Key Takeaways

- Credit unions often offer lower fees, better interest rates, and flexible lending terms.

- They provide personalized service and easier access to business credit.

- Navy Federal, Financial Resources, and Sound Credit Union are our top choices.

- Other options include Alliant, Consumers, America First, and Digital Federal.

- Small community banks can also offer lower fees and flexible terms.

- Research and compare options to find the best fit for your business.

As a small business owner or founder, where you choose to do your banking can have a major impact on your long-term operations. And, when researching the best bank or credit union for small businesses, you may have realized that you would rather work with a credit union. Now, let’s look at the top credit unions for small business banking.

What you’ll find here:

So, let’s get to it.

First, Are Credit Unions Better Than Banks?

There’s a longstanding debate about whether banks or credit unions are “better.” And, it’s important to understand the difference to answer this question. A bank is a for-profit institution and a credit union is a nonprofit organization that provides comparable financial services. So, what are the advantages of credit unions?

At most credit unions, the shareholders are the members while banks funnel their profits to up the chain to its owners. This means that there is more opportunity for members to save on services and earn a larger percentage of total interest accrued with savings accounts and other investments.

As a credit union member, you typically end up with lower interest rates and fees (a major plus). On the flip side, major banks typically have more branch locations where customers can do business and invest more in apps and convenience services. So, you could say that which is the best is a matter of preference.

But, I have a tie-breaker: credit unions have less stringent and often flexible qualification terms for credit. You can’t walk into a bank like Wells Fargo and negotiate the terms of business banking fees, loans, or credit cards. At a credit union, more than not, you can because credit union underwriters usually work in-house and can modify terms and conditions of business and individual financial services.

So, I say that credit unions are in-fact better than banks. Now, let’s move forward.

But, Are Credit Unions Better for Business Accounts?

Aside from the general advantages above, there is another aspect of business banking with credit unions worth considering. When you bank with a credit union, you can leverage the perks above when obtaining business credit. For this reason, we prefer to work with credit unions. Alternatively, small community banks can be better for businesses than large banks.

How to Leverage Business Credit to Transform Your Life

Now, the Best Credit Unions for Small Business

You should have a solid understanding of why or why not a credit union might be best for your small business banking. And, here are the top credit unions to join.

1. Navy Federal Credit Union

With tons of free ATMs sprinkled throughout the United States and several other countries, Navy Federal Credit Union was created for members of the armed forces, DoD, or the National Guard. While you don’t necessarily have to be an active member to join, you must have ties to the military. So, if you are an active member, veteran, or a spouse, parent, grandparent, sibling, child, or grandchild of someone who qualifies, you can qualify for membership.

If you are not a service member, you will have to apply in-person at a branch location. Once you are approved for a personal account, you can then apply for a business membership. And, Navy Federal has excellent offers for businesses.

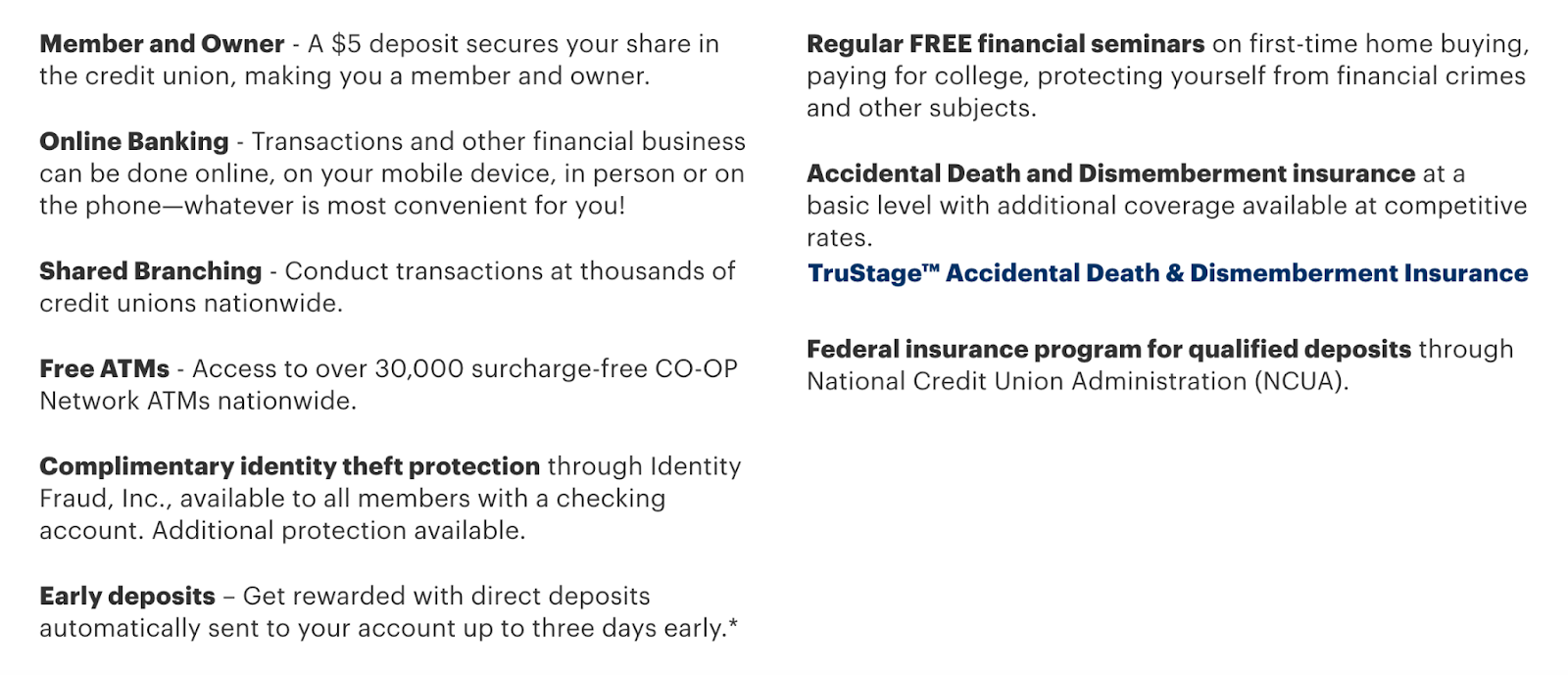

- 3 types of checking accounts (Basic, Plus, & Premium)

- 3 types of savings accounts (Basic and Jumbo Money Market & Certificate)

- Real estate, vehicle, and term loans

- Business lines of credit

Navy Federal is one of the best credit unions with the lowest rates and fees. Minimum deposits for business savings accounts start as low as $100. And, transaction fees range from $0 to $0.25. And, all accounts earn dividends.

2. Financial Resources Credit Union

With 13 branch locations in New Jersey and New York, Financial Resources Credit Union has been the top SBA Lender in New Jersey since 2013. So, you know their business financial services are dependable.

Here’s what you can leverage with Financial Resources Credit Union:

- 2 types of checking accounts

- 3 types of savings accounts (Business Purple, Money Market, & Certificates)

- Real estate, equipment, and term loans

- Lines of credit

So, whether you’re investing in real estate or you simply want checking and savings accounts to process your business finances, Financial Resources gives you options. Here, terms are flexible and you can get expedited approval on SBA-backed loans because the institution is a preferred lender.

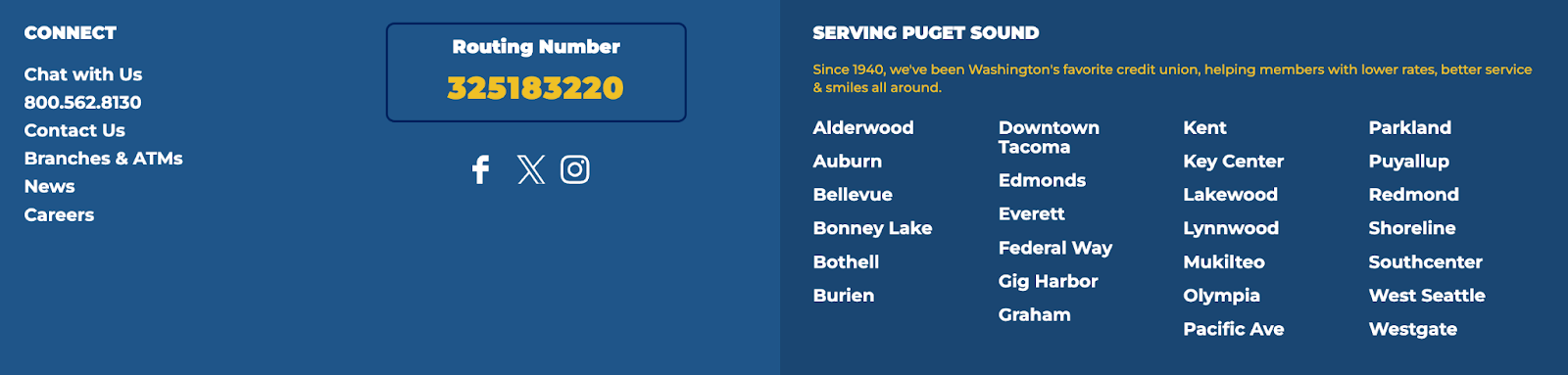

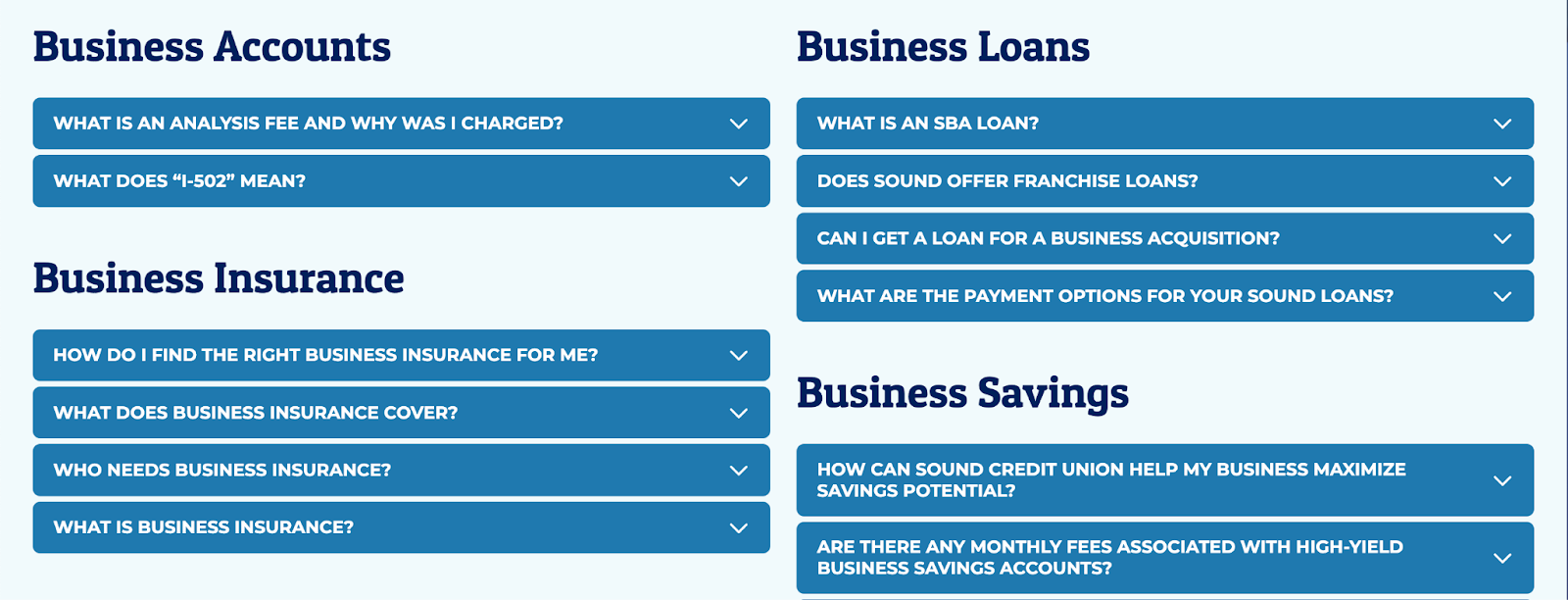

3. Sound Credit Union

With 29 locations in the Puget Sound area of Washington State, Sound Credit Union is self-labeled “Washington’s Favorite Credit Union.” And, they stand out from most financial institutions in more than one way.

For one, they cater to cannabis businesses, which isn’t common. Next, they offer low interest rates, cashback options on certain loans, and they do a lot to support the local community. Furthermore, they have over 5,000 shared branch locations and 30K+ free ATMs nationwide.

And, businesses can take advantage of the following:

- Checking accounts

- Savings and certificate accounts

- Cannabis (I-502 Analysis) business checking accounts

- Business loans

- Business credit cards

In addition, with Sound CU, you can access a full suite of business services that includes terminals and point of sale systems, eCommerce payment solutions, mobile card readers, payment acceptance, gift card, reward, and incentive programs, and mobile apps and software. The institution’s tech is as advanced as you can get with most major banks.

+Honorable Mentions

Obviously, these three credit unions are only a small drop in the ocean of options. So, in case you aren’t able to select one of these three, I want to share four more credit unions that you can research yourself:

- Alliant Credit Union – 2 branch locations in Illinois and 80K+ free ATMs

- Consumer Credit Union – 8 branch locations in Tennessee

- America First Credit Union – Located in Ogden, Utah

- Digital Federal Credit Union – 23 branch locations in Massachusets and New Hampshire, 5.9K shared branches, and 80K+ free ATMs

Why choose a credit union instead of a bank?

Compared to a major bank, a credit union or small local community bank is likely to offer lower fees, increased savings, and more lenient qualification terms for lending.

What are the disadvantages of credit unions?

Typically, credit unions run operations from their own funds, so they might offer less in the way of mobile apps, online banking features, and other conveniences. But, they still have many valuable perks.

Are credit unions good for small business?

Credit unions can be beneficial for your small business. They offer lower fees and interest rates, personalized service, a local focus, easier access to credit, and the opportunity for relationship building. Research and compare different credit unions to find the one that suits your specific business needs.

Which bank is best for small businesses?

A small local community bank or credit union can be the best choice for small business banking. Fees are typically lower than those at major banks and lending qualification terms have more wiggle room. These institutions tend to have more control over their terms and conditions.

How do I choose a bank for my company?

First, create a list of local small community banks and credit unions in your area. Then, call each institution on your list and ask about business checking and savings options as well as underwriting terms for business loans and lines of credit. Finally, choose the option that is the best fit for your operations and goals.

Final Thoughts

The above-listed credit unions offer the best financial services for businesses. If you want your operations to run smoothly, you can’t go wrong with one of these choices. But, do your homework to make sure you choose the best institution to fit your needs.

To find out which banks and credit unions we’re currently working with to obtain lines of credit up to $100K in as few as 30 days, join Business Credit Workshop today.