In the vast landscape of financial institutions, credit unions like Oregon Community Credit Union stand out for their unique approach to serving members—Unlike big banks, credit unions are not-for-profit cooperatives owned by their members, prioritizing their financial well-being over profit.

This member-focused philosophy translates into tailored solutions and personalized service, making credit unions a popular choice for businesses seeking a more personalized banking experience. In this review, we’ll delve into Oregon Community Credit Union, with a spotlight on business credit cards, loans, and other products specifically designed to meet the needs of small businesses.

Let’s explore how credit unions like OCCU can help businesses thrive in today’s competitive landscape.

This is what’s in store:

- What is Oregon Community Credit Union?

- Business Financial Products & Services

- OCCU Customer Service

- OCCU Community Involvement

- Conclusion

Now, let’s get into it!

What is Oregon Community Credit Union?

Oregon Community Credit Union (OCCU) is a not-for-profit financial cooperative owned by its members and based in Oregon and Washington. It all started with a bunch of Oregon state employees who pooled their cash into a shoebox in Eugene, Oregon. From those humble beginnings, OCCU has grown while sticking to the credit union philosophy of “people helping people”

This means they reinvest their profits back into:

- Their members

- Their operations

The communities they serve

Reinvestment of profits leads to lower fees, higher savings rates, and lower loan rates.

OCCU is big on supporting small businesses—They offer a range of business banking services tailored to fit the needs of different businesses.

They’ve got traditional business accounts, which include checking accounts that can grow with your business, no-fee trust accounts for lawyers, and nonprofit accounts that let you focus on your impact without worrying about fees and minimum balances.

If you’re looking to save, they’ve got great rates on business savings and money market accounts.

When it comes to lending, OCCU is there for small businesses with competitive rates and low fees on business loans and lines of credit. Need to finance a vehicle or some new equipment? They make that process quick and easy too. Plus, they offer the OCCU Business Visa® Credit Card, which helps you manage expenses, earn rewards, and protect your purchases.

Recommended: 3 Best Credit Unions for Small Business Banking

OCCU Locations Served

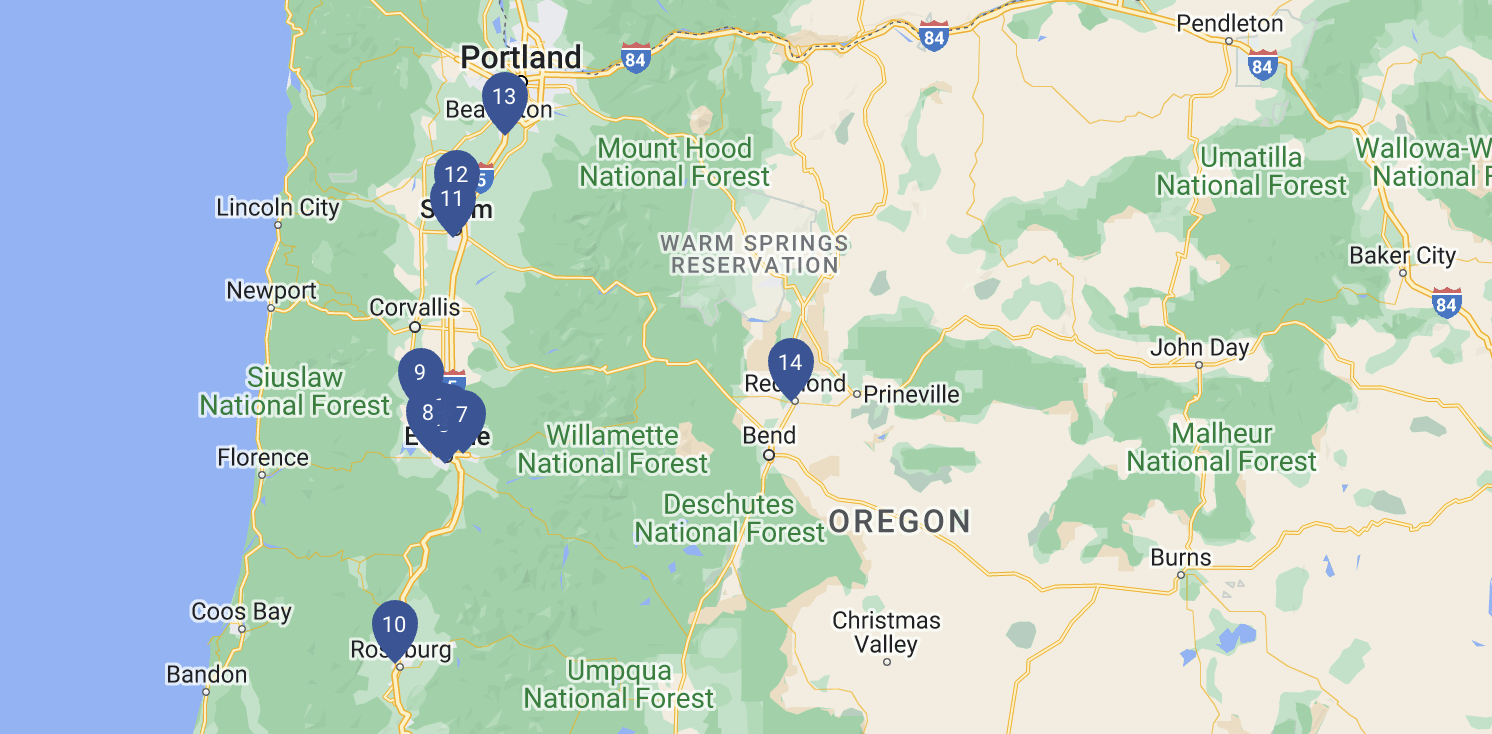

OCCU serves businesses primarily in Oregon and Washington, with a network of branches and ATMs in key locations like Eugene, Springfield, Junction City, Keizer, Redmond, Roseburg, Salem, and Wilsonville. Each branch provides essential services like video tellers and enhanced ATMs, which means extended hours and 24/7 access for deposits, withdrawals, and loan payments.

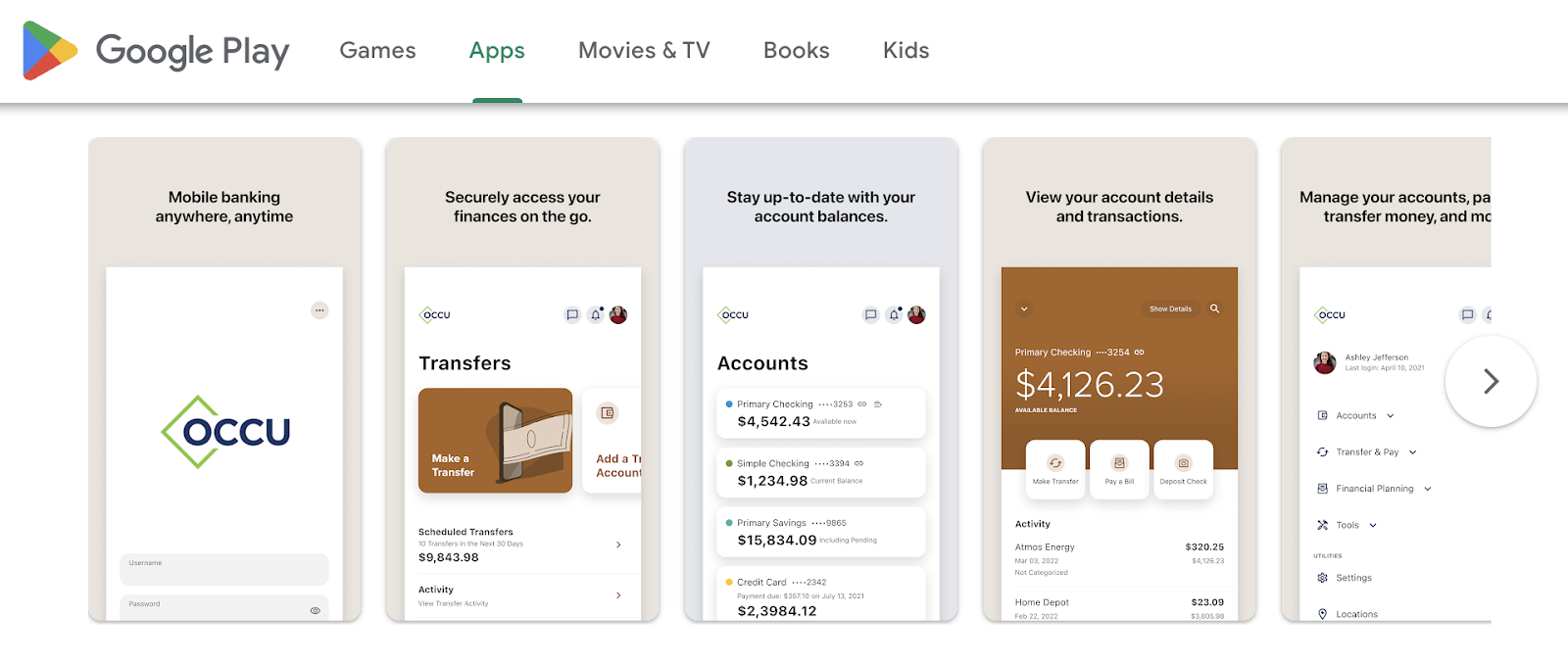

MyOCCU Online & Mobile Banking enables you to do a lot from your computer or mobile device:

- See your balance

- Browse transactions

- Pay bills

- Transfer funds

- Download statements

- Deposit funds

- Apply for loans and credit

These online tools ensure that OCCU business members have convenient access to their accounts and financial services nationwide, making banking easy and accessible no matter where you are.

You might also like: Business Credit Report – Run a Free Company Search with Experian

OCCU Membership & Eligibility

To become a business member of OCCU, your business needs to meet certain eligibility criteria—If your business is located in one of the 67 counties in Oregon or Washington, you’re eligible to join. Additionally, if you or your business partners are immediate family members of an existing OCCU member, students or employees of the University of Oregon, employees or members of Bi-Mart, or employed by the State of Oregon, you can join.

The process to join OCCU as a business member is straightforward:

- Visit the OCCU website and navigate to the membership section.

- Fill out the online application form with your business details and personal info.

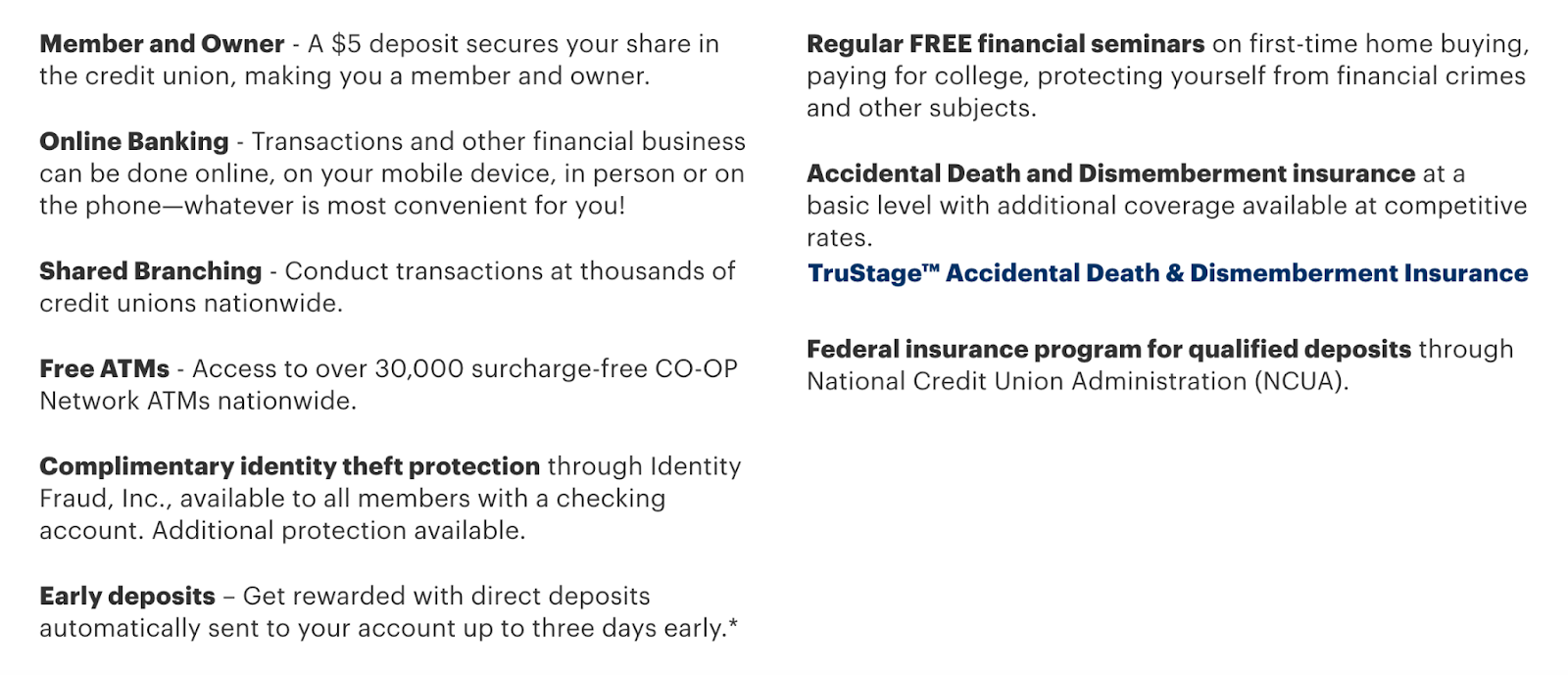

- A $5 deposit secures your share in the credit union, which makes you a member (and owner).

- Submit your application.

OCCU will review your application and verify your eligibility…You might need to provide additional documentation during this step.

Once you’re a member, you can access a wide range of OCCU’s products and services. And, you can take advantage of shared branching, which lets you conduct transactions at thousands of credit unions nationwide.

If you join, you can also enjoy:

- Access to over 30,000 surcharge-free CO-OP Network ATMs nationwide.

- Complimentary identity theft protection through Identity Fraud, Inc., with additional protection available.

By becoming an OCCU member, your business gains access to valuable financial products and services, as well as numerous benefits designed to enhance your financial security and convenience.

You might also like: 14 Best Credit Monitoring Services for Scores, Reports, & ID Theft Protection

Business Financial Products & Services

The benefits are really selling the credit union. But, as a business, you need to make sure that your institution offers everything you need. From business checking to credit cards and treasury services, here’s what you can expect from OCCU.

1. Diverse Business Checking Accounts

OCCU offers three business checking account options tailored to fit the diverse needs of local businesses:

- Launch Business Checking

- Thrive Business Checking

- Optimum Business Checking

With all OCCU business checking, you may be eligible for a $2 discount on monthly service fees with eStatements.

Launch Business Checking is ideal for new businesses or those with limited transactions. You’ll have no monthly service fee when maintaining a $1K minimum balance. And, your first 250 transactions and up to $5K in cash deposits per month are complimentary.

Next, Thrive Business Checking is designed for growing businesses that want interest earnings. There’s no monthly service fee if you maintain a $3K minimum balance. Plus, your first 500 transactions and up to $15K in cash deposits per month are complimentary.

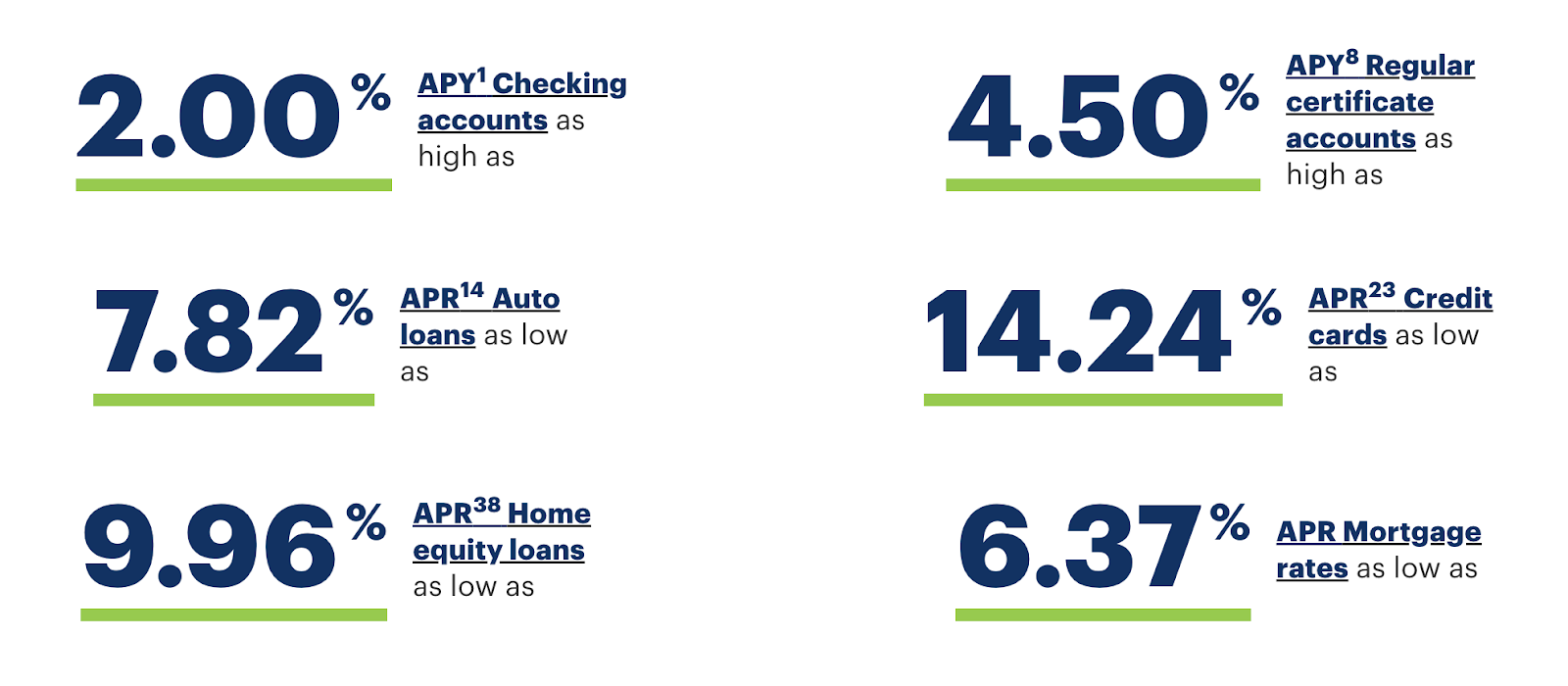

Finally, the Optimum Business Checking account is suited for established businesses that aim for higher earning potential. It offers a competitive 0.45% APY on balances and low monthly service fee of $16. This account features “itemized fees,” which ensures you only pay for the services you use.

You might also like: Amex Business Checking Review: What You Need to Know…Really

2. Interest on Lawyers’ Trust Accounts

The Interest on Lawyers’ Trust Accounts (IOLTA) Checking offered by OCCU provides law firms with a hassle-free way to manage client funds.

Here’s a quick overview of its features:

- No monthly fees

- Unlimited transactions

- Competitive interest rates

- $100 minimum opening balance

These accounts allow legal professionals to to focus on serving your clients without worrying about account maintenance costs. You can conduct an unlimited number of check and ACH transactions, providing flexibility in managing client funds. And, you’ll earn competitive interest rates on the funds held in the account, ensuring that client funds work for them while awaiting distribution.

The minimum opening balance of $100 makes the IOLTA account accessible for law firms of various sizes.

By choosing IOLTA Checking, you contribute to a public service program that helps provide legal assistance to those in need. The interest generated from this account supports access to legal services for individuals and communities, which aligns with their philosophy of “people helping people.”

You might also like: Everything You Need to Know About a DUNS Number – and Why You Should Care

3. Specialized Non-Profit Banking

OCCU offers nonprofit banking services designed to support organizations dedicated to community betterment. I’ll give you a quick summary.

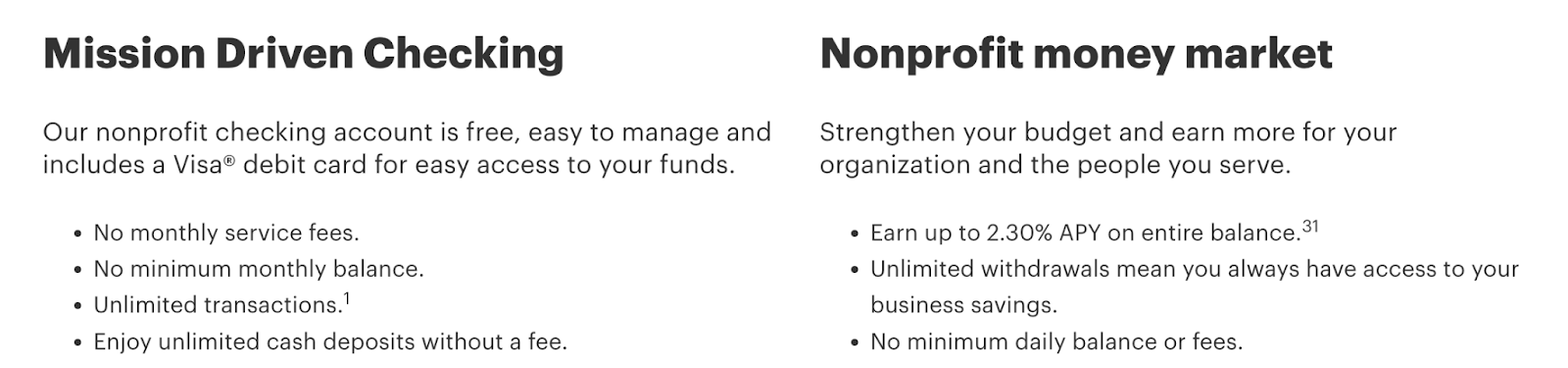

Their Mission-Driven Checking includes:

- No monthly service fees or minimum balance requirements

- Unlimited transactions and cash deposits at no extra cost

- Includes a Visa® debit card for convenient access to funds

- Easy account management through MyOCCU

And, the Nonprofit Money Market account offers:

- Competitive interest rates of up to 2.30% APY on the entire balance

- Unlimited withdrawals for easy access to funds

- No minimum daily balance or fees

These services empower nonprofit organizations to strengthen their financial foundations while continuing to make a positive impact on their communities.

You might also like: Low-Risk NAICS Codes +Best SIC Codes for Business Credit

4. The OCCU Business Visa® Credit Card

The OCCU Business Visa® Credit Card offers businesses a suite of features designed to streamline expense management and enhance financial flexibility.

With this card, you can get:

- Competitive interest rates ranging from 15.24% to 22.24% APR

- Rewards points for cash back, merchandise, travel, and gift cards

You can easily track expenses and cash flow online, ensuring efficient management of your business finances. Security features, including Visa’s Zero Liability Policy and Purchase Security, provide peace of mind against unauthorized charges and protect purchases from theft or damage.

You can redeem rewards points online or by phone, with no expiration date for accrued points. Additional benefits include no monthly account service fees, unlimited transactions, and access to MyOCCU Online & Mobile banking for seamless account management.

Recommended: Corporate vs Business Credit Card: What’s the Difference?

5. OCCU Business Loans & Lines of Credit

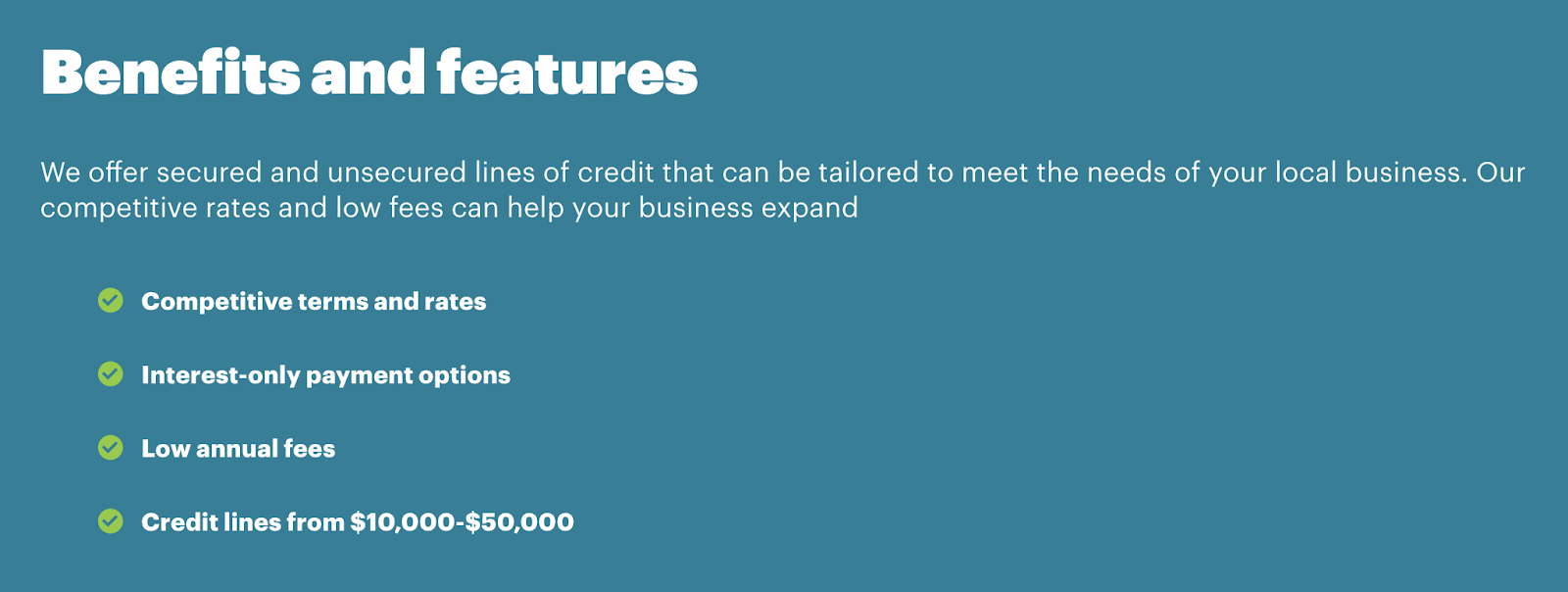

OCCU offers flexible lines of credit designed to support the financial needs of local Oregon businesses.

These lines of credit come with several benefits and features:

- Credit lines ranging from $10K to $50K

- Secured and unsecured options available

- Competitive interest rates and low fees

- Interest-only payment options

They also offer business vehicle and equipment loans—Whether you need a new delivery van or essential equipment, they’ve got you covered. With options for new or used vehicles and equipment, terms up to 84 months, loan amounts ranging from $10K to $250K, and just a $100 origination fee, they can help you get the wheels turning on your business.

Recommended: 6 Best Business Credit Cards for Entrepreneurs: Fuel Your Growth

6. OCCU Business Savings & Investment Opportunities

OCCU offers a range of business savings options designed to help businesses achieve their financial goals while providing low fees, competitive interest rates, and exceptional member service. Here’s a breakdown of their business savings products.

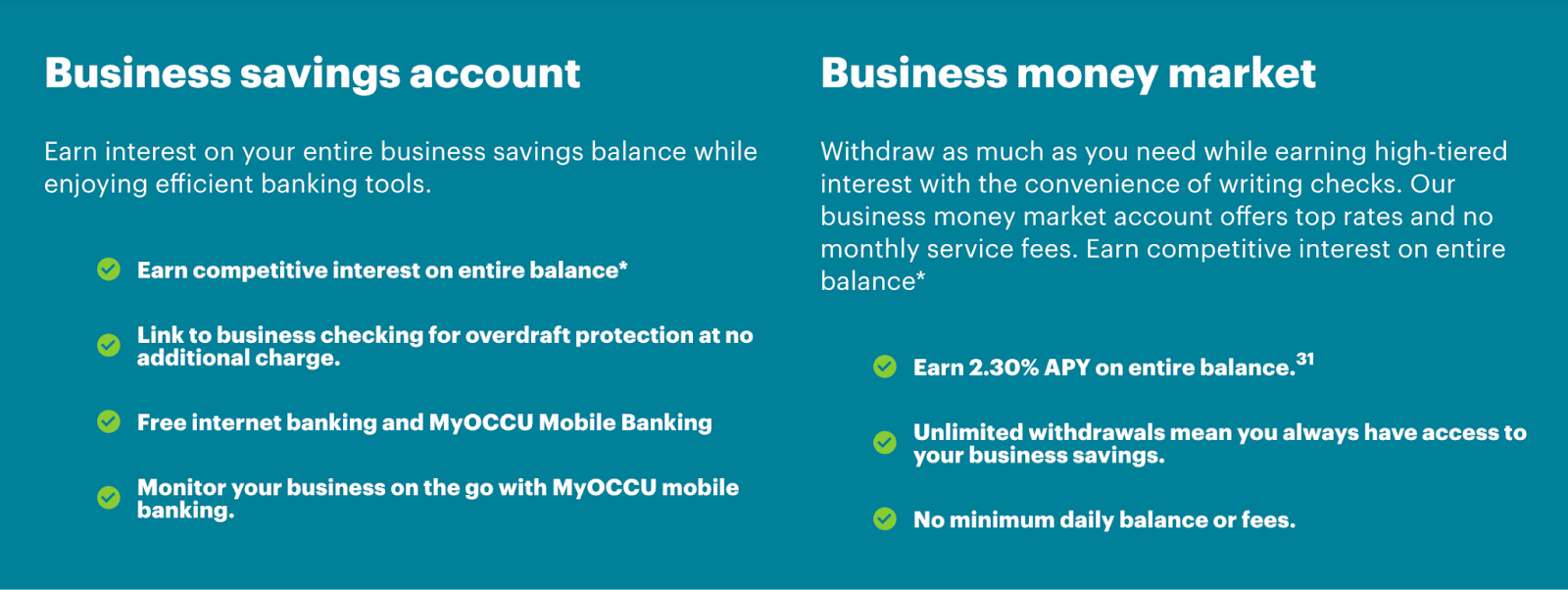

With OCCU’s Business Savings Accounts, you can:

- Earn competitive interest on your entire balance

- Link your business savings account to your checking account for overdraft protection at no additional charge

- Enjoy free internet banking and MyOCCU Mobile Banking

Next, the Business Money Market enables you to:

- Earn a high-tiered interest rate of 2.30% APY on your entire balance

- Benefit from unlimited withdrawals

- Maintain no minimum daily balance

- Pay no monthly service fees

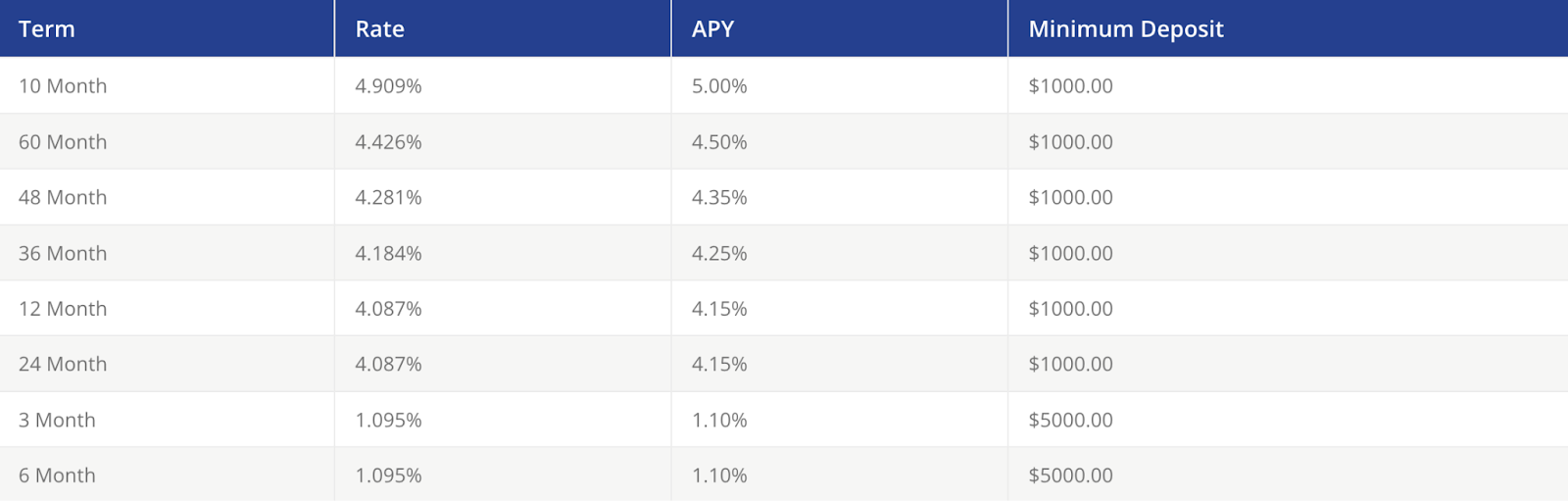

And Business Certificates come with:

- Interest rates that are typically higher than standard savings or money market accounts

- Fixed rates and terms ranging from six months to 60 months

- Flexible maturity options

- “Relationship pricing” on 24-month certificates

The option for bump-up certificates allows you to increase your rate once per product per term to match any rate offered by OCCU.

With OCCU’s business savings options, you can maximize your savings potential while benefiting from flexible terms, competitive rates, and convenient account management features.

You might also like: Is the National Debt Relief Program Legit? The Honest Answer

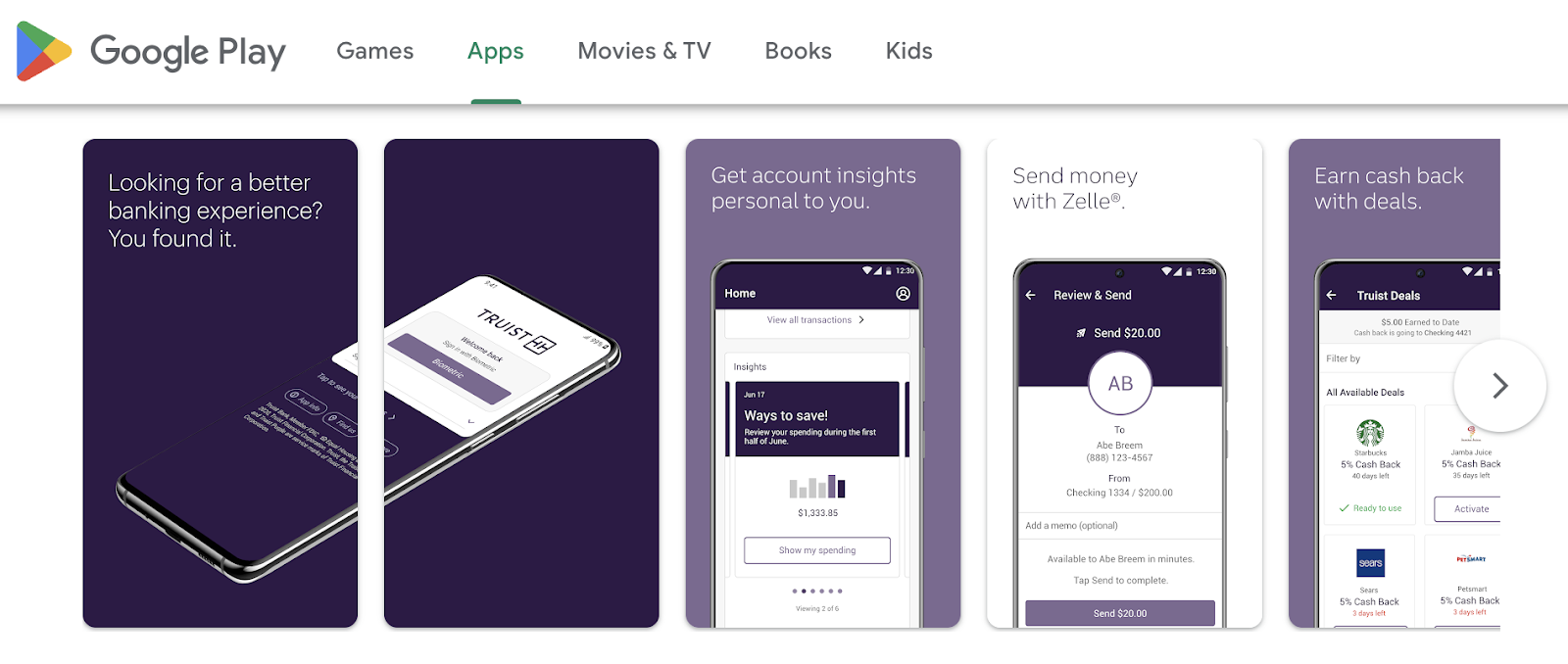

7. The MyOCCU Mobile App

The MyOCCU Mobile Banking app gets a solid 4.8-star rating, showing folks generally like it. Users dig its updated look and features, making banking easier on the go. They especially like zipping money between accounts and settling bills with a few taps. The Snapshot feature is a hit too, letting you check balances in a flash.

But, there are occasional hiccups, like slow loading or bugs with stuff like mobile check deposits. Despite these, it’s still a handy tool for managing finances on your phone.

You might also like: The PEX Card: Is it the Best Corporate Card for Your Business?

OCCU Customer Service

Oregon Community Credit Union (OCCU) offers robust customer service for its business members, with dedicated support channels tailored to their needs. Business members can contact OCCU’s call center during extended hours on weekdays and even on Saturdays, ensuring accessibility to assistance when it’s needed most.

Additionally, there are specialized lines for credit and debit card inquiries, including reporting lost or stolen cards, providing swift resolution to security concerns—The option to send secure messages through MyOCCU Online & Mobile is available for account-related queries, prioritizing confidentiality and convenience.

You might also like: Can Tradeline Supply Reviews Be Trusted? The Full Picture

OCCU Community Involvement

While OCCU prioritizes helping its members, you don’t have to join to cash in on their resources and advice. First of all, the credit union has a library of financial info in their learning center/blog. From starting a business to sales and marketing, they share lots of advice to help you get off the ground…right on their website.

These types of resources are invaluable for the community at large, but are just a supplement to what OCCU does in the community.

Oregon Community Credit Union (OCCU) demonstrates its commitment to the community through various initiatives, including hosting an annual ‘Shred Fest’ event aimed at preventing identity fraud by offering free document shredding services to the public. This event underscores OCCU’s dedication to promoting safety and security for its members and the community at large.

Additionally, OCCU recently tested a four-day workweek for call center employees, leading to increased staff productivity and satisfaction, showcasing its commitment to fostering a positive work environment.

The credit union’s broader community involvement reflects its dedication to social responsibility and supporting local needs.

You might also like: A Full Skip Review: Business Grants, Funding, & More

Conclusion

OCCU doesn’t advertise any treasury services or payment processing solutions. But, they do offer pretty much everything else you could ask for with a business banking experience. And, their rates are better than you would probably expect to get from any big bank.

They’ve got some sweet perks for business members—They offer different checking accounts with interest-bearing options like Lawyers’ Trust Accounts, perfect for managing client funds hassle-free. If you’re a non-profit, they’ve got specialized services just for you, too.

And, when it comes to borrowing, OCCU’s got competitive loans and lines of credit—Their Business Visa® Credit Card even comes with rewards points and cool security features to keep your transactions safe.

Oh, and customer service seems solid, with extended hours and dedicated support lines just for you. So, if you’re looking for a credit union that’s got your back and cares about the community, OCCU could be the place to be!

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!