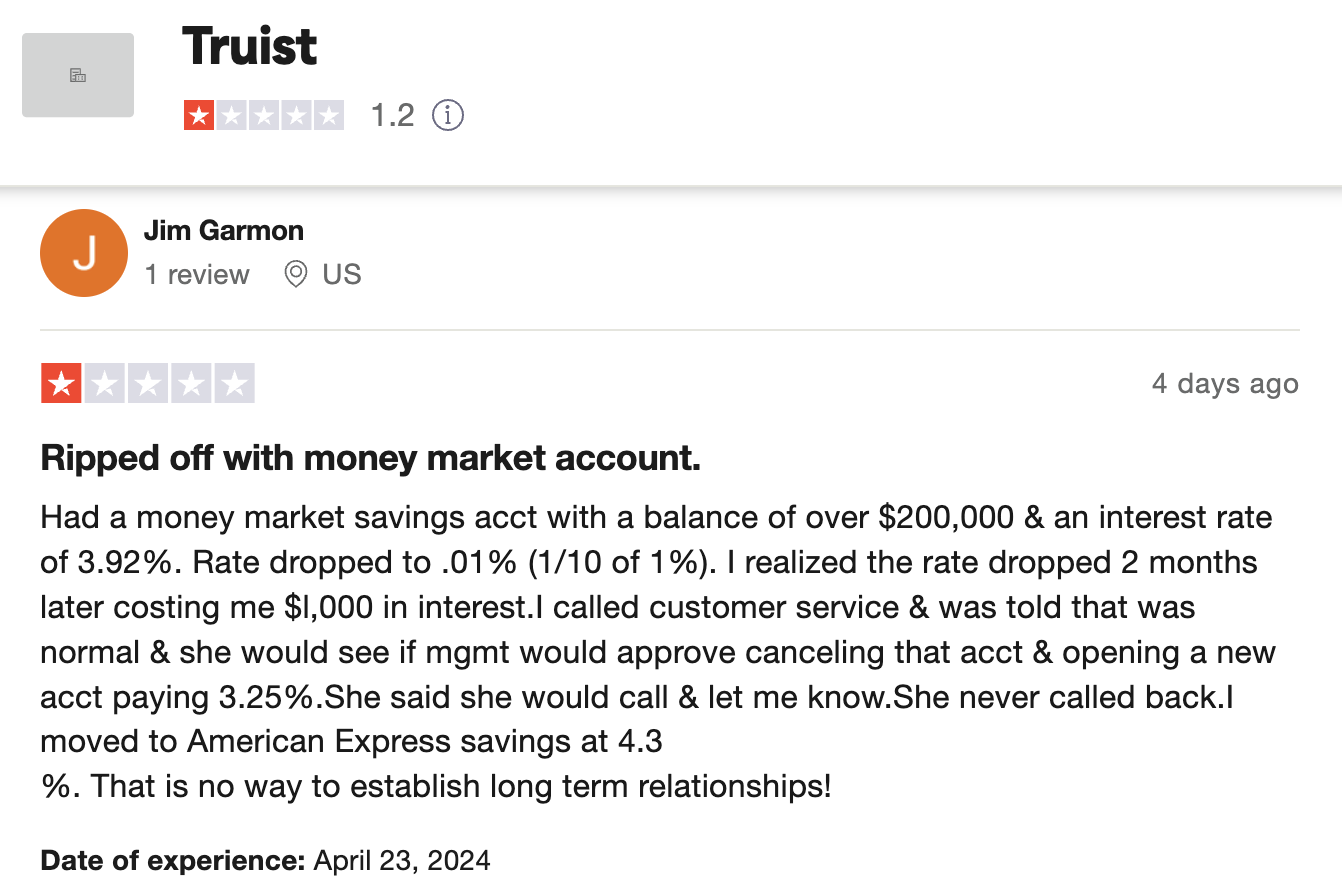

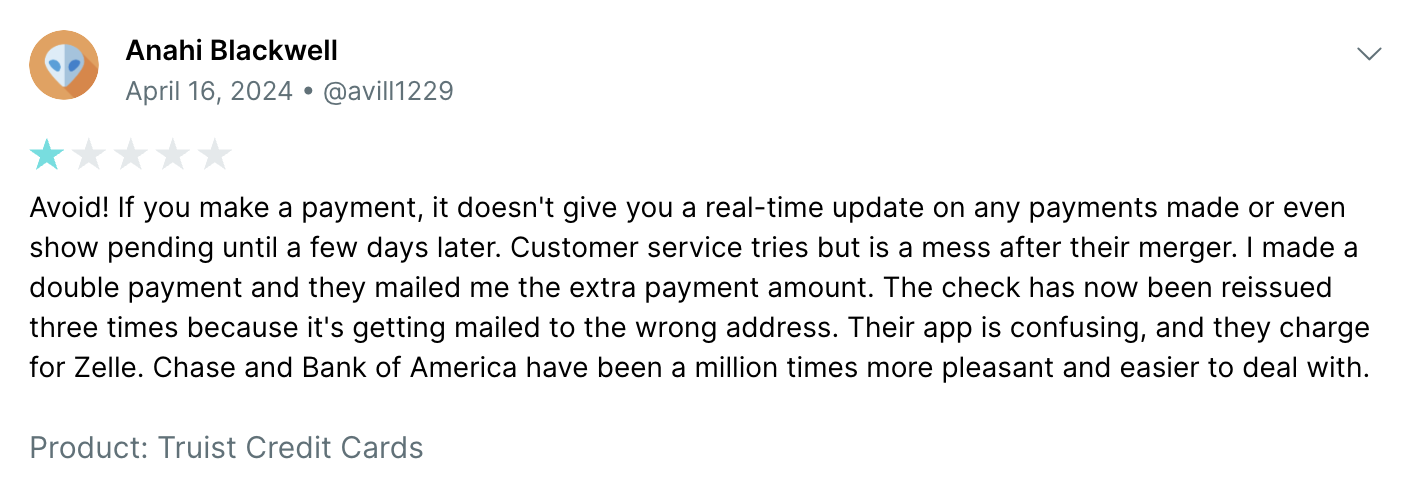

Even more important is what their customers think. Out of X,XXX reviewers on Trustpilot, Truist has an average 1-star (bad) rating. Most of the complaints point to customer service, but some people are completely dissatisfied with the financial products as well.

In general, Wallethub reviewers seem to have similar sentiments about Truist. Most people have complaints about customer service. Some people have said that their experience with Suntrust Bank was better before the 2019 merger.

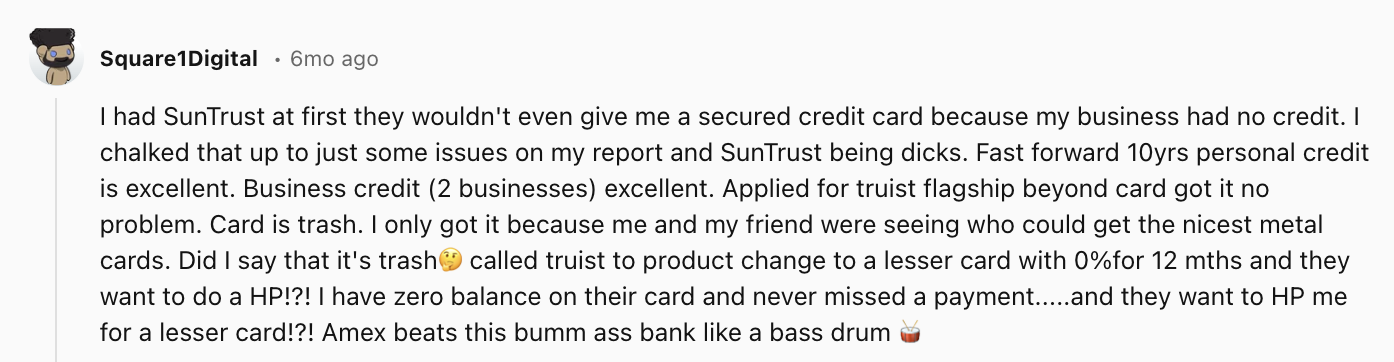

And, Redditors seem to believe the company is understaffed to handle all of their customers responsibly. However, at least one has reported that they were able to get a Truist Bank business credit card when they were unable to qualify through Suntrust—This tells me the qualifications may be less stringent now.

Despite their 1-star rating with the Better Business Bureau (BBB), Truist Bank maintains an A+ rating on the platform. And, they’ve been BBB accredited for nearly 60 years.

Now, in response to all of the negative reviews, I’ve only heard good things from my Business Credit Workshop students.

Finally, as far as legal problems, the bank isn’t squeaky clean—Truist Financial Corp. recently settled a case for $6.3 million, concerning allegations of unjustly reducing interest rates on high-yield money market accounts opened by customers 30+ years ago.

With all of this, it’s not easy to make a recommendation for this bank, but some business credit card holders I know have been satisfied.

Recommended: 6 Best Business Credit Cards for Entrepreneurs: Fuel Your Growth

The 3 Truist Business Credit Cards

Now, Truist offers three business credit cards:

- Truist Business Cash Rewards Credit Card

- Truist Business Travel Rewards Credit Card

- Truist Business Credit Card

Let’s take a closer look at each of them!

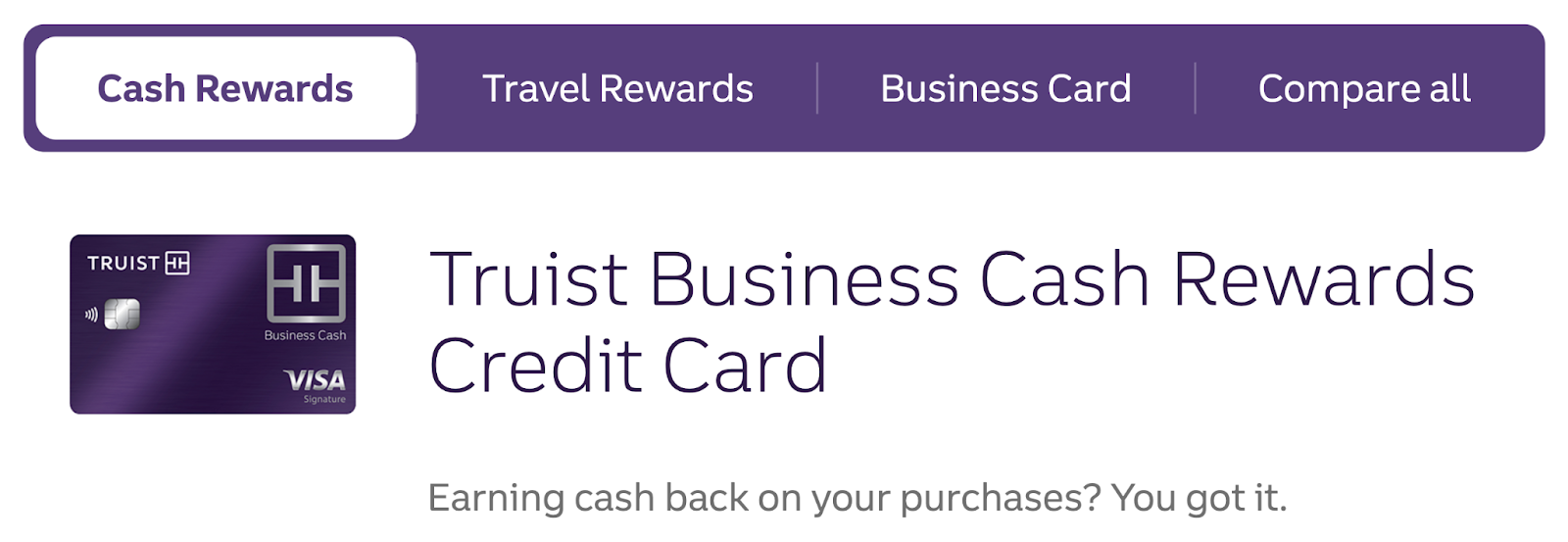

1. Truist Business Cash Rewards

Truist Business Cash Rewards Credit Card comes with no annual fee and an introductory APR of 0% on purchases for the first 9 months (which later ranges from 17.49% to 26.49% variable APR).

This card offers cash back rewards, including:

- 3% on gas

- 2% at restaurants and office supply stores (up to $2,000 in combined spend per month)

- 1% on all other eligible purchases

Additionally, cardholders can earn a Loyalty Cash Bonus of 10%, 25%, or 50% when depositing cash rewards into an eligible Truist business checking, savings, or money market account.

This card is ideal for businesses that spend a significant amount of time on the road entertaining clients or making everyday business purchases. It could provide cash back rewards on common business expenses like gas and dining.

You might also like: 7 Best Cash Back Corporate Credit Cards to Explore

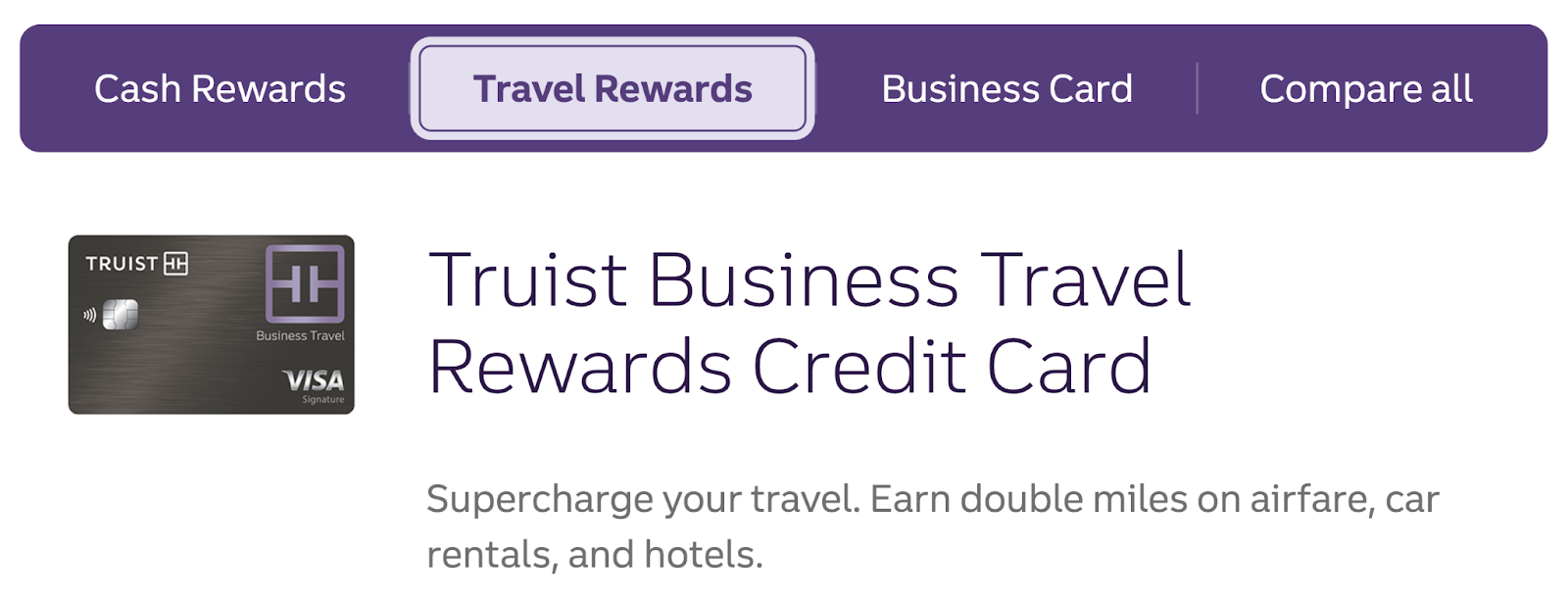

2. Truist Business Travel Rewards

The Truist Business Travel Rewards Credit Card comes with an annual fee of $49, waived for the first year. The APR ranges from 17.49% to 26.49% variable on purchases and balance transfers.

It offers rewards of:

- 2 miles per dollar spent on airfare, hotels, and car rentals

- 1 mile per dollar spent on all other eligible purchases

Cardholders can also earn a Loyalty Travel Bonus of 10%, 25%, or 50% when redeeming miles for travel with a Truist business checking, savings, or money market account.

This card is tailored for businesses with frequent fliers or international travelers. It allows you to earn rewards specifically for travel expenses such as flights, accommodations, and rental cars.

You might also like: What are the Best Business Credit Cards for Travel?

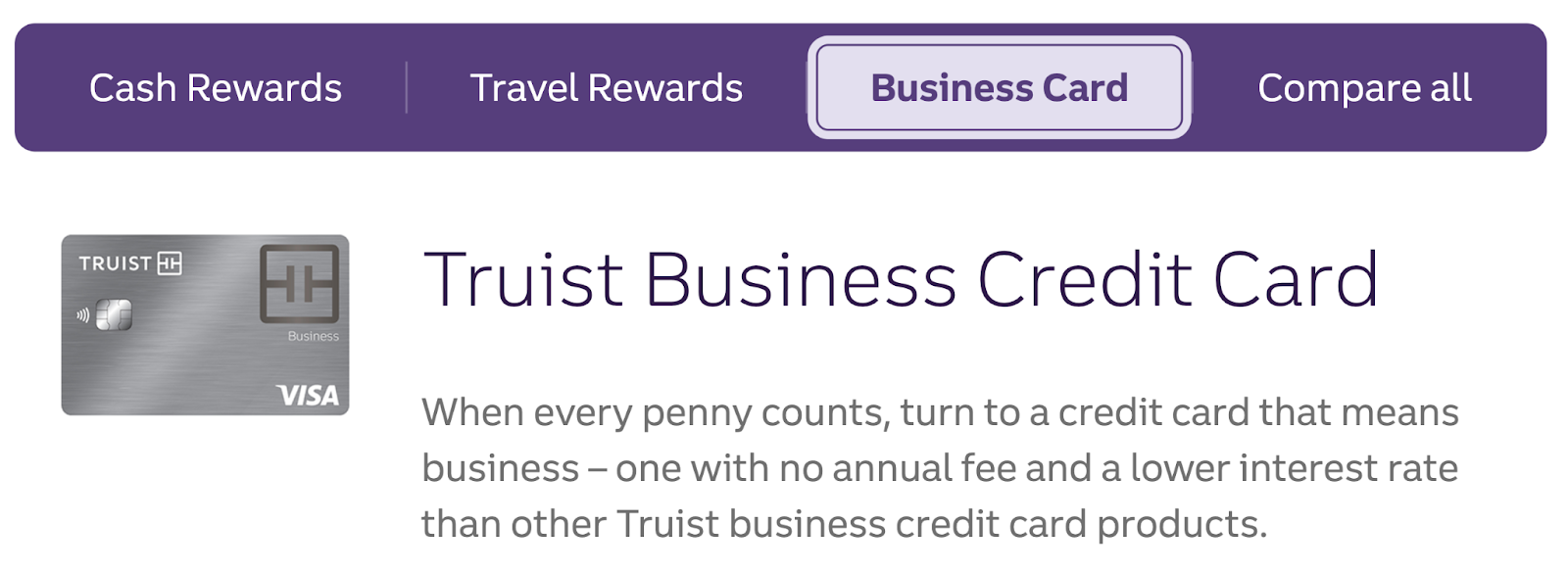

3. Truist Business

The Truist Business Credit Card has no annual fee and an introductory APR of 0% on purchases for the first 12 months (which later ranges from 15.49% to 24.49% variable APR).

Unlike the other cards, it does not offer any loyalty bonuses.

This card is suitable for businesses with low monthly expenses or those who typically carry a balance on their credit cards, offering an introductory 0% APR period and no annual fee.

You might also like: What is the Best Bank of America Business Credit Card for Your Needs?

More Truist Small Business Products

The monthly spending limit on cash back for restaurant and office supply spending on Truist’s Business Cash Rewards Card caught my attention—Once you reach the $2,000 combined limit on purchases within the two main cash back categories, things start to decline.

However, if you’re a Truist business banking customer and meet the requirements for the Loyalty Cash Bonus booster, it could improve your situation. So, you might want to know that, in addition to their business credit cards, Truist also offers a suite of financial services.

With Truist, you can access various business banking solutions like:

- Checking accounts (including Simple Checking, Dynamic Checking, and Community Checking)

- Savings options (including Simple Business Savings, Business Money Market, and Business CDs)

- Online banking

- Payroll management

- Merchant services

- Small business loans (including Simple Business Loan, Auto Loan, Equipment Loan, Real Estate Loan, and Line of Credit)

- Employee benefits

- Insurance options

- A resource center featuring a blog and webinars

Plus, their mobile app is highly rated on the Google Play store and the iOS app store—this might be the highlight of their offer, and it’s worth looking into.

So, if you’re feeling like this might be a good place to seek credit cards, consider Truist’s other banking and business resources.

You might also like: Novo Bank Review: First-Rate Small Business Banking or Scam?

Frequently Asked Questions

Can I get a business credit card using my EIN number?

Yes, you can apply for a business credit card using your Employer Identification Number (EIN). Truist and many other banks allow businesses to apply for credit cards using their EIN rather than their personal Social Security number.

Do I need a business credit card for an LLC?

While not mandatory, having a business credit card for your LLC can help separate your personal and business finances, track expenses, and build credit for your business.

What credit score do you need for a Truist credit card?

Truist does not publicly disclose specific credit score requirements for their credit cards. However, generally, a good to excellent credit score is typically needed to qualify for a Truist credit card.

Does Truist business credit card report to personal credit?

Truist business credit cards may report to personal credit bureaus, depending on the card and your usage. They will typically report activity to both business and personal credit bureaus

What is the minimum credit limit for Truist?

Truist does not specify a minimum credit limit publicly. Credit limits are determined based on various factors including creditworthiness, income, and other financial considerations.

Conclusion

Truist Business Credit Cards offer diverse options tailored to small businesses’ needs. With features like cash back rewards, travel rewards, and no annual fees on select cards, Truist aims to provide valuable solutions for businesses of all sizes. In general, existing Truist customers tend to send more warnings than inviting recommendations—this says a lot.

My students like the card and I haven’t heard any complaints from them.

However, you should carefully consider your specific business needs and financial situation before applying. While Truist does not publicly disclose specific credit score requirements or minimum credit limits, having a good to excellent credit score is generally advisable for approval.

Keep in mind, Truist business credit cards may impact your personal credit score as they may report to personal credit bureaus.

Overall, Truist offers a comprehensive suite of financial products and services beyond credit cards, including checking and savings accounts, online banking, small business loans, and more. Whether Truist is the right fit for your business ultimately depends on your individual needs and preferences.

Do you want to learn how to get up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!