If you’re an agriculture business owner, you know that there are a lot of expenses involved in running your operation. From buying supplies to hiring employees, it can be tough to keep up with the costs. That’s where a business credit card can come in handy.

A business credit card can help you earn rewards on your purchases, which can be used to offset your business expenses. Plus, many business credit cards offer other benefits, such as travel insurance and purchase protection.

Here, we’ll explore the best credit cards for agriculture businesses, including popular options such as Capital One Spark Business, American Express, Tractor Supply Credit Card, John Deere Credit Card, and Affirm.

|  |  |  |  |

| 2% cash back on all purchases | No annual fee and 2X points on eligible purchases | Special financing and rewards on purchases | Flexible financing for John Deere products | Flexible financing with clear repayment plans |

| → Learn More | → Learn More | → Learn More | → Learn More | → Learn More |

We’ll also address common questions and concerns related to business credit cards for agriculture businesses.

Here’s what’s in store:

- What to Look for in a Business Credit Card

- Let’s Choose the Right Business Credit Card for Your Agriculture Business

- Frequently Asked Questions

- Wrapping Up

Now, let’s get goin!

What to Look for in a Business Credit Card

When it comes to choosing the right business credit card for your agriculture business, there are a few important factors to consider.

- Rewards – Find a card that offers relevant rewards, like cash back on fuel and farm supply store purchases. Earn rewards on these expenses to save money in the long run.

- Interest Rate – Carefully consider the card’s interest rate, especially if you plan to carry a balance. High rates can eat into your profits, so choose a card with an affordable rate or look for lower-rate options.

- Annual Fee – Some business credit cards charge an annual fee. Consider whether the benefits and rewards justify the cost. If you don’t expect to use the card extensively or the benefits don’t outweigh the fee, opt for a card with no annual fee.

- Features and Benefits – Look for additional features like travel insurance, purchase protection, or expense tracking tools. Choose a card that offers the features most important to your agriculture business, such as travel insurance for agricultural conferences.

By considering these factors, you can find a business credit card that aligns with your agriculture business’s needs and helps you save money while managing your finances effectively.

→ Recommended: 6 Best Business Credit Cards for Entrepreneurs: Fuel Your Growth

Let’s Choose the Right Business Credit Card for Your Agriculture Business

No matter what your business needs, there’s a business credit card out there that can help you save money and grow your business. Do some research to find the best card for you, and start taking advantage of the rewards and benefits today.

Here are some top credit card options to consider from major banks. Keep in mind that you may have better luck with a small local community bank or credit union.

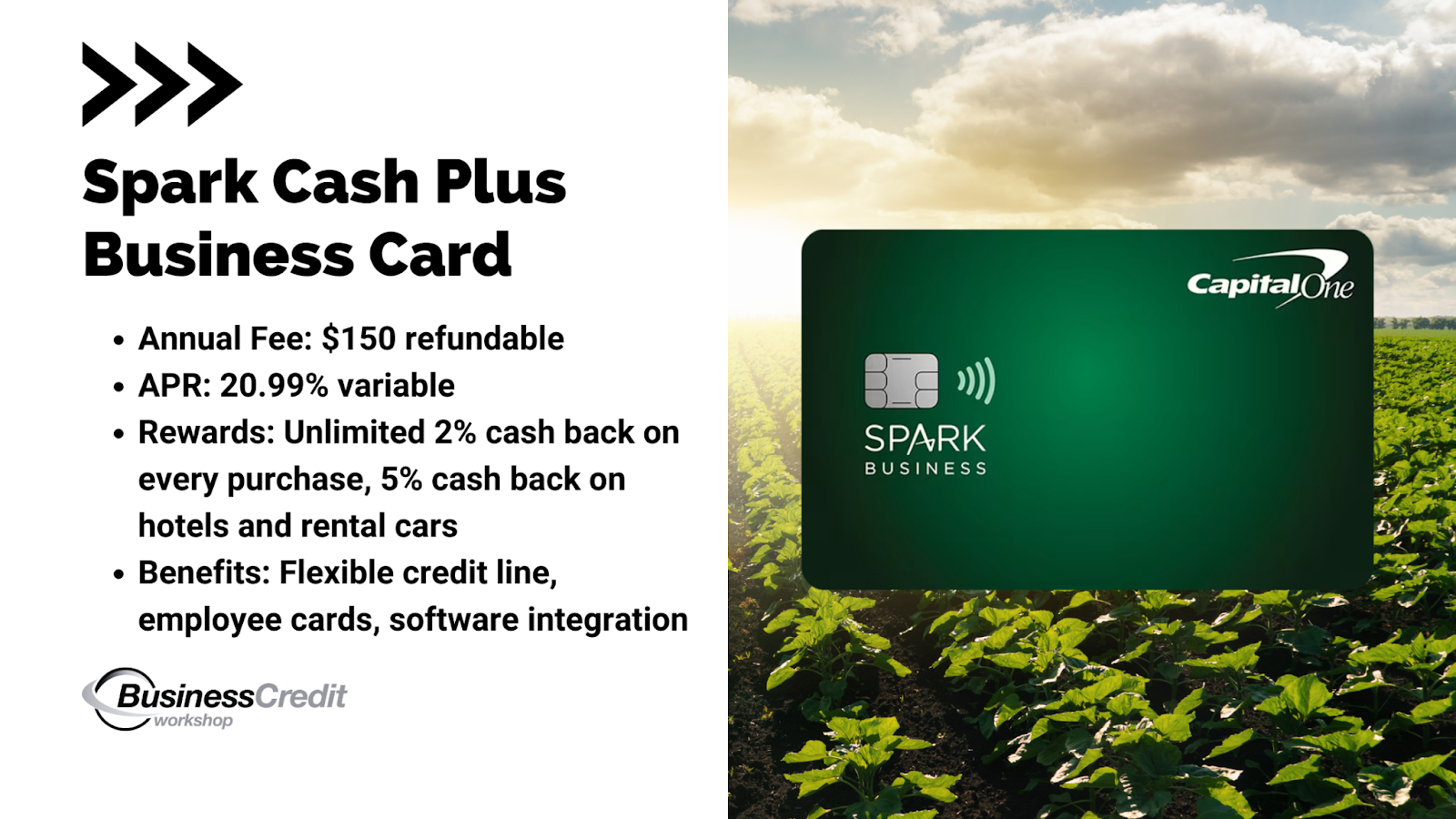

Spark 2% Cash Plus Business

Issuer: Capital One

Rewards: Earn unlimited 2% cash back on every purchase for your agriculture business. Additionally, you can earn unlimited 5% cash back on hotel and rental car bookings made through Capital One Travel.

Interest Rate: Variable purchase rate: 20.99% APR. The APR may vary with the market based on the Prime Rate.

Annual Fee: The Spark 2% Cash Plus credit card has an annual fee of $150.

Features and Benefits: This credit card offers several features and benefits that can be highly advantageous for an agriculture business. It has no preset spending limit, adapting to your business’s needs based on spending behavior, payment history, and credit profile.

If you spend at least $150,000 per year, you can receive an annual fee refund of $150. The card provides business-grade capabilities, including free employee and virtual cards, enabling your team to make purchases while earning rewards.

It also offers benefits such as:

- Account management tools

- Employee access

- Travel perks

- Fraud liability protection

- The ability to download purchase records in multiple formats for easy record-keeping.

Summary: The Spark 2% Cash Plus credit card is a valuable choice for agriculture businesses. With unlimited 2% cash back on all purchases, it allows businesses to earn rewards on their everyday expenses. The card’s business-specific features, such as free employee and virtual cards, empower team members to make purchases while earning rewards.

Additionally, the annual fee refund of $150 incentivizes higher spending. The card’s benefits, including account management tools, travel perks, fraud protection, and easy record-keeping, provide further convenience and protection for agriculture businesses.

Overall, the Spark 2% Cash Plus credit card can help agriculture businesses maximize their rewards, streamline purchasing processes, and enhance financial management.

American Express Blue Business Plus

Issuer: American Express

Rewards: Earn 2X Membership Rewards® points on eligible business purchases up to $50,000 per calendar year. After reaching the spending cap, you earn 1X points on other eligible purchases.

Interest Rate: The introductory APR on purchases is 0% for the first 12 months from account opening. After that, the APR becomes a variable rate ranging from 18.24% to 26.24%.

Annual Fee: The Blue Business® Plus Credit Card has no annual fee, making it a cost-effective choice for agriculture businesses.

Features and Benefits: The Blue Business® Plus Credit Card offers various features and benefits that can be beneficial for agriculture businesses. It provides cash flow flexibility through Expanded Buying Power, allowing you to make purchases above your credit limit based on your payment history, credit record, and other factors.

The card earns Membership Rewards® points, which can be accumulated quickly, offering potential rewards for your business expenses. Employee cards come with no annual fee, and you can earn points on their eligible purchases.

The card also offers expense management tools such as:

- QuickBooks® integration

- Online statements

- Account alerts

- A year-end summary for efficient budgeting and expense tracking

- Vendor Pay by Bill.com

- The American Express® App

- Dedicated customer service via Relationship Care®

- Insurance coverage, including Car Rental Loss and Damage Insurance, Extended Warranty, and Purchase Protection

Amex Blue Business provides added peace of mind for business transactions.

Summary: The Blue Business® Plus credit card is an excellent choice for agriculture businesses. With its rewards program, agriculture businesses can earn 2X Membership Rewards® points on eligible purchases. The introductory 0% APR for 12 months and no annual fee offer cost-saving advantages.

The card’s expense management tools, such as employee cards, QuickBooks® integration, online statements, and account alerts, help streamline financial management. The Vendor Pay feature simplifies bill payments, and the Year-End Summary aids in budgeting and tax preparation. The card also provides insurance coverage and access to the American Express® App for convenient account management.

With its valuable features and benefits, the Blue Business® Plus Credit Card can enhance cash flow, reward business spending, and provide essential financial tools for efficient operations in the agriculture industry.

Tractor Supply Co. Business Credit Card

Issuer: Tractor Supply Company (TSC)/ Citibank

Rewards: New cardholders receive a $20 reward with their first qualifying purchase of $20 or more. Earn 5% in rewards storewide on eligible Tractor Supply Co. purchases.

Interest Rate: Variable purchase rate: 30.99% APR (as of May 9, 2023). The APR may vary with the market based on the Prime Rate.

Annual Fee: The TSC card has no annual fee.

Features and Benefits: Deferred interest promotional offers:

- No Interest if Paid in Full in 6 Months

- No Interest if Paid in Full in 12 Months

- No Interest if Paid in Full in 18 Months

- No Interest if Paid in Full in 24 Months

Summary: The TSC Visa credit card provides attractive benefits for new cardholders, including a $20 reward with their first qualifying purchase and 5% in rewards storewide on eligible Tractor Supply Co. purchases. These rewards can be utilized to offset future expenses or used towards purchasing agricultural supplies and equipment.

Additionally, the card offers deferred interest promotional offers, allowing cardholders to make purchases and pay no interest if the balance is paid in full within specific periods of 6, 12, 18, or 24 months. However, if the balance is not paid in full by the end of the promotional period, interest charges will be imposed at the variable purchase rate of 30.99% APR.

Agriculture businesses can take advantage of these promotional offers to manage their cash flow effectively and make necessary purchases while avoiding interest charges if paid within the specified timeframes.

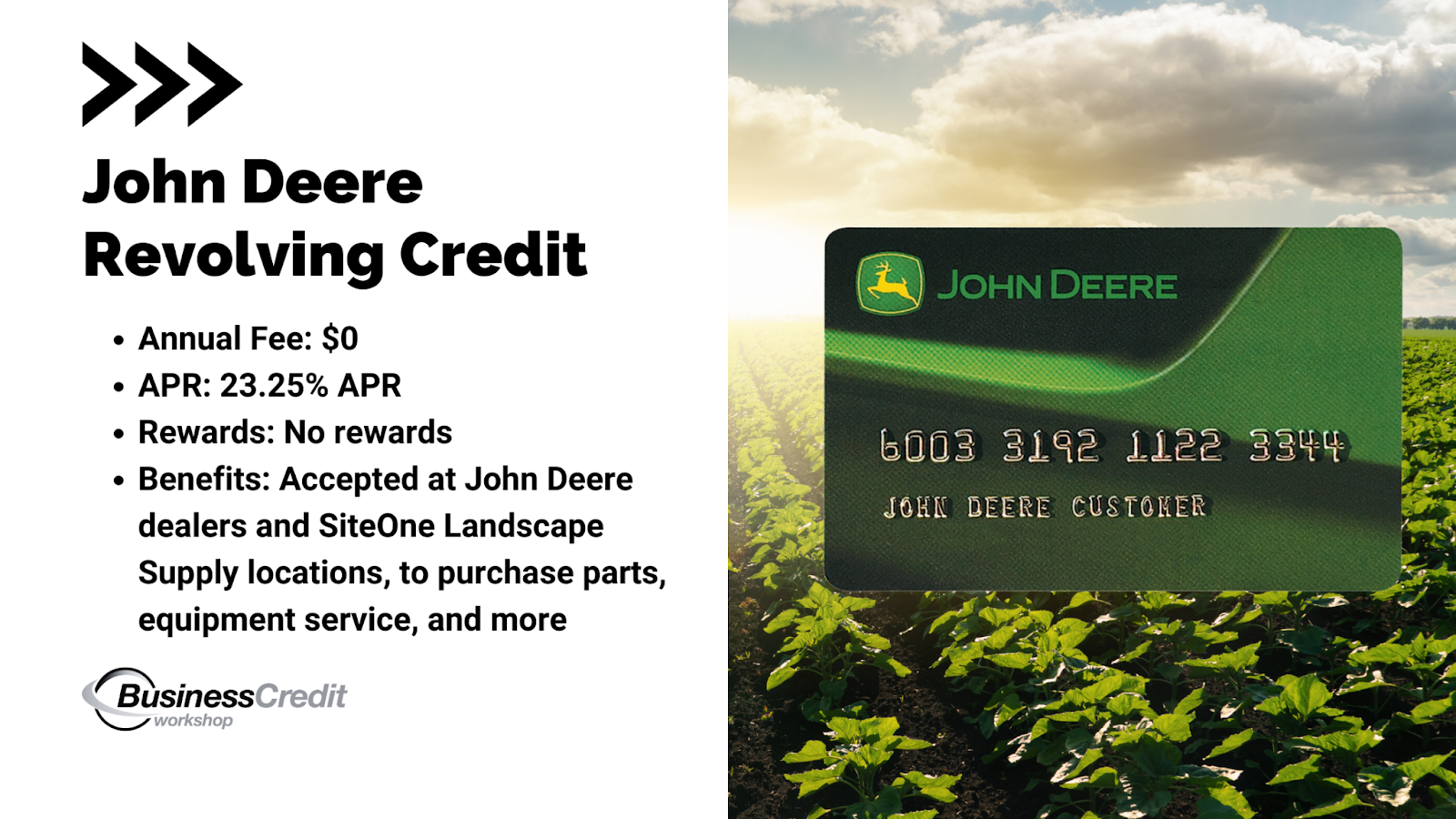

John Deere® Credit Card

Issuer: John Deere

Rewards: The John Deere Credit Revolving Plan Account does not explicitly mention a rewards program.

Interest Rate: The periodic rate is 0.06370% per day, which corresponds to an annual percentage rate (APR) of 23.25%. The periodic rate is 0.07192% per day, which corresponds to an APR of 26.25%

Annual Fee: The John Deere revolving credit account has no annual fee.

Features and Benefits: The account is accepted at John Deere dealers and SiteOne Landscape Supply locations, providing flexibility in purchasing parts, attachments, batteries, equipment service, and more. Consolidate all purchases into one easy-to-read statement, making it convenient to track expenses.

This card offers options for minimum monthly payments or full payment, providing flexibility in managing cash flow. And, account holders may receive special offers on equipment, parts, and service, providing potential cost savings.

Summary: The John Deere Credit revolving account offers a flexible line of credit for financing purchases related to John Deere products. The account provides convenient payment options with minimum monthly payments or the choice to pay in full. Account holders may benefit from special offers on equipment, parts, and service. However, it is important to note that the account has relatively high-interest rates, with a regular purchase rate of 23.25% APR and a default rate of 26.25% APR.

Despite the interest rates, the account can still be beneficial for an agriculture business as it offers convenience, consolidated statements, and access to necessary equipment and services from John Deere dealers and SiteOne Landscape Supply locations.

It allows businesses to manage their cash flow and make essential purchases to keep their operations running smoothly.

→ Recommended: Is a Floor & Decor Business Credit Card Still Worth It?

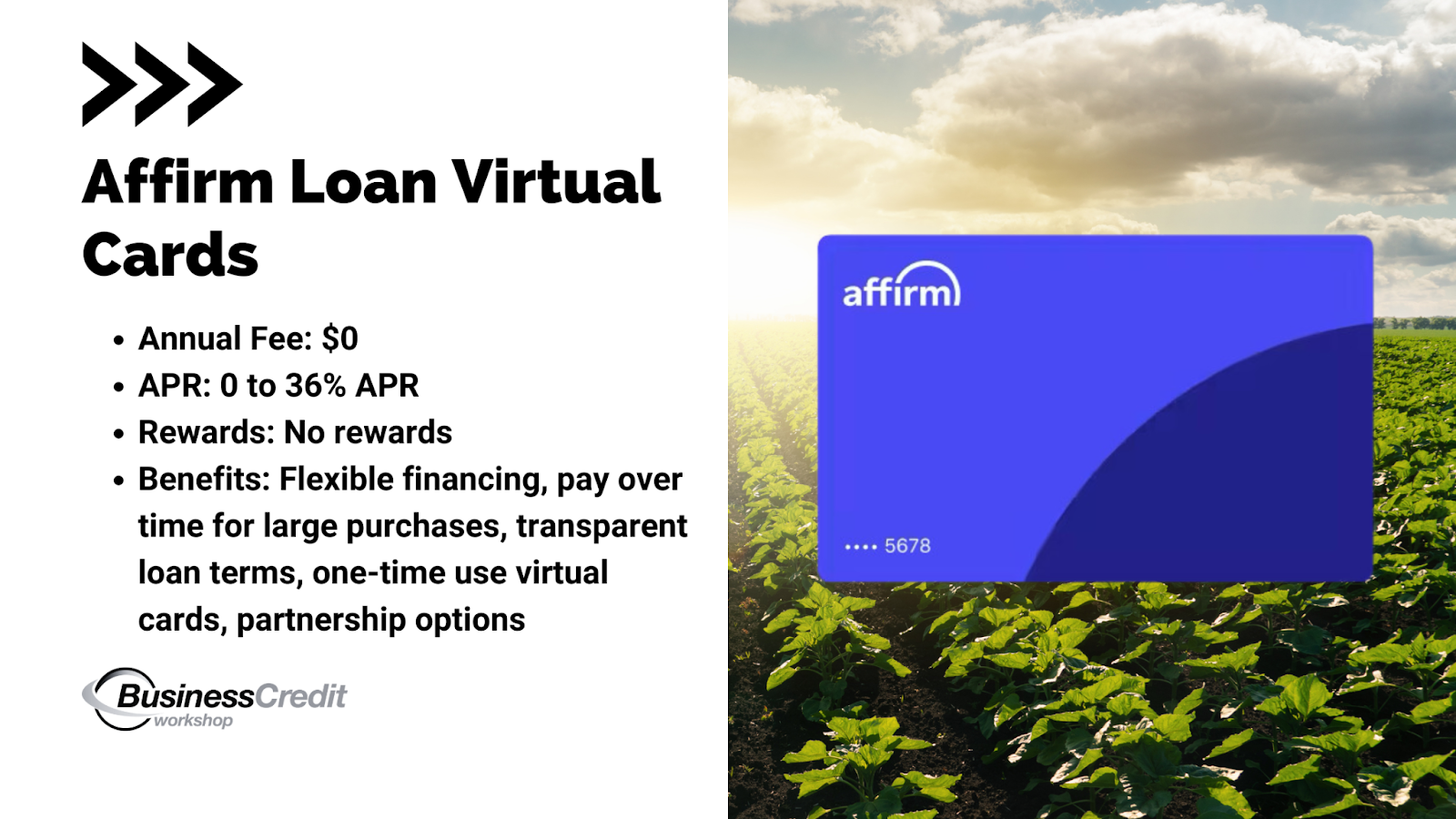

Affirm Virtual Card

Issuer: Affirm Loans

Rewards: Affirm loans do not offer traditional rewards or cashback programs.

Interest Rate: The interest rates for Affirm loans can range from 0% to 36% APR, depending on the customer’s creditworthiness and the specific loan offer.

Annual Fee: Affirm loans do not charge an annual fee.

Features and Benefits: Affirm loans provide flexible financing options for customers, allowing them to make purchases and pay over time with fixed monthly payments. The loan terms and interest rates are clearly disclosed upfront, ensuring transparency and enabling customers to make informed financial decisions.

Affirm loans also offer a user-friendly platform and a seamless application process, making it convenient for customers to access financing for their online purchases.

Summary: Affirm virtual cards provide a convenient and flexible financing option for customers, allowing them to make purchases and pay over time with fixed monthly payments. While Affirm loans do not offer traditional rewards or benefits, they enable customers to access financing with transparent terms and clear repayment plans.

Remember, the virtual card expires 24 hours after it’s issued. If you don’t use it, you won’t owe anything. You can cancel the card anytime before it expires without any obligations. It works with Apple Pay and Google pay. If you don’t use the full amount on your card, that’s okay. You’ll only owe the amount you spend, plus any accrued interest.

After the merchant processes your purchase, Affirm will provide a payment schedule for the full card amount. After 21 days (or longer, depending on the transaction), any unused funds will be returned, and the payment schedule will be updated accordingly. This means you may have a smaller final payment, fewer upcoming payments, or both.

Keep in mind that you can’t use your virtual card at merchants that violate Affirm’s Terms of Service, such as those selling firearms and alcohol.

While not a traditional business credit account, Affirm can help you with larger agriculture business expenses by giving you the ability to pay over time.

★ Note: This can also be beneficial for agriculture businesses as it expands the purchasing power of customers, making your products or services more affordable and accessible. By partnering with Affirm, you can attract more customers, increase sales, and enhance customer satisfaction by offering a convenient and transparent financing solution.

Frequently Asked Questions

What is credit card farming?

Credit card farming refers to the practice of obtaining multiple credit cards to take advantage of sign-up bonuses and rewards. However, it’s important to use credit responsibly and avoid accumulating excessive debt.

Can I use a business credit card for multiple businesses?

Generally, business credit cards are intended for use by a specific business entity. Using a single credit card for multiple businesses can complicate your financial records and accounting. It’s recommended to have separate credit cards for each business.

Do you need a DBA to open a business credit card?

While a Doing Business As (DBA) name can help you establish a separate business identity, it’s not always a requirement for opening a business credit card. Each credit card issuer may have its own criteria and guidelines. I usually recommend an LLC registered with a low-risk NAICS code.

Do I need a business bank account to apply for business credit?

Having a dedicated business bank account can demonstrate financial stability, but it’s not always mandatory for applying for a business credit card. Check with the credit card issuer to understand their specific requirements. I typically recommend businesses bank with a local community bank or credit union.

Can you have a business credit card with bad credit?

It may be challenging to obtain a business credit card with bad credit. However, some credit card providers offer secured credit cards or cards specifically designed for businesses with less-than-perfect credit – The best thing to do is fix your personal credit before you apply for business credit.

Can a nonprofit get a credit card?

Yes, nonprofit organizations can apply for business credit cards tailored to their specific needs. Many credit card companies offer cards designed for nonprofits, which may include features such as donation rewards or special nonprofit discounts.

Wrapping Up

Choosing the best credit card for your agriculture business requires careful consideration of your specific needs, rewards programs, fees, and flexibility. Explore options from trusted providers such as Capital One Spark Business, American Express, Tractor Supply, John Deere, and Affirm to find a card that aligns with your agricultural operations.

Remember to use credit responsibly, keep your personal and business expenses separate, and always pay your bills on time to build a positive credit history.

Wanna know a secret?

You can get much larger lines of business credit when you establish your entity properly, work with local small banks and credit unions, and follow a proven process.

Ready to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!