I’ve been really excited to review Bluevine since so many people have asked me about it. This is a free small business checking account offer that earns 50X the national average interest with no monthly fees or minimum deposits. Of course, they can’t possibly cater to every business owner… Can they?

That’s what we’ll explore here.

- Bluevine Business Checking Overview

- Bluevine Company Overview

- Frequently Asked Questions

- The Verdict: Is Bluevine Legit?

Now, let’s fire away!

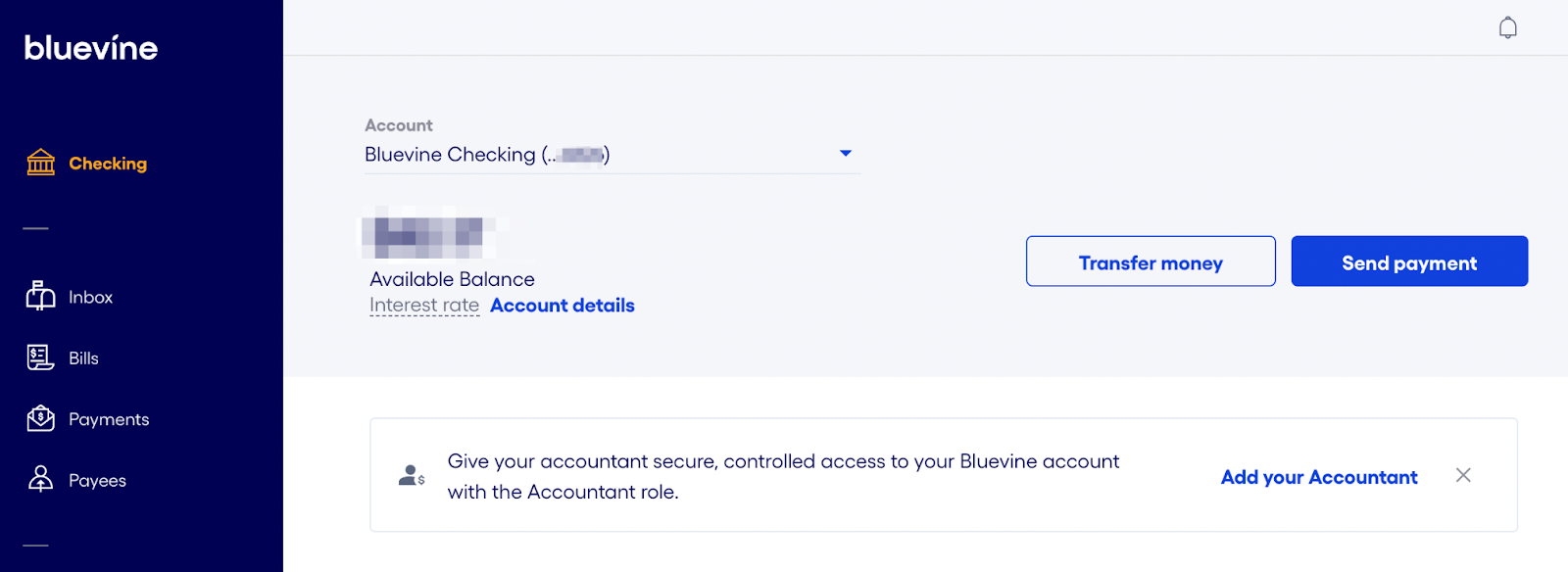

Bluevine Business Checking Overview

Bluevine offers free, single-user business checking accounts that can earn 2% interest on up to $100K with qualifying activity. There are no minimum deposits or NSF fees, which is incredible.

One standout feature that Bluevine doesn’t seem to advertise much is the ability to give your bookkeeper access to your account without sharing your dedicated login information — this can come in handy!

To qualify for interest accrual, account holders must meet at least one of the following requirements:

- Spend $500 with your Bluevine debit card in a calendar month OR

- Receive or deposit $2.5K via ACH, mobile deposit, wire transfer, or via a merchant payment processor (not ATM).

Bluevine uses the MoneyPass ATM network, with 37K locations nationwide. So, if you’re super rural, you may not be able to access a surcharge-free ATM. In this case, you would pay $2.50 for every ATM transaction.

While most services are free online and within the MoneyPass network, Bluevine charges $4.95 for all cash deposits made at an ATM. This might be steep for a business that makes multiple cash deposits, but online businesses wouldn’t be affected much.

There are no limits to the number of transactions that can be made in a Bluevine account, but cash transfers are limited to $1.5K per transaction, $2K per day, and $7.5K per month.

| Pros | Cons |

| Free checking with no monthly fees | No joint accounts |

| 2% interest on balances up to $100K | Minimum requirements to collect interest |

| No minimum deposits | $7.5K maximum monthly cash transfers |

| Sub-accounts with dedicated account numbers | $2.50 fee for out-of-network ATMs |

| Unlimited, fee-free transactions | No branch access (ATM-only) |

| No NSF fees | $4.95 fee for cash deposits |

So, a Bluevine checking account seems like a fantastic option for certain businesses. The offer seems to be catered to accountants, bookkeepers, freelancers, and other service businesses that primarily conduct digital transactions.

Naturally, there are businesses that Bluevine isn’t going to work well for.

For one, partnerships might not be a great fit, since only one account holder is permitted for each account. Next, super rural businesses without easy access to MoneyPass ATMs might end up paying quite a bit in surcharges (assuming you would need ATM access). Finally, this offer is simply not well-suited for businesses that need to deposit more than $7.5K in cash monthly, as that’s where Bluevine maxes out.

Fun Fact: Bluevine checking is powered by Coastal Community Bank, which is also the servicer for the X1 credit card.

Bluevine’s Line of Credit

Bluevine offers lines of revolving credit up to $250K, with rates as low as 4.8%, serviced by Celtic Bank. Once approved, you can get access to funds quickly. Note that the advertised interest rate is “simple interest,” which means compounding isn’t accounted for, and the low 4.8% is based on a 26-week repayment plan.

You can apply for a line of credit online in minutes. Bluevine uses Plaid to connect to your bank account and analyze cash flow. To qualify, you must have been in business in the U.S. for at least 6 months, have at least $10K in monthly revenue, and have a personal FICO score of 625 or higher.

According to at least one satisfied lendee, you cannot apply for a Bluevine loan using your Bluevine checking account, which seems a little wonky. Hopefully, they will update their lending platform to work with their own bank at some point in the future. But, as of now, there doesn’t seem to be a workaround.

If you apply and are approved for a Bluevine line of credit, you can choose to wire transfer funds for access within a few hours and a fee of $15. Alternatively, you can choose an ACH deposit, which can get your funds to you as soon as the next business day (however, in some cases this can take a few days).

Recommended: Meet Celtic Bank: A Humble Brand With an Enormous Reach

Bluevine’s Bill Pay

If you have the banking information for your payees, you can add them manually in your Bluevine account dashboard. I feel like online check services like Checkbook.io might be easier to use, since you only need an email address and name to deliver payments. But, bill pay is a nice feature for any bank account.

Moreover, you can connect Bluevine to Quickbooks to view income and expenses from your checking account dashboard.

Bill pay funds are held by Silicon Valley Bank, a trusted FDIC-insured institution. All-in-all, I think Bluevine’s bill pay options are competitive.

Bluevine Company Overview

Bluevine Inc. was co-founded in July 2013 by Eyal Lifshitz, Moti Shatner, and Nir Klar in Redwood City, California. The company started as an invoice factoring company, offering capital loans from $5K to $50K with “cash in as fast as 1 day.” They exited the factoring game and announced their free checking account offer in early 2020.

I found this gem from 2014 in the Wayback Machine:

Frequently Asked Questions

What happened to Bluevine?

There are a few rumors floating around that Bluevine is not accepting new applications. This is not the case — Bluevine is accepting new applications for lines of credit and new bank accounts. The rumor that they were closed may have started when PPP funding ended, as Bluevine was an approved lender for the Paycheck Protection Program.

Is Bluevine accepting new applications?

Yes! Despite the hearsay, Bluevine is currently accepting applicants for business checking accounts and lines of credit.

Does Bluevine run a credit check?

Yes, Bluevine runs a credit check for applicants looking for a line of credit. For approval, applicants must have a FICO score of 625 or higher.

Does Bluevine do a hard pull?

For businesses organized as an LLC, Bluevine does not do a hard pull, so applicants’ credit will not be negatively impacted.

What bureau does Bluevine pull from?

Bluevine has a partnership with Experian, Equifax, and Dun and Bradstreet, and reports on-time payments to all three.

Does Bluevine affect credit score?

Since they report payments to business credit bureaus, on-time payments to Bluevine will have a positive impact on your credit score.

Does Bluevine charge a fee?

The only fees Bluevine charges for checking accounts are ATM fees for cash deposits. Most ATMs within the MoneyPass network are surcharge-free for Bluevine account holders.

How much can I withdraw from Bluevine?

The maximum amount you can withdraw from Bluevine is $1,500 per transaction, $2,000 per day, and $7,500 per month

Is Bluevine a direct lender?

No. Bluevine’s lines of credit are serviced through Celtic Bank.

Who owns Bluevine?

Bluevine was founded by Eyal Lifshitz, Moti Shatner, and Nir Klar, who still currently own and operate the company.

What credit score does Bluevine use?

Bluevine uses applicants’ FICO scores to determine creditworthiness.

Is Bluevine FDIC insured?

Bluevine checking accounts, loans, and bill pay funds are FDIC insured through the respective banks that service these offers (Coastal Community Bank, Celtic Bank, and Silicon Valley Bank).

How many customers does Bluevine have?

As of February 2022, Bluevine had 450K customers.

The Verdict: Is Bluevine Legit?

Yep! This business checking offer is legit, and I would go as far as to say that I recommend it… for some business owners, namely accountants, freelancers, and other entities that conduct mostly digital banking. However, if you move a lot of cash through your company, or you have more than one owner, Bluevine probably isn’t your best option.

As far as Bluevine’s line of credit, I do trust offers from Celtic Bank, but I’m not the biggest fan of these fast-cash-type offers that use the owner’s personal FICO score to determine creditworthiness. Instead, I like to teach business owners to obtain credit using their business credit. What I do like is that Bluevine reports payments to D&B. So, with responsible payments, a Bluevine loan can help you build business credit.

If you’d like to learn how to obtain up to $100K in business credit in as few as 30 days, join Business Credit Workshop today.