The US Stimulus has some extremely helpful legislation for small businesses written into it. And, there are certainly quite a few rumors floating around. If you don’t have the truth, how are you supposed to know what to do?

The answer is, you can’t. Unless you have all pertinent information, your decisions are sure to be ill-informed. But, the Stimulus may be your saving grace right now, so read on to find out.

- What is the US Coronavirus Stimulus?

- How will new legislation provide relief for small businesses?

- How can you obtain an SBA 7(a) loan and have it forgiven?

Now, go grab a pen and paper because you’re going to want to take notes.

First, What is the US Coronavirus Stimulus of 2020?

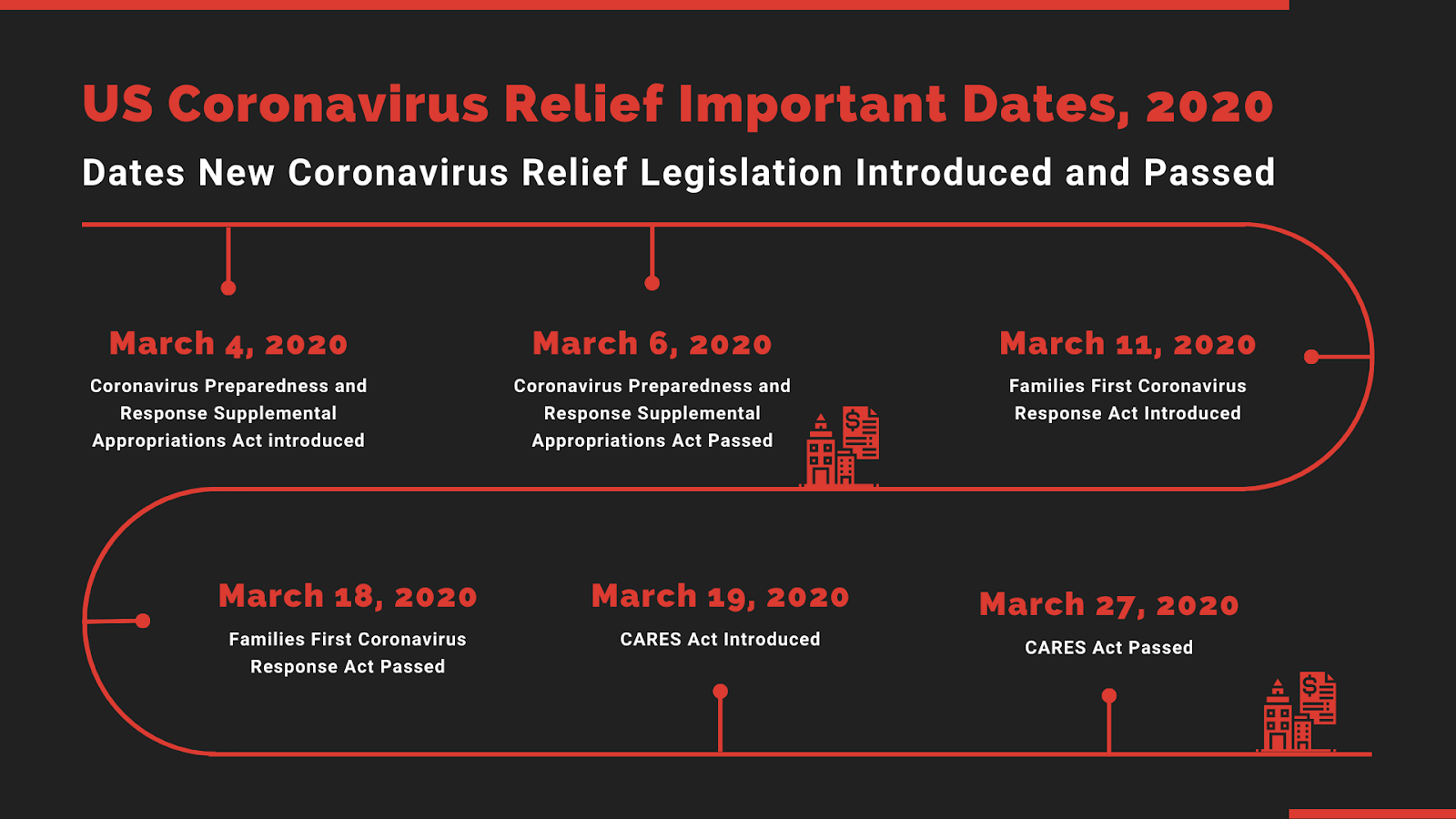

While many people are talking about the US relief legislation for COVID-19 as if it’s a single document that will help individuals and small businesses get through this catastrophe, it’s not that simple. In fact, thus far, the stimulus legislation has been rolled out in three phases.

- Phase 1: Coronavirus Preparedness and Response Supplemental Appropriations Act passed on March 6, 2020

- Phase 2: Families First Coronavirus Response Act passed on March 18, 2020

- Phase 3: Coronavirus Aid, Relief, and Economic Security (CARES) Act passed on March 27, 2020

And, while the second phase was important, it didn’t focus on small businesses like the first and third. So, for this purpose, let’s look at phases one and three.

Next, How Does the Coronavirus Preparedness and Response Supplemental Appropriations Act Help Small Businesses?

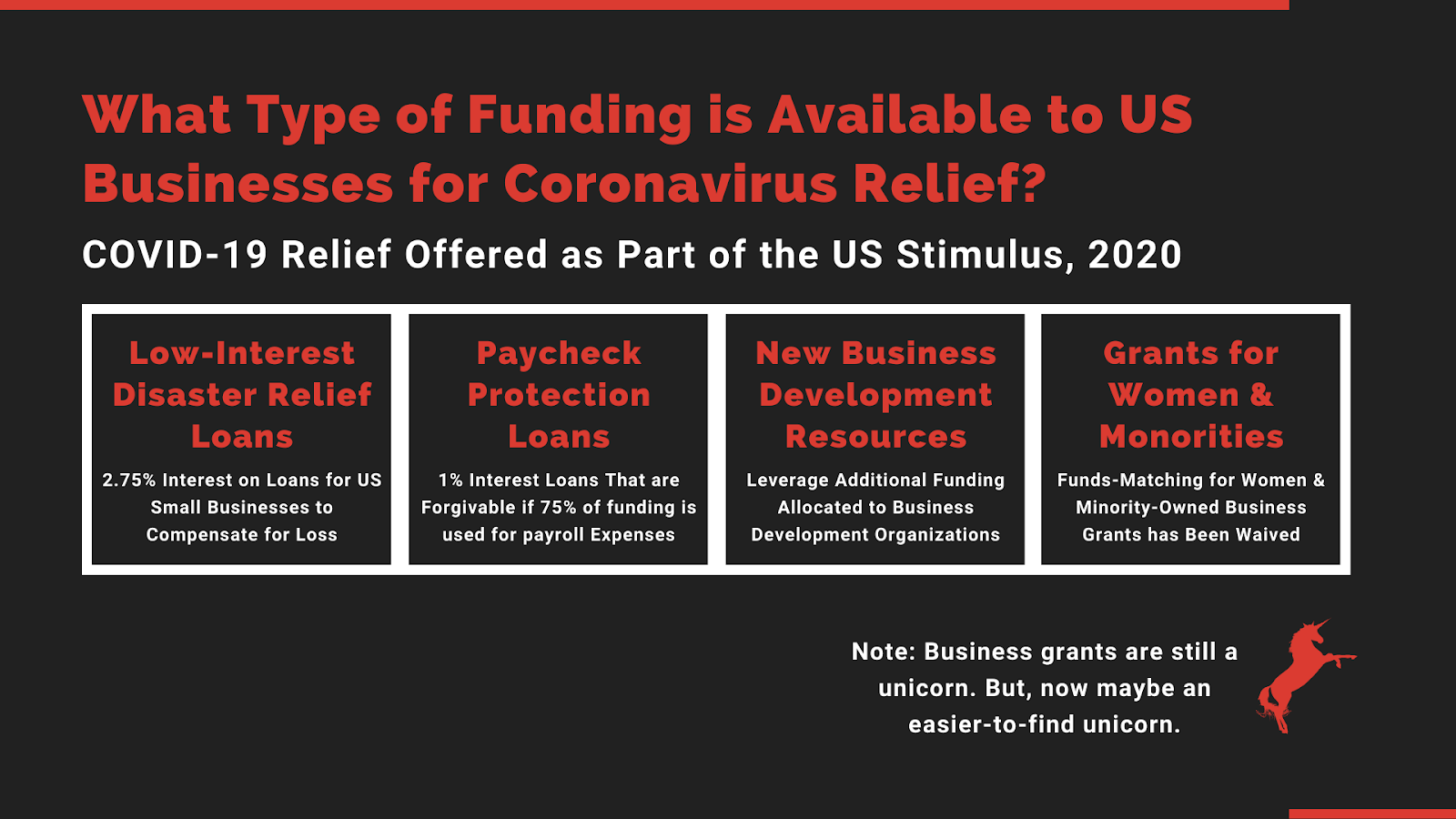

The Coronavirus Preparedness and Response Supplemental Appropriations Act or H.R. 6074 was made law in early March in response to the COVID-19 pandemic. This bill primarily outlined new funding rules and allocations for emergency response organizations and certain departments of government. And, it opened an existing SBA 7(a) loan, Disaster Assistance to individuals and small businesses that had been affected medically or financially by the Coronavirus.

SBA-guaranteed Disaster Assistance is now available to individuals and small businesses in a declared disaster zone to help pay for any damages that are not covered by FEMA. The low interest (3.75% for business and 2.75% for non-profit) loans can be used to pay for physical damage and economic injury caused by a given disaster.

Working capital loans of up to $2 million and economic injury relief loans up to $10K can be obtained through the program. When H.R. 6074 passed on March 6, 2020, the SBA opened this loan to the entire United States and outlying territories.

And, How Does the CARES Act Help Small Businesses?

The rate of unemployment skyrocketed in the month of March. And, the CARES Act was introduced on March 19 as a solution to keep employees paid during this critical time. An entire section of this bill is dedicated to small businesses.

The small business section of the CARES Act covers new legislation for the following:

- SBA 7(a) loans for small businesses, deferment, forgiveness opportunities, and prepayment penalties

- Entrepreneurial development for owners

- Requirements for financing programs through the Women’s Business Center and the Minority Business Development Agency

In a nutshell, what does this mean for you?

Paycheck Protection

First, the bill introduces SBA-guaranteed, low-interest (1%) “interruption” loans, which are now being called Paycheck Protection loans. These loans will be forgivable under certain terms (i.e. as long as you continue to pay your staff and use the funds primarily for payroll, you won’t have to pay them back).

M&T Bank has a great visual infographic you can take a look at for the PPP Program here

Furthermore, if your loan does not qualify for forgiveness, payments are automatically deferred for six months — you won’t start paying on a Paycheck Protection loan until six months after you obtain funds. And, you will receive no penalty if you are able to pay the loan off early.

Entrepreneurial Development

Next, new funding has been allocated to SBA partners for entrepreneurial development including help with navigation through the Coronavirus pandemic. Programs might include low-cost or free guidance on sanitation and health standards and will likely also involve new general business development training and resources.

Women and Minority-Owned Business

If you were interested in a business grant but did not have the means to meet the required 1:1 or 1:2 funds matching, you may have a new opportunity to rescue or grow your business. According to the new law, certain women and minority-targeted SBA-guaranteed funding programs will no longer require funds matching. These programs help female and minority entrepreneurs with grants and training on finance, management, marketing, and other operational aspects of a business.

So, you’ve repeatedly heard that economic development grants are unicorns. And, maybe the government was hiding them and has now released the mythical creatures to pasture in the SBA’s front lawn. But, you shouldn’t expect them to be easy to catch — they’re still unicorns.

How to Utilize an SBA-Guaranteed Coronavirus Economic Disaster Relief or Paycheck Protection Loan

SBA 7(a) loans are not issued directly through the Small Business Association. Instead, the department partners with banks, credit unions, and other financial institutions. They guarantee the funds so that if a business goes into default, the bank does not lose money.

If you ever had a federally-backed student loan, you may have an idea of how these programs work. You apply for a loan through a financial institution, often with the help of a broker. Then, the loans go into deferment so that you are not required to pay them back for a set time. For student loans, deferment typically lasts through the duration of your education.

You will need to find a bank or a broker with which to apply for a loan through one of these programs, which shouldn’t be hard. Most major lending institutions will be able to help you.

Coronavirus Disaster Relief & Paycheck Protection Loan Eligibility

All small businesses in the US and outlying territories are eligible to apply for one of these SBA 7(a) loans at this time. You must be able to prove that you were in operation on March 1, 2020, and that you are considered a small business under the SBA’s guidelines. Companies including Sole Proprietorships, Contract Workers, and Self-Employed persons may qualify.

Typically, a small business is a company with less than 500 employees. However, if you run a business with multiple locations that each employ less than 500 staff members, you could still qualify. Use the SBA’s small business size standards tool to see if your company size might qualify.

So, How Can You Get a Coronavirus Economic Disaster Relief or Paycheck Protection Loan Forgiven?

Through the new guidelines laid out in the CARES Act, Coronavirus Economic Disaster Relief funds are eligible for debt relief. This will defer payments until the end of 2020. And, while interest will accrue, your principal payments and fees will be waived during this time.

And, Paycheck Protection loans will be eligible for forgiveness under certain terms. You can have your entire loan forgiven as long as at least 75% of the funds go toward payroll and the remaining 25% or less is used to pay for interest on mortgages, rent, and utilities. “Payroll” includes salary, paid sick leave, and paid family leave for staff and self.

So, if you plan to use funds for operational costs that fall outside of the listed activities or for growth-related investments, look for a different type of funding.

Around the time that your Paycheck Protection loan is set to come out of deferment, you will need to apply for forgiveness. Again, this process will be similar to that of forgivable student loans that you might be more familiar with.

Additional SBA Resources

For more information about COVID-19 financial support for your business, see these resources from the SBA.

- Coronavirus Economic Disaster Relief

- Paycheck Protection Program

- Final Rules for SBA Business Loan Temporary Changes | Paycheck Protection Program

- Women’s Business Center Directory

- Minority Business Development Agency

Final Thoughts

It seems as though there may be a silver lining in this cloud. And, as long as your business credit qualifies you for funding, you might be able to take advantage of an unprecedented relief opportunity. If you need a guide to help you through the paperwork jungle, don’t hesitate to reach out with questions.

Stay well and stay safe.