Disclaimer: Business Credit Workshop does not recommend or endorse tradeline brokering. However, there are several people in the business credit community who have leveraged Superior Tradelines’ services and reported good results. So, we wanted to learn everything we can about the offer and, of course, share our findings here.

Please, do your own due diligence, as this post is only meant to provide more information.

Now, in a nutshell, Superior Tradelines rents out tradelines (credit accounts) to boost credit scores by increasing the age and credit limit on users’ credit profiles.

So, is it a scam? Or, is it a good way to boost your credit score?

Here’s what you’ll learn:

- What is a Tradeline Broker?

- Superior Tradelines Company Overview

- What to Expect When You Become a Superior Tradelines Member

- Conclusion

Now, let’s explore the offer in full.

What is a Tradeline Broker?

A tradeline broker like Superior Tradelines is a company that brokers tradelines between the original account holders and those looking to piggyback off the accounts to boost their credit.

The idea is that the end user pays a fee to have their name and social security number added to an existing credit account in good standing.

Companies like Superior tradelines offer a credit-boosting service that connects those without high-limit, mature accounts instant access to them for a fee.

Why Would You Want to Buy/Rent a Tradeline?

Imagine that someone wants to get a business line of credit, but they don’t have a very strong personal credit profile. On the other hand, their spouse happens to have a ten-year-old Amex account with a $0 balance and a $20K credit limit. By adding themself as an authorized user on the account, it will lower their credit utilization and increase their average account age to increase their credit score and approval odds for a business line of credit.

So, as you can see, someone might want to add a tradeline to their credit profile when seeking business lines of credit. Another use-case is before applying for a mortgage, auto loan, or other major financing.

A new tradeline can improve your credit report. A more established credit profile can help get you better rates and approval odds with lenders… and pretty quickly.

How Long Do Tradelines Last?

Any impact that a “purchased” tradeline might have on your account will likely last at least one reporting cycle (usually, 30 days). There’s even a slight chance that a tradeline could stay on your report for years.

How Much Do Tradelines Increase Credit?

How many points your credit score will increase with an additional tradeline depends on where you’re at right now. A new tradeline can cause anywhere from no impact to an instant, 50-point boost.

Let’s say that you have several accounts that total $20K on your credit report with a credit utilization ratio of 10%. If you were to purchase a new tradeline with a $10K limit and 0% utilization, that would bring your utilization down to 6%. The positive impact, if any, would be minimal.

Now, let’s imagine that you’re in a different boat: You have only one account reporting with a $1,000 limit, and a 90% utilization ratio (you still owe $900). Now, you add the same tradeline from above — a $10K card with 0% used. This would bring your utilization ratio from 90% (very bad) to 8% (very good). This would have a tremendous impact on an otherwise healthy credit score.

Remember, lenders like to see a credit utilization ratio of 33% or less.

Can Tradelines Hurt Your Credit?

While the idea of increasing the average age of your accounts and lowering your credit utilization ratio is enticing, renting a tradeline (or renting out a tradeline) comes with risks.

For “buyers” being added as an authorized user on someone else’s account, there is always the chance that you won’t get what you bargained for. The other person is the owner of the account and can do with it whatever they like, which could involve maxing out their credit card. If they did, your credit utilization would go up as well, harming your credit score.

And, “for sellers,” proceed with caution — according to countless testimonies, many lenders close accounts if they find out users are using theirs to piggyback like this.

Superior Tradelines Company Overview

Superior Tradelines, LLC was founded in 2010, in Cocoa Beach, Florida, by Robert Sigman. Sigman is also the founder of Credzu (credit repair broker), launched in 2012, and Cocoa Beach Office (coworking space), launched in 2019.

Prior to his entrepreneurial ventures, Sigman was a counterintelligence professional who worked with the US Army and General Dynamics Mission Systems.

Superior Tradelines Features & Benefits

There are four key benefits to becoming a Superior Tradelines member.

1. Credit report analysis

The admins at Superior Tradelines will review your three-bureau report straight away and provide guidance on the best step to take next. This might be to purchase a tradeline, or they might advise you to clean up your credit.

2. Buy and sell tradelines

As a verified member, you will be able to access hundreds of tradelines currently up for “sale.” In most cases, this means that you may add yourself as an authorized member to these accounts for a fee.

Tip: If you purchase a tradeline, take advantage of the boost right away.

One major perk here is the $10K surety bond — your purchase is insured.

As a member with a seasoned credit profile, you may also rent out your tradelines on the marketplace. You might be able to make a few thousand dollars per year if you offer up your own accounts.

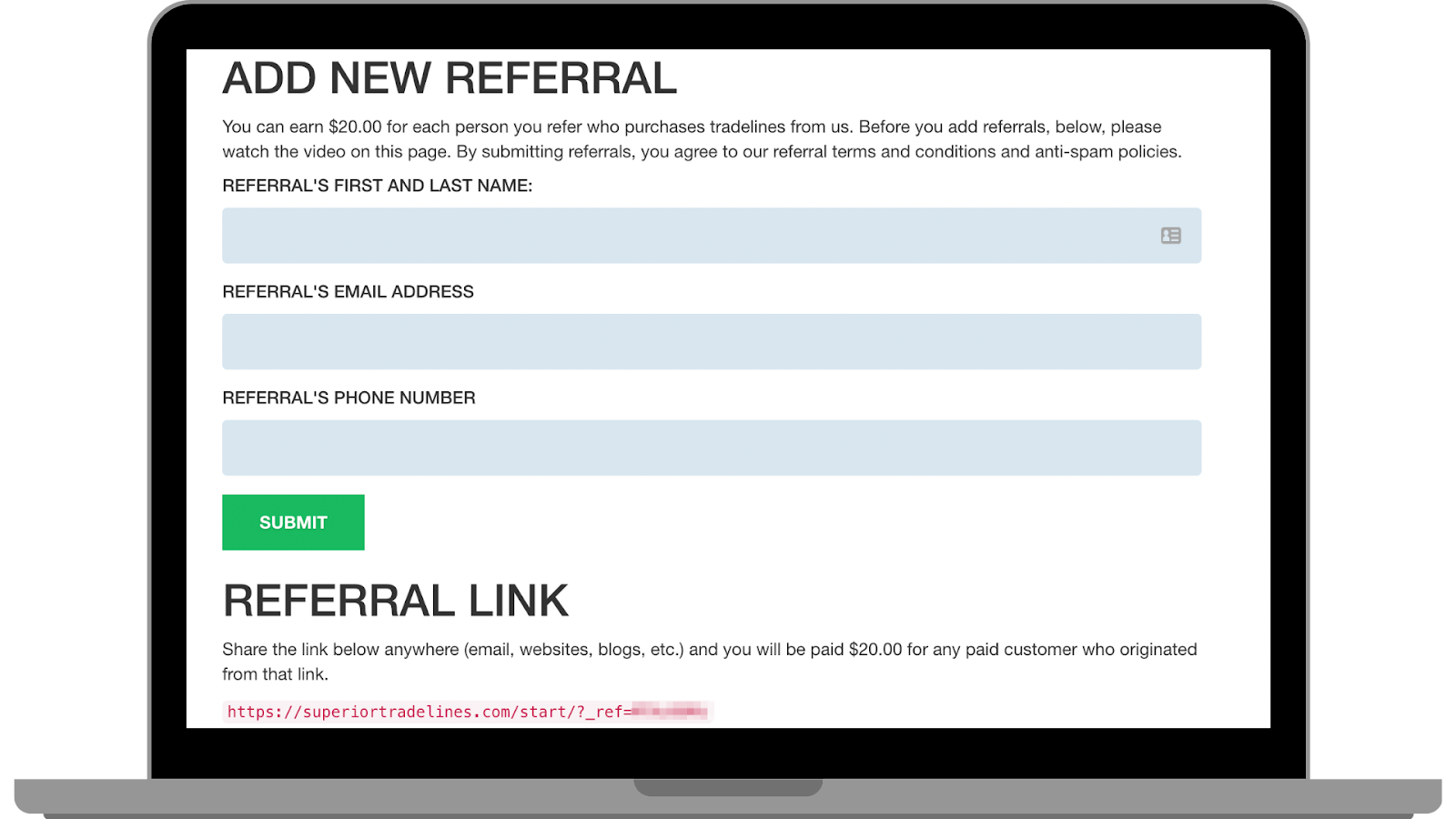

3. Join the referral program

As a Superior Tradelines member, you can earn $20 for each new person you refer who purchases a tradeline through the platform.

4. Get financial education

While Superior Tradelines’ content seems pretty typical to me, their educational resources are boasted across their website and marketing materials. Yes, information is a resource, and so I list it here.

What to Expect When You Become a Superior Tradelines Member

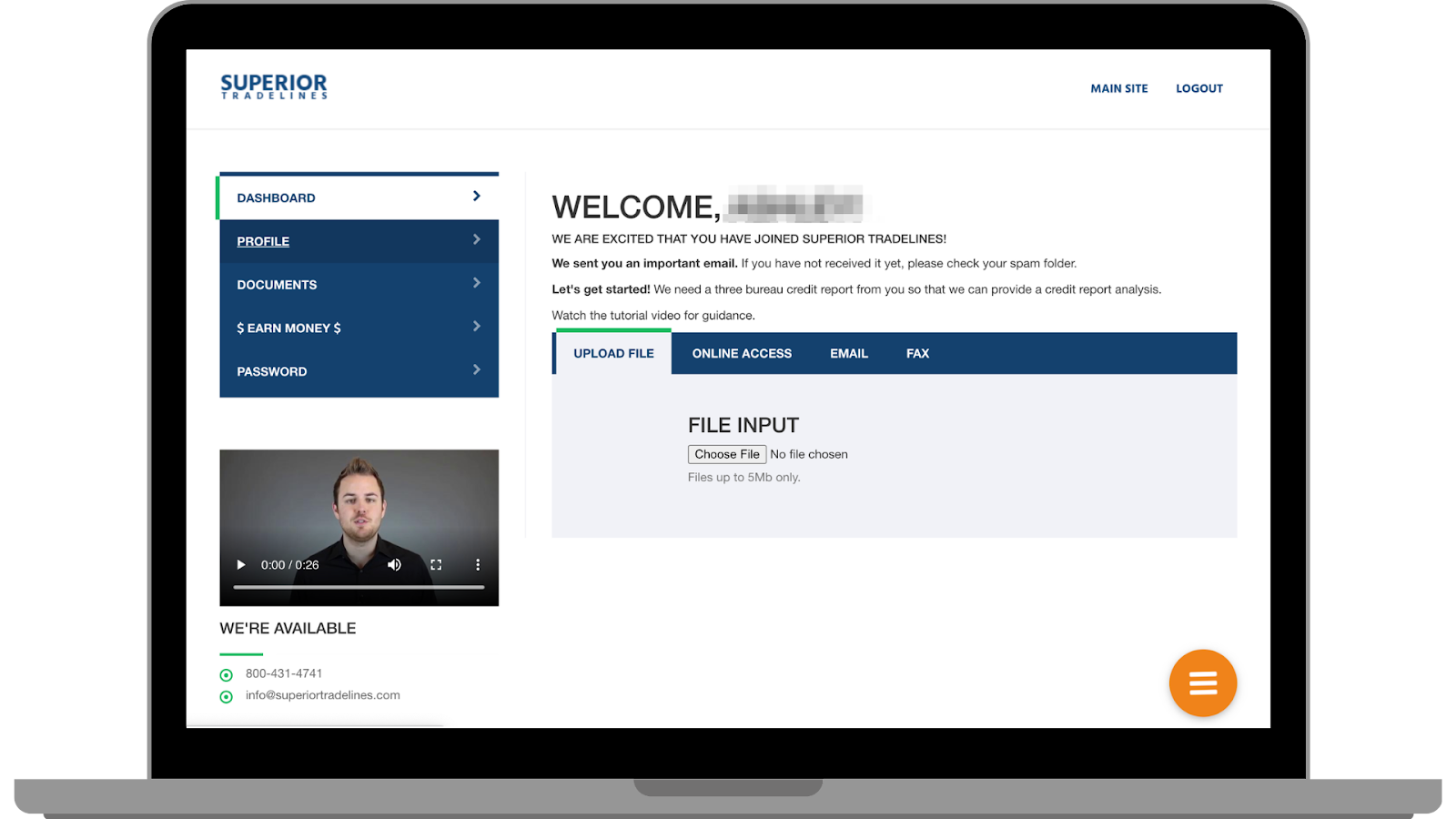

You can sign up for a Superior Tradelines account in just a few clicks. You’ll have pretty much instant access to your online dashboard.

The first step is to submit your three-bureau credit report for review. You can upload the file, provide online access, email, or fax your report.

After your reports have been reviewed, you will be notified whether you are a good candidate for the services, or if you should work on some other form of credit repair first.

If you need to do some work before you add new tradelines to your account (perhaps you have items in collections), Superior Tradelines will likely refer you to someone in their network. My guess is that they’ll direct you to someone in the Credzu network.

| Note: I recommend Credit Secrets, as it’s the best credit repair offer I’ve ever seen. |

After you find out if you’re a good candidate for the offer, you will need to upload identity verification:

- SS card front

- SS card back

- State-issued ID front

- State-issued ID back

- A copy of your recent three-bureau report

- Proof of address

- Any other verification that might be requested

You’ll also get instant access to the referral program. And, once you’re ready to purchase tradelines, you will be guided along in the process. Typically, each tradeline you purchase will cost between $500 and $1,000.

And, the impact to your score should happen by the next reporting date. You may see results in as little as 15 days, but allow up to 45 days for slower reporters.

I did call in to ask about the amount of time that members are able to keep an account on their credit profile, but I was taken to a generic voicemail, and have yet to hear back. What I do know is that the tradelines you purchase may fall off your account in as little as 45 days, but some can stay on your report for years — this probably depends on the lender and the original account owner.

Conclusion

So, is Superior Tradelines a scam? I would say no. In fact, it seems to be a service to boost credit fast by adding your name to an existing tradeline account. However, the fees are a little steep.

Before I refer you to a service like this, I recommend you consider asking someone you trust — like a parent or spouse — to add you to their existing credit account. The results would be the same and you would have a free tradeline.

If that idea fails (or if you don’t know anyone with healthy tradelines), then, by all means, look into Superior Tradelines’ offer. Just be prepared to pay at least $500 per tradeline and to take advantage of the benefits of an increased score right away — before the account falls off your report.

Furthermore, I’m not 100% sure I trust the framework. Anyone whose account you add your name to will have access to at least some of your identifying information. And, sellers are at-risk for closed accounts. If you have high risk-tolerance, explore the offer.

Want to learn how to obtain up to $100K in business credit (separate from your personal credit) with our safe and proven, seven-step framework? Join Business Credit Workshop today.