InDinero advertises itself as a business-saving solution to manage business accounting and taxes. And, may seem like a great, convenient option, especially when you want quick answers.

But, is InDinero everything it’s cracked up to be? Here, I’ll share everything I know about the platform, the company, and insights to help you decide whether this is the right answer for your business needs.

This is what’s in store.

Now, let’s roll!

What is InDinero?

InDinero is a comprehensive financial services company designed to assist businesses with various aspects of their financial management.

They offer services like:

- CFO (Chief Financial Officer) support

- Tax planning and filing

- Payroll

- Accounting

- Bookkeeping

Their CFO services provide strategic financial guidance, including budgeting, forecasting, and cash flow management to help you make informed decisions. For accounting and bookkeeping, InDinero aims to simplify financial processes, reduce errors, and enhance efficiency. They also specialize in tax planning to optimize strategies and minimize liabilities.

InDinero offers a blend of software and human support to handle complex financial tasks—It provides businesses with proactive advice and guidance to navigate the path towards growth and profitability.

You might also like: 1-800Accountant Reviews: Expectations vs Reality

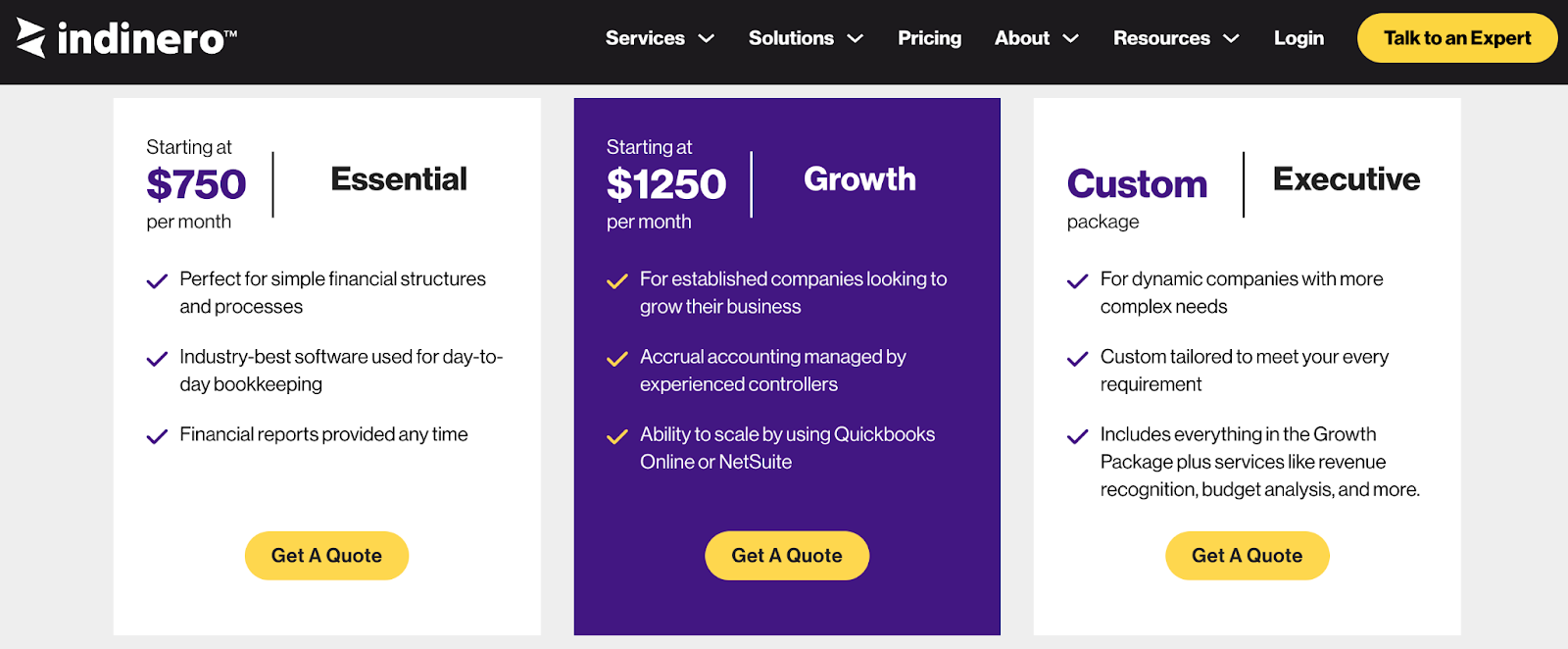

InDinero Pricing

InDinero offers three pricing plans tailored to different business needs:

- Essential package – Starting at $750 per month, this package is for businesses with straightforward financial needs to leverage top-notch software for daily bookkeeping and on-demand financial reports.

- Growth package – Starting at $1250 per month, this one’s ideal for established businesses looking to expand, managed by professionals who handle accrual accounting and facilitate scalability via platforms like Quickbooks Online or NetSuite.

- Executive package – With custom pricing, the executive package is tailored for dynamic businesses with complex needs and offers advanced services like revenue recognition, detailed budget analysis, and personalized solutions.

To get accurate pricing and ensure you receive the right services for your business, reach out to InDinero for a customized quote.

You might also like: Melio Payments Review: Can It Make Business Payments & Getting Paid Easier?

Company Overview

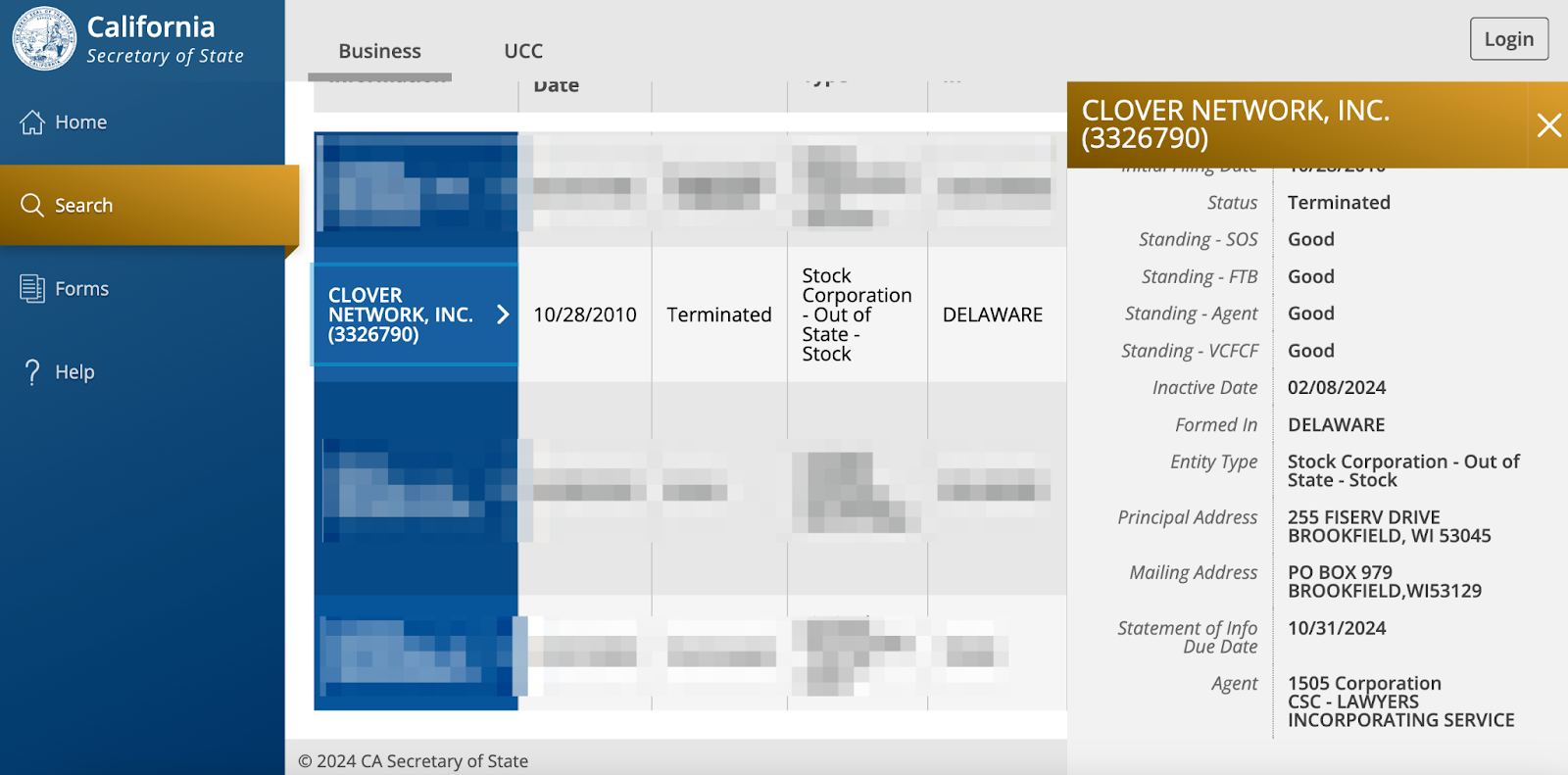

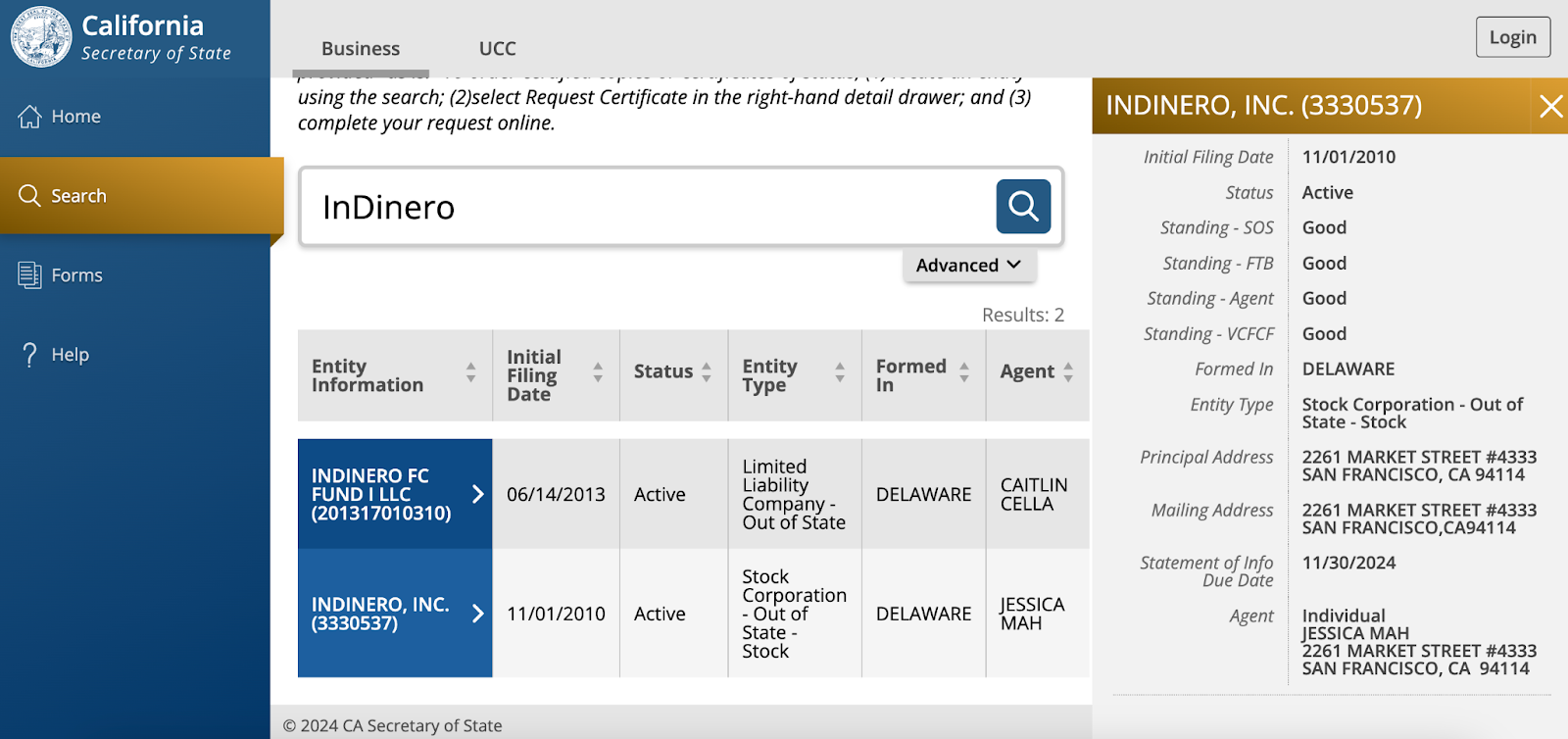

InDinero Inc. is a private, for profit, San Francisco-based company that was founded in 2009 by Jess Mah, Andy Su, and Andrea Barrica. The company is registered, active since 2010, and in good standing with California’s Secretary of State.

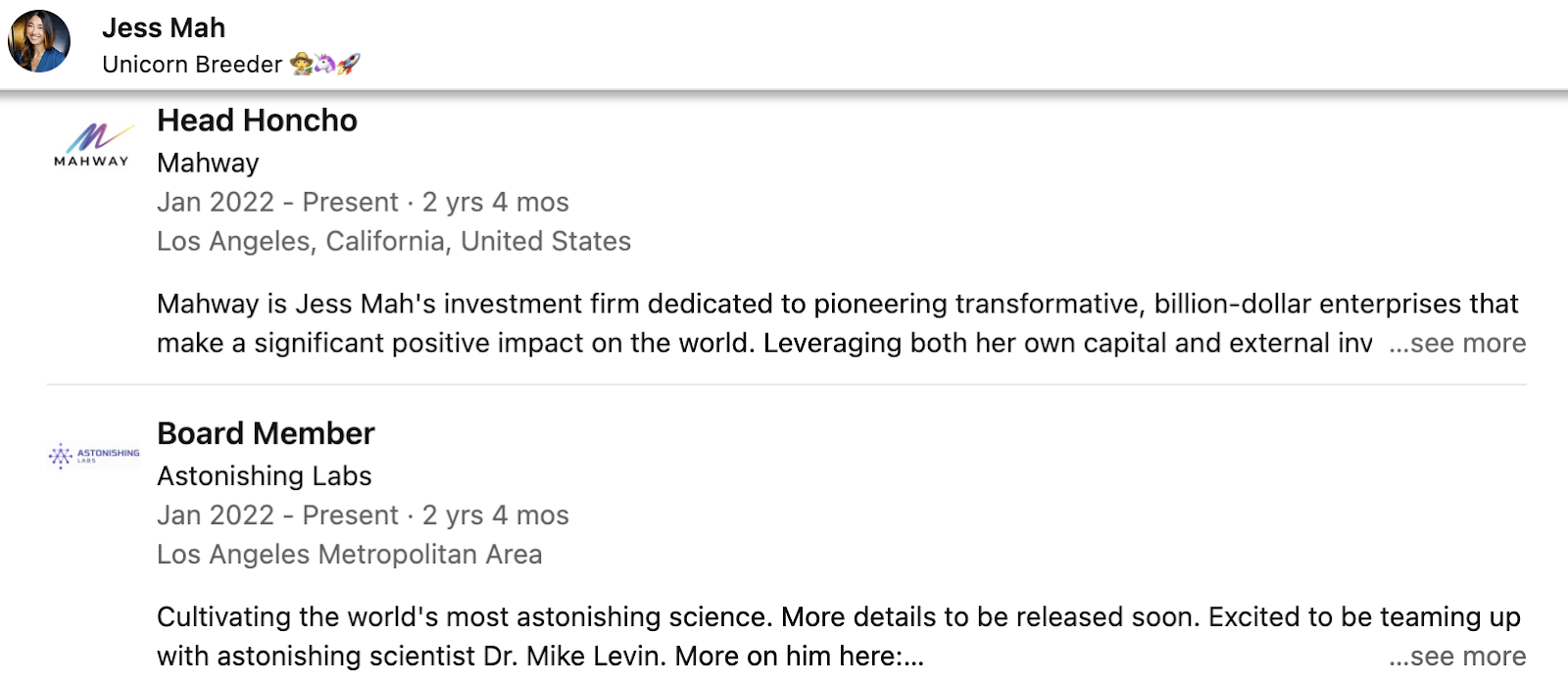

Mah is also the “Head Honcho” at investment firm, Mahway, and a board member of biotechnology research institution, Astonishing Labs.

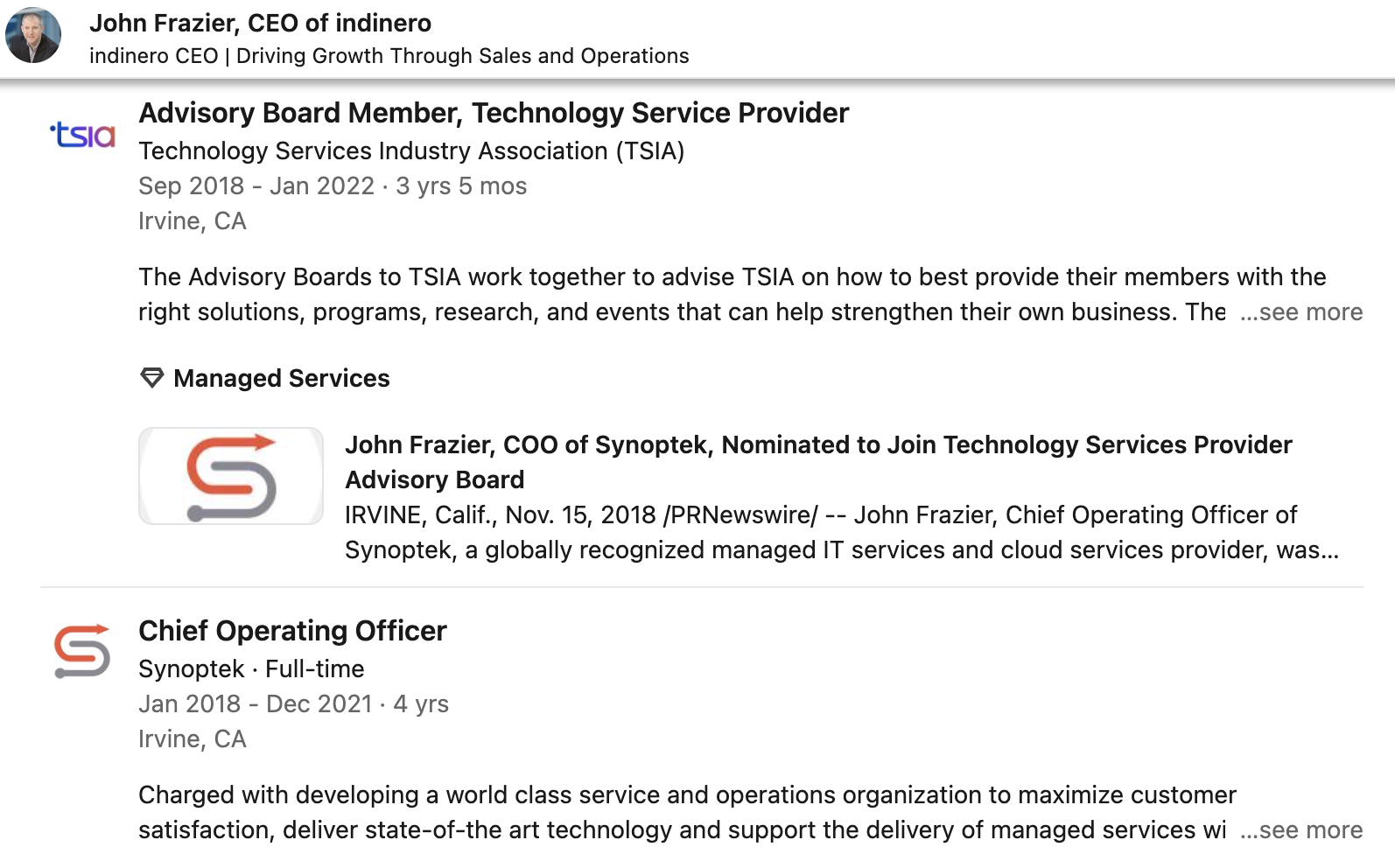

InDinero’s current CEO is John Frazier. Prior to starting at InDinero in January 2022, Frazier was a member of the advisory board at Technology Services Industry Associates (TSIA) and the COO of technology consulting company, Synoptek, before that. He also worked previously at Deloitte and JDA software.

Leadership seems to have a strong technology background that most employees seem to support. According to Glassdoor, 61% of InDinero’s staff would recommend the company to a friend and 68% approve of the CEO.

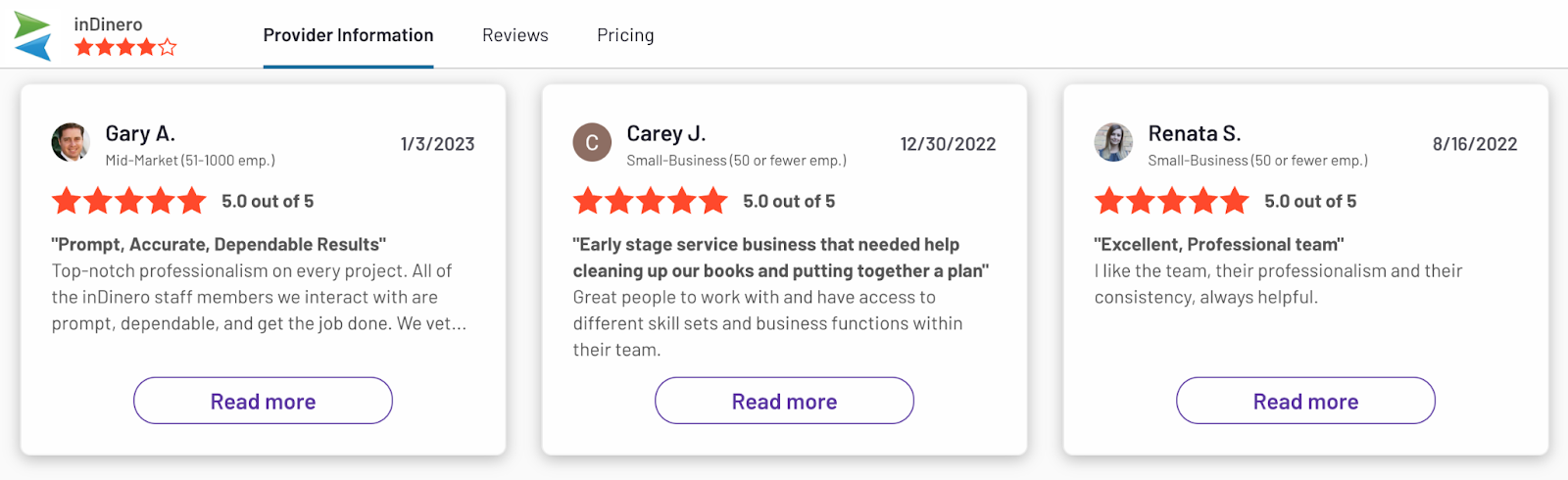

What staff has to say about a company says at least as much as what users think. InDinero’s G2 reviewers give the company an overall 4-star rating. For some reason. Despite being around for so many years, InDinero doesn’t have any ratings on Trustpilot.

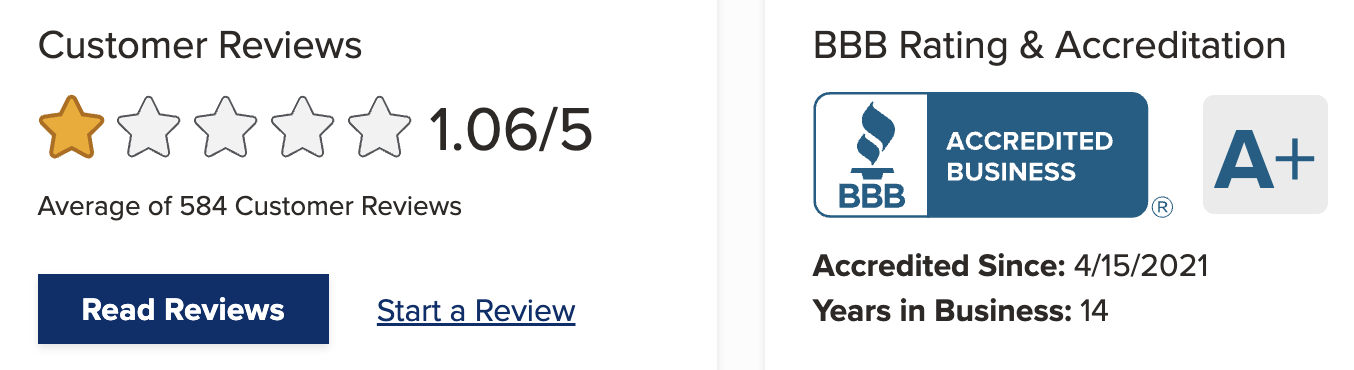

Likewise, one customer review (1-star) on the Better Business Bureau isn’t enough to gauge the way people think of the company. But, in InDinero’s favor, no complaints are listed on the platform, and they have an A+ rating.

I found a couple of pending lawsuits against InDinero – One claiming that InDinero misappropriated funds and another that an employee was wrongfully terminated.

These allegations don’t have anything to do with how InDinero handles customer accounts, but it could speak to their overall business ethics. Keep in mind, the jury is still out on this.

You might also like: Gusto Review: Let’s Really Evaluate This Famed Payroll Platform

What Does InDinero Do?

InDinero combines financial technology with outsourced accounting and bookkeeping services to give you financial data and help drive your business strategy. Whether you’re a startup or an established enterprise, InDinero might be a good place to get comprehensive guidance and support.

Read on to decide if this looks like an offer you might want to cash in on.

You might also like: Comprehensive ZenBusiness Review: Is it Legit for LLCs?

1. Accounting + Bookkeeping

InDinero’s accounting and bookkeeping services cover a wide range of essential financial tasks for businesses. This includes managing accounts receivables and payables, ensuring timely and accurate tracking of financial transactions.

They handle expense tracking, invoicing, and generate detailed reports to provide insights into financial performance. Additionally, InDinero takes care of payroll processing and performs reconciliations to ensure that financial records are accurate and up-to-date.

2. CFO Advisory

InDinero provides strategic financial leadership through their CFO advisory services—This involves offering valuable insights and guidance to businesses in key financial decisions. Their team assists in due diligence processes, especially useful during mergers, acquisitions, or fundraising activities.

InDinero also manages investor relations, helping you communicate effectively with stakeholders. The focus is on driving profitability through operational consulting, optimizing financial strategies to achieve business goals.

3. Business Tax Services

InDinero’s business tax services cover comprehensive tax compliance for federal, state, and local regulations. They assist businesses in maximizing tax benefits, including R&D tax credits.

InDinero identifies tax savings opportunities by leveraging tax credits, deductions, and strategic entity structuring. They provide proactive tax planning to optimize tax liabilities and ensure businesses are compliant with ever-changing tax laws.

4. Financial Planning & Analysis (FP&A)

InDinero’s FP&A services focus on helping businesses plan and forecast their financial future. They assist in budgeting processes, ensuring that financial resources are allocated efficiently.

InDinero conducts scenario modeling to evaluate potential outcomes under different circumstances, enabling businesses to make informed decisions. They analyze key performance indicators (KPIs) to measure business performance and develop financial models that support strategic planning and growth initiatives.

Conclusion: Is InDinero Legit?

InDinero is a reputable firm that merges state-of-the-art financial technology with skilled accounting and bookkeeping services to analyze financial data and provide practical guidance. Whether you’re a startup tackling growth hurdles or an established business aiming to enhance financial strategies, InDinero is dedicated to supporting businesses throughout their journey to financial success.

Is this something you need? Well, if it’s worth investing $750+ per month to find out, then it seems to me like a decent platform to try. However, I always advise that you shop around and make sure you know your options.

And, if you’re the type of person who prefers in-person meetings and more personal support, then you may do better to find a local CPA or accountant to work with—This is important to consider, since InDinero works primarily remotely.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!

Note that simply signing up for a Square account doesn’t make you automatically eligible.

Note that simply signing up for a Square account doesn’t make you automatically eligible.