As an entrepreneur, managing your finances is crucial. And guess what? A business credit card can be a game-changer. In this article, we explore the world of credit cards designed specifically for entrepreneurs. We’ll reveal the leading contenders, highlight their impressive features, and address the burning questions you have about credit cards for contractors, independent contractors, and self-employed individuals.

But first, let’s give you a sneak peek of the cards—because that’s what you’re here for!

Presenting the most practical (and rewarding) business credit cards for entrepreneurs:

| Chase Ink Business Preferred Generous rewards program and travel benefits → Learn more |

| BoA Mastercard Business Platinum Comprehensive travel insurance coverage → Learn more |

| American Express Business Gold Flexible rewards and bonus categories for common expenses → Learn more |

| Capital One Spark 2% Business Cash Unlimited 2% cash back on all purchases → Learn more |

| CitiBusiness/AAdvantage Platinum Select Travel benefits and rewards for American Airlines → Learn more |

| Divvy Corporate Card Simplified expense management and budget controls → Learn more |

These credit cards from major banks are quite popular, but here’s a little secret: If you have a solid relationship with a small community bank or credit union, you might be able to secure even higher credit limits. In fact, we specialize in teaching entrepreneurs like you how to build those relationships and access credit lines worth hundreds of thousands of dollars at Business Credit Workshop. So, don’t overlook the potential benefits of working with local financial institutions!

Now, let’s take a closer look at each of the cards mentioned above and uncover valuable information and advice to help you maximize your business credit profile. Get ready to elevate your financial strategy and unlock new opportunities for your business!

Here’s what’s in store:

- Explore the Best Credit Cards for Entrepreneurs

- How to Build Credit for a New LLC or Business with No Credit History

- Frequently Asked Questions

- Final Takeaway

Now, let’s get crackin’!

Explore the Best Credit Cards for Entrepreneurs

| Chase Ink Business Preferred | Competitive APR, employee cards, Mastercard Easy Saving® Program | Cash flow management tools, online & mobile access, travel and emergency services, free access to business credit scores |

| BoA Platinum Plus® Business Mastercard® | Competitive APR, employee cards | Cash flow management tools, online & mobile access, travel and emergency services, free access to business credit scores |

| Amex Business Gold | 4X points on top 2 business categories, 1X points on other purchases | Cash flow flexibility, expense management tools, travel benefits, additional services |

| Spark 2% Cash Plus Business | Unlimited 2% cash back on every purchase, 5% cash back on hotels and rental cars booked through Capital One Travel | Flexible underwriting, cards for every employee, seamless software integration |

| AAdvantage Platinum Select | Travel benefits, mileage benefits, additional benefits | First checked bag free, preferred boarding, savings on inflight purchases |

| Divvy Corporate Card | Flexible rewards program | Control over rewards earnings, effortless management, various redemption options |

When it comes to choosing the perfect credit card for your small entrepreneurial venture, it’s smart to consider some of the major cards specifically tailored to meet the needs of small business owners like yourself. Before we delve into the world of business credit and its intricacies, let’s take a closer look at the unique features and benefits offered by each of these top credit cards.

Recommended: What’s the Best Credit Card for a Small Construction Business? +TIPS

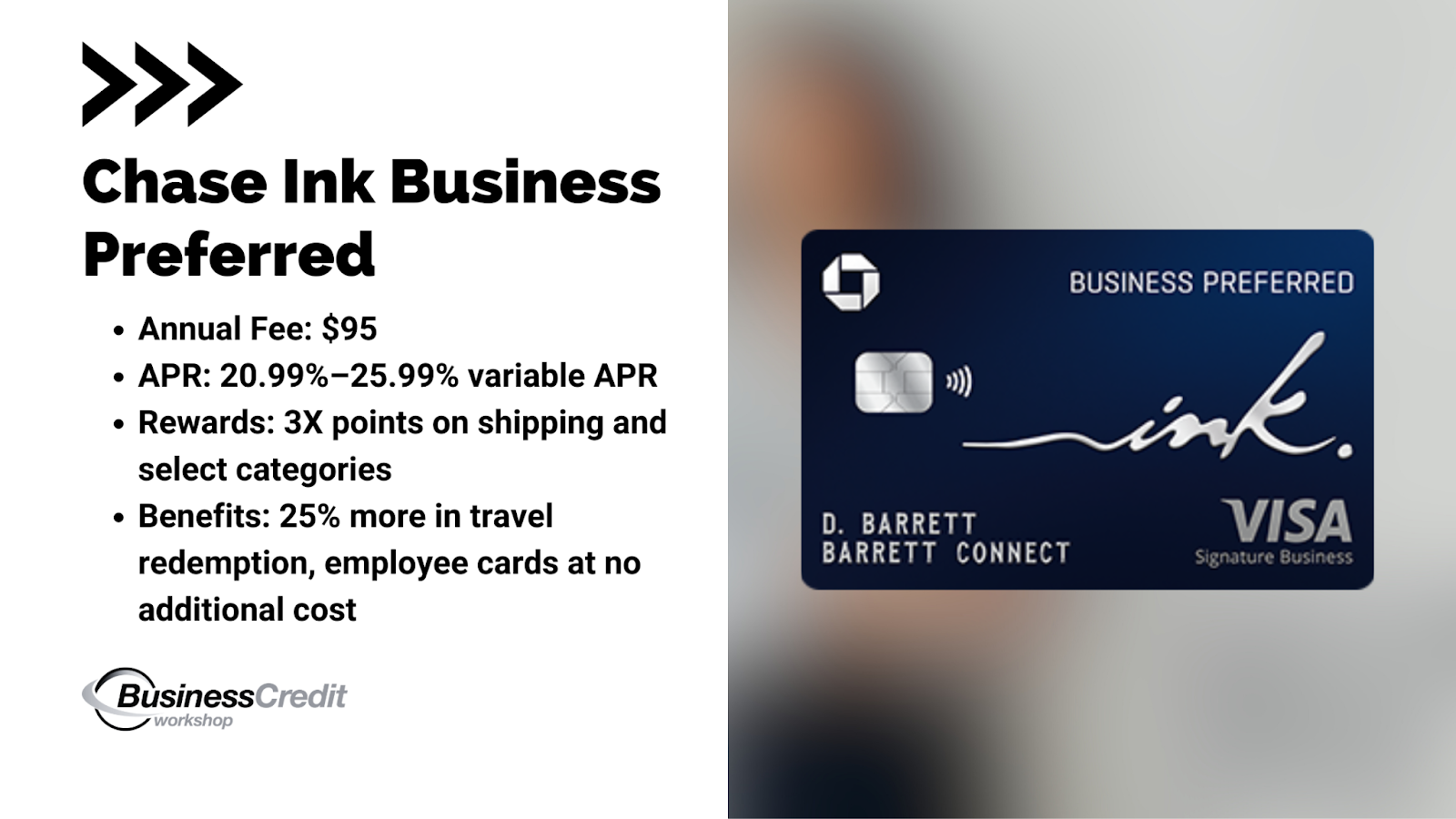

1. Chase Ink Business Preferred

Credit Card: Ink Business Preferred® Credit Card

Issuer: Chase

APR: 20.99%–25.99% variable APR

Annual Fee: $95

Rewards Program:

- Earn 3X points on shipping and other select business categories

- Earn unlimited 1 point per $1 spent on all other purchases. Points do not expire as long as the account is open

- Redeem points for cash back, gift cards, travel experiences, and more through Chase Ultimate Rewards

- Get 25% more value when redeeming points for travel through Chase Ultimate Rewards

- Earn 5X points on Lyft rides through March 2025

Benefits:

- Employee cards at no additional cost, with individual spending limits

- No foreign transaction fees

- 1:1 point transfer

- Travel and purchase coverage

- Stay on top of your business with expense tracking tools

- Referral program: Earn up to 200,000 points per year by referring other business owners to any Chase Ink® Credit Card

The Ink Business Preferred® Credit Card from Chase is a top choice for entrepreneurs looking for flexible and rich rewards. With a generous sign-up bonus, accelerated points earning in select business categories, and various redemption options, it provides value for business expenses. The card also offers additional benefits like no foreign transaction fees, point transfers, and purchase coverage. Positive customer reviews highlight its effectiveness for earning rewards and the overall satisfaction of cardholders.

Recommended: Chase Ink Business Preferred Credit Card: A Deep Dive Analysis

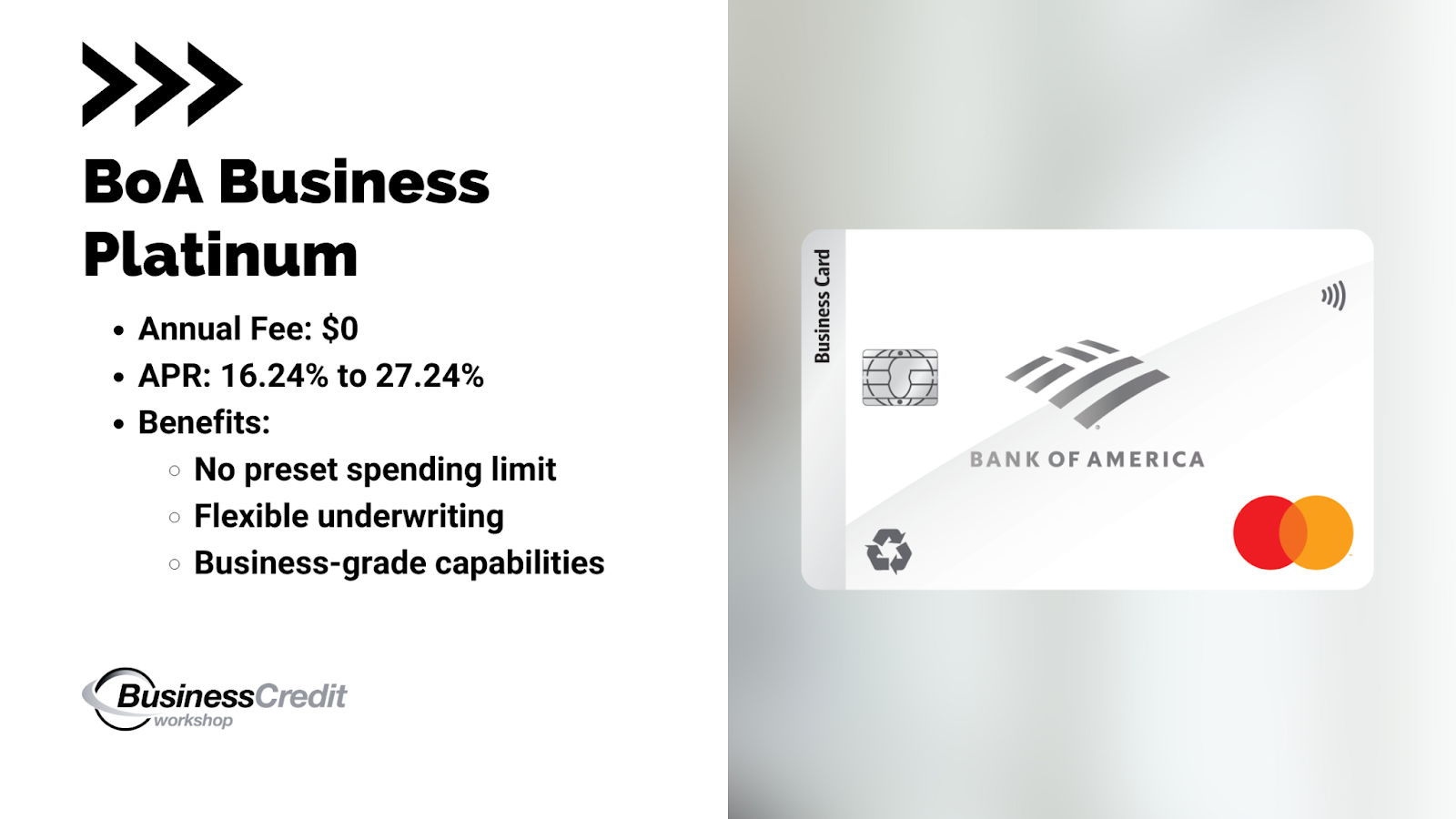

2. BoA Mastercard Business Platinum

Credit Card: Platinum Plus® Mastercard® Business card

Issuer: Bank of America

APR: 0% introductory APR for the first 7 billing cycles, then a variable APR of 16.24% to 27.24%

Annual Fee: $0

Benefits:

- Employee cards at no additional cost: Get employee cards with credit limits set by you

- Mastercard Easy Saving® Program: Automatic rebates when using the card at tens of thousands of locations across the U.S.

- Cash flow management tools: Suite of online services for managing your business finances

- Online and mobile access: Secure access to manage your account online 24/7

- Travel and emergency services: Includes travel accident insurance, auto rental insurance, emergency ticket replacement, lost-luggage assistance, and more

- Free access to business credit scores: View Dun & Bradstreet business credit scores within Business Advantage 360, Bank of America’s Small Business Online Banking platform

- Security features: Zero liability protection, fraud monitoring, paperless statement option, and more

- Balance Connect® for overdraft protection: Link your credit card to a Bank of America business checking account for overdraft protection

The Platinum Plus® Mastercard® Business card from Bank of America offers competitive features, including a 0% introductory APR, no annual fee, and a $300 online statement credit offer. It also provides benefits such as employee cards, access to the Mastercard Easy Saving® Program, cash flow management tools, travel and emergency services, free access to business credit scores, and various security features. This card can be a suitable choice for businesses looking for a straightforward credit card option with cost-saving benefits.

Recommended: Bank of America Corporate Cards: A Complete, Uncut Review

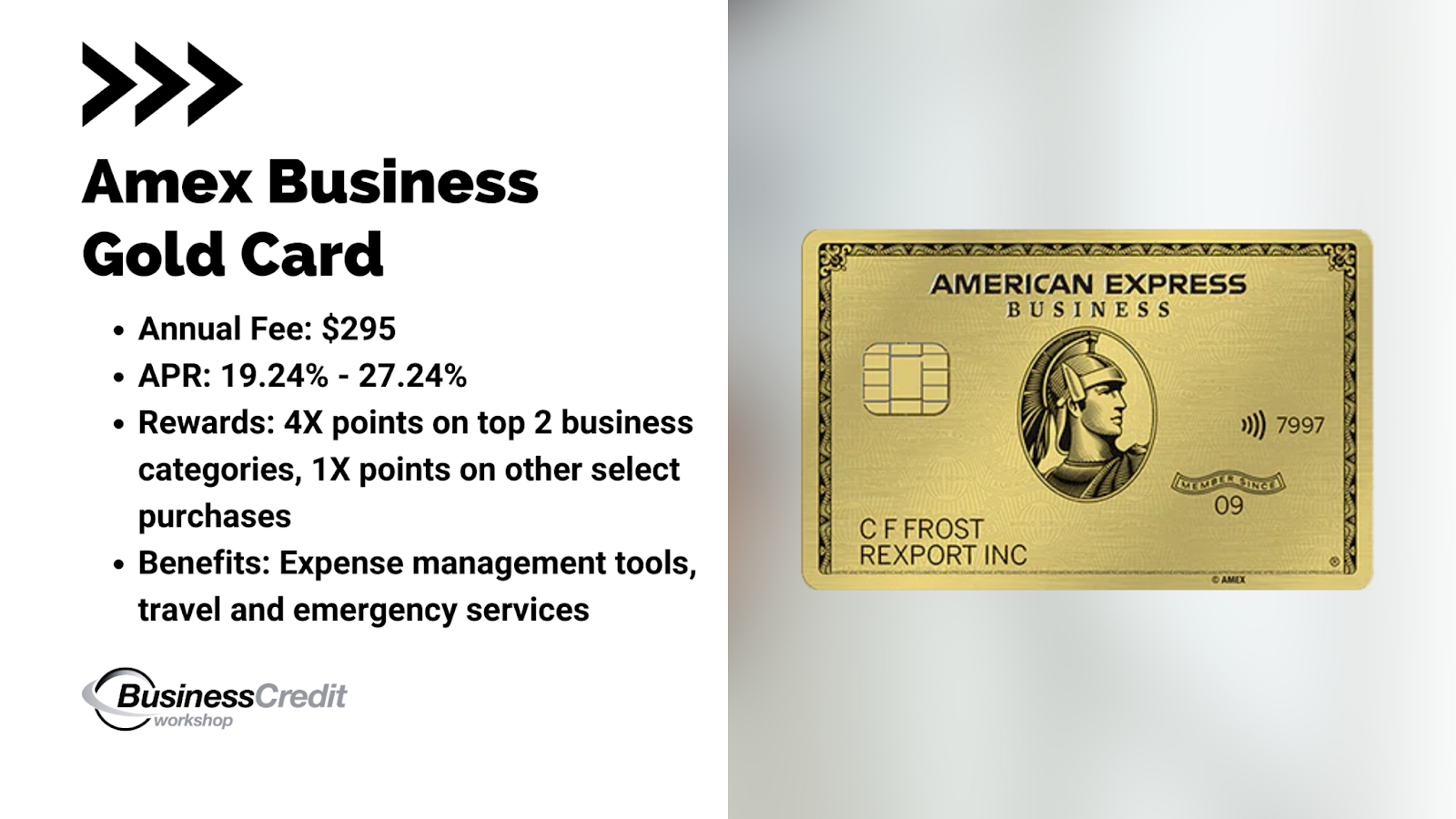

3. Amex Business Gold

Credit Card: Amex Business Gold Card

Issuer: American Express

Annual Fee: $295

Rewards:

- Earn 4X Membership Rewards points on the top 2 business categories where your business spends the most each billing cycle.

- Airfare purchased directly from airlines

- U.S. purchases for advertising in select media

- U.S. purchases made directly from select technology providers

- U.S. purchases at gas stations

- U.S. purchases at restaurants (including takeout and delivery)

- U.S. purchases for shipping

- Earn 1X points on other select purchases made using the Business Gold Card.

Benefits:

- Pay Over Time APR: APR on purchases will be a variable rate of 19.24% – 27.24%, based on creditworthiness and other factors at the time of account opening

- Acceptance: American Express can be used at 99% of places in the US that accept credit cards

- Expense management tools for better cash flow management

- Travel benefits and additional services

The American Express Business Gold Card offers a competitive rewards program with the opportunity to earn 4X Membership Rewards points on the top 2 business spending categories each billing cycle. It also provides 1X points on other select purchases. With a special welcome offer of 100,000 Membership Rewards Points and various expense management tools, this card aims to provide flexibility and benefits for business owners. The card has a variable APR for purchases and is widely accepted across the US.

Recommended: Amex Business Checking Review: What You Need to Know…Really

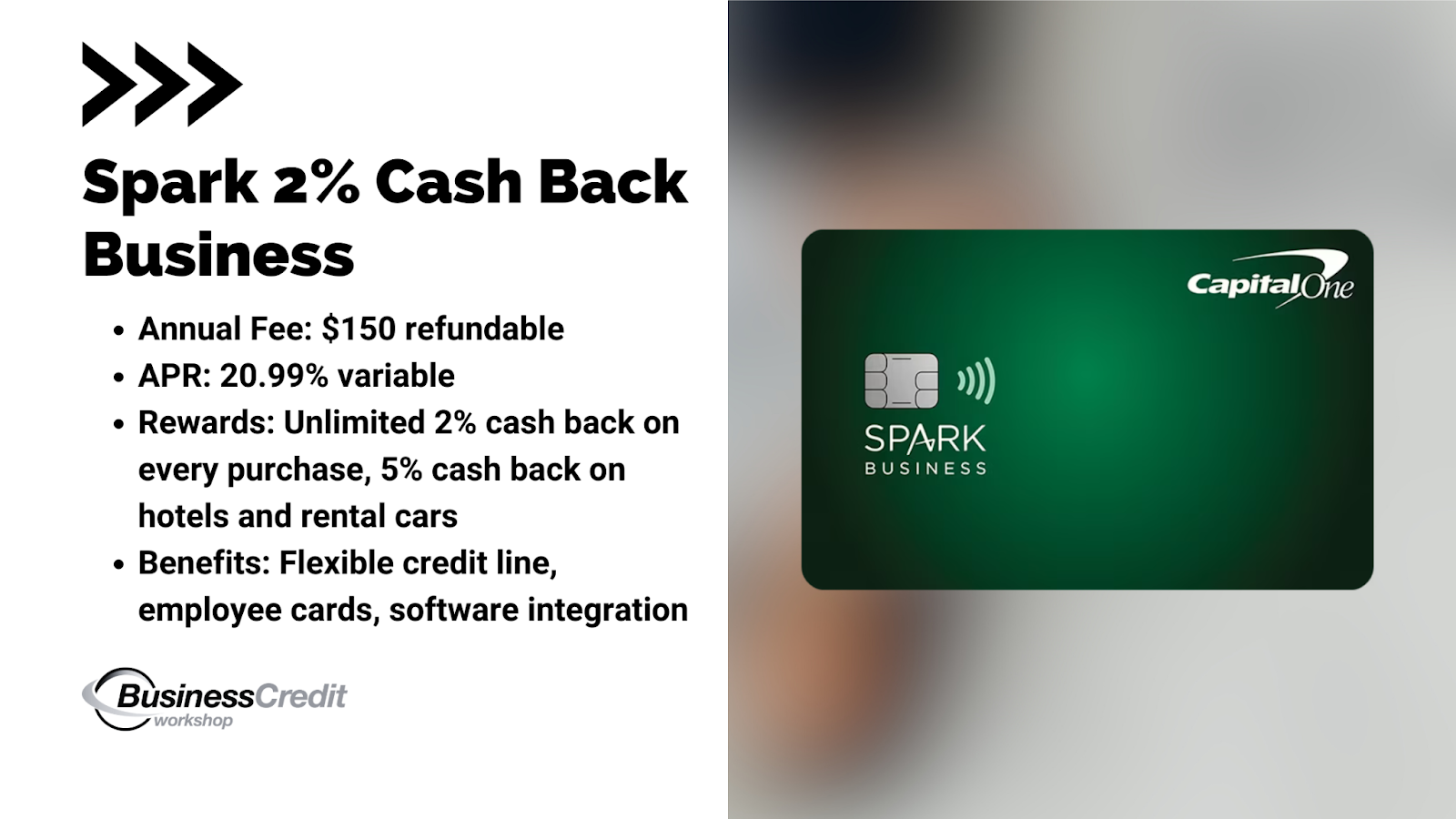

4. Capital One Spark 2% Cash for Business

Credit Card: Spark 2% Cash Plus

Issuer: Capital One

Annual Fee: $0

Rewards Program:

- Unlimited 2% cash back on every purchase, everywhere, with no limits or category restrictions

- Earn unlimited 5% cash back on hotels and rental cars booked through Capital One Travel

Benefits:

- Pay-in-Full Charge Card: The balance must always be paid off in full every month

- No Preset Spend Limit: Adapts to your needs based on spending behavior, payment history, and credit profile

- Annual Fee Refund: Get your $150 annual fee refunded every year you spend at least $150,000

- Business-Grade Capabilities: Empower your team with free employee and virtual cards, and easily pay vendors

- Additional benefits include account management tools, employee access, travel benefits, service and protection features such as automatic payments, $0 fraud liability, year-end summaries, account managers, purchase records, and virtual card numbers

The Spark 2% Cash Plus card from Capital One offers excellent cash back rewards with unlimited 2% cash back on all purchases and 5% cash back on select travel bookings. With a one-time cash bonus of $1,200 and the option to earn an annual fee refund, this card provides significant value for business owners. It also includes various business-grade capabilities, such as employee cards, vendor payments, and a range of benefits and features to manage accounts and protect against fraud.

Recommended: What are the Best Unsecured Business Credit Cards for Startups?

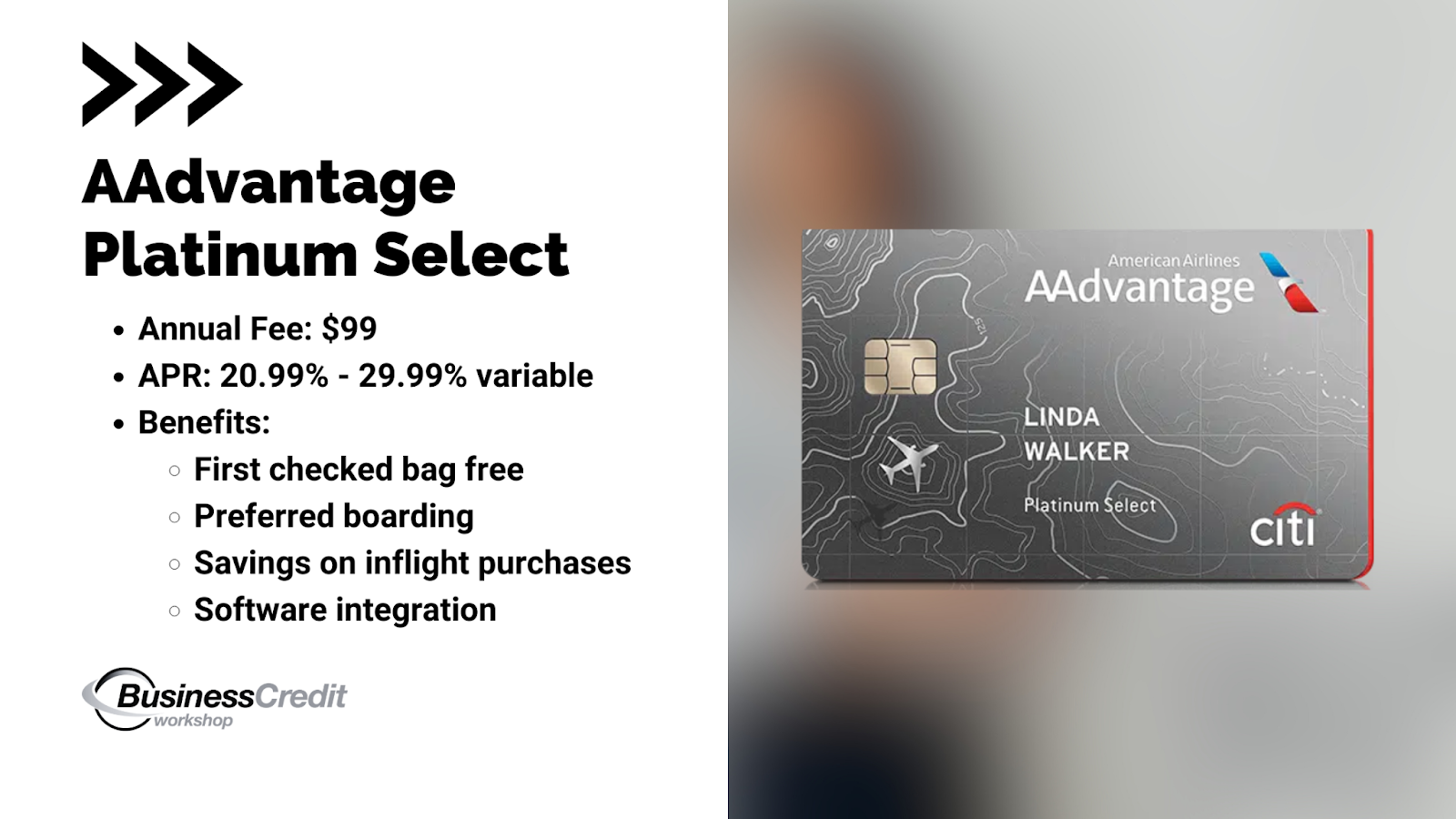

5. AAdvantage Platinum Select

Credit Card: AAdvantage® Platinum Select® World Elite Mastercard®

Issuer: Citibank

Annual Fee: $0 intro annual fee for the first year, then $99

Rewards:

- AAdvantage® Miles: Earn miles from purchases

- Loyalty Points: Earn 1 Loyalty Point for every 1 eligible mile earned from purchases

Benefits:

- First checked bag free on domestic American Airlines itineraries for you and up to 4 travel companions on the same reservation (savings of up to $300 per round trip)

- Preferred boarding on American Airlines flights

- 25% savings on inflight food and beverage purchases on American Airlines flights when you use your card

- Variable APR for purchases and balance transfers: 20.99% – 29.99% based on creditworthiness.

- No foreign transaction fees

The Citi® AAdvantage® Platinum Select® World Elite Mastercard® offers travel benefits, including a free checked bag, preferred boarding, and savings on inflight purchases. You can earn AAdvantage® miles and loyalty points for eligible purchases. The card has a variable APR for purchases and balance transfers, and there are no foreign transaction fees. The annual fee is $0 for the first year, then $99*.

Recommended: Should You Open a Citibank Commercial Card Account?… It Depends!

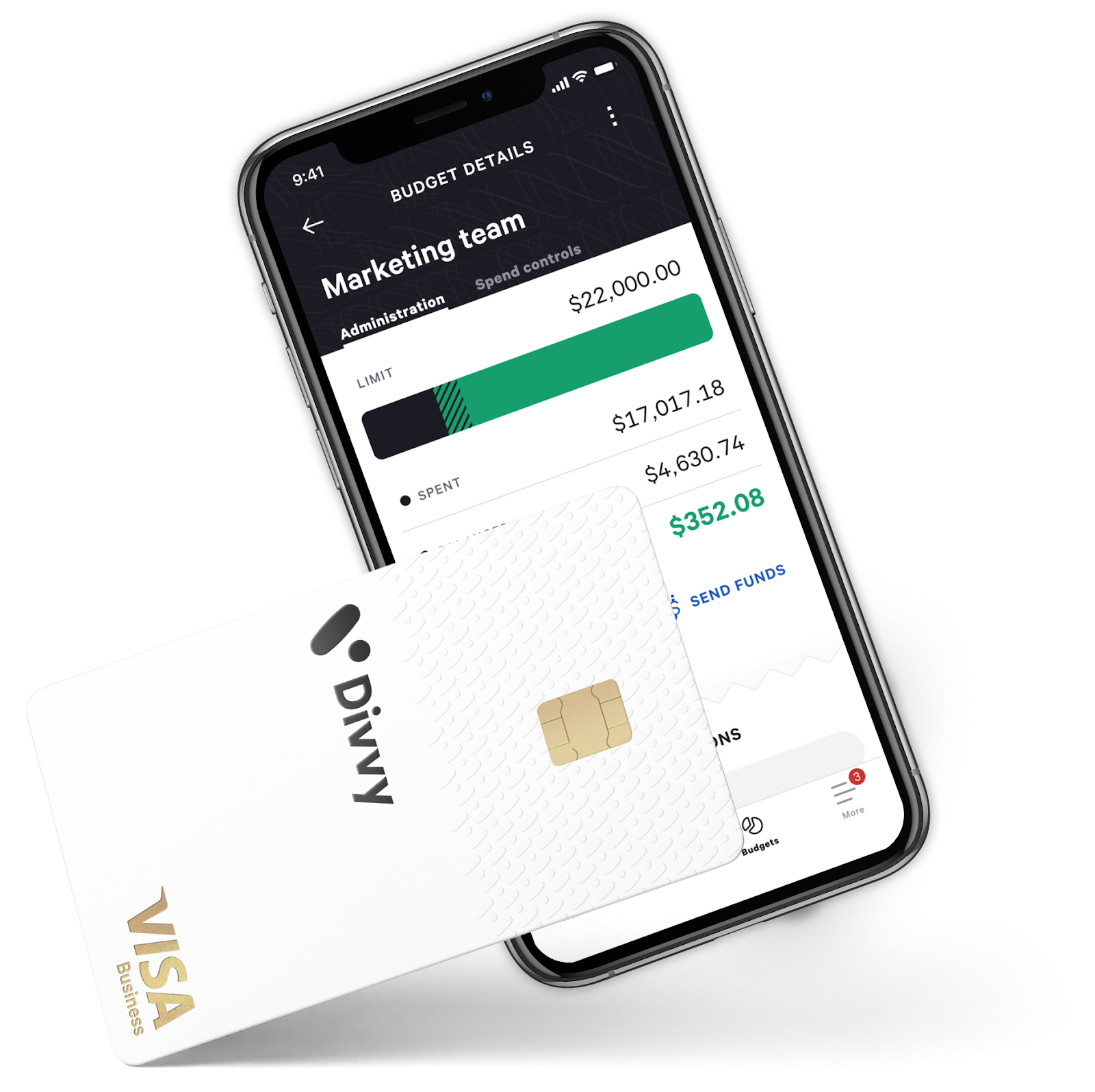

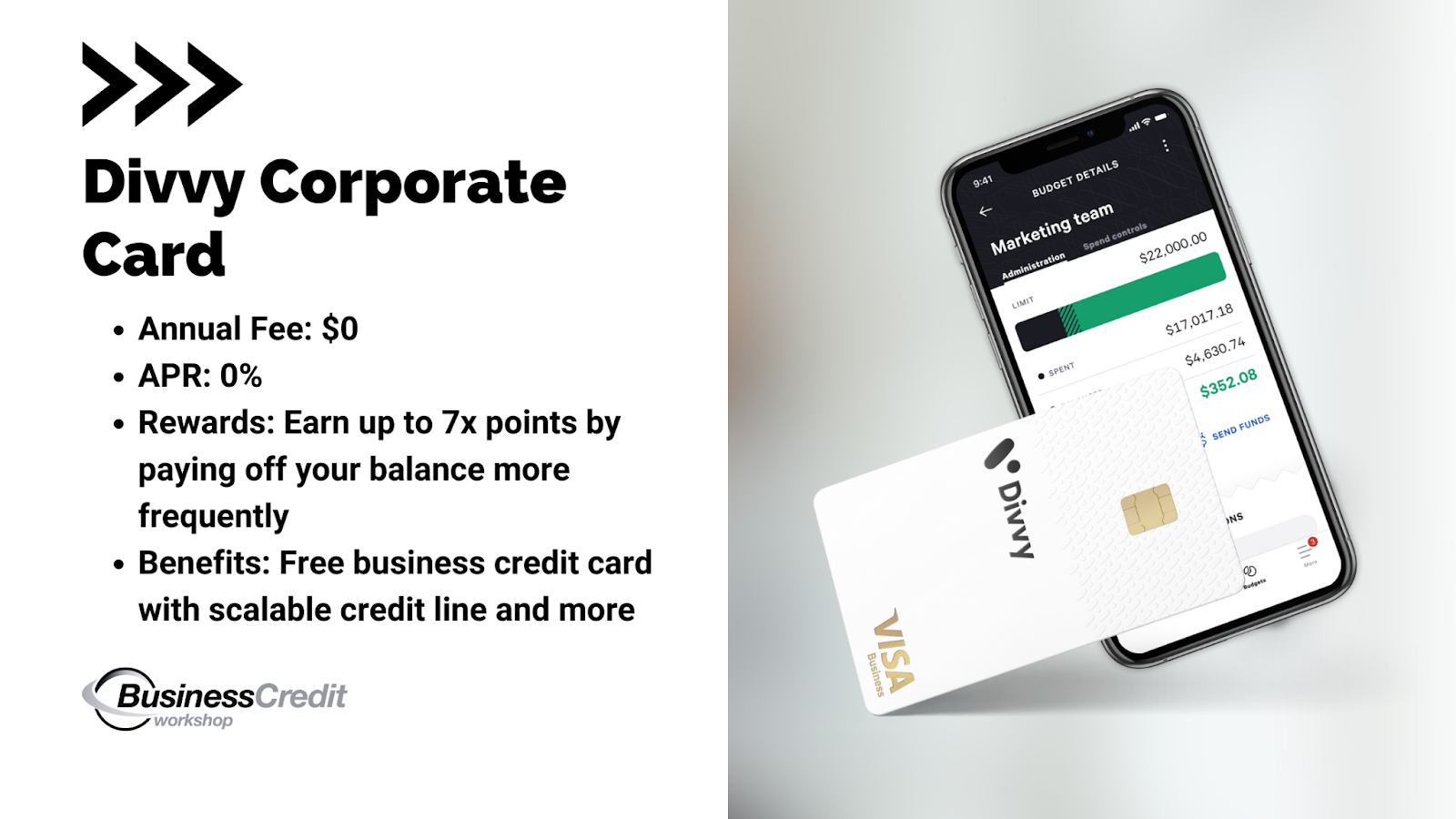

6. Divvy Corporate Card

Credit Card: Divvy Corporate Card

Issuer: Divvy

Annual Fee: $0

Rewards:

- Earn up to 7x points by paying off your balance more frequently

- Weekly: 7x points on restaurants

- Semi-Monthly: 5x points on hotels

- Monthly: 2x points on recurring software subscriptions

- 1.5x points on everything else

- Unlimited Earnings: Earn rewards points daily with no cap and no expiration.

- Effortless management: Track and redeem points easily through the rewards dashboard.

- Boost your ad spend: Earn up to 2.25% cash back on advertising spend through Divvy, with no limit on earnings.

- Flexible rewards redemption options: Cash back, gift cards, statement credit, and Divvy Travel partnership for double the point value and industry-leading rates.

Benefits:

- Free, fast, and flexible business credit with credit lines up to $15M

- Credit line scales with your business, with the ability to apply for credit line increases

- Flexible underwriting options based on your business’s unique needs

- Cards for every employee with proactive spend controls

- Seamless software integration with desktop software and highly-rated mobile app

- Advanced fraud protection for secure transactions

The Divvy Corporate Card is a free business credit card that offers fast and flexible funding options for businesses of all sizes. With its simple online application process, businesses can access credit lines up to $15M. The card scales with your business and offers flexible underwriting options to fit your needs. Divvy provides cards for every employee, seamless software integration, and advanced fraud protection. Additionally, businesses can earn rewards based on payment frequency. The Divvy Corporate Card is a valuable tool for managing business expenses and streamlining financial operations.

Recommended: In-Depth Divvy Credit Card Review: Read This Before You Apply

How to Build Credit for a New LLC or Business with No Credit History

If you’re eager to build your business credit fast, I’ve got some great insights for you! Building solid business credit can open up funding options beyond your personal credit limits and even help you secure lower insurance rates.

But before we dive in, let’s address some commonly asked questions about business credit. Can you use your EIN (Employer Identification Number) to apply for credit? Absolutely!

As long as you have an EIN assigned by the IRS, you can use it for business credit applications. Getting a business credit card isn’t as hard as you might think. With a high business credit score, you’ll have no trouble securing one. While some business credit cards may do a soft or hard pull on your personal credit, there are others that don’t.

And yes, an LLC can have a credit score! With an EIN and a DUNS number from Dun & Bradstreet, your LLC can have a credit score separate from your personal credit score.

Now, let’s jump into the steps to build business credit quickly. Remember, just like with personal credit, paying your debts on time is crucial for maintaining a good score.

Here’s a breakdown of the steps:

- Form your business — Just like laying a strong foundation for a building, you need to properly form your business. Choose a neutral business name that allows for flexibility in funding options. Once you settle on a name, try to stick with it to show stability. Decide how you want to establish your business entity, whether it’s through an attorney, an online service, or manually with your local Secretary of State

- Get your company “business credit ready” — Think of this step as adding a rough frame to your business. Establish a physical address (avoid using P.O. boxes), get the necessary business insurance if required, obtain any required business licenses, and create a strong online presence with a website and domain. Listing your business in relevant directories adds credibility and trustworthiness.

- Network with local banks — Networking is vital, whether in buildings or business credit. Attend local Chamber of Commerce events if possible, or network online with local professionals to build connections. Research local banks and credit unions to understand their financing programs and underwriting processes.

- Setup business credit profiles — This step involves setting up insulation for your business. Establish a business credit profile with Dun & Bradstreet (D&B) to obtain your PAYDEX score, which is a crucial business credit score. Monitor your Equifax and Experian business credit scores for free, fixing any inaccuracies you come across. Utilize business credit monitoring services like Nav to stay on top of your credit profile.

- Build small trade lines of credit — Here’s where we add the finishing touches to make your building habitable. Establish small tradelines of credit, which are credit accounts with vendors or suppliers. These tradelines play a significant role in solidifying your business credit. Secure credit with suppliers and make timely payments to build trust and a positive credit history.

By following these steps, you can accelerate the process of building your business credit. We teach the full, 7-step process to build business credit in Business Credit Workshop.

Now, find out what you can do if your credit needs some work.

What if You Have Bad Credit?

If you’re wondering if personal credit affects business, it does. So, before you apply for large lines of business credit, it’s important that you clean up your personal credit score.

Here’s my best advice to clean up bad personal credit.

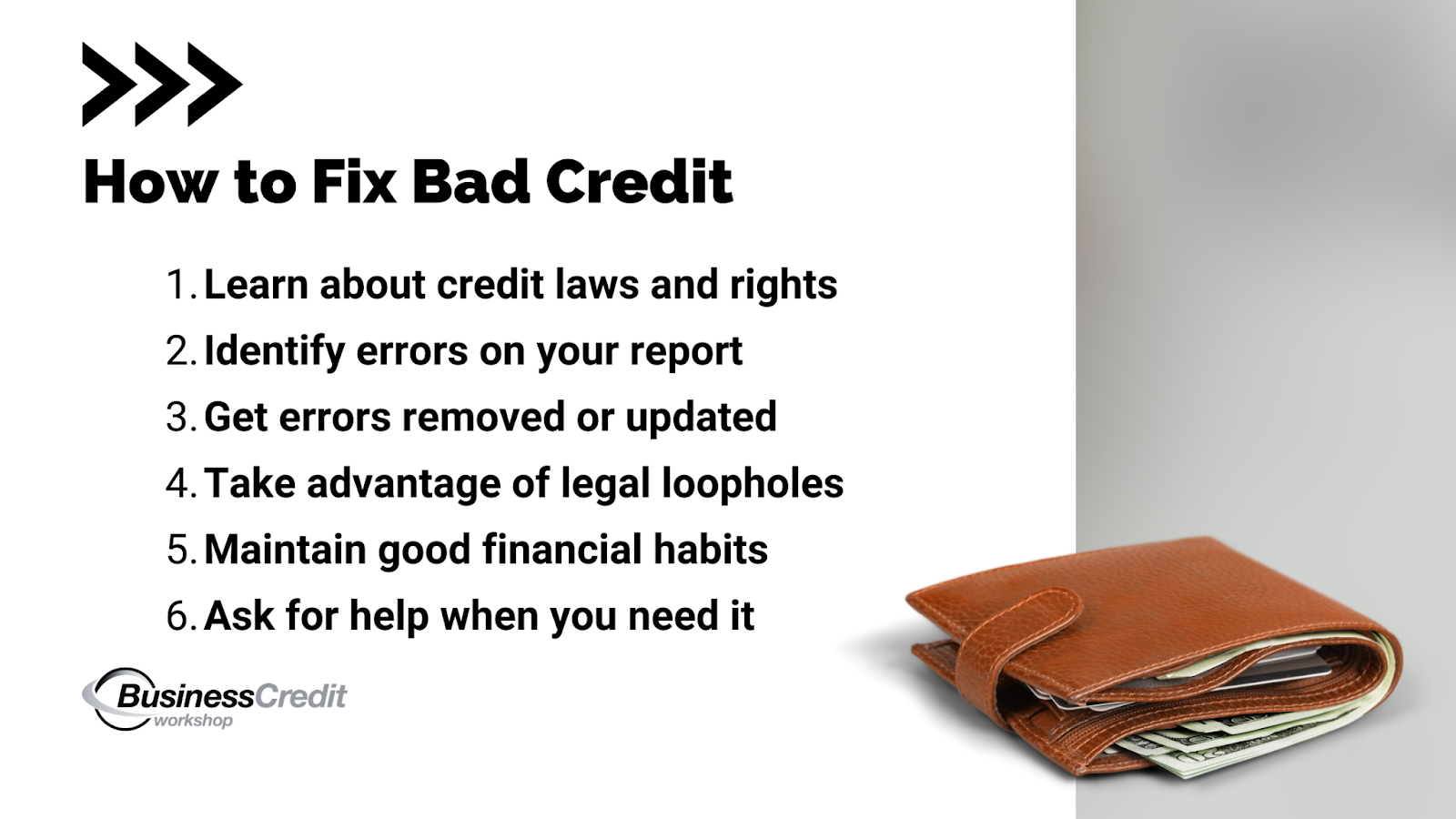

- First, educate yourself. Gain knowledge about credit repair strategies and consumer protection laws that can work in your favor. Understanding the credit reporting system will help you navigate the process more effectively.

- Next, identify errors. Carefully review your credit reports for any inaccuracies, incomplete information, or unfair items. These errors are common and can have a negative impact on your credit score. Disputing and resolving these issues is crucial.

- And, take action! — This is key and may include sending dispute letters to creditors and credit bureaus, requesting the removal or update of erroneous information. Follow step-by-step tutorials and utilize letter templates provided in credit repair resources.

- Furthermore, take advantage of legal loopholes. Learn about the consumer protection laws that safeguard your rights. This knowledge can empower you to file small claims lawsuits against creditors, credit bureaus, or collection agencies if they have violated these laws. Seek legal advice when necessary to understand the best course of action.

- Then, as you make changes, maintain good financial habits. Focus on making on-time payments, reducing debt, and managing your credit responsibly. Avoid common credit mistakes, such as late payments, high credit utilization, opening multiple accounts simultaneously, relying too heavily on one type of credit, and neglecting to review your credit report for inaccuracies.

- Finally, seek professional help if needed. While credit repair resources like books and online communities can provide valuable insights, it’s always wise to consult with professionals, such as credit counselors or attorneys, for specific legal advice or guidance tailored to your situation.

Remember, cleaning up your personal credit takes time and effort. Stay committed and patient as you work toward improving your financial health and credit scores.

Recommended: Credit Secrets Book Review: Can You Erase Bad Credit History?

What if Your Business Has Bad Credit?

So, let’s talk about fixing your not-so-great business credit in a way that’ll make you feel optimistic about the future. There could be a few reasons why your business credit isn’t where you’d like it to be. Maybe you had some hiccups in the past, like late payments, debts piling up, or even unfortunate situations like liens or bankruptcy.

But hey, don’t fret! You have the power to turn things around.

Now, when it comes to your credit score, one important thing to consider is the Paydex score from Dun & Bradstreet (the main business credit bureau). It’s like a report card that ranges from 0 to 100 — The higher your score, the better your creditworthiness. If your business credit isn’t so hot right now, your Paydex score might be on the lower side. But fear not, my friend, because there’s a way to fix it so that you don’t have to rely on those high-interest business credit cards for bad credit.

So, how do you get started on the road to credit recovery?

Let’s break it down in a way that’s easy to understand:

- Become a champion of timely payments — One of the biggest factors in improving your credit is paying your bills on time. It’s like scoring a winning goal in the game of credit. Make it a priority to pay your suppliers, vendors, and lenders right on schedule, or even earlier if you can. Timely payments are key to boosting your creditworthiness.

- Tackle those overdue accounts — If you have any lingering debts or accounts that are past due, it’s time to face them head-on. Develop a plan to pay off those outstanding balances as soon as possible. Don’t be afraid to negotiate payment arrangements or settlements with your creditors. You’ll feel a weight lifted off your shoulders once those accounts are squared away.

- Say bye-bye to high debt levels — Picture this: your debt levels dropping like confetti at a celebration. It’s a beautiful sight, isn’t it? High levels of debt can drag down your credit score, so it’s important to reduce those balances. Make consistent payments and resist the temptation to take on unnecessary new debt. Gradually, you’ll see that credit score start to rise.

- Build friendships with credit-worthy partners — Relationships matter in business and credit building is no exception. Seek out vendors and suppliers who are willing to report your stellar payment history to credit bureaus. It’s like having cheerleaders in your corner, rooting for your credit success. These positive credit relationships can work wonders in improving your creditworthiness. You might consider working with a credit broker (proceed with caution), but I am more inclined to recommend a business credit consultant or coach.

- Embrace the power of a fresh start — In some cases, if your current business has deep-rooted credit issues, starting anew might be the way to go. It’s like hitting the reset button and getting a chance to build a shiny new credit profile. Just remember, starting a new business comes with its own considerations, so consult with the experts to figure out the best approach for your situation.

Remember, improving your credit takes time and dedication. But don’t be discouraged! — With each positive step you take, you’re moving closer to a brighter credit future. So roll up those sleeves, put on your optimistic mindset, and let’s get to work on fixing that business credit of yours.

The future is looking mighty bright!

Recommended: This is How to Leverage Business Credit to Transform Your Life

Frequently Asked Questions

What is good credit for small business owners?

A Paydex score between 70-80 is a strong score that can be considered “creditworthy” by business lenders.

How can I get a 100 business credit score?

By having several positive reporting tradelines, you can get a perfect (100) Paydex score. But, this isn’t a common or believable score for a business to have.

How good does my credit need to be to get a business loan?

Nearly any business with income can get a business loan. Even with a low business credit score, most companies can qualify for merchant cash advances, factoring, and other alternative loans. The higher your credit score, the more likely you are to qualify for business loans with lower rates and more favorable features and rewards.

What credit score does a business start with?

The minimum credit score (Paydex) for a business is zero — Scores are calculated on a scale of 0-100. If you have no reporting tradelines, you will not have a credit score. You can use net 30 accounts and gas cards to establish your business credit score.

Final Takeaway

Business credit is a tool that can help you improve your cash flow to grow your company in invest in your future The cards listed here are some of the most popular business credit cards for entrepreneurs — Each has its own set of pros and cons.

- The Chase Ink Business Preferred offers a generous rewards program and travel benefits, making it an attractive choice.

- If comprehensive travel insurance coverage is a priority, the Mastercard Business Platinum is a great option to explore.

- For those seeking flexible rewards and bonus categories tailored to common expenses, the American Express Business Gold is worth considering.

- The Capital One Spark Cash for Business provides unlimited 2% cash back on all purchases, offering simplicity and value.

- If you’re a frequent flyer with American Airlines, the CitiBusiness/AA Advantage Platinum Select offers travel benefits and rewards specifically designed for American Airlines customers.

- Lastly, the Divvy Business Card streamlines expense management and budget controls, making it an efficient choice for businesses.

With these options in mind, you can choose the business credit card that aligns with your specific needs and preferences.

If you want to learn how to obtain up to $100K in business credit in as few as 30 days, join Business Credit Workshop today.