If you’re diving into the world of real estate investment, you might have come across the Kwak Brothers. Sam and Daniel Kwak are well-known in this space, but you might be wondering whether they’re truly worth your attention.

Here, I explore who the Kwak Brothers are, what they do, and what reviews and other sources say about them to help you decide if they’re a good fit for your investment goals.

This is what’s in store:

- Who are the Kwak Brothers?

- What Do the Kwak Brothers Do?

- Frequently Asked Questions

- Conclusion: Are the Kwak Brothers Legit?

Who are the Kwak Brothers?

The Kwak Brothers, Sam and Daniel, are prominent entrepreneurs, real estate investors, mentors, and authors dedicated to helping you achieve financial peace of mind. They’ve made a name for themselves through their work teaching real estate investing and personal finance.

Their companies include:

- Accelerated Banking, which helps homeowners pay off their mortgages faster using a proprietary strategy.

- The Passive Income Mastery Program that coaches new investors to help them achieve substantial monthly income in a short period.

- IBC Jumpstart, which offers an educational approach to financial independence through life insurance products.

Their expertise is widely-shared through social platforms like YouTube, where they provide valuable insights. They also host live speaking engagements where they motivate and educate prospective investors and those who want to increase their net worth.

In this case, “real estate investment” refers to a focus on raising capital and acquiring rental properties through owner financing—They also offer training on how to implement these strategies effectively.

Beyond investing, they serve as mentors, specializing in personal finance and real estate to help individuals secure a stable financial future.

You might also like: A Credit Stacking Breakdown: What it is & How it Works

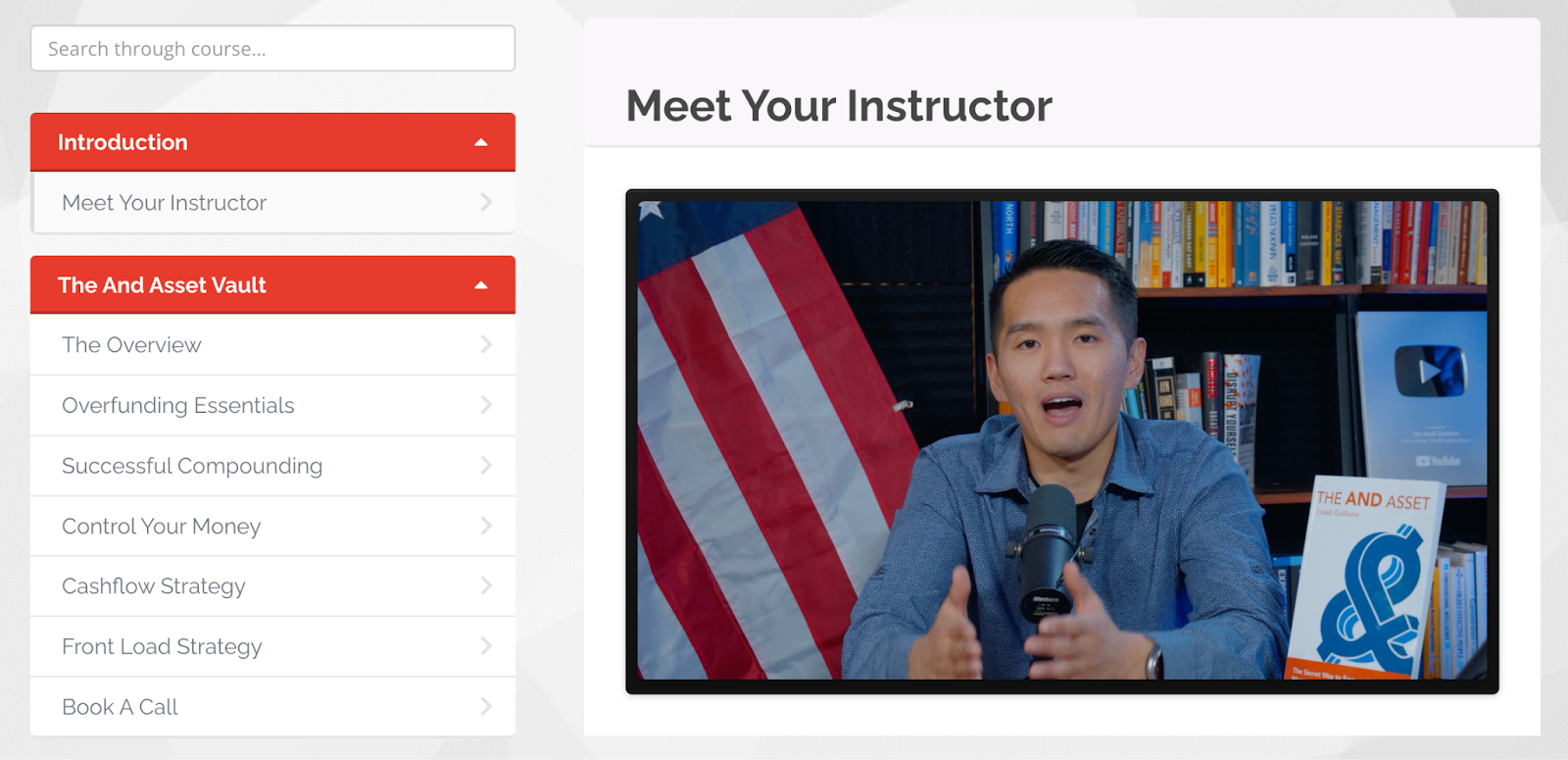

Who is Sam Kwak?

Sam Kwak is a prominent real estate investor and frontman of The Kwak Brothers. Before his career, he prioritizes being a devoted Christ-follower, father, and husband. Based in Chicago, Sam and his brother Daniel manage a real estate portfolio worth over $4.5 million.

Sam’s entry into real estate was sparked by a desire for financial freedom, and inspired by Rich Dad Poor Dad—He started by volunteering for a local investor, which he views as a shortcut to success. His first major deal came through social media, where he used owner financing to acquire a portfolio of single-family homes.

In 2017, Sam experienced significant growth, expanding his rental properties from zero to 75 units in just one year. His success is attributed to effective capital raising and seller financing. Sam also leverages his marketing and technology background to help property managers automate their businesses.

Sam’s YouTube channel, which was initially a real estate resource, now has over 780 videos and 348K followers. The Kwak Brothers channel now also includes political commentary, aimed at a conservative audience while subtly introducing real estate concepts.

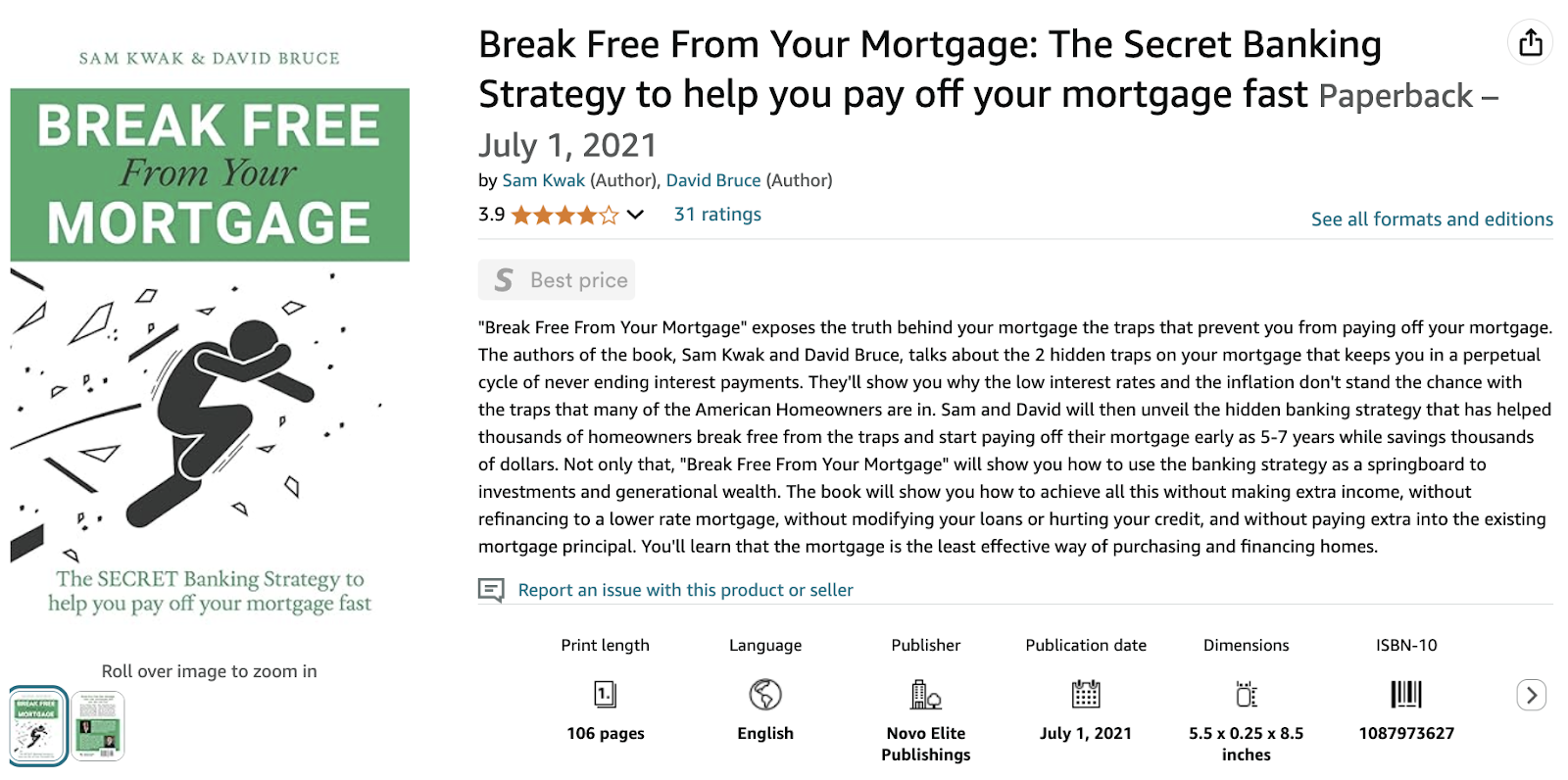

Sam Kwak has co-authored at least one book. Break Free From Your Mortgage: The Secret Banking Strategy to Help You Pay Off Your Mortgage Fast by Sam Kwak and David Bruce reveals hidden traps in mortgages that keep homeowners in a cycle of endless interest payments. The book introduces a banking strategy that promises to help you pay off your mortgage in as little as 5-7 years without extra income, refinancing, or modifying loans.

Reviews on the book are mixed, and it has a 3.9-star rating overall. Some readers appreciate the powerful financial insights, while others feel the book focuses too much on upselling the authors’ services.

Recommended: 9 Best Business Credit Books Worth Reading

Who is Daniel Kwak?

In addition to co-managing The Kwak Brothers’ ventures, Daniel Kwak is the founder and Chief Investment Officer (CIO) of Miotti Partners Capital. Founded by Daniel at 26, Miotti Partners Capital is a core-satellite fund that pioneered the equities fund management model in the real estate industry.

His role at Miotti Partners Capital involves overseeing investments and building strategic relationships, complementing his responsibilities within The Kwak Brothers.

Daniel’s focus on raising capital and fostering relationships has been instrumental in the growth of their real estate ventures. Like his brother Sam, Daniel is deeply involved in both real estate investment and education.

Their partnership leverages Daniel’s strengths in capital raising and networking, while Sam focuses on marketing and systematizing their operations. Their combined efforts have established a robust platform for educating and empowering others in the realm of real estate investing.

Recommended: How to Get Money for Real Estate Investing: 18 Practical Ideas

Company Overview

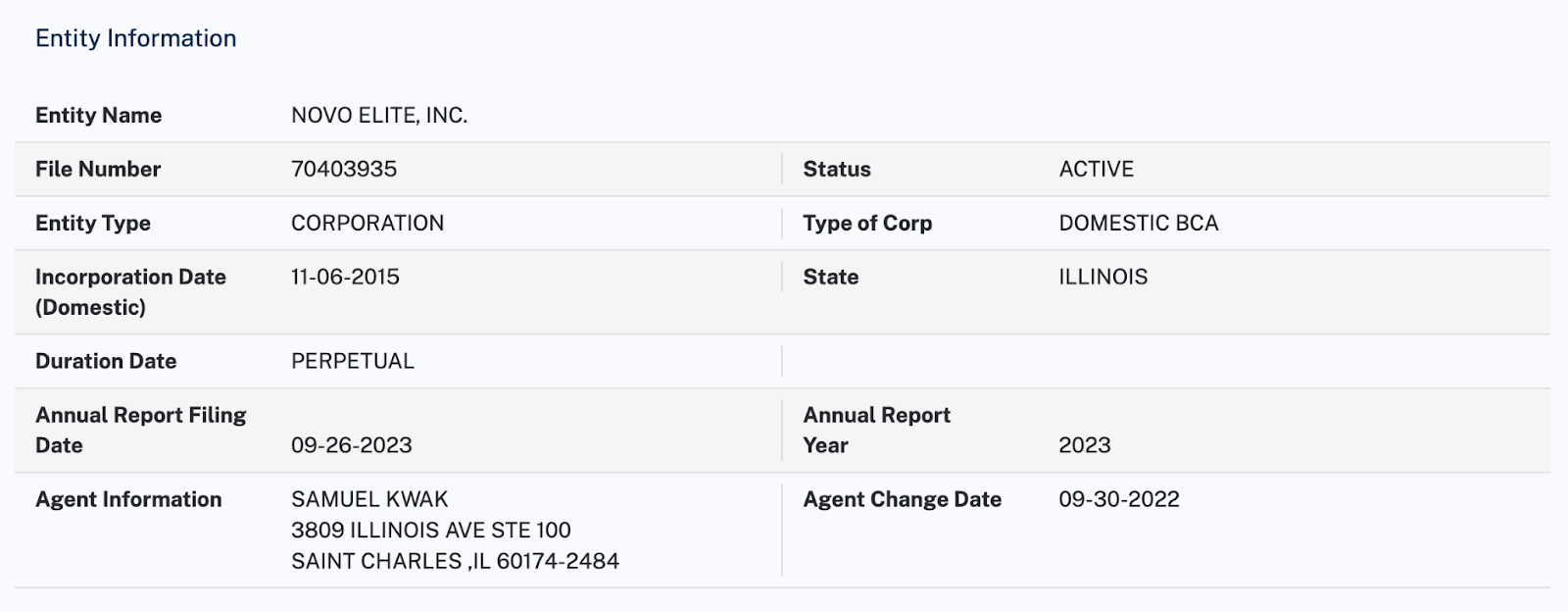

While brothers began their real estate venture over a decade ago, Novo Elite Inc., the company doing business as The Kwak Brothers, is an Illinois-based corporation that’s been around since 2015, and is officially registered to Samuel Kwak. The company is active and in good standing with the Office of the Illinois Secretary of State.

Over the past decade, the business has evolved to offer a range of educational resources and services aimed at aspiring investors—They’ve maintained a strong presence in the real estate field for several years, continuously updating their content and services to reflect current market trends.

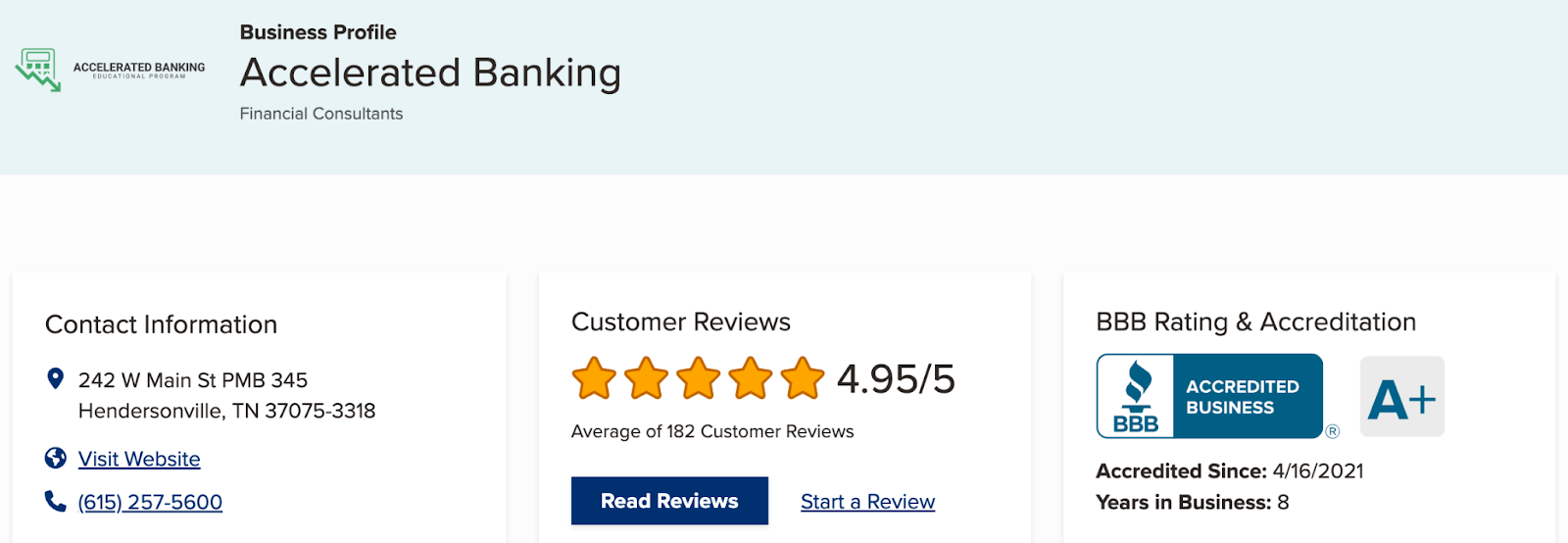

Reviews on sites like the Better Business Bureau (BBB) are mostly positive. A majority of clients find their advice and training beneficial, while a few express concerns about the value and effectiveness of their offerings.

At any rate, they run a real business, registered and in good standing across the board. And, I couldn’t find any major complaints or lawsuits against Novo Elite, which is a good sign.

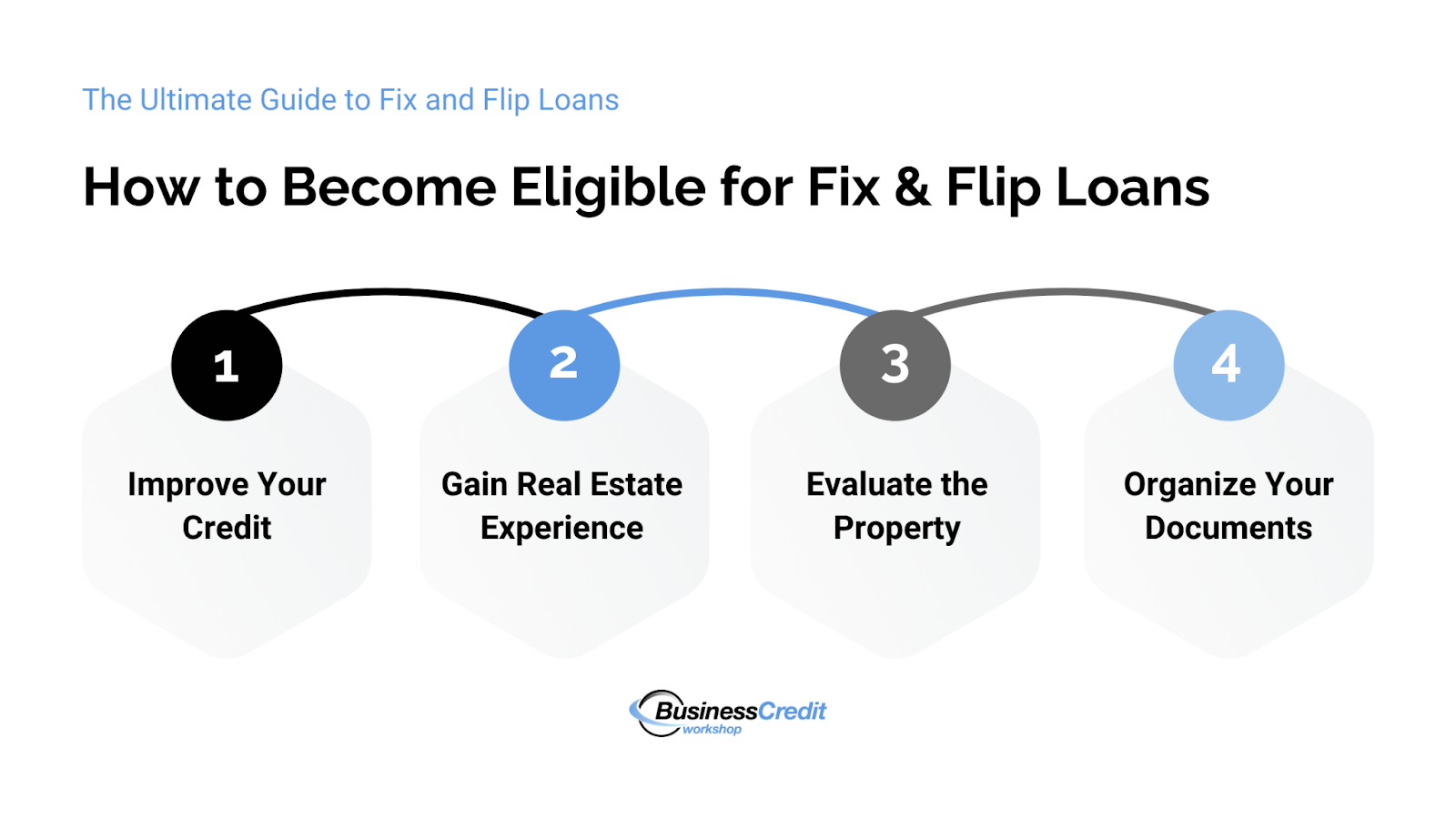

You might also like: The Ultimate Guide to Fix and Flip Loans: Fund Your Next Venture

What Do the Kwak Brothers Do?

The Kwak Brothers offer several services designed to help individuals succeed in real estate investing and financial management. Here’s a closer look:

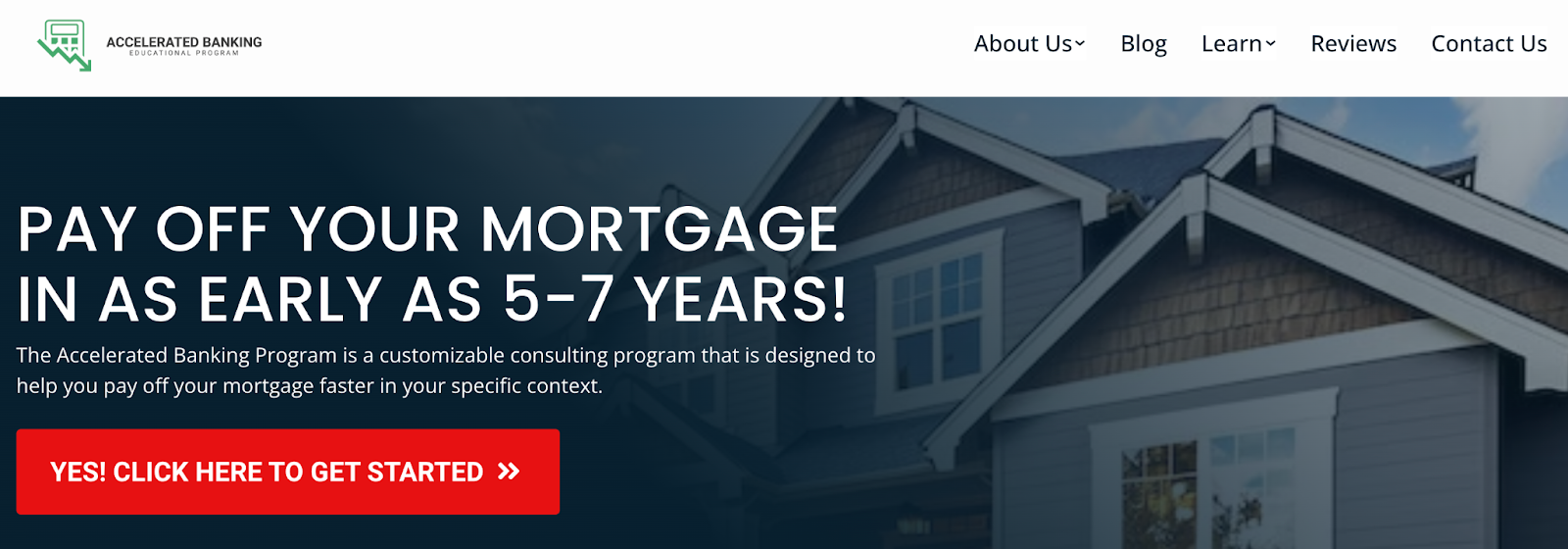

1. Learn to Pay Off Your Mortgage Early

The Kwak Brothers’ key offer is a program called Accelerated Banking—the value proposition is that you can pay off your mortgage in five to seven years. Accelerated Banking promises a practical way to pay off your mortgage early using a Home Equity Line of Credit (HELOC). It’s run by Sam and Daniel Kwak and David Bruce (co-author of Break Free From Your Mortgage). Allegedly, the group has a combined 70 years of investment experience.

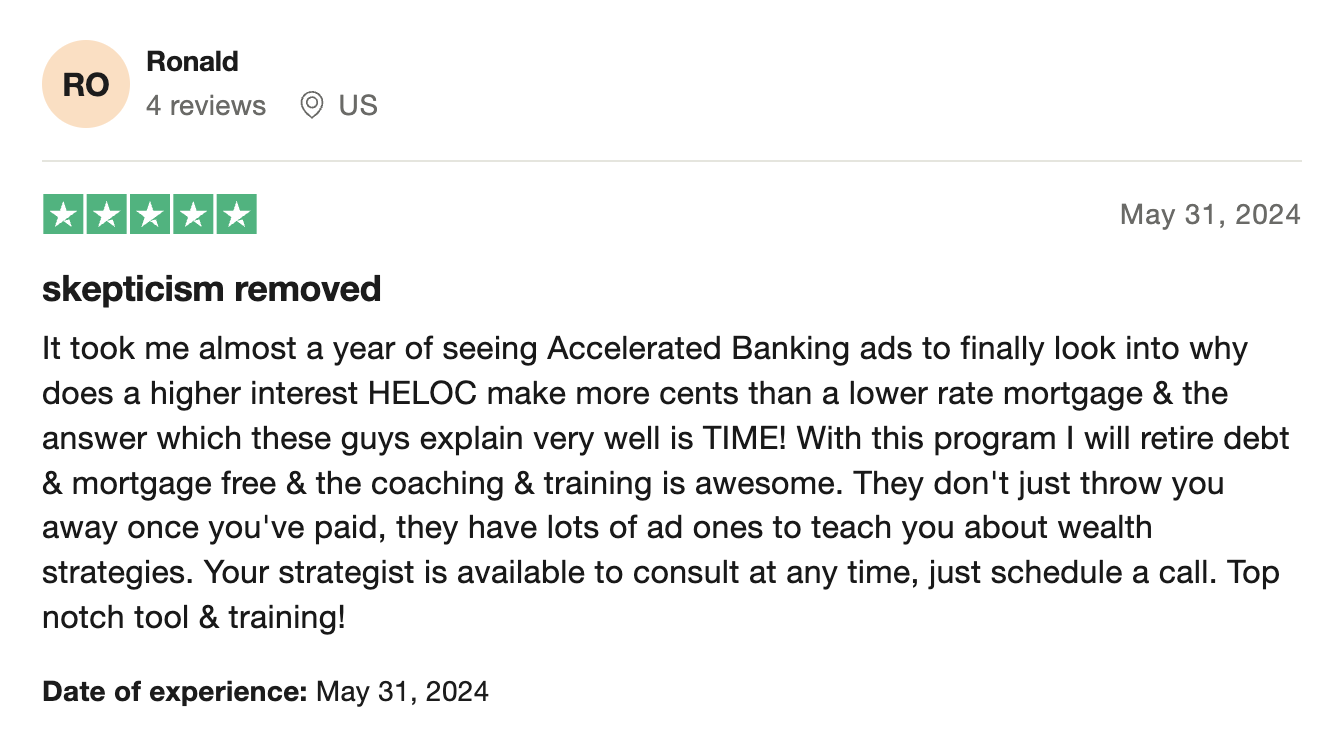

According to real user reviews, students seem to learn how to use HELOCs to reduce their mortgage term, manage their finances better, and save significantly on interest payments—Reviewers mention the program’s detailed guidance, personalized strategies, and accessible educational resources.

So, you should be able to expect a tailored approach that aligns with your financial goals, ongoing support from knowledgeable advisors, and a community of like-minded individuals all working towards financial freedom.

Accelerated Banking’s facebook page has 1.2K followers and a bit of engagement on their posts. Their free webinar introduces what they will teach in their training. And, rather than paying off your mortgage in five to years, the cited results are actually of people who cut five to seven years off their mortgages.

My first impression in that the offer is a bit misleading, but still could be valuable.

Recommended: The BRRRR Method: A Real Estate Portfolio-Building Blueprint

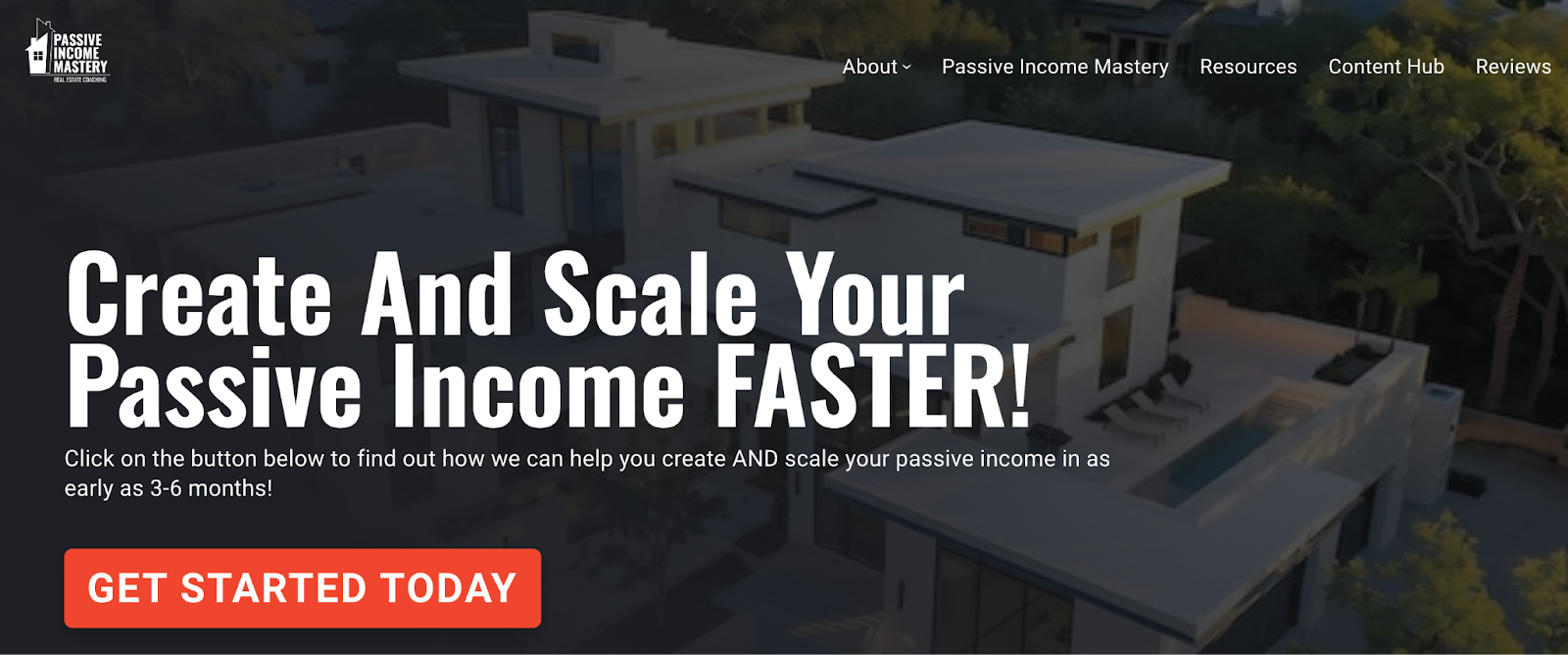

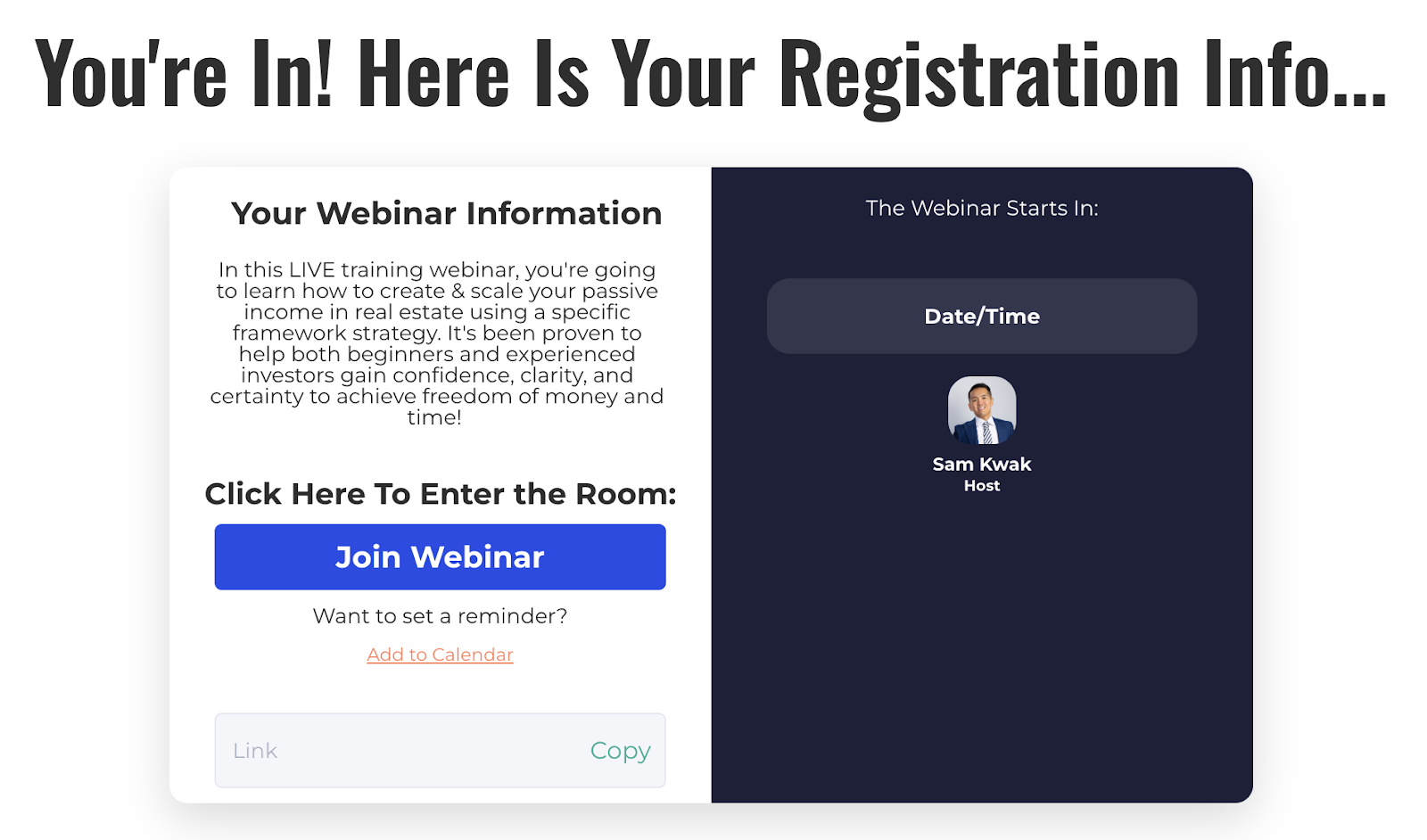

2. Create and Scale Your Passive Income

Passive Income Mastery promises hands-on coaching, an inspirational community, and virtual education to help you achieve your real estate goals. According to trainee reviews, students find the coaching effective and appreciate the supportive community—They feel empowered by the expert guidance and resources available.

When you join, as with Accelerated Banking, you can expect personalized coaching, access to proven strategies, and a network of like-minded individuals working toward financial freedom through real estate investing.

The program starts with a free training webinar that covers:

- Creative financing ideas

- How to fund down-payments owner financing

- How to create your passive income stream

I popped into the webinar myself, and I didn’t like that it was set up to appear like a “live training” with over 100 viewers (Passive Income Mastery’s Facebook page only has 260 total followers). I could tell the training was pre-recorded and that Alonzo T and Britt P were fake viewers—And, I don’t love a lack of transparency.

Be that as it may, the webinar did provide a solid intro to what the training should cover, and it was completely free to check out.

You might also like: Read This Before You Hire a Business Credit Coach [Quick Guide]

3. Learn the Infinite Banking Concept

The Kwak Brothers’ IBC Jumpstart is a deep dive into the infinite banking concept (IBC). IBC is a financial strategy that uses whole life insurance policies to create your own personal banking system.

Originally coined by Nelson Nash, the IBC lets you borrow against the cash value of your life insurance instead of going to a bank for loans—This way, you can finance big expenses, like buying a car or starting a business, while your policy continues to grow. The idea is to build wealth with your policy’s cash value, which you can access tax-free and pay back on your schedule.

IBC Jumpstart offers free access to their Infinite Banking Masterclass. This includes a 6-video course to teach you how to manage your finances by becoming your own bank. After completing the course, you can schedule a one-on-one consultation with a wealth coach to set up your IBC policy.

The aim of the masterclass is to help you understand and implement the Infinite Banking Concept for better financial control.

You might also like: Complete Guide to Small Business Insurance in New Jersey

Frequently Asked Questions

Who are the Kwak Brothers?

Sam and Daniel Kwak are well-known for their work in real estate and financial education. They focus on providing training, coaching, and resources to help individuals achieve financial success through real estate investment.

What is the Kwak Brothers’ net worth?

Exact figures on their net worth are not publicly available. However, they are recognized as successful entrepreneurs in the real estate sector, with at least $4.5 million in combined real estate holdings.

What do the Kwak Brothers reviews say?

Reviews about the Kwak Brothers are mostly positive. Some people appreciate their detailed advice and practical tips, while the minority question their marketing practices and the effectiveness of their programs.

Conclusion: Are the Kwak Brothers Legit?

The first thing I will say that I don’t love about these offers is that it’s very difficult to find the pricing for all of the Kwak Brothers’ offers. Moreover, their training intros are slightly misleading.

With that said, The Kwak Brothers have made a significant impact in real estate and financial education. They offer a few different resources and services aimed at helping you succeed. While they have a notable online presence and their reviews are resoundingly positive, I’m on the fence with this one.

If you’re thinking about signing on to one of the Kwak Brothers’ offers, research thoroughly, weigh the feedback from different sources, and determine if their approach aligns with your investment goals.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days so you can invest in your financial future? Join Business Credit Workshop today!