Since you’re interested in repairing your business credit, I’ll assume that you had a good credit score at one point. Now, for one reason or another, it has taken a hit (If that’s not the case, and you haven’t established credit yet, you might want to start here).

First of all, if your business credit is not so great, don’t beat yourself up — it happens more than you would think.

Don’t believe me? According to US Courts, in 2021, a total of 14,347 businesses filed bankruptcy in 2021. If you think this might have been a COVID-related spike, think again — the same source cites 23,157 business bankruptcy filings in 2017, a couple of years before the pandemic began.

But, I don’t want you to focus too long on anything negative. Instead, let’s be solution-oriented and explore how business credit repair works.

Bear in mind that business credit is not the same as personal credit and some of the laws protecting consumers don’t apply, which isn’t necessarily a bad thing. In fact, business credit is much easier and faster to restore than personal credit.

This is what’s in store:

- What is Business Credit Repair?

- 8 Steps to Repair Your Business Credit

- 1. Review Your Business Credit Reports

- 2. Note Every Item You Want Removed From Each Report

- 3. Dispute Entries in Your Dun & Bradstreet Report

- 4. Dispute Entries in Your Experian Business Report

- 5. Dispute Entries in Your Equifax Business Report

- 6. Reach Out Directly to Creditors

- 7. Establish New, Healthy Accounts

- 8. Continue to Monitor Your Business Credit

- Final Thoughts

Now, here’s everything you need to know to restore your business credit.

What is Business Credit Repair?

Business credit repair or restoration typically refers to a third-party service that attempts to get negative information, like missed or late payments and defaulted accounts, removed from business credit reports in exchange for a payment.

A business might have a net 30 account on their report that shows as a late or slow pay that they want to clear up. Or, maybe they need to remove an old address from the credit bureau’s record. Business credit repair organizations might offer a service to help for a monthly or one-time fee in addition to any settlement offers they submit to creditors.

Luckily, in most cases, these services are not needed. You can easily restore business credit on your own, which is the primary focus of this guide.

The Golden Rule of Good Credit

Whether you’re talking about business or personal finance, here’s the golden rule of good credit: Make your payments to lenders on-time, as agreed.

While this may seem too obvious, it’s crucial. If you make your payments to lenders as agreed, you are very likely to maintain a high credit score.

So, when life gets in the way, and you can’t make business loan and credit card payments like you expected, stay in communication with your lenders. As soon as you think you might miss a payment, pick up the phone and reach out to ask about your options.

If you’re reading this early, at the first sign that your credit is about to slip — you never know — the above advice might be enough to keep you afloat while you figure out your finances.

If you’re already sitting on a low business credit score, it’s time to take action.

8 Steps to Repair Your Business Credit

Here’s the process, step-by-step, to restore your business credit.

1. Review Your Business Credit Reports

The first thing you need to do when restoring your business credit is get an up-to-date copy of each of your credit reports from the business credit bureaus.

There are three main business credit bureaus that most lenders will use to determine whether or not your company is worthy of financing.

Get a copy of your report from each bureau:

- Dun & Bradstreet: Access your PAYDEX report

- Experian Business: Get your Experian business credit report

- Equifax Business: Obtain your Equifax business credit report

Download or print copies of each report so you can thoroughly review for accuracy.

You may be able to obtain copies of your business credit report at no cost if you have recently been denied financing. Within 90 days of your denial, mail a request to the creditor and ask that they send a copy of your business credit report to you.

Set up a free account with Nav to access and monitor your Experian and Dun & Bradstreet business credit summaries.

| Note: In addition to these three bureaus, I have heard of a couple of outliers here and there. But, I don’t recommend you pay them any attention (unless you are getting denials after cleaning up the main 3). Every business credit lender I’ve ever worked with has used one of the above to determine a company’s creditworthiness. |

Recommended: How to Check Your Business Credit Score

2. Note Every Item You Want Removed From Each Report

The more organized you are at this stage, the better. Examine every potentially negative item on your report and read through your company details for inaccuracies.

Incorrect and negative information on your business credit report not only decreases your chances of obtaining financing, but adds additional hurdles. For example, you might pay higher insurance premiums, be charged higher interest rates on the funds you do receive, and find it difficult to rent equipment or office/retail space because of a mistake on one of your reports.

Look for any slow or late payments on your accounts that might affect your score. In addition, look for old business addresses or outdated contact information that you would like removed.

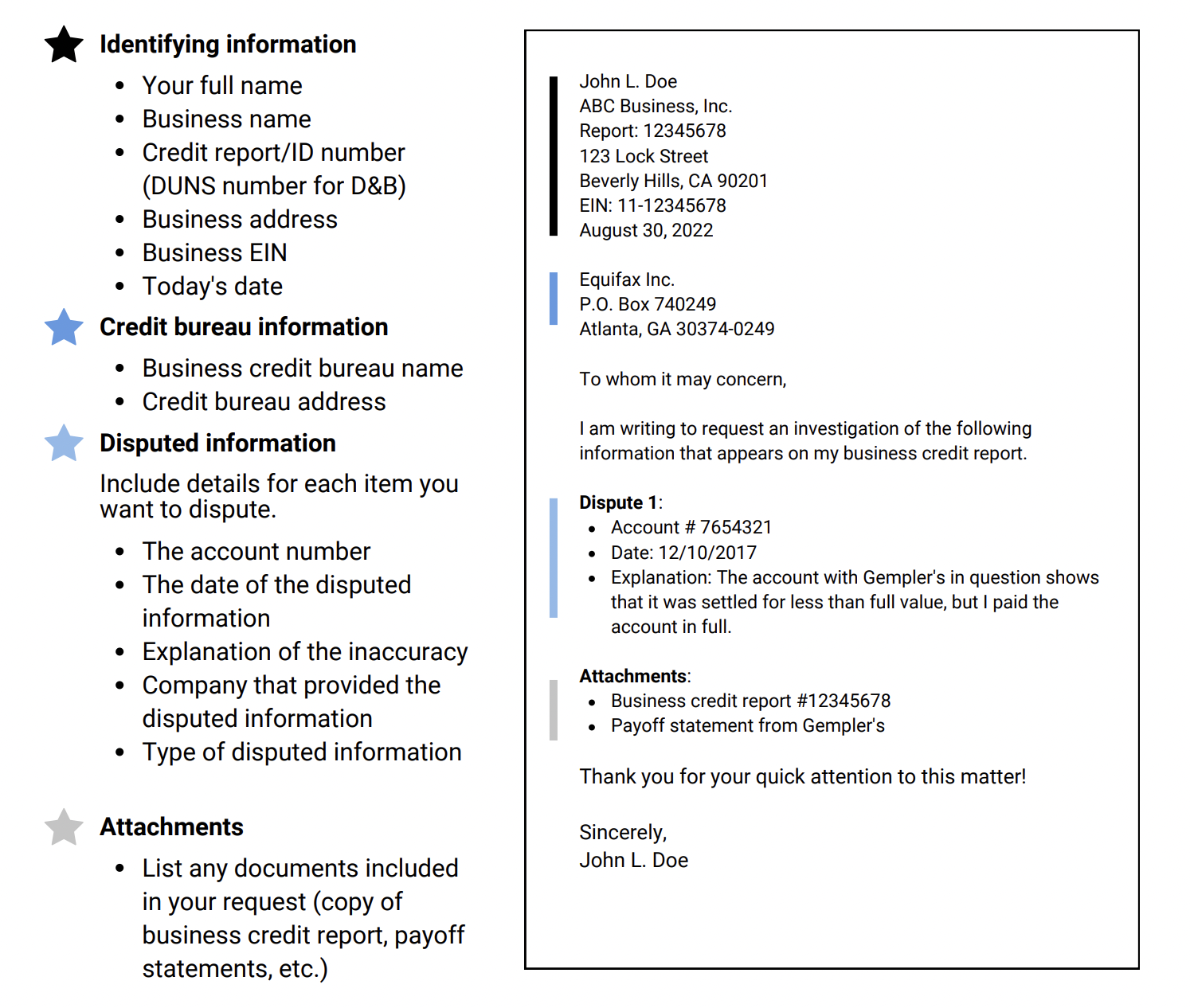

For each report, list each item that you would like reviewed for removal. Include the following:

- The account number

- The date of the disputed information

- Explanation of the inaccuracy

- Company that provided the disputed information

- Type of disputed information (contact, missed/late payment, etc.)

Once you have completed your list, you’re ready to move forward.

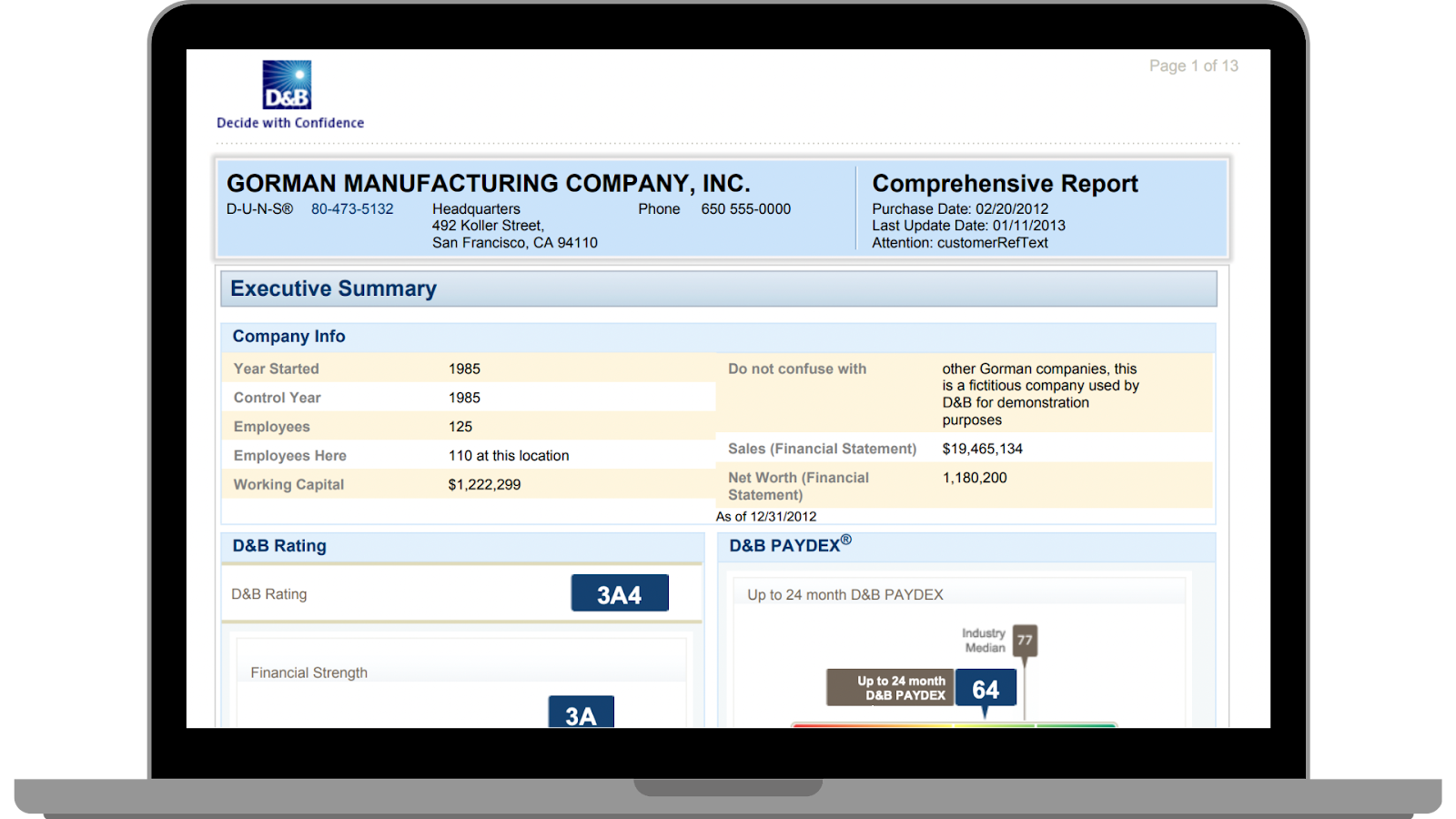

3. Dispute Entries in Your Dun & Bradstreet Report

For Dun & Bradstreet, the simplest option is to dispute incorrect items online via your account dashboard. You can pay for an upgraded account, but all you need is the free version (there aren’t many scenarios where I recommend paying for a premium account).

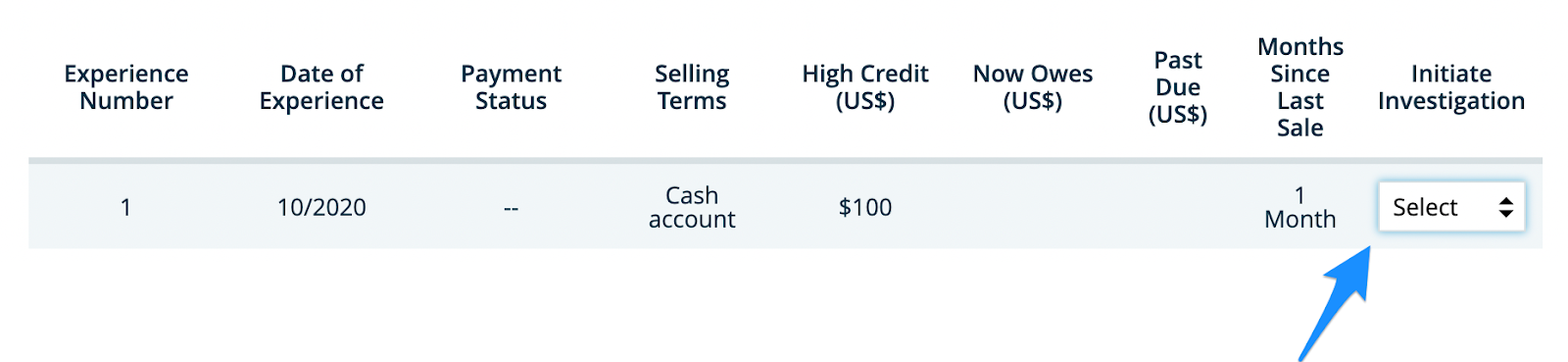

Simply login to your account > navigate to D-U-N-S Manager > scroll down to Trade Payments in the left sidebar.

Your trade accounts will appear in the dashboard with an option to select from the dropdown under Initiate Investigation.

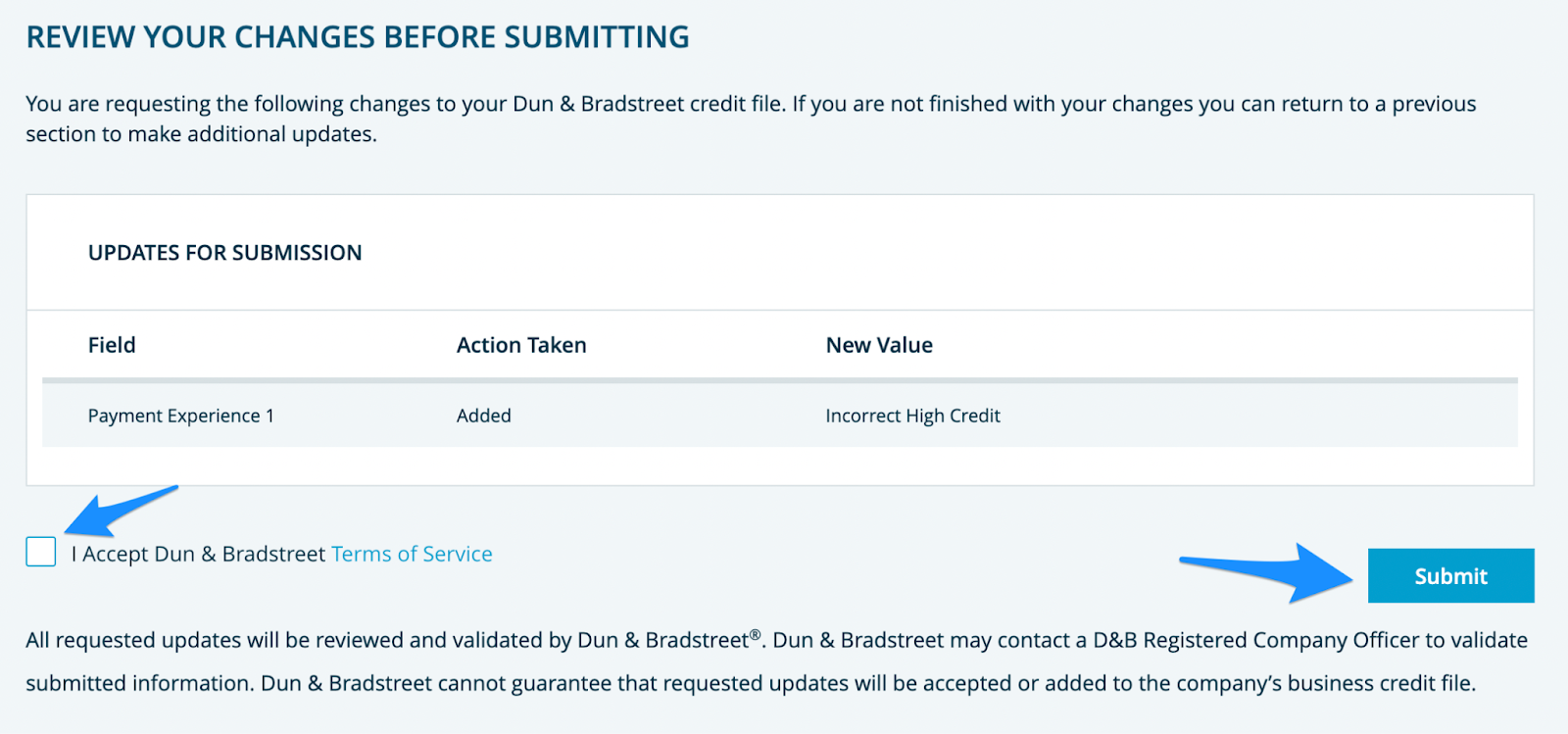

Follow the prompts to continue at the bottom right of the screen until you come to the summary page.

Accept the terms of service, then click Submit.

You will receive a reply relatively quickly, letting you know whether the investigation has resulted in a removal of the items you requested or not.

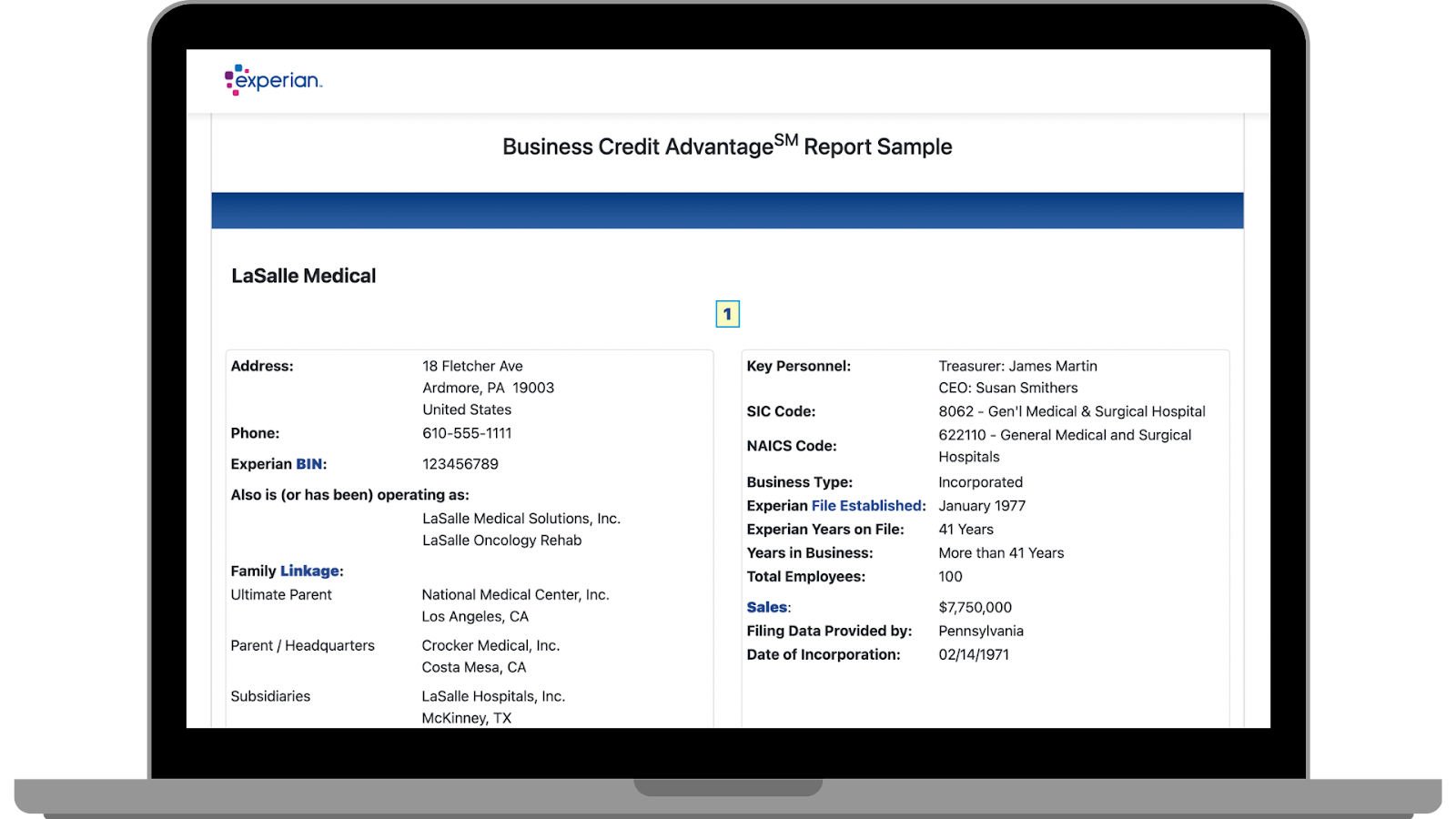

4. Dispute Entries in Your Experian Business Report

The best way to execute Experian business disputes is to print your full, updated report, circle the incorrect information, and write-in the reason you are disputing each item.

Scan and email the edited report to businessdisputes@experian.com, along with any additional documentation you have to support your request for information removal.

Alternatively, you can open an account with Experian business, then call in to initiate a dispute: (888) 397-3742. When you place the call, have your list handy so that you can accurately indicate which items you want the bureau to investigate.

5. Dispute Entries in Your Equifax Business Report

Equifax disputes can be handled online or via mail, email, or phone. Recently, I’ve seen email disputes resolved within about one week.

Equifax Inc.

P.O. Box 740249

Atlanta, GA 30374-0249

commercialdisclosures@equifax.com

(800) 727-8495

Download business credit dispute template PDF

6. Reach Out Directly to Creditors

After you’ve waited about a month after initiating your dispute(s), or you’ve heard back from the bureaus, are there any red flags still on your reports? If so, it might be worth reaching out to the creditor directly.

In some cases, you may be able to negotiate a deal to get negative information removed from your account. For example, if an account shows unpaid, you might be able to get the creditor to report the account paid in full with a lump sum payment.

If you do negotiate a deal like this, be sure that you get the agreement in writing, including the date by which the creditor will report to the credit bureaus.

7. Establish New, Healthy Accounts

A crucial ingredient for a strong business credit score is to have healthy accounts. If your credit profile is sparse, it might be a good idea to add a few accounts that report on-time payments to the business credit bureaus.

After your reports have been cleaned up, you might benefit from opening new accounts — depending on how established your business credit profile is.

To get started, see our list of 41+ Companies That Help Build Business Credit.

Be sure to keep any revolving accounts below 30% utilization for an optimal impact to your credit score. For example, if you have a revolving business credit card with a $30K limit, never use more than $10K at a time. Better yet, pay the card off in full each month.

Ask for credit limit increases on revolving accounts. From time to time, some creditors will automatically increase your spending limit. Other creditors require that you make the requests for increases yourself. If you can request an increase from your account dashboard, go ahead — if not, pick up the phone and call customer service and ask if you qualify for a higher spending limit.

8. Continue to Monitor Your Business Credit

Like personal credit, it’s important to monitor your business credit and keep an eye out for inaccuracies. If you haven’t already, sign up for a Nav account.

Nav can help you monitor your business credit… and more.

- Get actionable insights into credit and cash flow

- See relevant financing recommendations

- Research customer and partner credit profiles

- Boost your chances of obtaining business credit

It doesn’t hurt to maintain accounts with all three bureaus, but you can accomplish most of what you need from a single dashboard with Nav alone.

Final Thoughts

Credit repair is important when you want to increase your business financing limits. Start by reviewing your reports from the three major business credit bureaus. Then, dispute any inaccuracies you find on your reports. If you need to, reach out to creditors directly to clean up any accounts in poor standing. After that, maintain healthy accounts, and monitor your business credit to watch for new inaccuracies or mistakes.

To learn how to obtain $100K in business credit in 30 days, join Business Credit Workshop today.