I mentioned Brex in my last post about the best business credit cards for startups (high on the list, I might add). That’s when it dawned on me that we haven’t covered the Brex corporate card offer yet. And, this is something you need to see.

The two top highlights for the Brex card are that there is no personal guarantee (underwriters don’t look at your personal credit score) and it’s free. Not every business will qualify for one of these cards. But, if you are able to, it’s definitely worth looking into.

This is what’s in store:

- Brex Card Overview

- Brex Card Rewards Summary

- How to Qualify for a Brex Card

- Brex vs Ramp vs Stripe vs Divvy

- Final Thoughts

Keep reading to learn everything you need to know about the Brex corporate card and find out if this offer is too good to be true or right for your business.

Brex Card Overview

The Brex card, issued through the Brex financial operating system, is a corporate credit card, which means it’s designed for businesses with multiple employee spending (in this case, tech, life sciences, and eCommerce companies). However, corporate cards don’t have to be used by several staff members. In fact, some applicants qualify for a single corporate card with a $1K limit for individual business spending.

Most corporate cards don’t require personal guarantees. Instead, applicants whose companies demonstrate a high probability to repay the funds are extended credit. The Brex card works the same way. So, if you own a company and you have a low FICO score, it shouldn’t affect your ability to obtain credit.

Now, the most impressive feature of this card is that it’s free. Cardholders pay no annual fee, no interest, and no other costs.

Recommended: 7 Best Cash Back Corporate Cards to Explore

Who Owns Brex?

Brex was co-founded by Henrique Dubugras and Pedro Franceschi in San Francisco, California. The pair previously co-founded the online payment system, Pagar.me before selling it in 2016 to Brazilian credit card processor, Stone. According to Forbes, the pair moved to the bay area to attend Stanford before dropping out after just a few months. Entrepreneurship seems to favor them.

Brex Account Offers

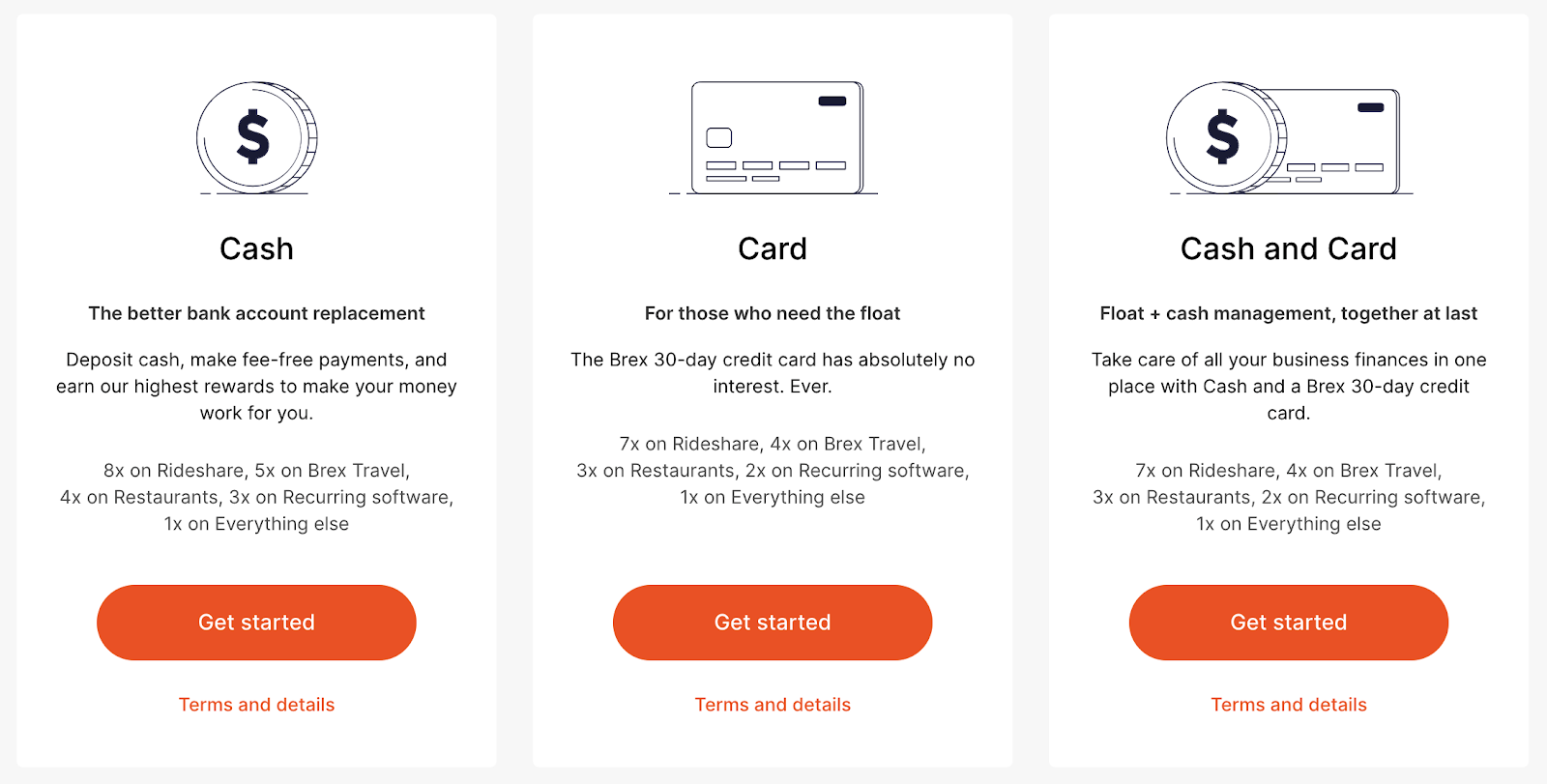

When you sign up for a Brex account, you will have the option to apply for three different offers: Cash, Card, or Cash & Card.

A Cash account is similar to a checking account, though the website explicitly states that it is not a bank account. Still, you can use a Brex Cash account to deposit money, make payments without fees, and earn rewards. Using your “daily pay” account, you can earn rewards on all your spending.

Essentially, Brex offers a way to get funding with net 30 terms, which means your account must be paid in full at the end of each month. Traditionally, credit cards offer users the ability to make a “minimum payment” each month. Brex terms are a little different. So, if you’re looking for a way to fund a large purchase and pay it off slowly over time, this card isn’t for you.

But, you can use a Brex Card to boost cash flow while you earn rewards. Furthermore, the company claims that tech companies specifically can get 10-20X higher limits than they will with other cards.

Cash & Card is the best of both worlds. Boost your cash flow with the Brex Card while you handle business transactions through Brex Cash.

How Does Brex Make Money?

Rather than charge interest rates and annual fees, Brex earns a percentage from merchants for each transaction. Cardholders are offered attractive rewards on spending with partners and given incentives to pay daily rather than monthly like most other credit cards. Shorter payment terms for users frees-up cash flow for the brand, allowing them to offer attractive terms.

Brex Card Rewards Summary

Above, I mentioned that Brex caters to tech, life sciences, and eCommerce businesses. While being in one of these industries isn’t a requirement to obtain credit, those that fall under this umbrella will benefit the most. In addition to being a free card with no fees or interest, here are the benefits of using Brex for your business spending.

Up to 30K in Introductory Bonus Points

Brex is the only corporate card with zero fees that currently offers an introductory bonus. Just for linking your new Brex credit card account to Brex Cash, you will earn 20K bonus points. In addition, when you spend $3K on your card in the first 3 months, you’ll earn 10K bonus points.

Earn 1-8X Points Per Dollar on Spending

All Brex spending has the potential to earn you points.

With a Brex Cash account, you can earn 8X points on rideshare apps, 5X points with Brex travel partners, 4X on dining at restaurants, 3X on recurring software subscription payments, and 1X on everything else.

And, with a Brex Card, you can earn 7X points on rideshare apps, 4X points with Brex travel partners, 3X on dining at restaurants, 2X on recurring software subscription payments, and 1X on everything else.

Points can be redeemed through Brex travel, via gift cards and cash back, or as statement credit (for cardholders who don’t use Brex Cash).

$150K Worth of Partner Perks

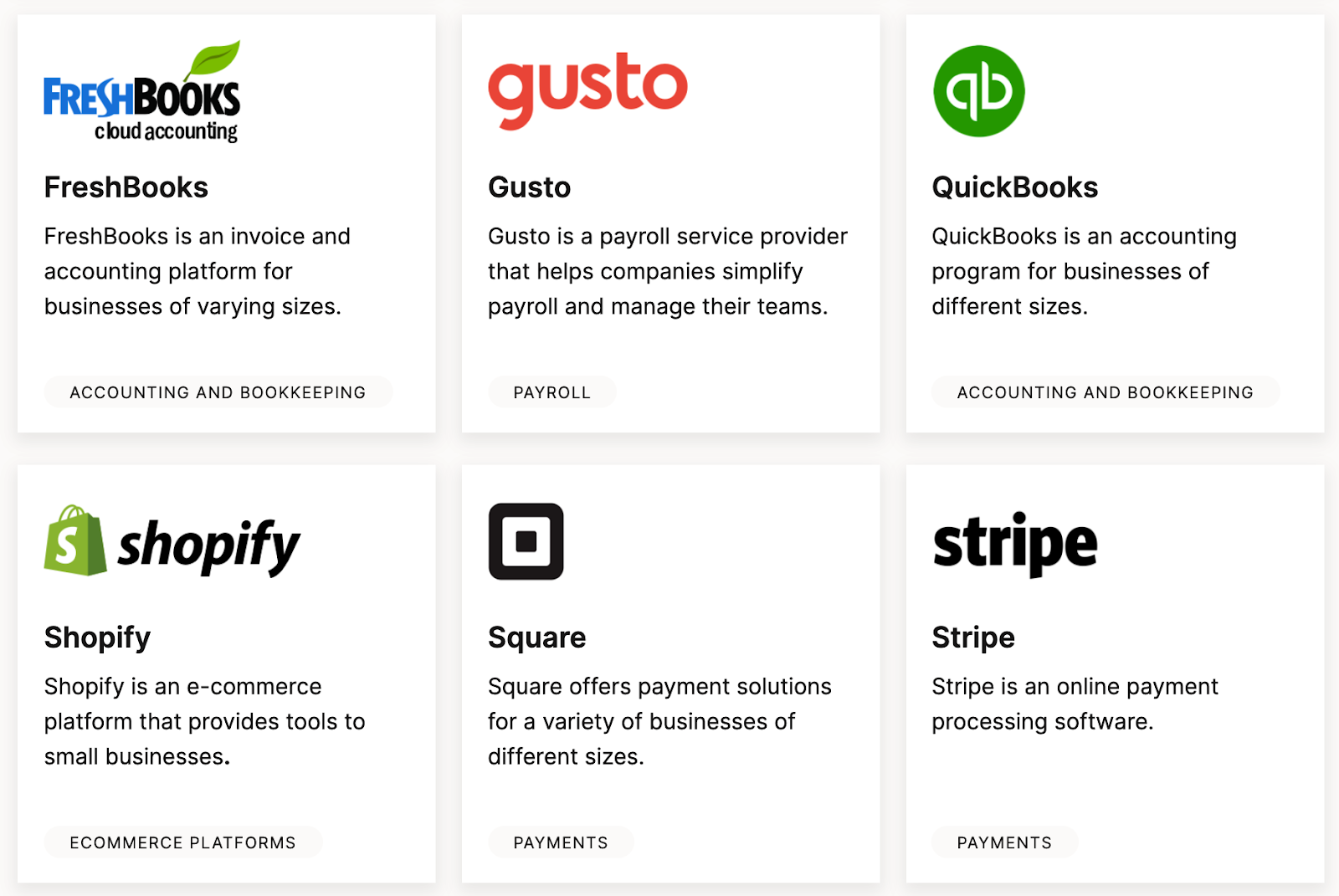

Brex partners include big names like AWS, Slack, and Google Ads. If you were to utilize all of the savings offered as a Brex cardholder, you could redeem up to $150K in perks.

- AWS – $5,000 credit and up to $100,000 in AWS Activate, depending on eligibility

- Slack – 25% off 12 months of eligible Slack paid plans

- Carta – 20% discount on first year and waived implementation fees, plus 10,000 Brex Points

- Zoom – 20% discount on annual Zoom subscription

- Quickbooks – 40% off your first 12 months of QuickBooks

- Google Ads – Up to $150 in Google Ads credit

- Dropbox – Get 50% off on all Dropbox Business, Standard, or Advanced plans

- Gusto – Get 50% off any plan for 12 months

Note that many of Brex’s competitors offer similar perks.

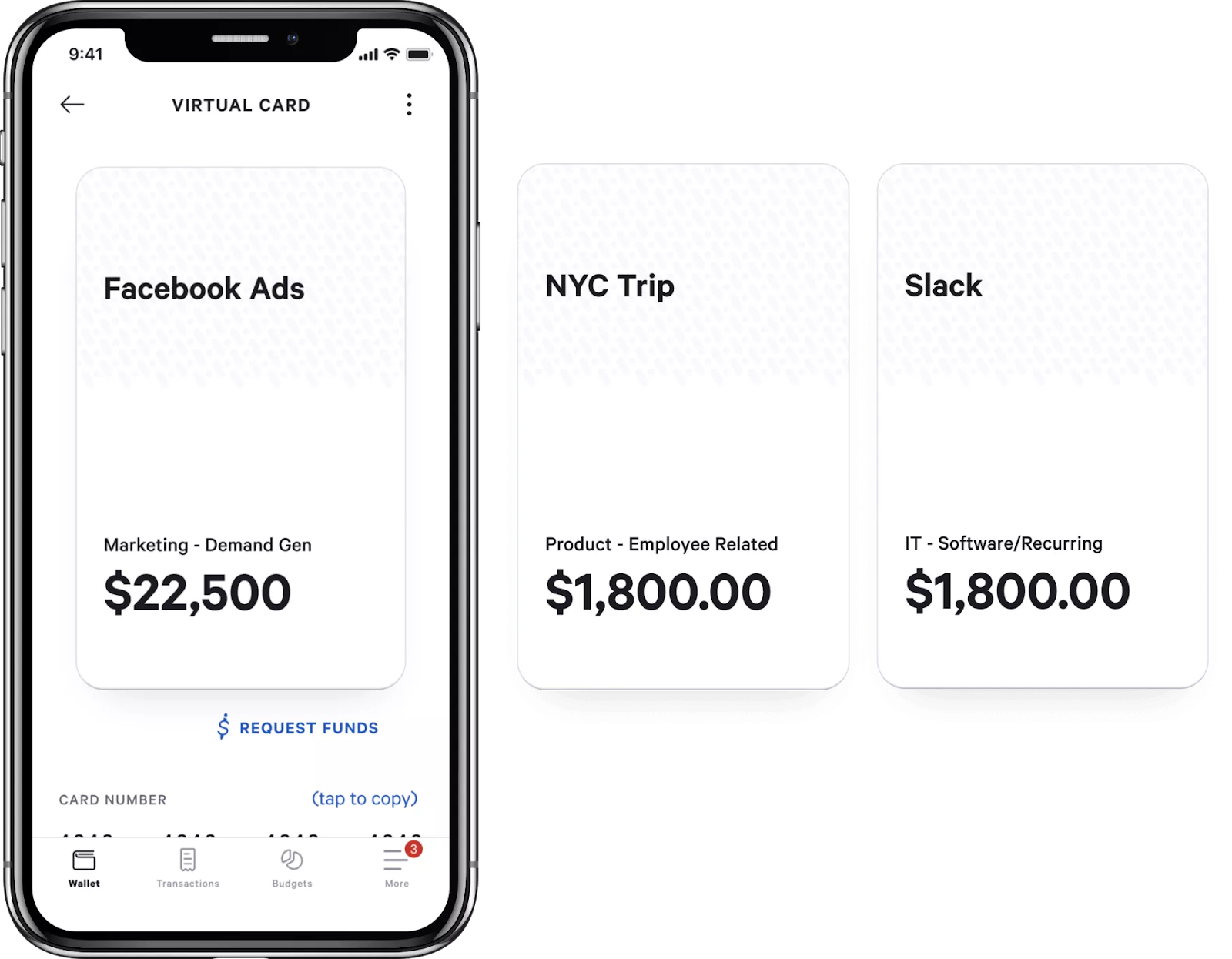

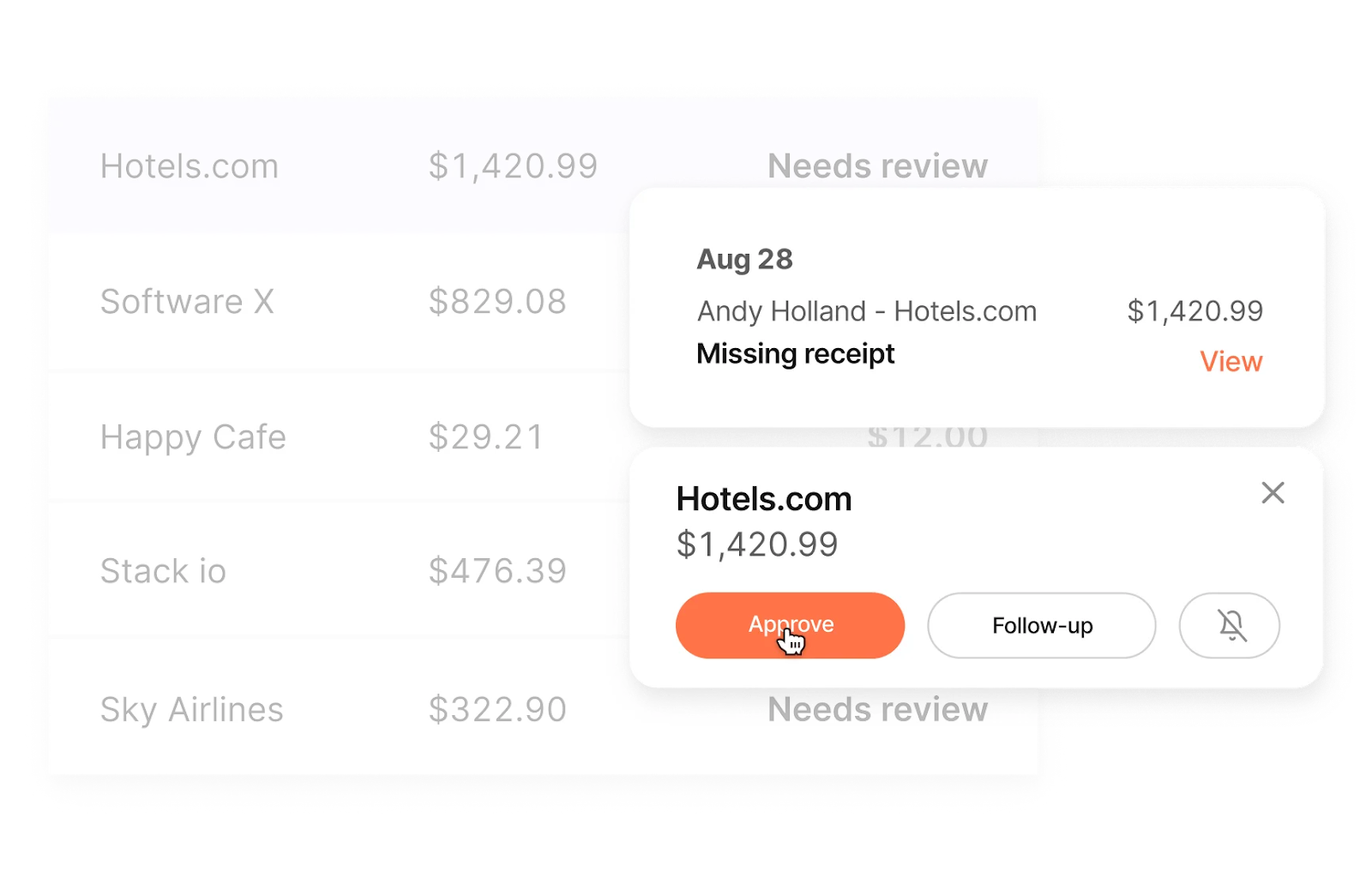

Built-In, Real-Time Expense Tracking

Essentially, Brex expense management tools enable you to put your expenses, including employee spending, on autopilot. Upload receipts and the software will match spending in your accounting platform. You may be able to cut reconciliation time by up to 50% and spend up to 75% less time chasing receipts.

You can also set up monthly spending limits for each card, which can give employees more flexibility and management more time freedom.

Another key feature of Brex expense management are the virtual cards. Divvy has a similar offer, which means your employees don’t have to wait for a physical card to be issued. The technology seems to be a hit amongst users.

Consultant, Accountant, and Travel Agent Connections

When you book your trips via Brex Travel, you can access experienced corporate travel agencies for free. Travel agents are available 24/7 to help you redeem points and book with 30% to 60% discounts.

Looking to hire an agency to help you with consulting services? Brex cardholders can access a directory of vetted agency and accounting partners that you can leverage to help you scale your business. Take advantage of the opportunity to work with service providers experienced with Brex expense tracking. As far as I know, other credit card companies don’t offer anything like this.

How to Qualify for a Brex Card

Brex isn’t super transparent about their qualification terms, but here’s what we do know:

- You must have an EIN for a US-based business

- You must have a business bank account

- You will need to verify your identity with photos of your government-issued ID

Furthermore, here’s what we think, based on anecdotes from existing cardholders.

- You should have $50K to $100K in the bank at all times

If you bank with a smaller community bank or credit union, you will need to upload your two most recent bank statements. The process is quick and painless, but applications can take up to 15 days to review.

Brex vs Ramp vs Stripe vs Divvy

Now, here’s how Brex stacks up side-by-side with its top competitors: Ramp, Stripe, and Divvy.

Each of the corporate cards is free and comes with some alluring rewards. Some of the key value indicators when we compare are that Brex is the only card that seems to offer an intro bonus. Next, in order to qualify for Stripe’s corporate card, you must use their software and either wait or ask for an invitation.

Final Thoughts

Brex has an impressive corporate card offer for tech, life sciences, and eCommerce companies. If you can qualify and you’ll take advantage of the rewards, I’m sure it’s worthwhile – you can’t really go wrong with free. But, if you aren’t able to qualify, you have plenty of other options. Want to learn how to obtain $100K in business credit in 30 days? Join Business Credit Workshop today!