Many business owners use LenCred to solve cash flow problems and increase their financial knowledge. But, before you take the leap and sign up for LenCred’s funding services, you need to know if it’s a wise decision. Will the system meet your company’s financial needs?

If you’re already seeking the answer to this question, you know that a Google search for ‘LenCred reviews’ spits back conflicting opinions.

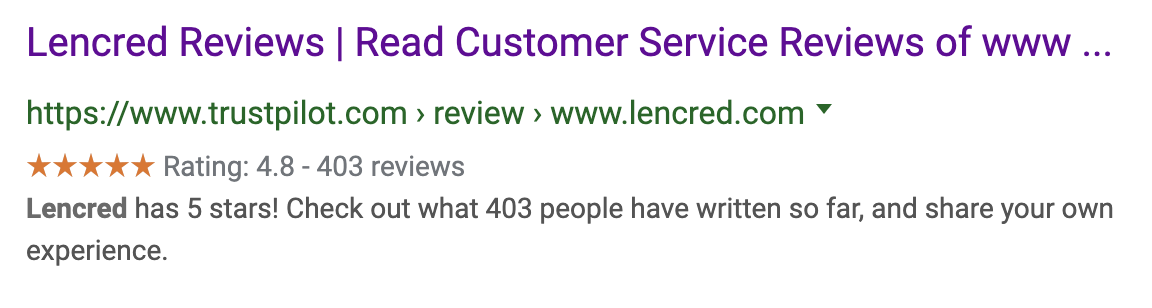

First, TrustPilot gives the platform nearly a five-star rating.

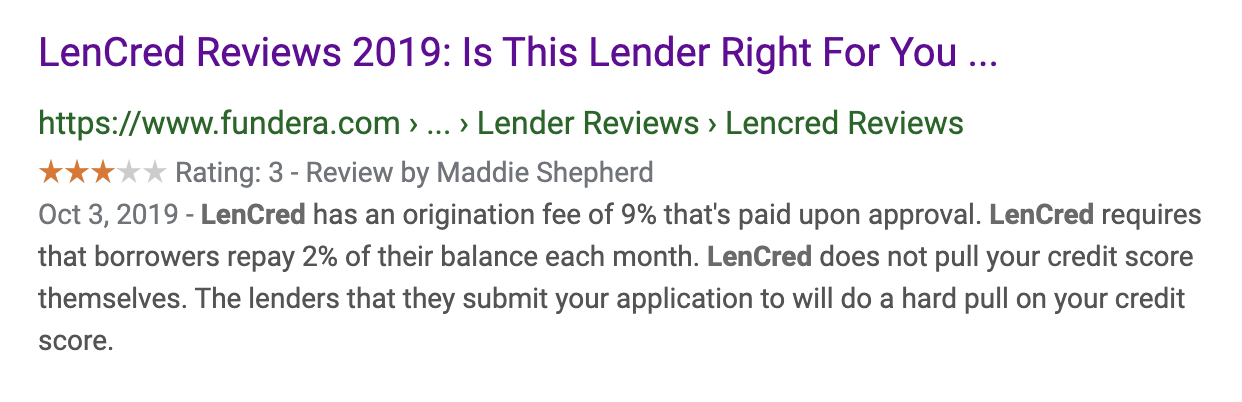

Then, Fundera only gives LenCred three stars.

Who can you trust? It’s my job to provide you with the most helpful information possible. So, I’ve dug a bit to find out what’s actually up with LenCred. Know the facts so you can make an informed decision for yourself.

First, What is LenCred?

LenCred is a small business funding platform that helps companies with financial education and startup loans or working capital. They provide in-depth credit, income, and financial background reviews before submitting applications to lenders on business owners’ behalf.

Individuals can leverage LenCred’s services to draw from $25K to $150K in loans or business credit lines. The funds acquired through these services can be used to start or grow a business.

What is a FICO Pro Certified Business Funding Advisor?

LenCred boasts in their introductory video that company owners can call in and speak with a “FICO Pro Certified” business funding advisor. But, what does that mean? A FICO Pro Certification is a financial education program launched in 2010 by a company called AllRegs, a Sallie Mae partner. The program has since been discontinued, which might signal that the credibility of the funding advisors should be questioned.

When evaluating merit, I try to look for contemporary and more credible credentials like SAP FICO Certification Exam completion (a test that ensures financial consultants possess proven knowledge and fundamental skills in financial accounting).

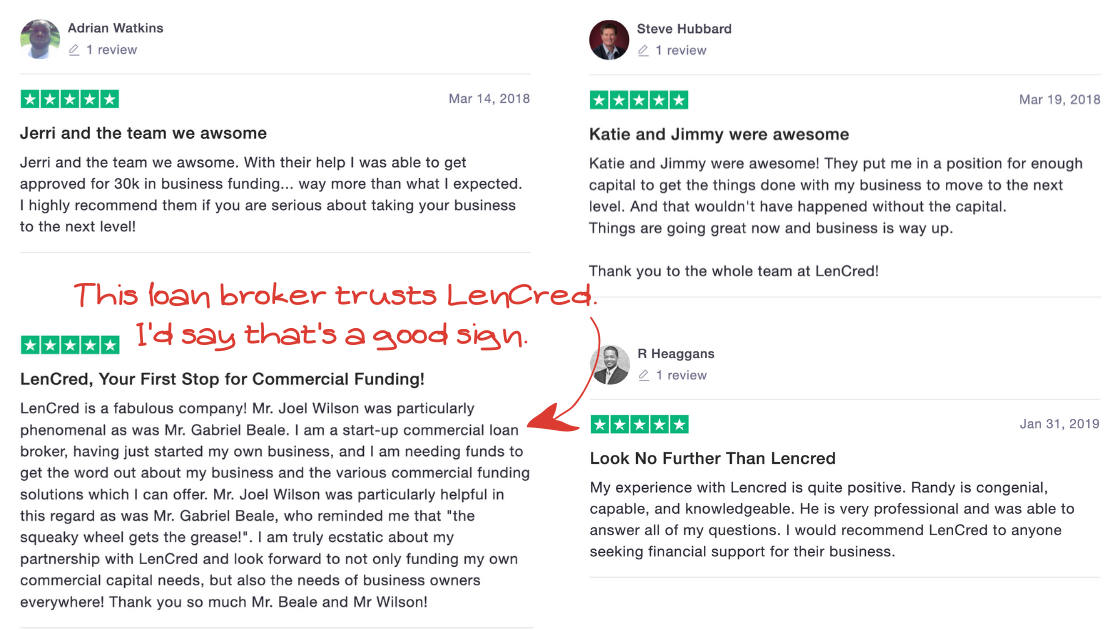

Still, most users that review the platform are satisfied with their LenCred advisors’ financial knowledge and experience. At least one loan broker has left excellent platform feedback. Since he’s working in the same realm, his opinion probably has some weight.

So, while a FICO Pro Certification probably isn’t the best determining factor for selecting a credit advisor, LenCred’s staff has the recommendations (and experience) to back up their claims. They have satisfied many small business owners with their services.

Next, How Does LenCred Work?

After doing a soft pull on your personal credit report, LenCred’s proprietary software gathers information from more than 20 data points in your financial background. The information is used to predict your prequalification potential for an unsecured line of revolving credit from various lenders. And, your applications are submitted to several companies at one time.

What Educational Resources Are Available Through LenCred?

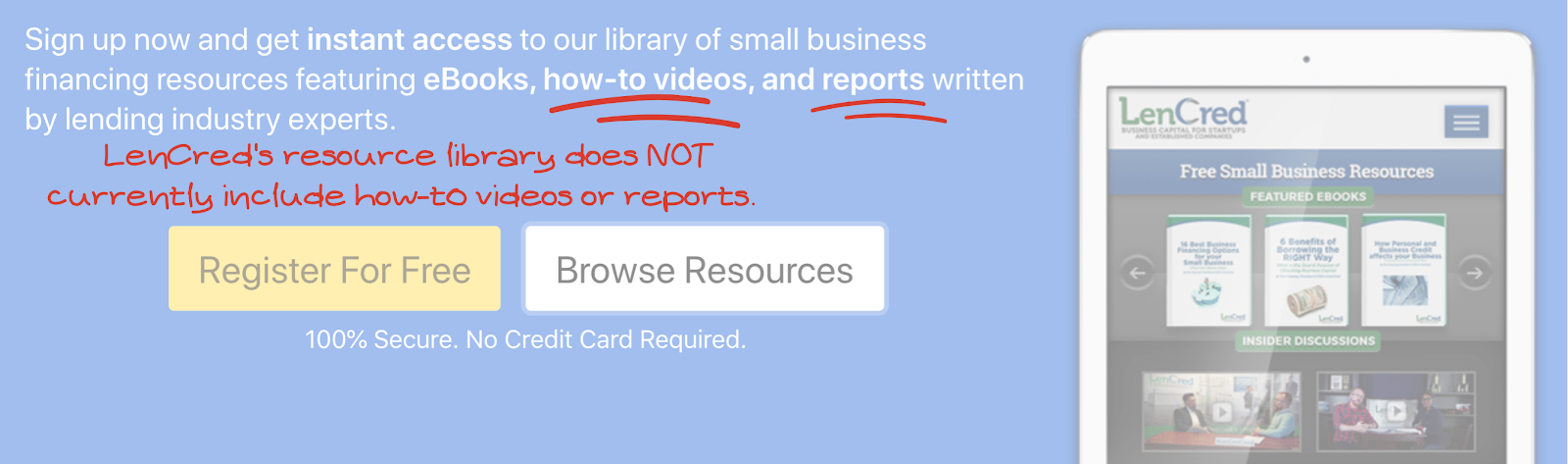

While the website boasts that they deliver how-to videos and reports, this is not true.

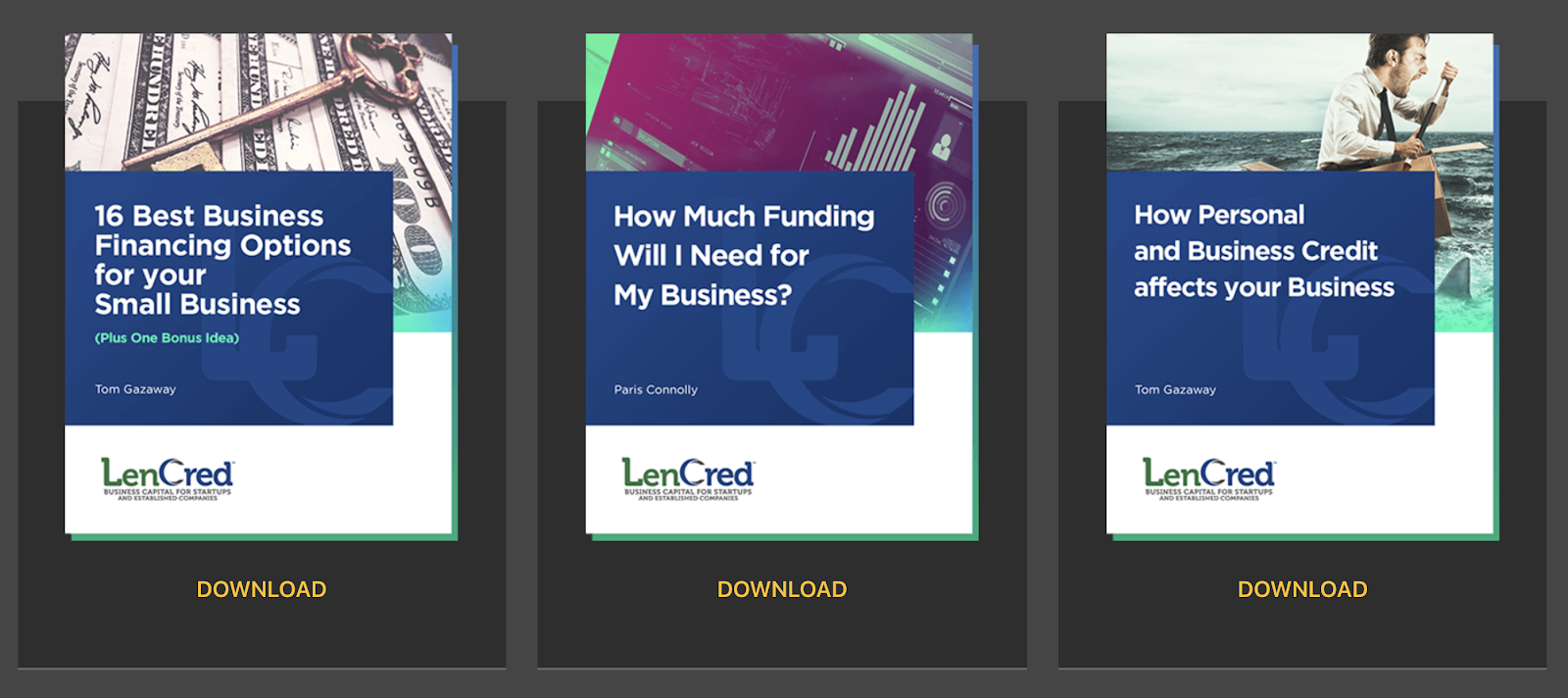

At this time, the financial resources available on the website are limited to eBooks.

LenCred’s Business Financing Guides provide helpful financial tips for small businesses. These eight eBooks are written by various financial experts.

- Tom Gazaway, President & CEO of LenCred

- Paris Connoly, Founder of PC Communications

- Rieva Lesonsky, CEO of GrowBiz Media

- Barbara Taylor, Co-Founder of Synergy Business Services

The guides cover topics like, “How Much Funding Will I Need for My Business?” and, “The Blessing and Curse of Starting a Business With Good Credit.” They seem to be around 15 pages each and are filled with professional advice from successful entrepreneurs. For startups and beginners who seek financial knowledge, this place is as good as any to start.

LenCred also has a Small Business Financing Blog on their website. Here, they publish new posts less frequently than once per month. This knowledge base covers 9 topics.

- Borrowing Money

- Business & Personal Credit

- Credit Disputes

- Credit Reporting

- Entrepreneurship Advice

- Raising Capital

- Small Business Advice

- Startup Capital

- Working Capital

The LenCred blog provides another decent resource for business beginners.

How Many Lenders Will Receive Your Application for Credit?

Your experience of the system will vary based on which advisor you work with and your personal credit history. And, the number of funding applications submitted by LenCred on your behalf will differ.

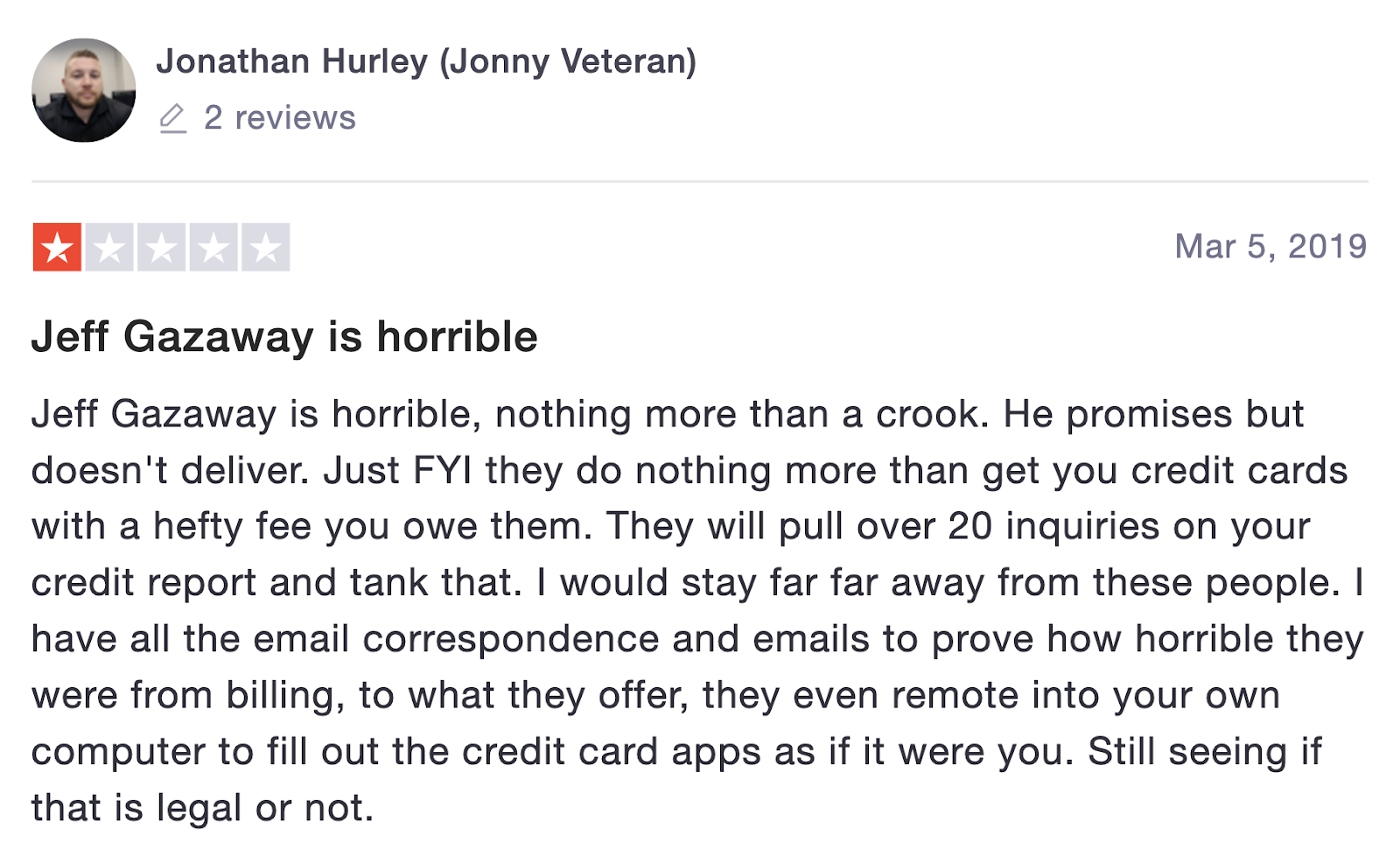

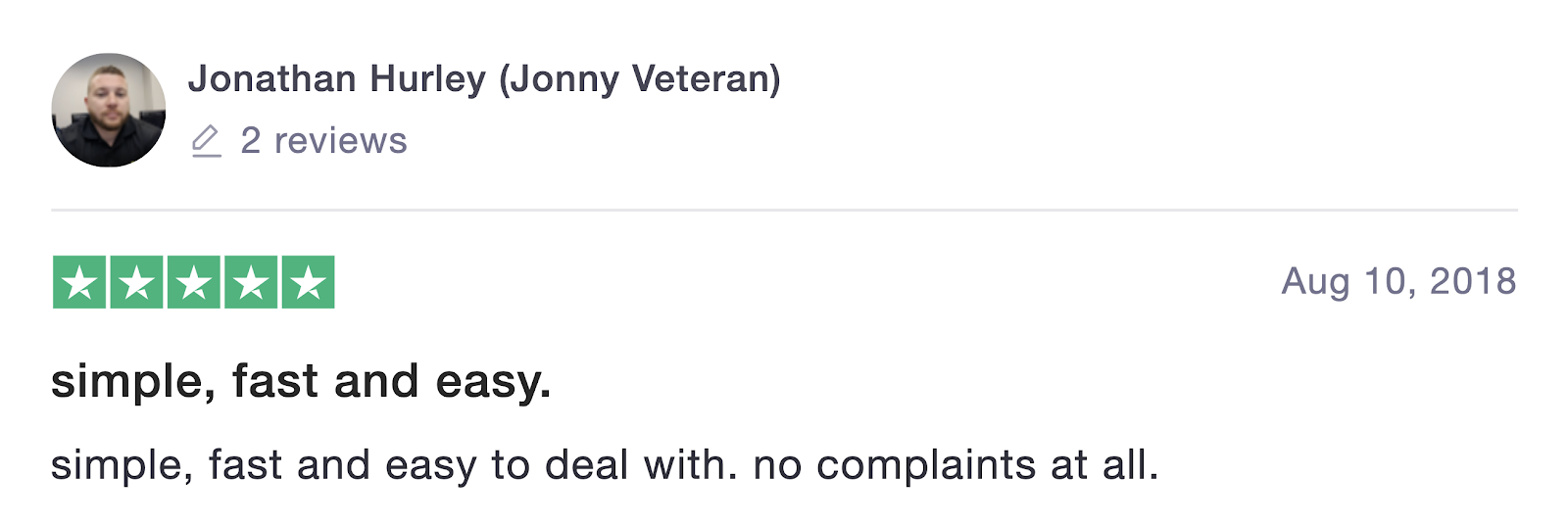

One fact is certain: you will receive numerous hard pulls on your personal credit report before you qualify for a loan through one of the businesses in LenCred’s network of lenders.

One user complained that using the system led to 20 hard pulls on his credit report, which would be frustrating for anyone and does seem excessive.

But, the same user was satisfied with LenCred’s services less than a year prior. So, it’s likely that fewer applications were submitted the first time he applied for working capital.

This aspect of the system isn’t unusual. For example, when buying a car through a dealership, the lending department often follows a similar process. So, while it can be annoying that you’re not approved for every line of credit you want or expect, numerous hard pulls are in alignment with best practices.

What’s Involved in LenCred’s Application Process?

When you are ready to apply for financing through LenCred, you should first contact the company through their website contact form. Be sure to choose ‘Business Financing’ from the dropdown menu for the ‘Type of Inquiry’ before you send your message. A representative from the company will reply as soon as possible.

Alternatively, you can call the company directly at (888) 783-1503.

Your LenCred representative will ask your business goals, the amount of working capital needed, and what you plan to use it for.

Then, an advisor will inform you of how to proceed with your application. This will involve submitting verification of income, identification number submission, and other typical financial documentation.

| Note: According to a LenCred representative I spoke with over the phone in December 2019, LenCred applies for lines of credit and credit cards based on your personal credit history through Experian. So, they will not use your EIN or DUNS™ number to check your business credit profile. |

After that, the company will do a soft pull to get a birds-eye-view of your financial history. From this data, an expert will make an informed prediction about the best types of credit to apply for based on what you will most likely qualify for.

And, there are a few minimum requirements to leverage their services.

- Experian credit score of at least 670

- 3-5 years of credit history

- $30,000-40,000+ in annual household income

If you meet the bar, the company should be able to help you.

What Types of Working Capital Will LenCred Try to Get for You?

LendCred typically works with four types of small business financing.

- Small Business Loans – term loans that are typically funded through a conventional bank or credit union.

- Business Lines of Credit – revolving credit, typically credit cards, obtained on behalf of a business.

- Equipment Financing – funding obtained directly from equipment retailers.

- SBA Loans – small business loans that are partially guaranteed by the Small Business Administration (SBA).

LenCred will not submit applications to net 30 vendors. Furthermore, the platform is not affiliated with angel investing, crowdfunding, invoice factoring, merchant cash advances, or any other unconventional working capital or startup funding.

One common complaint multiple business owners have had, “I could have applied for these credit cards myself.” Company representatives typically respond right away with an explanation.

The usual reason for establishing multiple credit cards for a business rather than a loan is that the applicant was not likely to qualify for a loan. LenCred promises to always choose the best finding option for each individual.

And, What Does LenCred Charge?

Now, you need to know how much LenCred’s services will cost. The service isn’t free and you will have to decide if the expert assistance is worth it to you.

- Educational resources: Free

- Initial consultation & application submission: Free

- Origination fees: 5-10% of credit line

| While LenCred does not list the cost of their services on their website, past clients have posted public statements that support the above origination fee range estimate. Your amount may vary based on your personal credit profile. |

The most likely origination fee for credit established through LendCred’s services is 9%. So, if you receive $25,000, you will likely pay $2,250. And, this amount will be instantly added to your repayment obligation. In other words, if you need $25,000 in working capital, LendCred will try to qualify you for around $27,250.

How Long Does it Take to Receive Funding Through LenCred?

Upon approval, it can take from 5 to 40 days to receive your funds, depending on the lender you establish a credit line(s) with. In some cases, you will acquire funds from multiple companies that will disburse funds on different dates.

Conclusion: The Value of LenCred’s Financial Services Depends on Your Situation

If you need working capital or startup funds, and you have good credit with low knowledge of conventional funding options, LenCred might be your saving grace. When you’re not interested in an unconventional option like crowdfunding and you don’t mind paying a 9% origination fee, you may prosper through Lencred’s financing services. However, if you’re trying to build business credit and want to obtain funding without paying high origination fees, LenCred would not be the suggested route. Since they do not use your business credit profile to acquire funds, their lenders are not likely to report to the business credit bureaus. To learn more about boosting your business credit score and acquiring small business lines of credit (without paying high origination fees), start here: learn how to obtain business credit in 30 days.