Update: In July 2023, Nav acquired Tillful and launched the Nav Prime program (along with new a charge card offer) in September. According to Nav, the Tillful card is no longer available.

→ You can read the full review of Nav’s new card here: Is the Nav Prime Card Right for Your Business? Let’s Find out!

Recently, I came across a Facebook post in a private group, announcing a new secured credit card for businesses — it’s perfect timing for an offer like this since Wells Fargo and Brex no longer offer secured business credit cards. So, naturally, I had to explore the offer. And, what I found was so much more than just a credit card.

This complete Tillful review is a breakdown of everything I learned, and how you might use this offer to build business credit.

Here’s what’s covered:

- What is Tillful?

- The Tillful Credit Card

- The Tillful App

- Tillful Company Overview

- Frequently Asked Questions

- Tillful Secured Credit Card Competitor Overview

- The Verdict: Is Tillful the Real Deal?

Now, let’s get going!

What is Tillful?

Tillful is a fintech company that offers businesses a free credit score (which is different from a DUNS number and other traditional credit scores) that they use to match account holders with curated financial offers. To me, the business closely resembles a new Credit Karma for business.

By connecting to users’ business bank accounts via Plaid, the platform is able to gain financial information about companies, which is delivered back to users to see how they stack up.

Tillful also offers their own free, secured business credit card with 1.5% cash back, to help owners build business credit, an innovative and timely offer.

Tillful Business Credit Score Overview

The folks at Tillful have created their own business health score, which ranges from 0-100 and is based partially — i.e. mostly — on a company’s cash reserves and industry, a measure of real-time financial performance. The Tillfull score is never shared with lenders and is meant to give users a fresh view of their company’s financial health.

I’m not confident that this scoring system will actually influence potential lenders outside Tillful’s platform, but it seems like a pretty clever and helpful tool.

In addition, Tillful has partnered with Experian, who recently launched a machine-learned business credit score called Intelliscore Plus V3 (IPV3) — the new model is said to improve risk assessment for business lenders. Active Tillful account holders can request their free IPV3 business credit score at any time.

However, Tillful users who want to see a full report will have to order it from Experian using a quick link in their Tillful account dashboard or by visiting Experian’s website directly.

At least in part, the IPV3 score is based on a company’s tradeline payment history and ranges from 300-850. Rather than a 12-month model prediction, the IPV3 is based on the previous 24 months of credit history.

Coming from Experian, I think this scoring system is going to stick and that continually more traditional lenders will use it to make funding decisions.

Recommended: Nav Review: A Tool that Helps Build Up Your Business Credit Score

Currently, Tillful has a 4-star rating on Trustpilot, which tells me they’re making users happy, for the most part.

Most business owners typically don’t have all of the information they need to access business lines of credit — Tillful gives them a new way to establish business credit at no cost (other than a security deposit for the secured credit card).

Recommended: This is How to Leverage Business Credit to Transform Your Life

Partner Offers Overview

New businesses that show very low financial reserves won’t qualify for the Tillfull credit card, but will be directed to Biz2Credit for alternative funding. If you have multiple business bank accounts, consider connecting all of them to get more relevant offers. I caution against connecting bank accounts in poor standing.

In addition to funding offers, Tillful might connect you with a new business banking or insurance offer. Especially since the company is fairly new, I assume they will continue to expand their partner offer — as of right now, it seems on par for a business just starting to build credit history (as long as you do your due diligence to make sure a better competitor offer doesn’t exist and pay your accounts responsibly).

Business Credit Education Overview

Tillful is built to help companies improve their credit (and to earn from partner commissions), so the offer wouldn’t be complete without business credit education. Tillful’s blog is stacked with information about how to improve your credit score, streamline your cash flow, create an effective budget, and learn about COVID-19 financial relief.

After browsing the blog, my official stance is that the information seems to be well-written, easy to digest, and helpful for businesses trying to build credit.

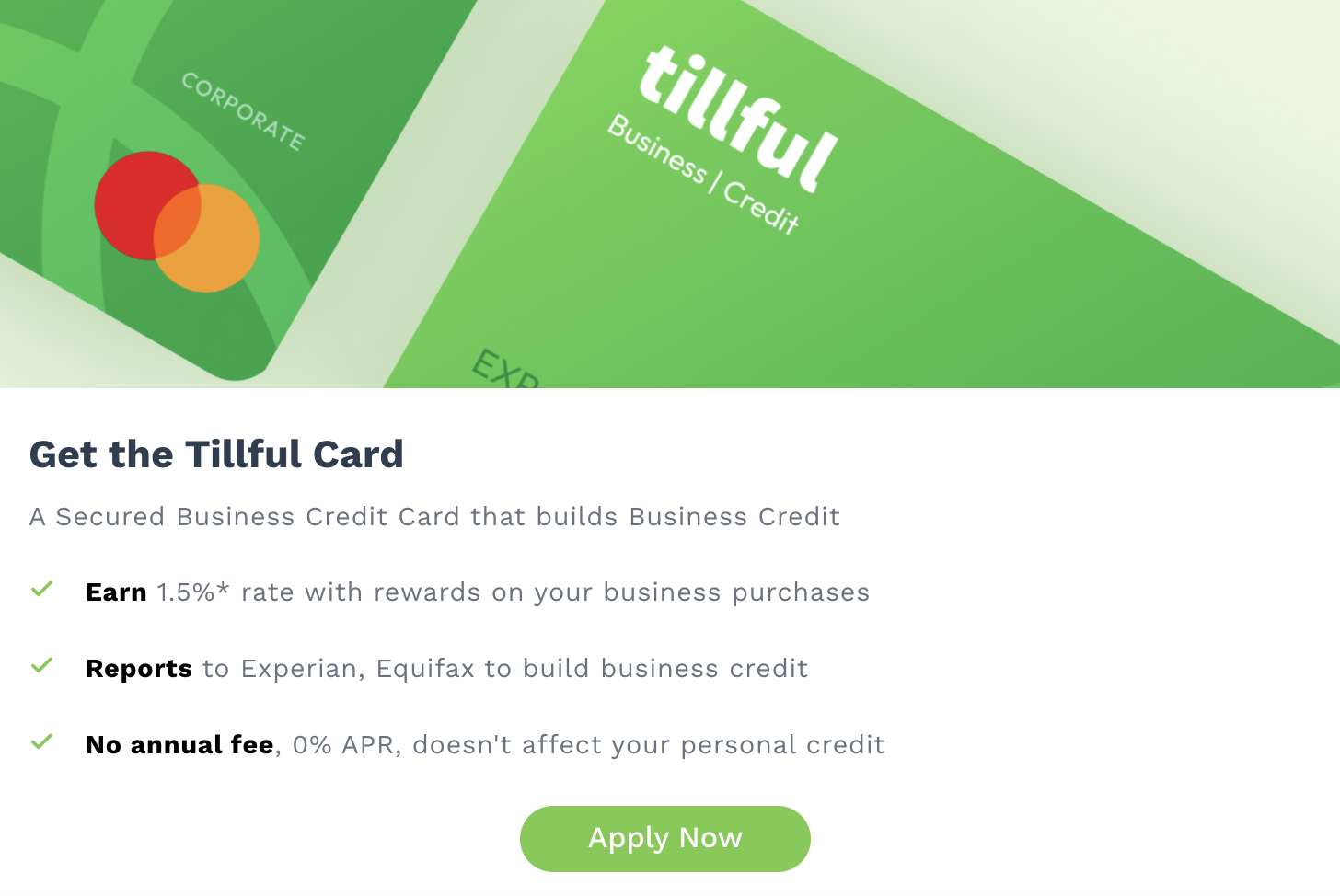

The Tillful Credit Card

The Tillful business credit card is a secured card for legal entities. Like a charge card, the balance should be paid in full each month. Unlike other secured business credit cards, Tillful uses Plaid to connect to your business bank account, sizes up your cash flow and reserves, then makes an offer to apply if you are likely to qualify.

One highlight is that this card comes with 1.5% cash back rewards on all spending. If you read the fine print, this is a promotional rate, which means rewards could decrease over time. Next, there is no personal guarantee. Finally, there’s no hard pull to an applicant’s credit.

Currently, the card reports payments to business credit bureaus to help build business credit scores. Tillful plans to report to Dun & Bradstreet in the near future.

Since it is a secured card, you will be required to deposit funds into your account, and the minimum security deposit is $500.

The Tillful App

If you didn’t already guess, Tillful also has an app available on the iOS App Stores. It has a 4.4-star rating on the platforms. So, users can conveniently monitor business credit and apply for funding from an Apple device. Thus far, there is no Tillful app in the Google Play store (you might just as easily log in using your mobile browser).

Using the app, you can get your free business credit score and see financial product recommendations, including funding options. It’s pretty straightforward.

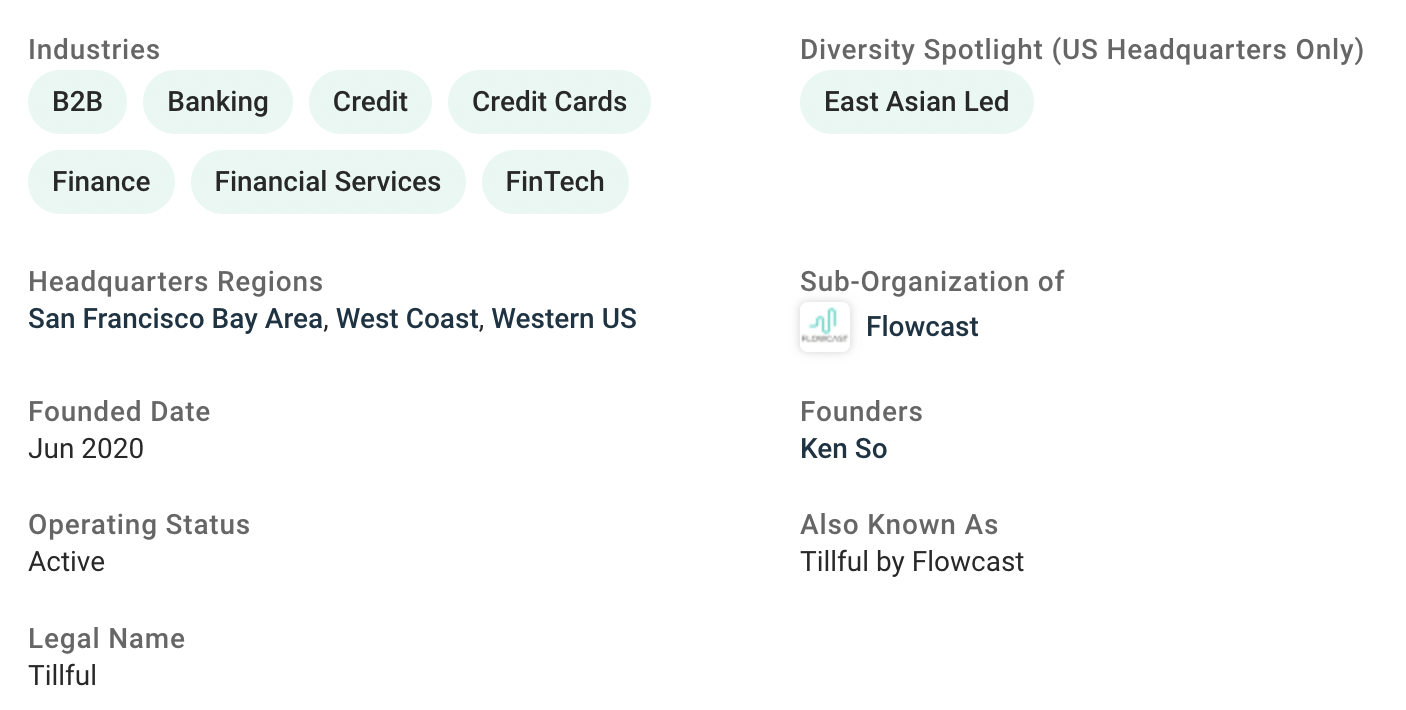

Tillful Company Overview

Located in the San Francisco Bay area, Tillful was founded by Ken So in June 2020. Tillful is a subsidiary of Flowcast, which is a company that uses AI to help financial institutions make credit decisions (hence the fast friends situation with Experian).

Flowcast has been around since 2015, and has a five-star glassdoor rating. So, from what I can tell, they’re a great company to work for — in full disclosure, there are currently only two reviews, so this isn’t a particularly scientific sample to base opinions on.

So, let’s talk about the founder, Ken So (also Flowcast’s CEO). Before all of this, So was the Director of Corporate Development at Ericsson and previously worked in the corporate dev department at Qualcomm – both very reputable companies. To me, this seems like a strong and trustworthy leader and makes me believe the offer is likely to be around for a while.

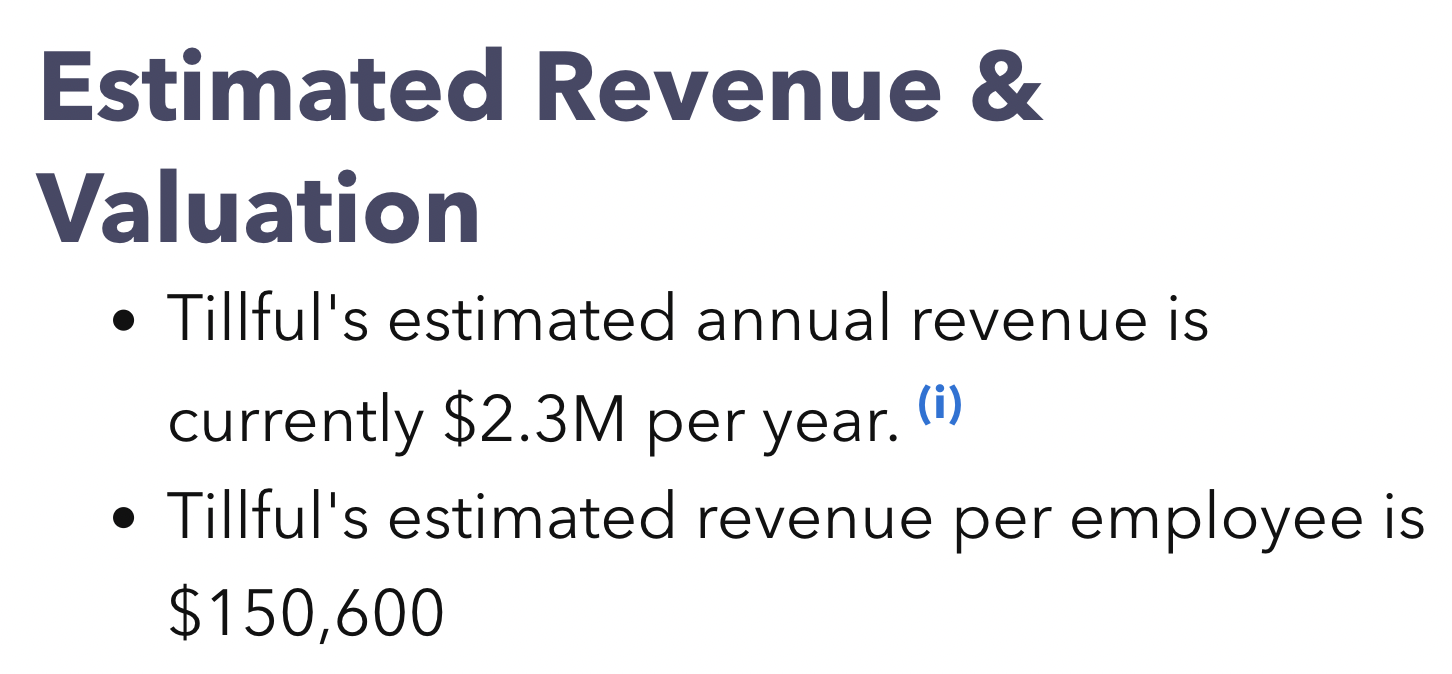

According to Growjo.com, Tillful’s current annual revenue is estimated at $2.3 million. And, since they’re not reliant on external funding, they’re likely at an advantage over other newcomers in the business credit-building arena.

Frequently Asked Questions

Here are the answers to the questions people are asking about Tillful:

Is Tillful free?

Yes, Tillful’s offer is completely free – users can access their credit score and secured credit card. However, any partner offers that Tillful recommends may charge fees and interest.

Does Tillful do a hard inquiry?

No, Tillful does not do a hard pull on business or credit reports. Instead, credit card approval is based on other factors.

Does Tillful report to credit bureaus?

Yes, Tillful reports payment history to business credit bureaus, as the credit card offer is intended to help entities build credit.

Which credit bureaus does Tillful report to?

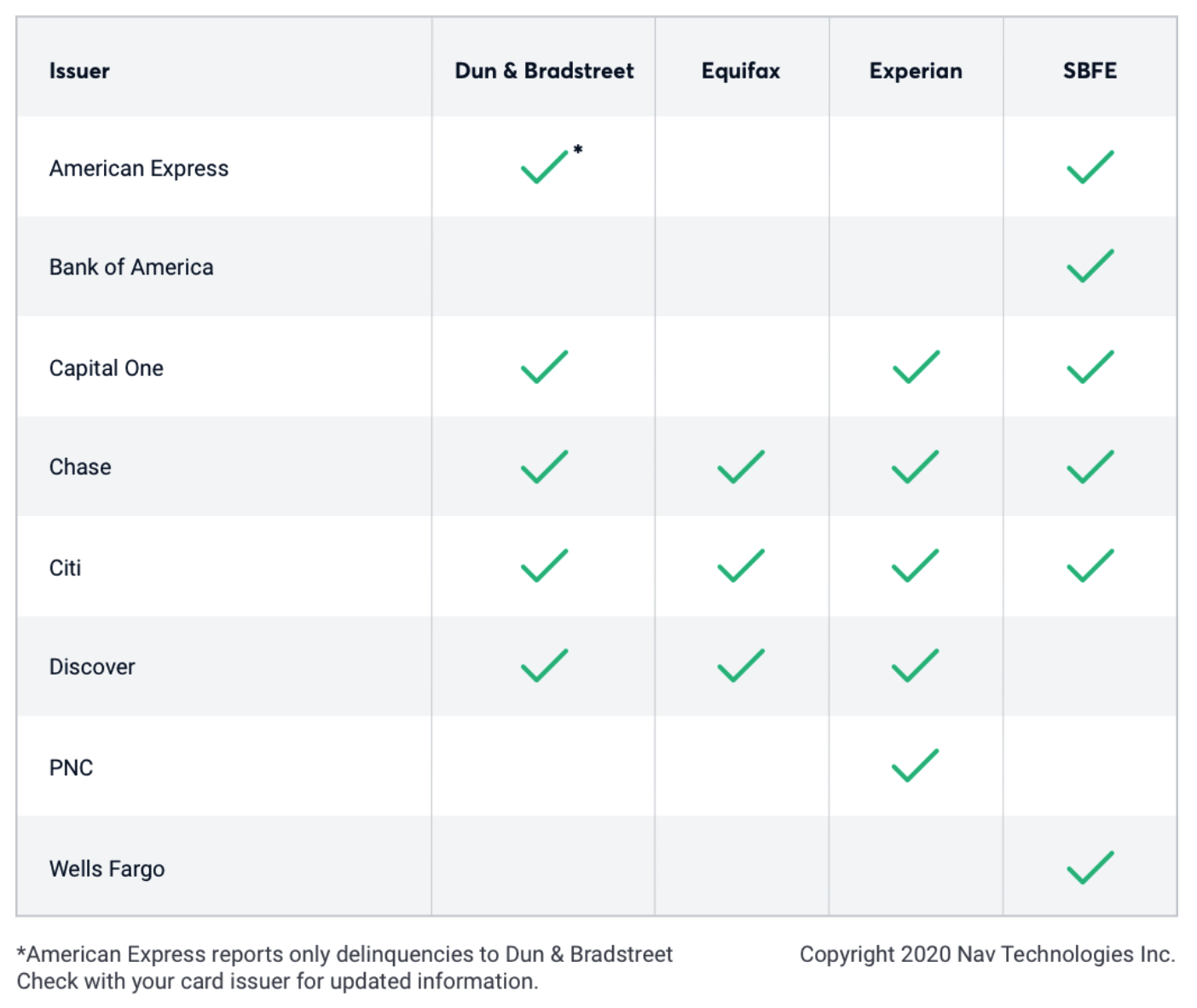

Currently, Tillful reports payments to Experian and Equifax Business.

Does Tillful report to Dun & Bradstreet?

Unfortunately, no. As of October 2022, Tillful does not report on-time payments to D&B or Equifax Business. However, they plan to in the near future.

Tillful Secured Credit Card Competitor Overview

Tillful is not the only secured business credit card on the market — a couple of veterans still exist: Bank of America (BoA) and First National Bank of Omaha (FNBO). See how these three secured business credit cards stack up next to one another.

The key tradeoff with the Tillful secured card is that you should pay your account in full each month, while the other available cards have revolving terms — you can make a monthly minimum payment if you choose, so there’s a bit more freedom with the old-timers.

However, monthly minimums come with the risk of high fees and interest; with the Tillful secured business credit card, if you make your payments as agreed, you’ll avoid this. Now, if you pay a BoA or FNBO card in full each month, you will avoid interest charges, so these offers almost balance each other out, not factoring FNBO’s $39 annual fee.

Tillful is available with a smaller minimum credit line. So, businesses with less cash in reserves are more likely to qualify. Plus. Tillful does no hard pull to your credit and there is no personal guarantee (the business owner is not liable for repayment of the funds — the business is), which is not the case with BoA or FNBO.

If I were going to use a secured credit card to establish business credit, I would choose Tillful over BoA or FNBO.

The Verdict: Is Tillful the Real Deal?

Of course, the question I was most interested in answering when I started down the Tillful rabbit hole is whether or not this is a good offer for building business credit. After some digging, it appears that this is a legitimate offer with a ton of potential. The offer is free, the company will help businesses improve credit (with on-time payments, anyway), and the brand is transparent about what they provide.

Right now, the biggest downside to Tillful’s offer is that they do not report on-time payments to D&B. To report to D&B, companies need at least 300 active accounts. So, I think it is likely that Tillful will do this in the future, in which case I would probably give the offer a 5-star rating (when appropriately utilized).

With that said, Tillful does currently report payments to Experian Business, and they claim that they will be reporting to Dun & Bradstreet as well as Equifax Business soon. Whether they deliver on that offer is yet to be seen, but do keep your eyes peeled.

Note that as far as business credit monitoring platforms, I’m still a bigger fan of Nav — mostly because I have more trust in established companies (Plus Nav has an Android app). But, I do encourage you to check out both offers and see which one you like best.

I teach a seven-step process to get up to $100K in business credit in as few as 30 days by leveraging the right combination of offers and setting up your business the correct way. If you’re interested in learning exactly how it works, join Business Credit Workshop today.