Looking to get into the world of aged shelf companies? You’re in the right place! Aged shelf companies, also known as blank check companies or ready-made businesses, are like the fine wine of the business world – they’ve been sitting on the shelf, waiting for the perfect moment to shine.

In this guide, we’ll take you on a journey through the ins and outs of aged shelf companies, from what they are to where to find them.

Here’s what’s in store:

- What are Aged Shelf Companies?

- Why Buy an Aged Shelf Corporation?

- How to Find Aged Shelf Companies for Sale

- How to Protect Yourself From a “Bad” Shelf Company

- FAQ

- Final Thoughts

Now, let’s get to it!

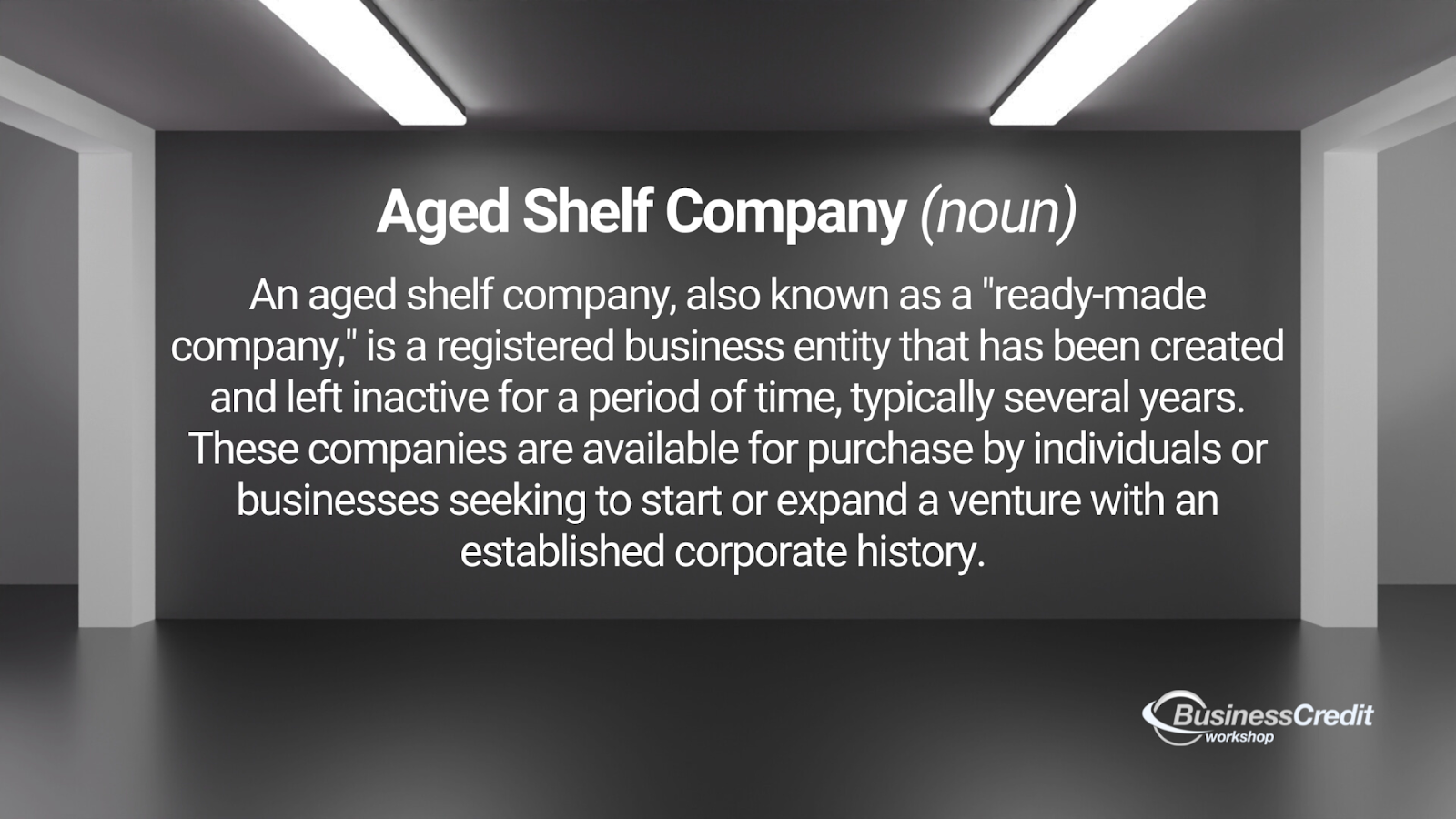

What are Aged Shelf Companies?

Also known as blank check companies, ready-made companies, or simply “aged” companies, aged shelf companies are registered entities that have had no activity. Think of it as setting your business on a shelf to age like a bottle of wine.

See our discounted offer on an Aged Shelf Corp for sale (plus our best training included for free). Just click Add to Card below

Like wine, when the right conditions are met, a business can improve when aged. Except, rather than enhance the flavor, a shelved company establishes corporate history and, when opened, can expedite business processes.

Note: Shelf companies are not to be confused with “shell corporations,” which are typically empty entities used for concealing ownership, avoiding taxes, or engaging in illicit activities.

What are the Characteristics of a Shelf Company?

In a nutshell, aged shelf companies have been around for several years or more, often decades, and remain inactive since their creation. They have a clean financial and operational history, with no debts or liabilities.

Now, let’s find out how much a shelf corporation costs and the considerations involved.

How Much Does a Shelf Corporation Cost?

So, how much does it cost to snag one of these shelf corporations? Well, it’s kind of like buying anything vintage – the price can vary, and it depends on several factors:

- Older shelf corporations tend to cost more because they’ve got that longer corporate history going for them.

- Where it’s registered matters. Some places have higher fees and maintenance costs.

- The person or entity selling the shelf corporation sets the price – It can be influenced by demand and what extras they throw in.

- Some sellers offer stuff like help with transferring ownership or handling compliance, which can affect the price tag.

- If the company’s got a snazzy name or a certain legal structure, that can drive up the cost.

- Sometimes, you get additional documents like articles of incorporation or organization and credit reports, which can bump up the price.

- The demand for shelf corporations in a particular area or industry can make the prices go up or down.

See: Low-Risk NAICS Codes +Best SIC Codes for Business Credit

Prices can range from a couple hundred bucks up to ten grand, so do your homework – think about what you need and make sure to check for any hidden surprises before you dive in!

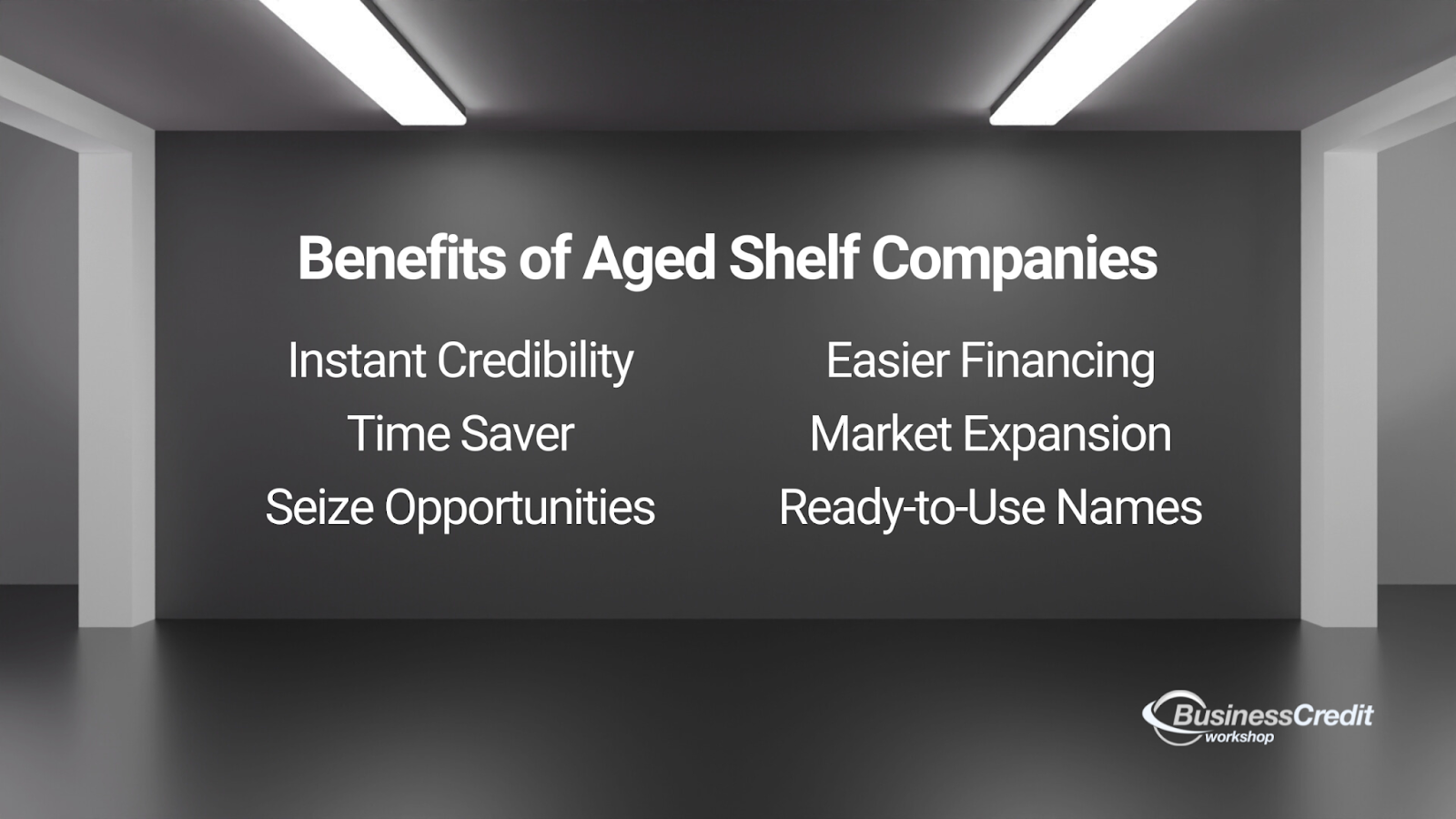

Why Buy an Aged Shelf Corporation?

Now, let’s talk about why some folks choose to snag an aged shelf company—it’s kind of like thrift shopping for businesses.

Here’s why you might want to buy one:

- Instant street cred – These old-timers have been around the block for a while, so your business looks legit right from the start. Customers and partners might trust you more.

- Skip the line – Instead of waiting in line to set up a brand-new business, you can waltz right in with a shelf company. Quick and easy, no fuss.

- Grab opportunities – Sometimes, to get certain contracts or loans, you need a business with a bit of history. Shelf companies meet those requirements with style.

- Borrowing made easy – If you need cash, lenders often prefer companies with a few years under their belt. With an established business, getting business credit can be smoother.

- Blink and You’re In – Expanding your business into new markets? A shelf company can help you jump through those legal hoops faster.

- Name Game – If the shelf company has a cool name, you can use it without the hassle of registering a new one.

- Tailor-Made – When you choose a shelf company that fits your business strategy, it’s like a ready-made suit, but for your business.

Next, let’s look at what you can do with them.

Recommended: This is How to Leverage Business Credit to Transform Your Life

What do People Do With Shelf Companies?

So, what’s the deal with shelf companies? Well, folks use ’em for all sorts of reasons.

Imagine you’re in a hurry to kickstart a business or snag some sweet contracts. A shelf company’s like a shortcut because it’s been around for a while, making your new venture look trustworthy right from the get-go. Plus, if you need loans or want to expand into new markets, having a seasoned business can make things way smoother. You can also protect specific assets or use a snazzy business name without the usual hassles.

Maybe you’re already working a business, but you’re unincorporated. An aged shelf company offers a nice way to slide right into the

But here’s the catch: before you take the plunge, do some digging. Not all shelf companies are the same, so be sure to check for any hidden surprises.

How to Find Aged Shelf Companies for Sale

State Secretary of State (SOS) offices typically maintain records of registered business entities, including corporations and LLCs.

However, while you can find information about existing businesses and their registration status through the SOS office, you typically won’t find aged shelf companies specifically listed for sale in these government databases.

Aged shelf companies are usually sold by individuals or businesses in the private sector, often through business brokers, legal and financial services, online marketplaces, or other commercial channels.

If you’re interested in purchasing an aged shelf company, you would typically need to search for listings or consult with professionals and businesses that specialize in providing aged shelf companies for sale. These sellers acquire and maintain shelf companies and then offer them for purchase to individuals and businesses seeking to expedite the startup or expansion of a new venture.

Finding aged shelf companies for sale can be relatively straightforward with the right approach. Here’s how to go about it.

Certainly, let’s break down how to use each channel to secure an aged shelf company, along with the pros and cons of each approach:

1. Online Business Brokers

Numerous online business broker websites specialize in selling aged shelf companies. These platforms list various aged corporations available for purchase, complete with details about their age, location, and price. You can search and filter listings to find the one that suits your needs.

- Visit reputable online business broker websites like Corporations Today Inc. or BSC & Associates.

- Seek out aged shelf companies that match your criteria.

- Review listings, including details on age, location, and price.

- Contact the broker to express your interest and inquire about the purchase process.

Pros:

- Wide selection of shelf companies.

- Detailed listings with essential information.

- Broker assistance with the purchase process.

- Potential for competitive pricing.

Cons:

- Broker fees may apply, increasing the overall cost.

- Limited opportunity for direct negotiations with the seller.

2. Legal & Financial Services

Some law firms and financial services companies offer aged shelf companies as part of their services. They can provide guidance on the purchase process, ensure legal compliance, and help with the transfer of ownership.

- Consult law firms or financial service providers like Companies Incorporated or AmeriLawyer that offer aged shelf companies.

- Discuss your specific needs and budget with the service provider.

- Review available shelf companies in their inventory.

- Work with the service provider to complete the purchase and transfer of ownership.

Pros:

- Expert guidance on legal compliance.

- Streamlined purchase process.

- Assistance with ownership transfer.

- May include additional services such as registered agent services.

Cons:

- Costs may be higher due to bundled services.

- Limited selection compared to online listings.

3. Business Directories

You can check business directories or databases for companies that offer shelf corporations. Look for contact information and inquire about their available inventory.

- Explore business directories or databases.

- Identify companies offering shelf corporations for sale.

- Contact the companies directly to inquire about available aged shelf companies.

Pros:

- Direct access to potential sellers.

- May find local options easily.

- Direct communication with the seller.

Cons:

- Limited information available in directories.

- May require extensive outreach and research.

- Limited selection compared to specialized platforms.

4. Networking

Connect with entrepreneurs, business consultants, or professionals in your industry who may have knowledge of or access to shelf companies for sale. They might provide valuable recommendations or leads.

- Network with entrepreneurs, business consultants, or industry professionals.

- Share your interest in acquiring a shelf company.

- Seek recommendations or referrals from your network.

Pros:

- Personalized recommendations.

- Potential for insider information.

- Trustworthy referrals from known contacts.

Cons:

- Networking may take time.

- Reliance on others to provide leads.

- Limited control over the selection process.

5. Online Marketplaces

Explore online marketplaces like eBay or Flippa, where sellers occasionally list aged shelf companies for sale. Be sure to conduct due diligence and verify the legitimacy of the seller and the company being offered.

- Search online marketplaces like eBay for aged shelf companies.

- Review listings, including seller ratings and descriptions.

- Contact the seller to discuss the purchase.

Pros:

- Accessibility to a wide audience.

- Opportunity to negotiate directly with the seller.

- Transparency through ratings and reviews.

Cons:

- Limited availability of shelf companies.

- May encounter less reputable listings.

- Need for thorough due diligence on sellers.

6. Legal Notices

Check local or national legal publications or government websites for any notices about companies being offered for sale – This might lead you to aged shelf companies available in your jurisdiction.

- Check local or national legal publications or government websites for notices about companies for sale.

- Contact the parties offering shelf companies.

- Inquire about the available options.

Pros:

- Potential to find local opportunities.

- Information often publicly available.

Cons:

- Limited listings.

- May not be actively updated.

- Limited details in legal notices.

7. Industry Conferences & Events

Attend industry-specific conferences, trade shows, or business events. You may come across vendors or experts who offer aged shelf companies as part of their services.

- Attend relevant industry conferences, trade shows, or events.

- Network with vendors or experts in the field.

- Inquire about any aged shelf companies they may offer.

Pros:

- Direct access to industry-specific opportunities.

- Face-to-face interactions for building trust.

Cons:

- Limited availability during specific events.

- May not align with your timeline.

8. Business Associations

Join business associations or chambers of commerce related to your industry. Members often share information and resources, including opportunities to purchase shelf companies.

- Join industry-related business associations or chambers of commerce.

- Engage with fellow members and express your interest.

- Seek information or leads from association members.

Pros:

- Networking within your industry.

- Trustworthy referrals from association members.

Cons:

- Reliance on the association’s network.

- May require time for connections to develop.

9. Online Forums and Classifieds

Participate in online forums, classified ad websites, or social media groups like Reddit r/business where businesses are discussed, bought, and sold. Some individuals or companies may advertise aged shelf companies there.

- Participate in relevant online forums, classified ad websites, or social media groups.

- Engage with members and express your interest in purchasing a shelf company.

- Inquire about any listings or opportunities available.

Pros:

- Direct access to potential sellers.

- Informal and open communication channels.

- Potential for unique opportunities.

Cons:

- Limited oversight, requiring thorough due diligence.

- May encounter less reputable listings.

- Time-consuming to filter through various sources.

When searching for aged shelf companies, always exercise caution and conduct thorough due diligence.

How to Protect Yourself From a “Bad” Shelf Company

So, before you buy an aged shelf company, you want to make sure you’re not getting a lemon, right?

Here’s what you should do:

- Check the articles – Look at the company’s articles of incorporation or organization. Make sure they match up with what you want to do with the business.

- Review financial records – If you can, get your hands on financial statements. You’ll want to know if the company’s in good financial shape – It should have no debt.

- Verify ownership transfer – Ensure the ownership transfer process is legit and filed with the authorities. Get clear documentation of the transfer signed by both parties.

- Legal documents – Check if there are any undisclosed legal issues or obligations lurking in the company’s records. And make sure the registered agent and address are up-to-date.

- Credit package – If applicable, review any credit packages associated with the shelf company to understand any existing credit lines or financing agreements.

By going through these documents, you’ll have a better idea of what you’re getting into and can avoid any nasty surprises down the road. Be sure to verify the authenticity of the seller, review all of the company’s history and records, and consult legal and financial experts to ensure a smooth and secure transaction.

FAQ

Why do shelf companies exist?

Shelf companies are like prepped-up businesses waiting for action. They exist for folks who want to skip the startup hassle and dive into business with a history.

Do shelf companies pay taxes?

Yup, they’re not tax-free. Shelf companies, like any other business, need to pay taxes based on their income and location (if they have no income, their tax obligation would likely be $0).

Can you register a business in a state where you don’t live?

Absolutely! You can register a business in a state where you’re not living. It’s common for folks to do this to tap into specific business advantages or markets. But, if you are active in your home state, the business may need to be registered there as well.

Should you buy a shelf corporation?

Well, it depends on your needs. If you want a head start and a business with history, it’s an option. But, always do your homework and make sure it’s the right fit for your goals.

Final Thoughts

So, there you have it – the lowdown on aged shelf companies, from what they are to why you might want to buy one and how to protect yourself from any surprises. Whether you’re looking to kickstart a business with instant history or expand your current venture, aged shelf companies offer a unique shortcut.

But remember, it’s all about doing your homework, verifying the details, and making sure it’s the right move for your entrepreneurial journey. Cheers to your future business success!

Want to learn how to get up to $100K in business credit? Join Business Workshop today.

See our discounted offer on an Aged Shelf Corp for sale (plus our best training included for free). Just click Add to Card below