If you applied for a loan with OnDeck, Lenzi, or another online loan marketplace, you may have been referred to Bitty Advance for business funding. But, their advertising isn’t super transparent about terms and fees. So, I wanted to do a deep dive to explain what you might expect.

Here, you’ll find out what Bitty Advance is, get some insights into their terms, and explore all the features of a Bitty merchant cash advance. Plus, I’ll answer some of the most common questions that people ask.

This is what’s in store:

- What is Bitty Advance?

- What to Expect With a Bitty Advance MCA

- Frequently Asked Questions

- Conclusion: Is Bitty Advance Legit?

Now, let’s go!

What is Bitty Advance?

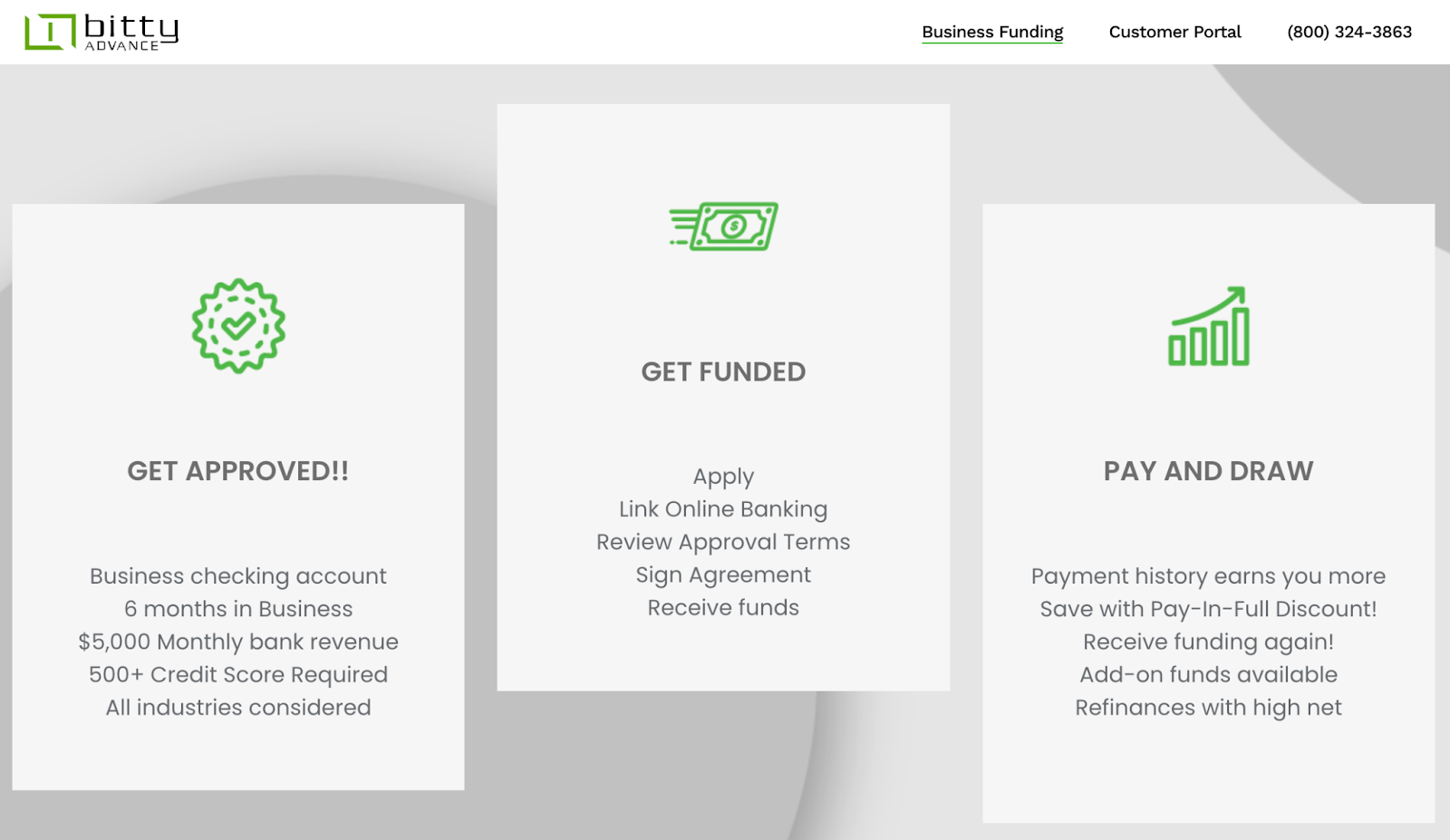

Bitty Advance is a newer financial services company that specializes in funding small businesses through Merchant Cash Advances (MCAs)—An MCA is a financial product where a business receives a lump sum of cash in exchange for a percentage of its future credit card sales or overall revenue.

It’s not a traditional loan but rather an “advance” against future earnings. They offer funds from $2K to $250K, and the company is known for its quick funding process and transparent terms.

Bitty Advance caters to businesses in various industries, including:

- Restaurants

- Trucking

- Healthcare

- Construction

- More

Bitty Advance aims to help small businesses by providing the capital they need to grow and thrive…even if they have bad credit.

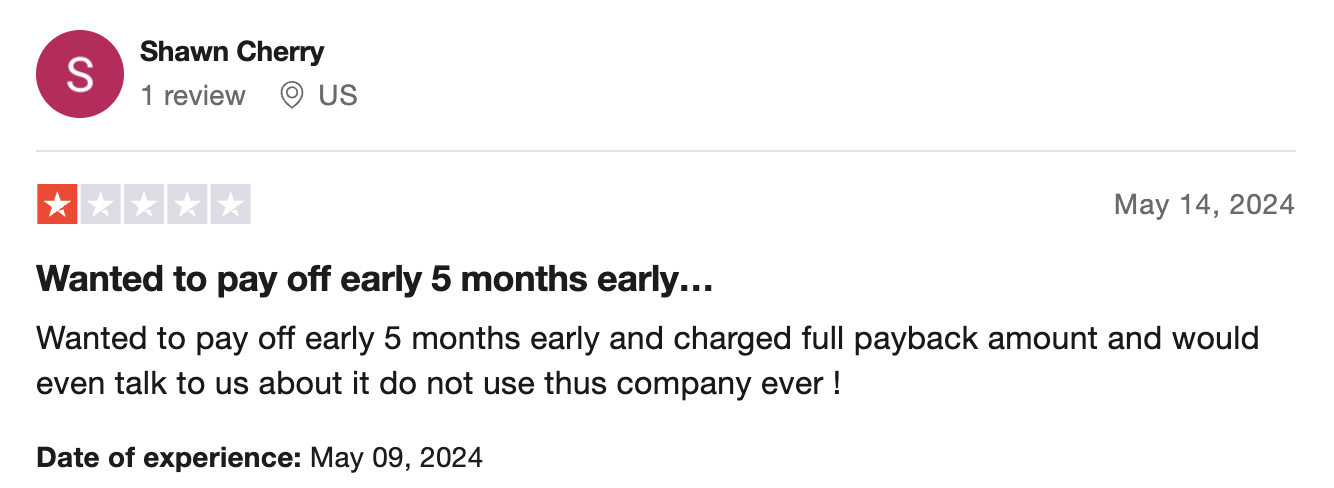

Now, Bitty is supposed to offer early payoff discounts. But, some user reviews suggest that this isn’t always the case, which can be disappointing if you expect savings.

Right away, in case you don’t already know, I should also say that MCAs are a factored loan, as opposed to a traditional interest-based loan. And, factored loans tend to be more expensive in the end.

You might also like: Full OnDeck Review: All You Need to Know About the Business Funding Offer

Company Overview

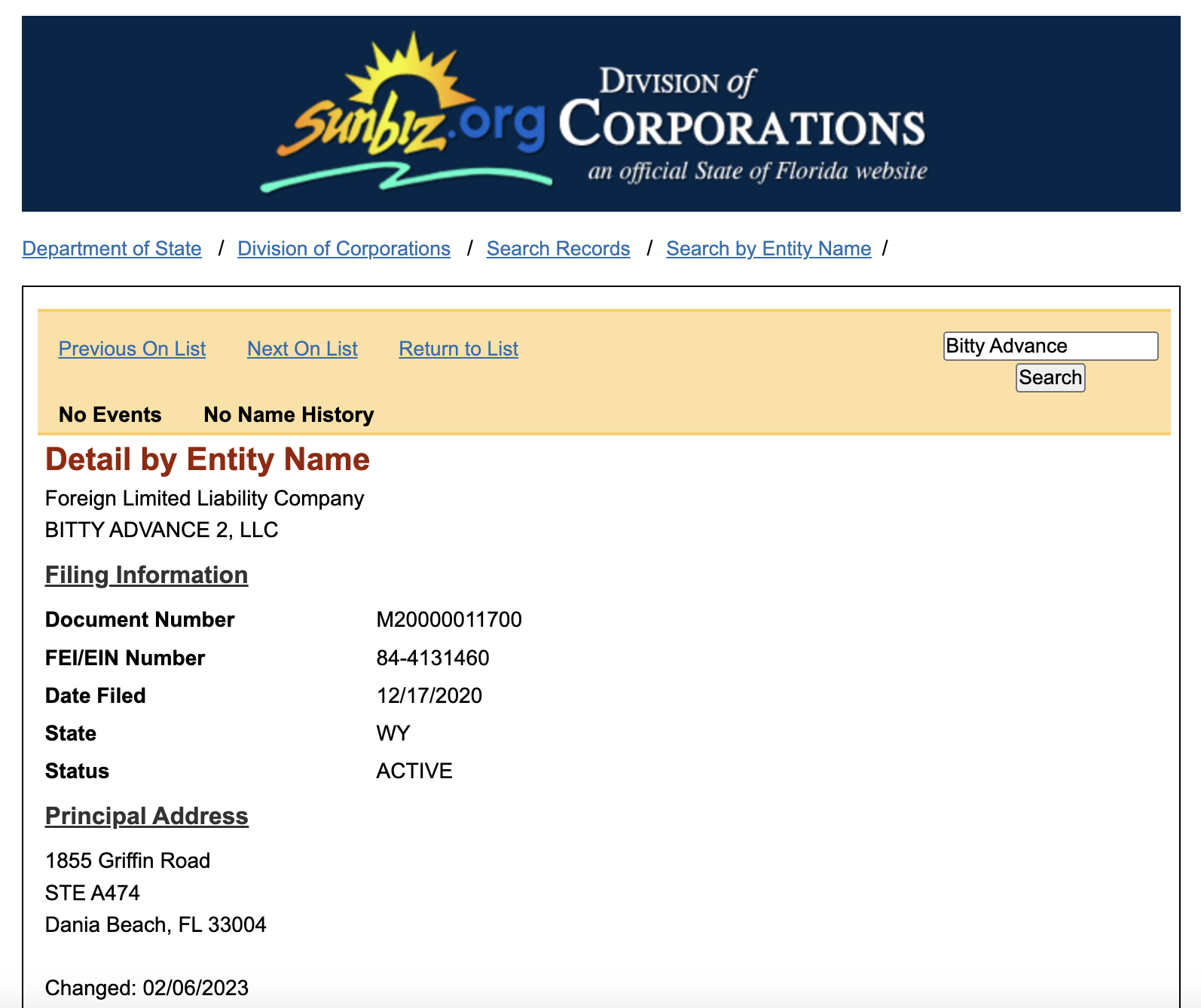

Bitty Advance 2 LLC has been actively registered in the state of Florida since December of 2020, though cited as operational since 2018. The company’s registered agent is “Registered Agents Inc.,” and the current manager is Craig Hecker (the same Craig Hecker who founded Rapid Capital Funding, no longer operational).

Right away, there are some red flags with Sunbiz records:

- I’m assuming there was a Bitty Advance 1 before Bitty Advance 2.

- Rapid Capital Funding II LLC last reported on their business in 2018.

- The first Rapid Capital Funding LLC was also active until 2018.

This just looks messy…

To me, the inconsistency indicates that there could have been some problems that led to re-registration and re-branding. After a 5-second search, I found about half a dozen lawsuits against both Rapid Capital and Rapid Capital II. Without delving into the specifics of each case, there are disputes ranging from breach of contract to unspecified claims.

And, if you do some digging of your own, it will shed light on legal matters involving Bitty Advance, including lawsuits, debt relief options, and complaints—Hinting at potential challenges faced by individuals and businesses dealing with Bitty.

With that out of the way, I notice that Bitty isn’t at all transparent about their terms, rates, and fees on their website or in their advertising (I’ll try my best to shed some light on that soon). I see this as a red flag too, since it doesn’t enable comparison shopping.

And, Bitty doesn’t allow you to apply online without speaking with a loan agent…This isn’t completely unheard of, but it appears they’re not keeping up with the industry.

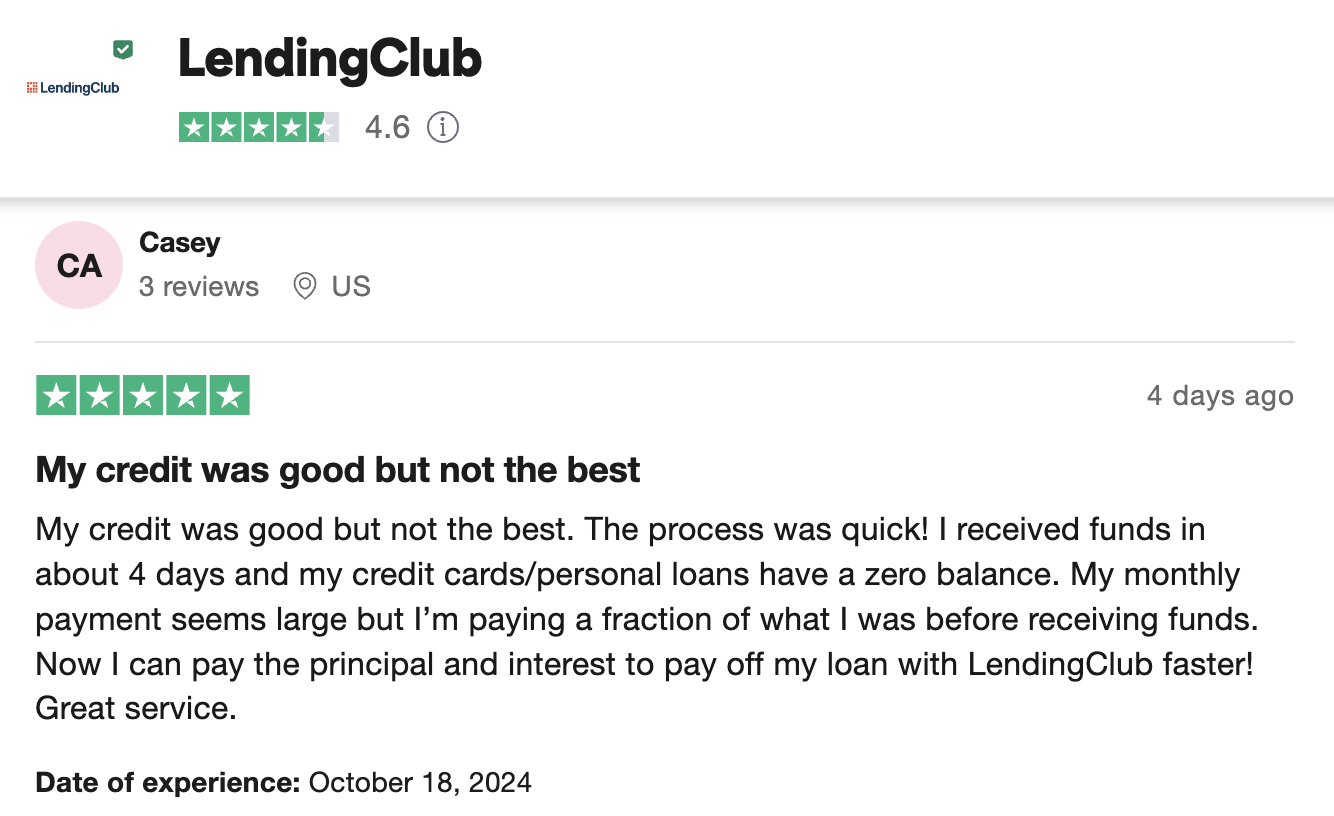

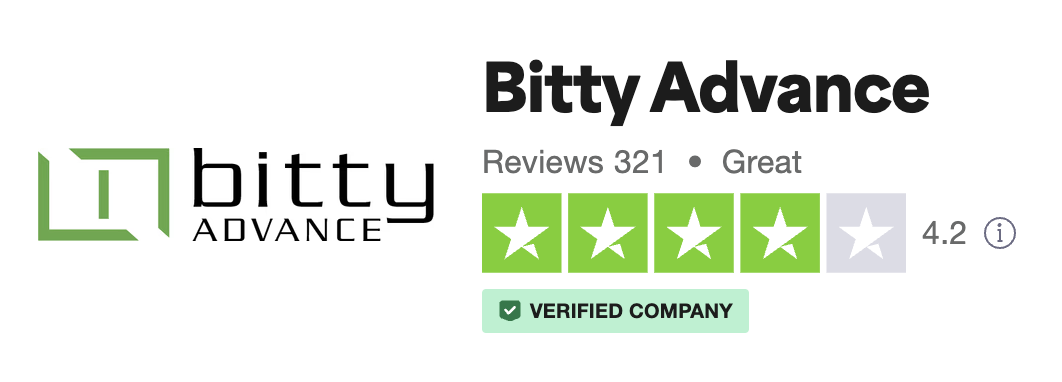

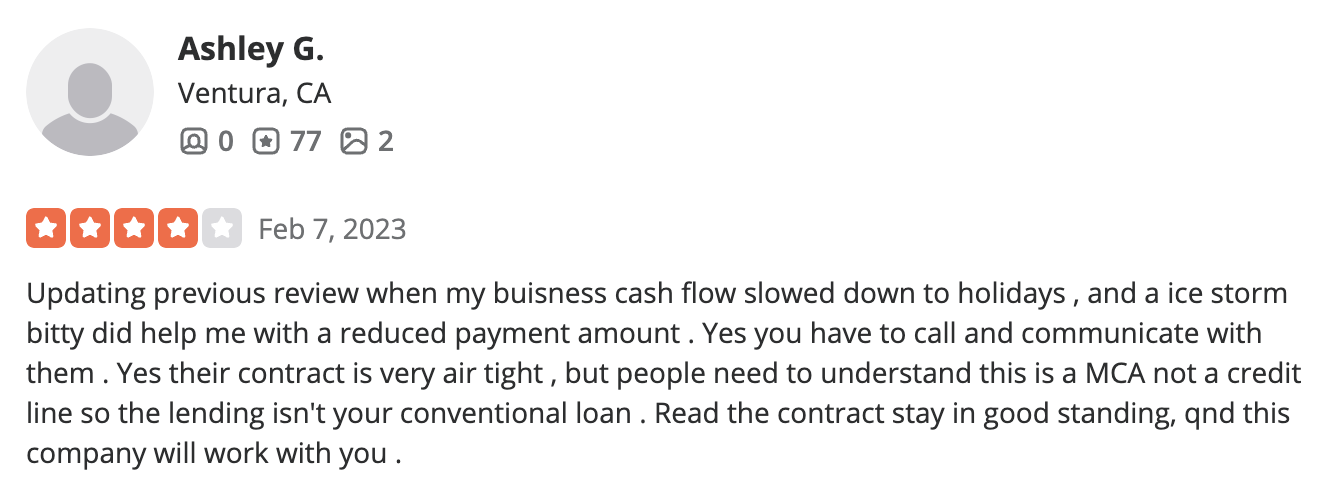

Now, on Trustpilot, Bitty Advance maintains a 4.2-star Trustscore, which is pretty high. Trustpilot reviewers have varied opinions on Bitty Advance, with some praising the company for its efficiency, quick disbursement, and helpful staff, while others express dissatisfaction with issues such as lack of communication, unexpected charges, and difficulties with early payoffs. Overall, the reviews highlight both positive and negative experiences.

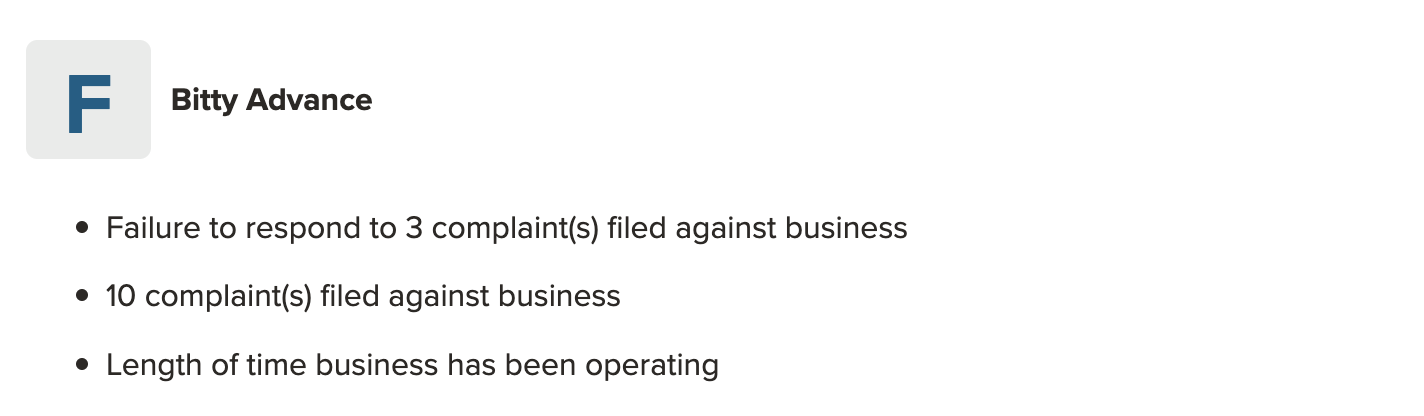

The Better Business Bureau (BBB), on the other hand, paints a different picture. Of ten BBB complaints filed against the business, three remain unanswered by the company. And, with the business not being super well established, BBB has given Bitty Advance an F rating.

This isn’t great, especially where some businesses have hundreds of complaints and maintain A ratings on BBB.

Altogether, the background of Bitty Advance 2 LLC raises some concerns, with past legal entanglements and a lack of upfront transparency, despite some positive reviews on Trustpilot. The Better Business Bureau’s F rating and unresolved complaints add to the complexity and might point at the potential for challenges.

You might also like: A Complete Northwest Registered Agent Review & Analysis

What to Expect With a Bitty Advance MCA

The main appeal, and most common highlight of Bitty’s offer is that you can get quick access to cash. You can call Bitty Advance at (800) 324-3863 to start the application process.

Based on the hundreds of user experiences I scoured through, I estimate that the factor rate range for Bitty Advance is likely between 1.5 and 2.5—This estimate is based on the “high fees,” “unexpected charges,” and substantial repayment amounts mentioned in reviews on Trustpilot and other platforms.

While Bitty Advance doesn’t provide exact figures for the factor rate, the significant costs incurred by borrowers suggest a factor rate higher than the industry average (I often see rates between 1.1 and 1.5).

Let’s break this down:

When you enter into an MCA agreement with a company like Bitty Advance, you would receive a lump sum upfront in exchange for a portion of your future credit card sales—This portion would be calculated using a factor rate, which is a multiplier applied to the amount funded.

For example, let’s say you receive a $25K advance from Bitty Advance with a factor rate of 1.8. The total amount you would need to repay would be $25K * 1.8 = $45K.

Now, repayment is typically made through a percentage of daily credit card sales. So, let’s assume that the agreement specifies a daily repayment percentage of 15% (anecdotally, it could be higher with Bitty, up to 35%)—If your credit card sales for a particular day total $3,000, they would need to remit 15% of that amount to Bitty Advance.

So, $3,000 * 0.15 = $450 (or more) would be remitted to Bitty Advance for that day’s repayment.

This repayment structure would continue until the total repayment amount of $45k was reached. And, the actual repayment amount would vary depending on your daily credit card sales.

Frequently Asked Questions

How do I get approved for Bitty Advance?

You need to meet their criteria, which usually includes a monthly revenue of around $5K or more and business history (established for at least 30-90 days). Apply online and provide requested documentation for review – there is no hard credit pull, so the main risk is paying any hidden fees.

Can a merchant cash advance hurt your credit?

Generally no, but defaulting on repayment could indirectly impact your credit score through collections or legal actions.

How do I know if a loan company is scamming me?

Watch out for unsolicited offers, upfront fees, lack of transparency, pressure tactics, unlicensed lenders, and trust your instincts.

Conclusion: Is Bitty Advance Legit?

Technically, yeah, Bitty Advance is a legitimate business, registered and active in the state of Florida. They are operating legally, but several lawsuits allege that leadership may be sitting in a gray area.

And, Bitty’s repayment structure could have both advantages and disadvantages:

- On the one hand, it provides quick access to capital without the need for collateral or a lengthy approval process.

- However, the high factor rate and daily repayment percentage can result in significant costs, which can impact your cash flow and profitability over time.

Personally, I never recommend factored loans unless there is absolutely no other option. And, always read the fine print before you sign anything.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!