Starting a business is no small feat, especially when you want to hit the ground running with a company that already has some history. Aged shelf corporations can be a shortcut to many goals. They almost instantly give you an established entity with credibility that can speed up access to business credit.

If you’re on a budget, you might be looking for shelf corporations under $500. This guide will explore these affordable options, answer common questions, and touch on some caveats you should think about.

This is what’s in store:

- How Much Does a Shelf Corporation Typically Cost?

- Is Buying a Shelf Company Worth It?

- How to Choose the Right Shelf Corporation Under $500

- 1. Check the Age of the Shelf Corporation

- 2. Verify Compliance Status

- 3. Review the State of Incorporation

- 4. Examine the Name of the Corporation

- 5. Check Financial History and Liabilities

- 6. Look for Additional Services and Features

- 7. Confirm the Legal Structure and Fit

- 8. Research the Seller’s Reputation

- Frequently Asked Questions

- Conclusion

Now, let’s dive in.

How Much Does a Shelf Corporation Typically Cost?

The price of a shelf corporation can vary, much like vintage items—Prices can range from a few hundred bucks up to $10K, so it’s super important to do your research.

Several factors influence the cost of a shelf corporation:

- Older shelf corporations usually come with a higher price tag because of the corporate history.

- The state where the company is registered also affects the cost—Some places have higher fees and maintenance expenses while some have more corporation-friendly laws than others.

- Pricing can vary based on additional services like help with the ownership transfer or compliance.

- A shelf corporation with a desirable name or specific legal structure might cost more.

- And, if the shelf company comes with extra documents like an EIN or credit reports, this can also increase the price.

Of course, demand in certain areas or industries can influence pricing trends as well. Consider your needs and check for any hidden costs before you make a decision.

Recommended: How to Find Aged Shelf Companies for Sale +Why Buy Them?

Can You Buy an Aged S Corp?

You can absolutely purchase an aged S Corp—This is a type of shelf company that elects to be taxed under Subchapter S of the Internal Revenue Code. These entities offer benefits such as pass-through taxation, which can be advantageous.

S Corps are available on several shelf corporation marketplaces. If you elect to purchase one, make sure the S Corp you’re considering has kept up with necessary filings and compliance requirements.

You might also like: How Much Does it Cost to Start an LLC (Beyond Licensing)?

What Are the Assets of a Shelf Company?

Shelf companies usually don’t have significant assets or liabilities. They’re like blank slates with a history, meaning their value comes from their age and the credibility they bring, not from physical or financial assets.

However, this can vary. Some shelf corporations may have been involved in transactions or other activities, while others remain completely unused and empty.

You can’t necessarily use a shelf corporation with no trading history and simply pretend it has been in business for a long time.

If you buy a shelf corporation that has been involved in activities like buying and selling products or services, be careful—There might be hidden problems or debts from its past. Make sure to carefully review business history and get legal advice to avoid future issues.

You might also like: 3 Best Business Credit Cards for a New LLC +More Resources

Is Buying a Shelf Company Worth It?

Buying a shelf company can be a smart move if you need to quickly establish business credibility. Instead of enduring the lengthy process of setting up a new business, you can quickly step in with a shelf company, making the setup process simple and hassle-free.

An aged shelf corporation might provide:

- Instant credibility

- Faster credit access

- Time savings

First, these established companies tend to provide instant street cred—Their age can make your business appear legit right from the start, which potentially earns you greater trust from customers and partners.

Shelf companies can also open doors to opportunities that require a business with history, like:

- Meet a corporate lease requirement

- Fulfill a business contract requisite

- Satisfy a business loan or credit stipulation

Business lessors, decision-makers, investors, and lenders often favor companies with a few years of operation.

So, an established shelf corp can make it easier to kickstart your business—Plus, if you want to expand into new markets, a shelf company might streamline some of the legal and regulatory aspects of your expansion. And, if the shelf company comes with a desirable name, you get the benefit of using it without the effort of registering a new one.

You might also like: Low-Risk NAICS Codes +Best SIC Codes for Business Credit

How to Choose the Right Shelf Corporation Under $500

To find the best shelf corporations under $500, search online marketplaces and business brokers.

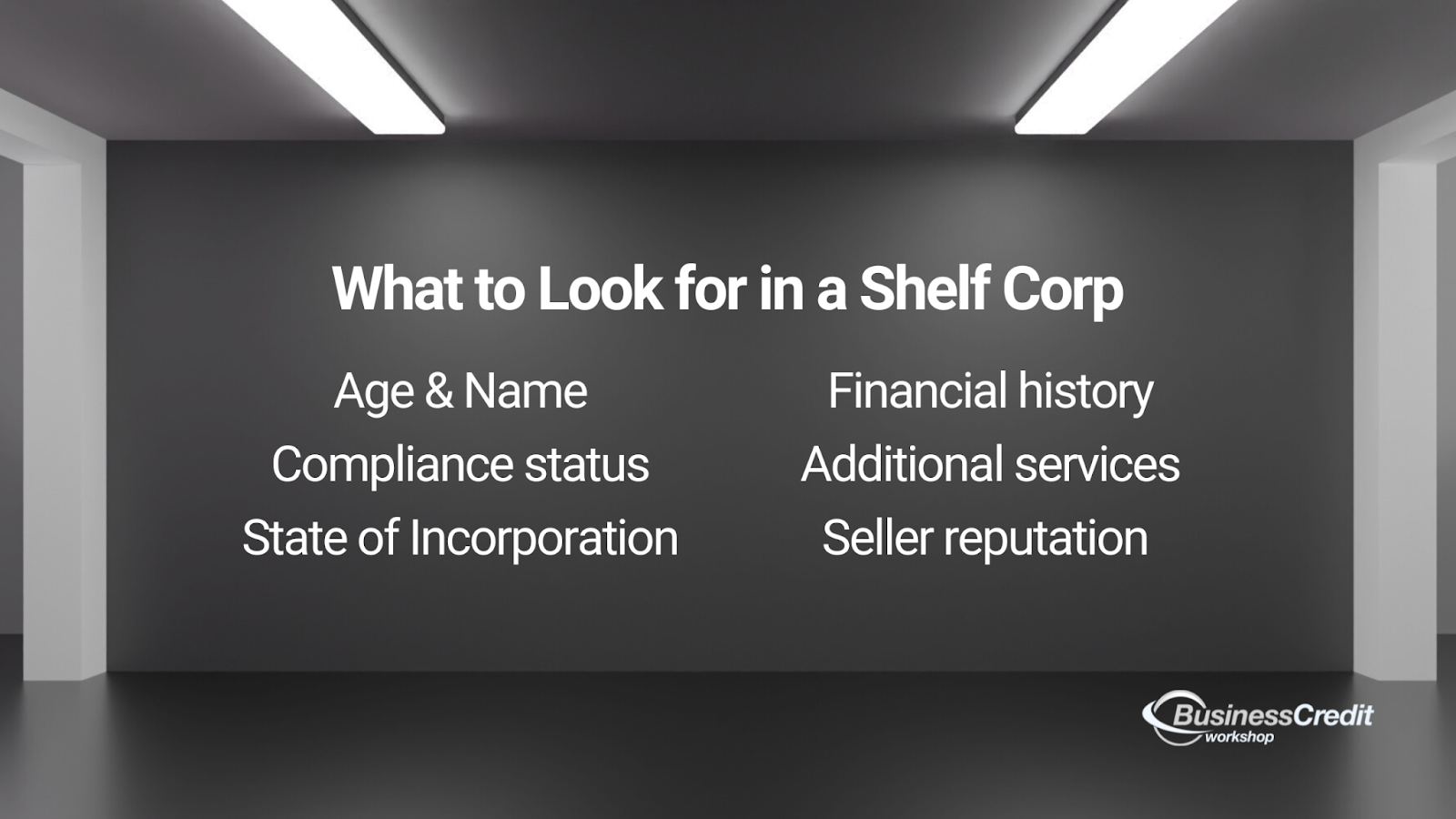

Make sure the shelf company meets your requirements:

- Age

- Compliance status

- State of incorporation

- Name

- Financial history

- Additional services

- Seller reputation

For the most part, shelf corporations available in this price range are less than a year old. But, just because they’re not listed doesn’t mean they’re necessarily unavailable.

Ask your friends, family, or anyone in your network if they have an old business they never used. My uncle had one, and lots of people do. If you can get it back in good standing, you might be able to buy it for under $500.

Now, let’s explore how you can go about making sure a registered entity has everything you need.

You might also like: Comprehensive ZenBusiness Review: Is it Legit for LLCs?

1. Check the Age of the Shelf Corporation

To start, evaluate the age of the shelf corporation—An established company with several years of history can offer significant advantages, like a credibility boost and easier access to credit.

If you’re looking at shelf corporations costing less than $500, you’ll usually find ones that are about a year old or younger. These newer companies might not seem as trustworthy as older ones, but they can still be useful in some cases.

2. Verify Compliance Status

Next, make sure that the shelf corporation is in good standing with all relevant regulatory requirements. Check that all necessary filings and fees have been paid and that there are no outstanding penalties or compliance issues.

A corporation in good standing reflects proper maintenance and reduces the risk of legal complications. Request documentation from the seller to verify the company’s compliance status and confirm that it meets all legal requirements.

3. Review the State of Incorporation

The state where the shelf corporation is registered can have a major impact on its advantages. Some states offer more favorable business laws, tax benefits, or regulatory conditions.

For example, Delaware is known for its business-friendly environment—this might be beneficial depending on your needs. Evaluate whether the state of incorporation aligns with your business strategy and operational requirements.

4. Examine the Name of the Corporation

The name of the shelf corporation is another critical factor to consider. A name that fits well with your branding or operational needs can enhance your business’s image and save you from the hassle of registering a new one.

Ensure the name is appropriate and does not conflict with existing trademarks or legal issues. A suitable name can help you establish a professional presence more quickly and seamlessly.

5. Check Financial History and Liabilities

It’s super important to investigate the financial history of a shelf corporation to make sure it’s free of any outstanding liabilities or debts. A clean financial record is crucial to avoid inheriting potential financial issues.

Request detailed financial statements or reports from the seller to verify that the corporation’s financial history is clear. Make sure there are no hidden obligations that could complicate your acquisition.

You might also like: Business Credit Report – Run a Free Company Search with Experian

6. Look for Additional Services and Features

When you evaluate a shelf corporation, consider any additional services or features included in the purchase.

Some sellers offer extras like:

- Help with ownership transfer

- Regulatory documentation preparation

- A credit-building package

These added benefits can streamline the setup process and provide additional value—Assess what’s included in an offer to determine if it meets your specific needs and adds convenience to the transaction.

You might also like: How to Create a Business Credit “Entity”

7. Confirm the Legal Structure and Fit

Verify that the legal structure of the shelf corporation aligns with your business needs. Whether you require an LLC, S Corp, or another type of entity, ensure that the corporation’s structure supports your operational and regulatory requirements.

The right legal structure can provide the appropriate legal protections, tax advantages, and operational flexibility. Confirm that the shelf corporation fits well with your business strategy and goals.

You might also like: Sole Proprietorship VS LLC: How to Choose Your Entity Wisely

8. Research the Seller’s Reputation

Finally, choose a shelf corporation from a reputable seller with positive reviews and a solid track record. A trustworthy seller will make sure you receive a legitimate, well-maintained entity—this minimizes the risk of potential issues.

Research the seller’s background and customer feedback to verify their reliability and the quality of their listings. A reliable seller will provide peace of mind and help ensure a smooth acquisition process.

You might also like: 11 Alternative Ways for Entrepreneurs to Raise Capital

Frequently Asked Questions

What are aged shelf corporations with credit packages?

These are shelf companies bundled with additional services like credit-building packages. These packages might help you secure business credit faster with extra resources.

What are the best shelf corporations under $500?

The best shelf corporation depends on your specific needs and preferences. Look for companies that offer a balance of age, credibility, and any extra features you might need.

Are Delaware shelf corporations for sale?

Yep, many sellers offer Delaware shelf corporations, which are popular because of Delaware’s business-friendly laws.

Can I buy a wholesale shelf corporation?

Yes, purchasing multiple shelf corporations at once, or a wholesale shelf corporation, can sometimes offer a discount—This option might be ideal for investors or businesses that need several entities.

Conclusion

Aged shelf corporations under $500 can offer a cost-effective solution for quickly establishing a business with a credible history. By understanding the costs, benefits, and legal aspects, you can find the right shelf company to meet your needs.

Looking to boost your business with a shelf company, faster access to credit, and a year of free Business Credit Elite Club membership? Get a 3-year old shelf corporation and elevate your business today.

Want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop!