Key Takeaways

- Lending Club offers personal and business loans for various needs.

- The company was the first fintech to acquire a U.S. bank in 2020.

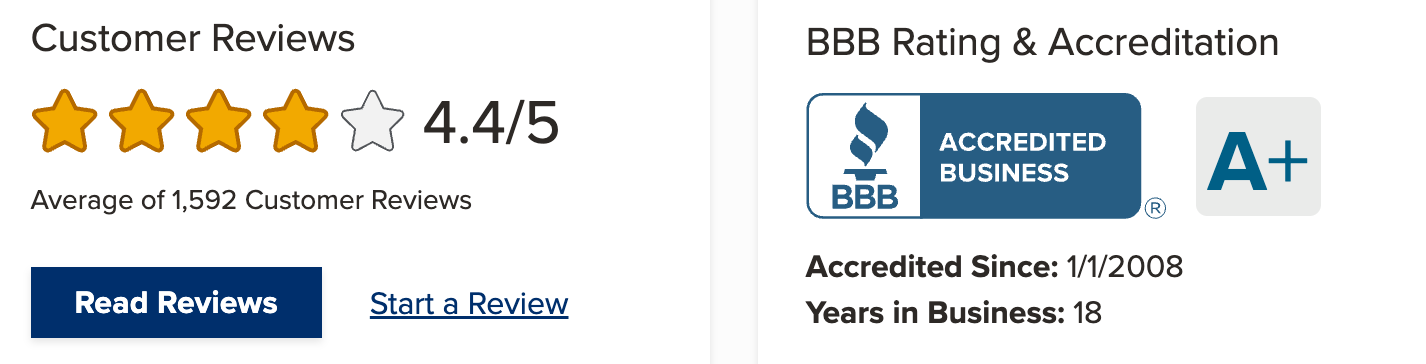

- They have an A+ BBB rating and a 4.6 TrustScore™ on Trustpilot.

- Their high-yield savings accounts provide up to 5.15% APY; business accounts earn 1.5% APY with 1% cash back.

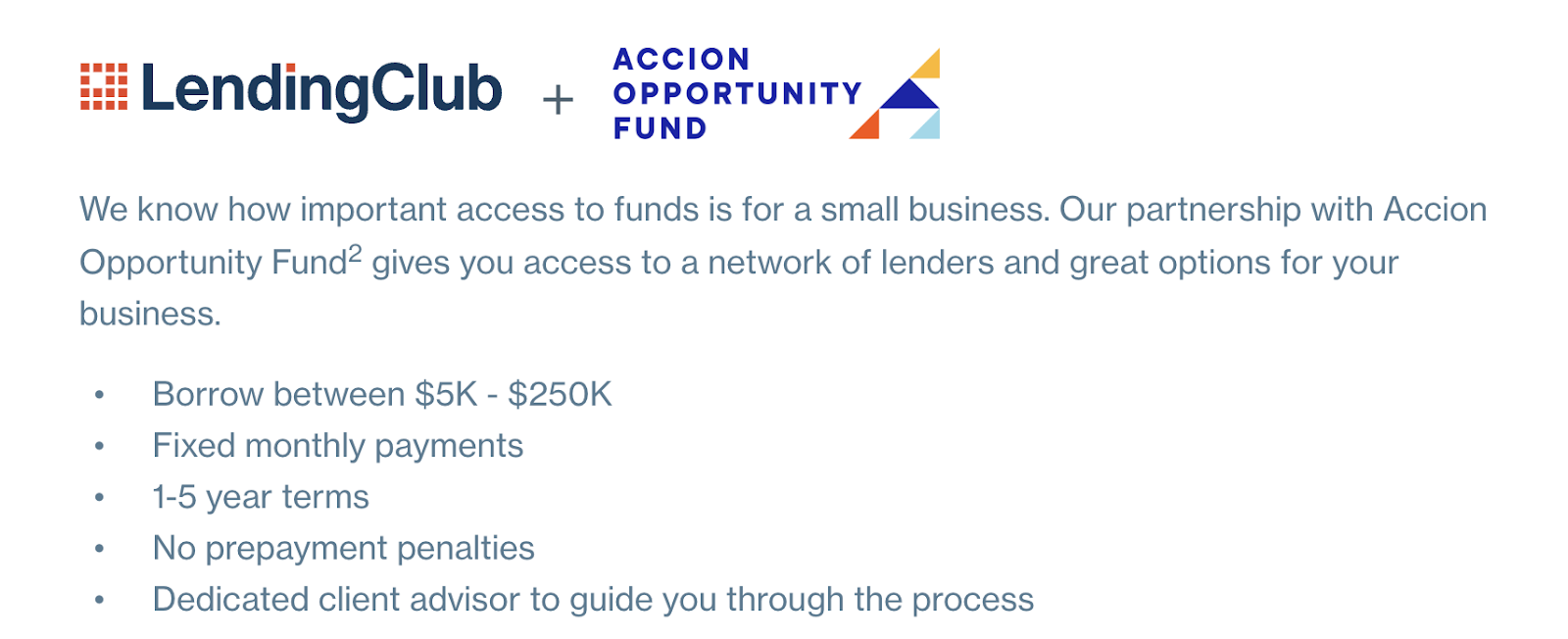

- Lending Clubs business loans are offered in partnership with Accion Opportunity Fund.

- The business loan application process is fast, with easy approval and direct deposits.

Since 2007, Lending Club has offered fair credit, unsecured, personal peer-to-peer (p2p) loans for debt consolidation and other major purchases. And they were the first fintech company to acquire a US regulated bank in 2020. Recently, they acquired a credit card debt payoff app, which aligns with the mission they’re on to become a financial health company, not just a lender.

Today, Lending Club offers personal and business borrowing, banking, investing, and financial resources. They’ve proven their ability to roll with the punches and their powerful offer is worth exploring. So, for every business owner wondering if you should work with the likes of Lending Club, here’s my honest opinion and complete overview.

This is what’s in store:

- What is Lending Club?

- Lending Club Business Loans

- How to Get a Small Business Loan with Lending Club

- Frequently Asked Questions

- Conclusion: Can Lending Club be Trusted?

Now, let’s go!

What is Lending Club?

LendingClub is a digital bank that offers a mix of personal and business loans, auto refinancing, and banking products. Known as a “marketplace bank,” it connects borrowers with investors to provide lending services while keeping costs low by operating fully online. LendingClub has issued more than $90 billion in loans to over 4.8 million members since it started in 2007.

LendingClub’s loan products include:

- Loans up to $40K to consolidate credit card debt or pay off personal loan balances.

- Personal loans of up to $40K for major purchases, home improvements, or life events.

- Loans up to $65K through the LendingClub Patient Solutions program for treatments like dental or fertility care.

- Options to refinance car loans with flexible terms and competitive rates.

- Small business loans up to $250K.

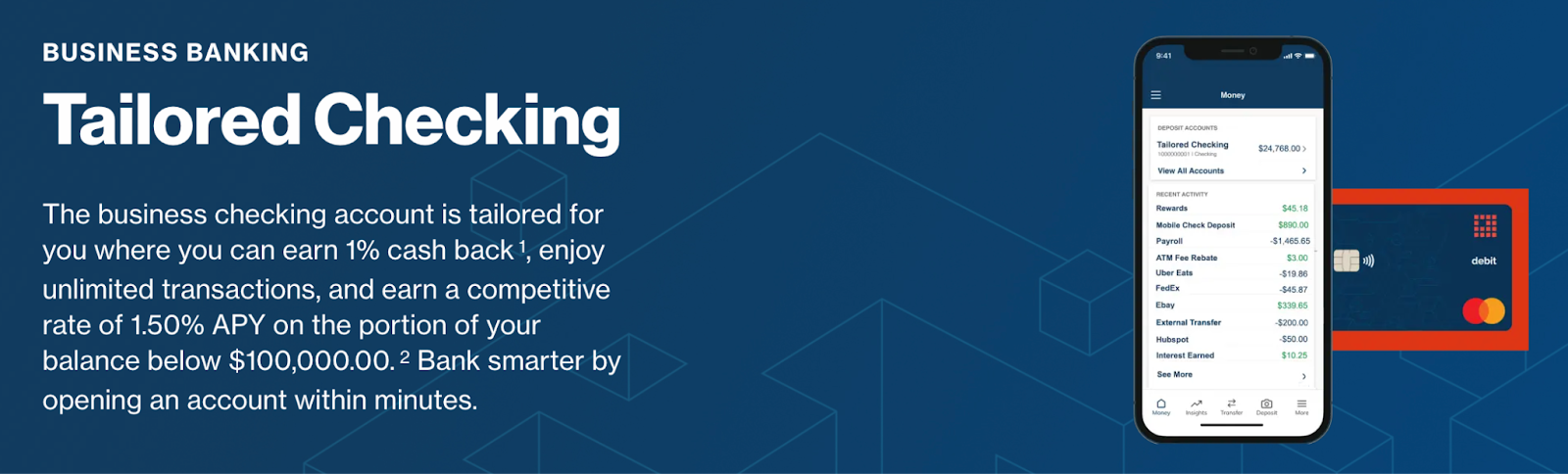

On top of loans, LendingClub offers banking products like Rewards Checking and High-Yield Savings Accounts with competitive interest rates and benefits like cash-back rewards. LendingClub’s high-yield CDs provide another savings option if you want to grow your savings steadily.

And, LendingClub positions itself as a bank that “only wins when customers succeed.”

You might also like: 11 Alternate Ways for Entrepreneurs to Raise Capital

What Bank Does Lending Club Use?

In February 2020, the LendingClub Inc. acquired and merged with Radius Bank, then re-launched under a self-branded title. This merger cut out the middle man, which was meant to lead to lower rates promised to bring high yields on new savings accounts.

At the time, I had doubts about how much difference this would actually make, since Radius Bank and Lending Club’s previous banking servicer (Webank) offered similar savings account yields at 0.25% APY. Happily, I was proven wrong.

Lending Club now offers 4.8% APY to 5.15% APY on the full balance of LevelUp (personal) savings accounts. And, their Tailored Checking (business) accounts yield 1.5% APY up to $100K.

Moreover, spending on Rewards Checking (personal) and Tailored Checking (business) accounts earn 1% unlimited cash back on spending.

Recommended: 3 Best Credit Unions for Small Business Banking

Company Overview

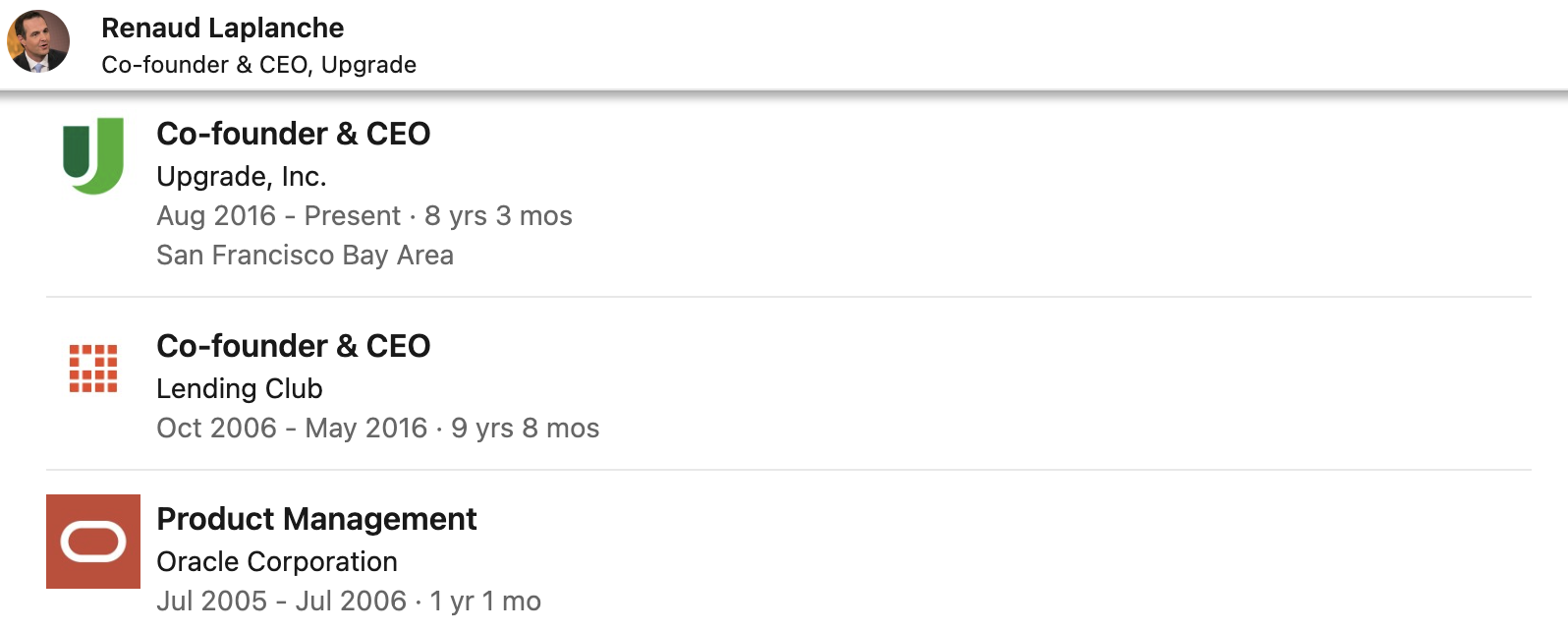

Lending Club, aka Lending Club Corporation, is a San Francisco-based company that was founded in 2007 by Renaud Laplanch, who is also the CEO & founder of Upgrade. Prior to launching two successful financial corporations ten years apart, he was a product manager at Oracle.

Oracle actually acquired one of Laplanche’s earlier products, MatchPoint, in 2005. So, he likely temporarily took over product management of that segment of Oracle’s business after the acquisition and merger.

Before his entrepreneurial ventures, Laplanche served as an associate at New York’s Cleary Gottlieb, a leading international law firm.

In May 2016, Laplanche resigned following what was labeled “improper decision-making.” LendingClub’s board stated that the resignation took place after Laplanche went against investors’ wishes in a multi-million dollar deal—This was commonly referred to as “the Lending Club scandal,” and made it sound like some sort of pyramid scheme gone wrong, which wasn’t the case.

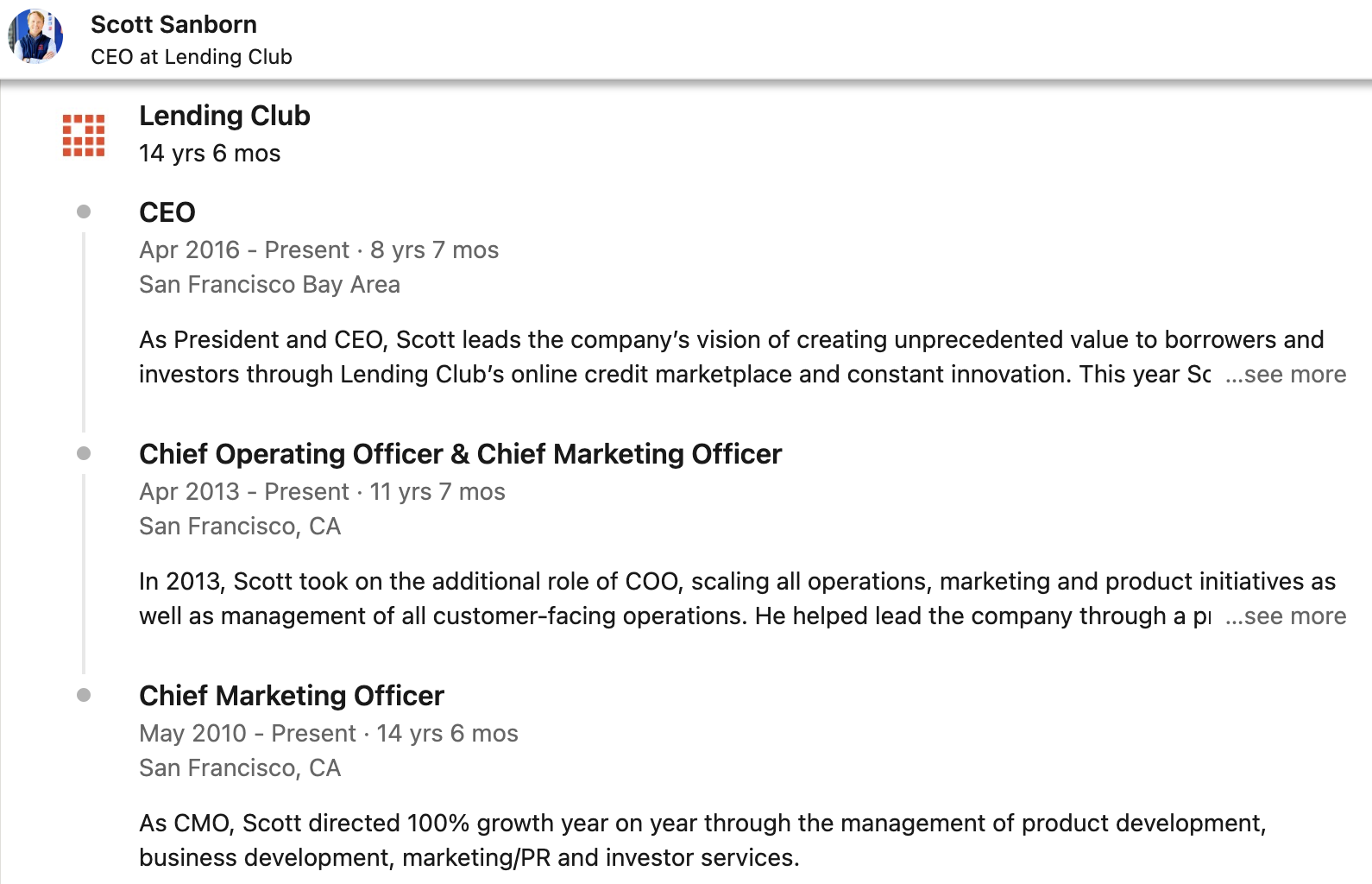

At that time, the COO/CMO, Scott Sanborn, took over as Lending Club’s CEO.

Sanborn has a strong business and marketing background, having held high-level executive roles at Home Shopping Network (HSN), RedEnvelope, and eHealthInsurance prior to 2010.

Today, Lending Club has an A+ Better Business Bureau (BBB) rating with 4.4 out of 5 average stars given and accreditation dating back to 2008. All of their 1,199 complaints in the last three years have been closed successfully.

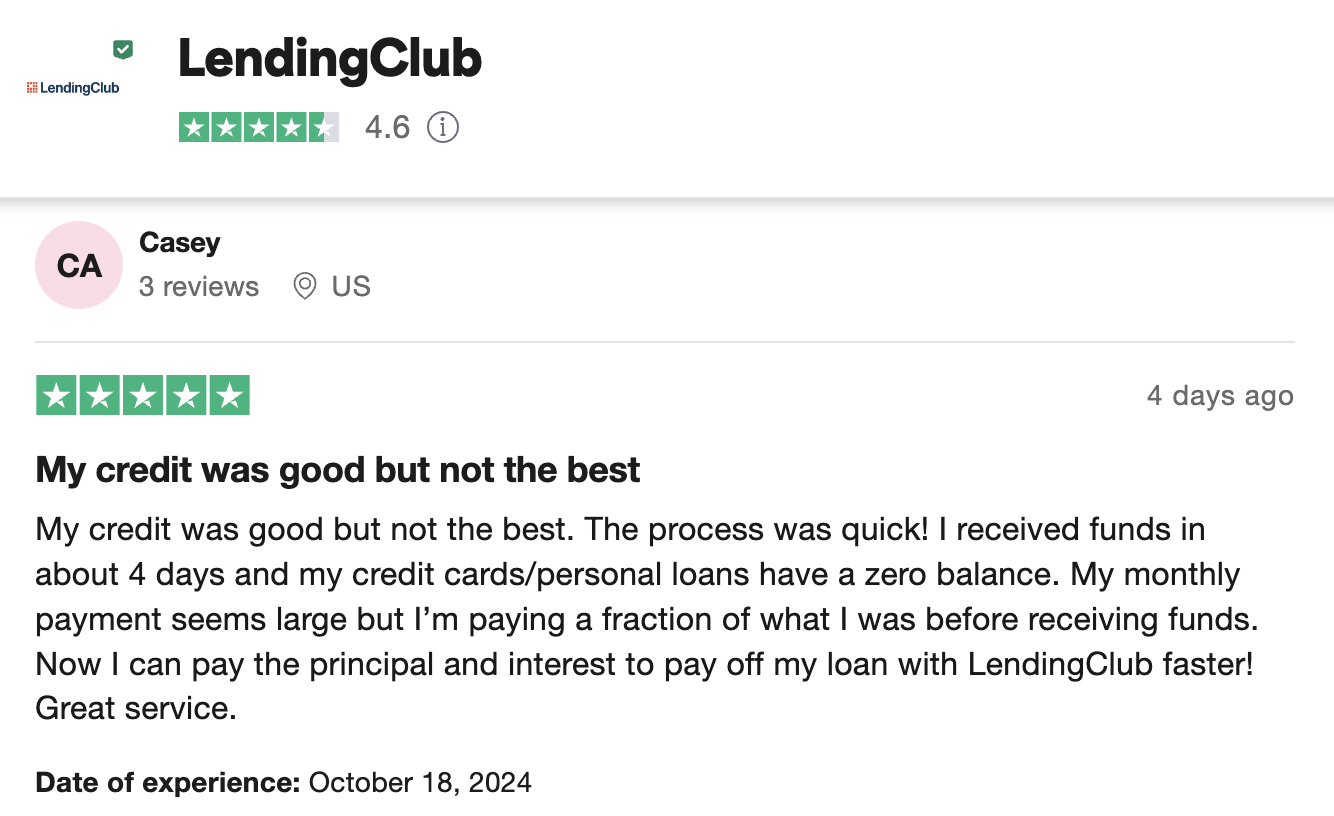

On Trustpilot, Lending Club’s TrustScore™ is 4.6 out of 5 (which is great for a financial offer). Customers praise its fast, easy loan process and “lower” interest rates. Positive reviews highlight efficient service and helpful customer support. Still, a small percentage report issues, mainly related to communication for investors and loan policies during the pandemic.

Overall, LendingClub is highly rated for quick funding and debt relief, though some users had isolated concerns.

However, in 2018, Lending Club paid $18 million to settle FTC charges that alleged that the company included hidden fees in their loan processes.

After this, Lending Club agreed to “clearly and conspicuously disclose the amount of any prepaid, up-front, or origination fee and the total amount of funds that borrowers will receive.”

Since this incident, a lot of people still ask, ‘why is Lending Club shutting down?’ The answer is, it’s not. That was a rumor from the beginning.

In all, it’s probably fair to say LendingClub has a generally positive standing but has faced serious issues with transparency in the past. But, they seem to have been addressed.

You might also like: Is United Capital Source Legit? A Complete, Uncut Breakdown

Lending Club Business Loans

Lending Club small business loans and lending club SBA loans cater specifically to businesses. Their business financing offers higher amounts to qualified business owners than to consumers. So, let’s find out what you can expect and what you might qualify for.

Note: Lending Club’s business loans are offered in partnership with Accion Opportunity Fund (a non-profit lender, that is also a driving force behind Skip’s small business grant offer).

1. Loan Amounts from $5K to $250K

With Lending Club, your business can borrow between $5K and $250K, which can give you the flexibility to secure the right amount based on your business needs. This range covers a variety of financial goals, whether you’re expanding, covering expenses, or consolidating debt.

You might also like: Ramp Card Review: Is This the Corporate Card for You?

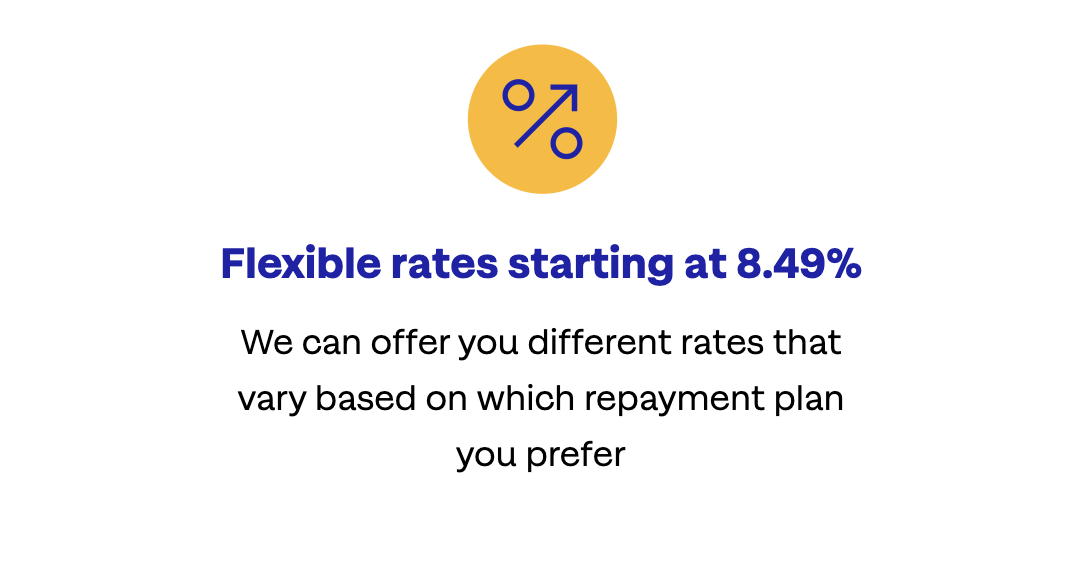

2. Competitive Business Loan Rates

Lending Club’s business loan rates, through Accion Opportunity fund, actually start on, at 8.49%. According to the most recent data from the Federal Reserve as of November 2024, the typical interest rate for small-business bank loans ranged between 6.42% and 12.41%.

Note: Lending Club’s SBA loan rates (not what we’re talking about here) are based on the current prime rate.

You might also like: No-Doc Business Loans: Get Funds Without Proof of Income

3. Fixed Monthly Payments & No Prepayment Penalties

Fixed monthly payments provide stability and make it easier to budget for loan repayments. This predictability can help keep your business cash flow on track without unexpected changes to payment amounts.

If you’re able to pay off your loan early, there are no penalties—This allows you to save on interest costs if your business finances improve sooner than expected, giving you more control over total loan expenses.

4. Flexible Terms, Easy Application, & Quick Funding

With term options ranging from 1 to 5 years, you can choose the repayment period that best suits your business’s financial strategy. Shorter terms mean less interest overall, while longer terms can make monthly payments more manageable.

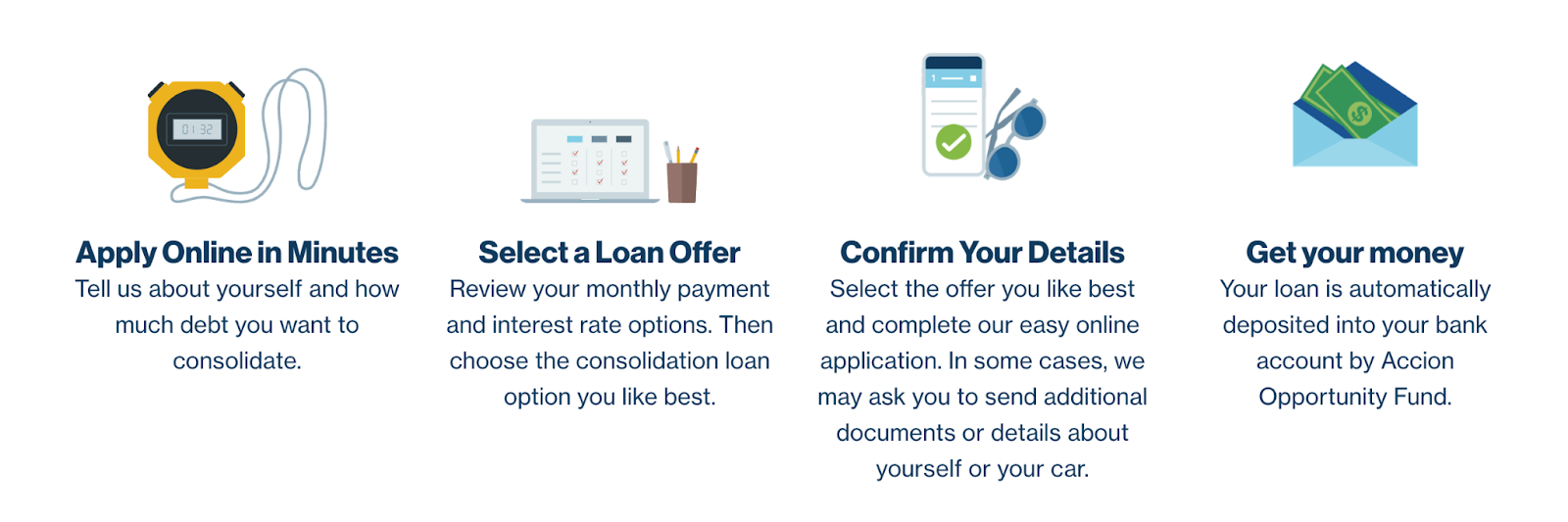

You can apply online in minutes, making the process quick and convenient. Once approved, Accion Opportunity Fund deposits the funds directly into your bank account, allowing you to access financing without delay.

How to Get a Small Business Loan with Lending Club

If you’re wondering how to get a business loan with Lending Club, the answer is uncomplicated.

To qualify, your business needs to meet basic eligibility criteria:

- 12+ months in business

- $50K+ in annual sales

- US-based company

- 20% or more ownership

- Consumer credit score of 600+

A lot of business loans that we review require at least 50% ownership for an owner-applicant to qualify. So, Lending Club stands out in this area.

While these loans appear to be issued based on the owner-applicant’s credit score, Accion Opportunity Fund is known to report business payment activity to Experian, Equifax, and Dun & Bradstreet—These are the leading business credit bureaus, so on-time payments can help you build your business credit score.

You might also like: This is How to Leverage Business Credit to Transform Your Life

Frequently Asked Questions

Is it hard to get a loan through LendingClub?

LendingClub has flexible lending criteria, but you’ll generally need a good credit score, steady income, and a manageable debt-to-income ratio to qualify. Their process is straightforward, though approval requirements may vary.

Is LendingClub an actual loan company?

Yes, LendingClub is a legitimate online lending company that connects borrowers with investors for personal, business, and medical loans. They’ve been in operation since 2007.

Is LendingClub bank in trouble?

No, LendingClub is not currently facing any known legal or financial issues. The company has faced some challenges in the past, but it maintains high ratings on platforms like BBB and Trustpilot today.

Is LendingClub a safe place to put money?

Yes, LendingClub is generally considered safe for both borrowers and investors, with strong security protocols. However, as with any investment, there are risks, especially in loan investing.

Conclusion: Can Lending Club be Trusted?

As a borrower, LendingClub’s offer is legit, yes. The company is established and has grown to become a trustworthy funding source for personal loans, business loans, auto refinancing, and patient solutions.

Through their partnership with Accion Opportunity Fund, you could qualify to get up to $250K in business credit if you and your business meet the qualifications. If you apply and don’t qualify for a business loan, Accion Opportunity will attempt to refer you to one of their partners to provide other resources.

Are you ready to learn how to get up to $100K in business credit? Join Business Credit Workshop today!