Here, I want to introduce Space Coast Credit Union (SCCU) and point out some of the special advantages that credit unions offer compared to large banks, particularly for businesses. You’ll find an overview of SCCU’s business credit cards, loans, and other small business financial products.

And, you’ll see insightful comparisons of some of SCCU’s accounts with highlights of their benefits, features, and how they cater to your needs. By the end, you’ll have a clear idea of what SCCU has to offer and whether or not you should consider them for your business banking.

This is what’s in store:

- What is Space Coast Credit Union?

- Business Financial Products and Services

- SCCU Customer Service

- SCCU Community Involvement

- Frequently Asked Questions

- Conclusion

Now, let’s get ready for takeoff!

What is Space Coast Credit Union?

SCCU is a financial institution that offers a range of services tailored for both personal and small business needs. Founded in 1951, it has grown to become one of the largest credit unions in Florida, serving over 500K members.

The credit union was established with the mission to give members competitive financial products and services and maintain a strong commitment to the community. Over the years, SCCU has expanded its offerings to include comprehensive banking solutions for individuals and businesses.

SCCU helps small businesses through a variety of offers:

- Business banking

- Business loans

- Business credit cards

- Merchant services

SCCU offers some unique benefits including the “True Cash Discount” from Banc Card, which promotes cash transactions and reduces fees. Plus, SCCU’s Business Advisors provide personalized guidance on strategic planning and financial management.

Finally, their “Honestly Free Business Checking” really has no hidden fees and no required minimum balance.

Recommended: 3 Best Credit Unions for Small Business Banking in 2024

Locations Served

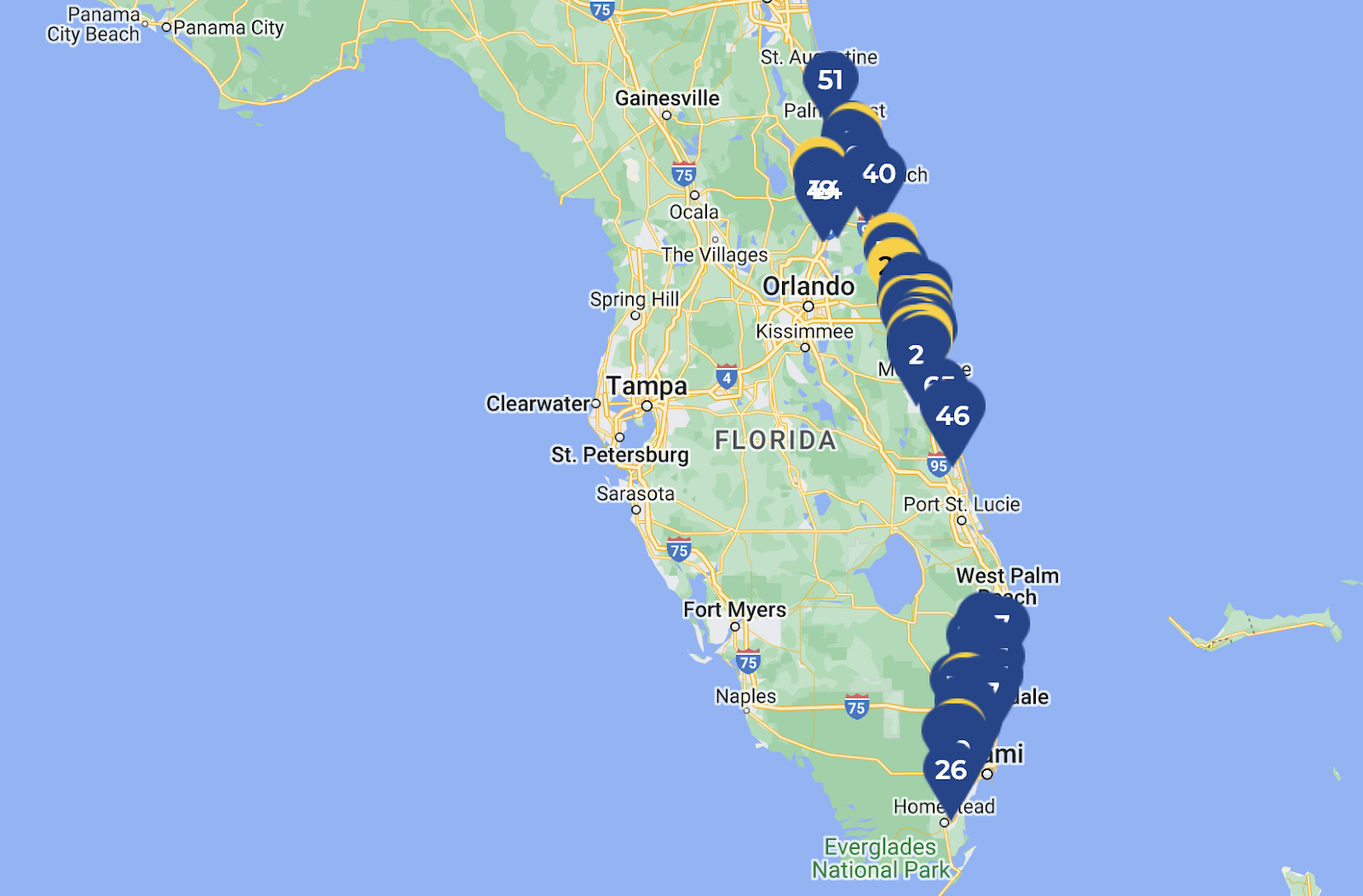

SCCU operates in the eastern part of Florida, with a strong presence in Miami, Melbourne, Palm Bay, Boca Raton, and Fort Lauderdale. They have approximately 60 branches spread across these areas to make sure members have convenient access to banking services.

Branches are equipped with features like ATMs with night drop boxes, drive-thrus, safe deposit boxes, coin sorters, and some offer specialized services like deposit ATMs and extended hours—Their online banking services further extend accessibility to members nationwide.

You might also like: Is BHG Financial Legit? Personal & Business Loans, VC, & More

Membership and Eligibility

To become a member of SCCU, you need to reside in one of the 34 counties in Florida that SCCU serves. These counties include Alachua, Brevard, Broward, Charlotte, Citrus, Clay, Collier, Duval, Flagler, Hernando, Hillsborough, Indian River, Lake, Lee, Manatee, Marion, Martin, Miami-Dade, Monroe, Nassau, Okeechobee, Orange, Osceola, Palm Beach, Pasco, Pinellas, Polk, Putnam, Sarasota, Seminole, St. Johns, St. Lucie, Sumter, and Volusia.

If you meet this criteria, you can join SCCU by opening a personal Share Savings Account online or at any of their 65 branch locations. Your Share Savings Account not only makes you a member but also a co-owner of the credit union—It comes with benefits like earning dividends on the first dollar of savings and no monthly maintenance fees.

When you join, SCCU will check your account, credit, and employment history to verify your eligibility. This may include getting reports from third parties, including credit reporting agencies. Once your membership is established, you can access SCCU’s business products and services.

To open a business account online or in-person with SCCU, you’ll need to provide:

- Business legal name

- Ownership percentage (and have at least 25% ownership

- Employer Identification Number (EIN)

- Articles of Organization, partnership registration, or fictitious name verification from Sunbiz

- Partnership agreement (if applicable)

- Signers/Beneficial owner information

SCCU will provide a Resolution of Authority Form and a Business Service Account Agreement.

You might also like: Novo Bank Review: First-Rate Small Business Banking or Scam?

Business Financial Products and Services

Whether you’re starting a new venture or expanding an existing one, SCCU offers many tools to help your business thrive. Learn more about their business banking, loans, lines of credit, and merchant services.

1. Business Banking/Checking

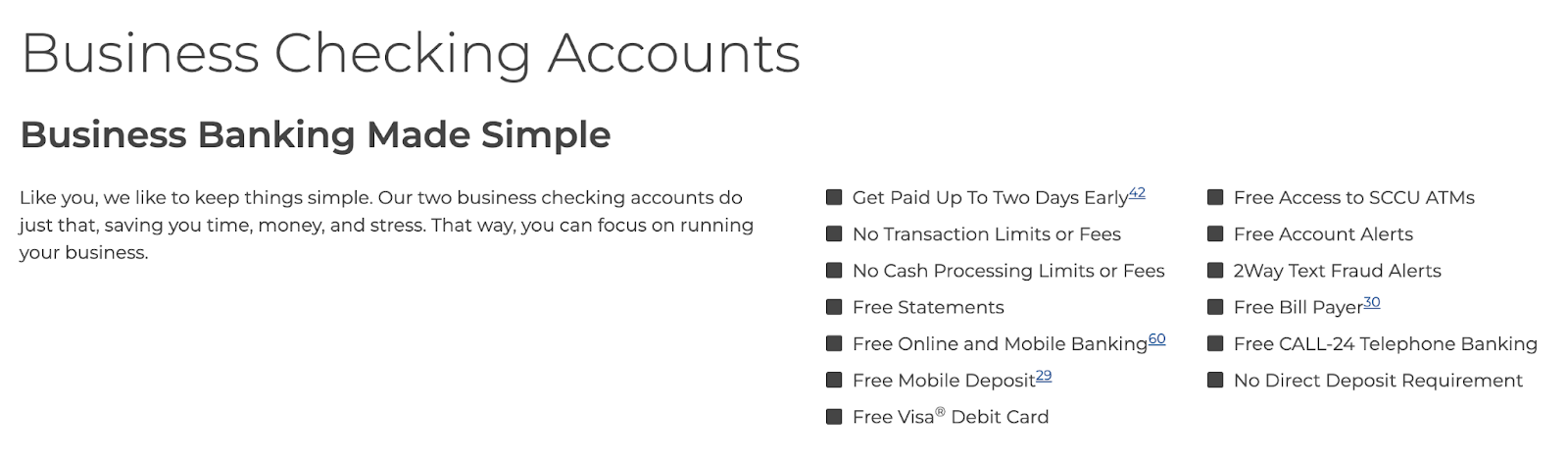

SCCU offers two main business checking accounts: Free Business Checking and Business Interest Checking. These accounts are designed to save you time, money, and stress, so you can focus on running your business.

- Free Business Checking is SCCU’s most popular option. It comes with no direct deposit requirement, no minimum balance requirements, no transaction limits or fees, and no monthly low balance fee. You only need a minimum opening deposit of $50. This account is ideal if you want a straightforward, cost-effective way to manage your business finances without additional costs.

- Business Interest Checking provides the added benefit of earning interest on your account balance, without the need for traditional bank sweeps. Like the Free Business Checking account, it also has no direct deposit requirement and no minimum balance requirement—This account allows your money to work for you while maintaining the simplicity of no monthly fees and transaction limits.

| Free Business Checking | Business Interest Checking | |

| Minimum Opening Deposit | $50 | $50 |

| Monthly Low Balance Fee | None | None |

| Minimum Daily Balance | None | None |

| Transaction Fees | None | None |

| Statements | Free | Free |

| Multiple Business Account Holders | Allowed | Allowed |

| Earns Interest | No | Yes |

Both accounts offer numerous free services, including:

- Free statements

- Free online and mobile banking

- Free mobile deposit

- Free Visa® debit card

- Free access to SCCU ATMs

- Free account alerts and 2-way text fraud alerts

- Free bill payer

- Free CALL-24 telephone banking

- No processing limits

Plus, SCCU advertises that you can get paid up to two days early.

2. Business Credit Cards

SCCU offers a Visa® Platinum Business Credit Card with rewards and competitive interest rates. You earn 3 points per dollar at restaurants and office supply stores, 2 points per dollar on gas, and 1 point per dollar on all other purchases.

Points can be redeemed for:

- Cash back

- Gift cards

- Travel

- Entertainment

- Theme park tickets

The card features a 0.00% introductory APR for the first 6 billing cycles on purchases, balance transfers, and cash advances. After the intro period, the APR is based on creditworthiness, with rates as low as Prime Rate (8.5% as of today) + 7.99%.

With this card, there are no annual fees, balance transfer fees, or cash advance fees. But, you can incur a late payment fee of up to $27 and there’s a minimum finance charge of $0.50.

Unique perks for cardholders include:

- Free 2-way text fraud alerts

- Visa zero liability protection

- Digital wallet payment options

- Contactless payments

- Card controls through the mobile app

The Visa® Platinum Business Credit Card provides financial flexibility, rewards, and essential security features.

Recommended: Corporate vs Business Credit Card: What’s the Difference?

3. Business Loans

SCCU offers a handful of business loans:

- Commercial real estate loans

- Commercial construction loans

- Commercial vehicle loans

- Business equipment loans

Commercial real estate & construction loans help you build, buy, or refinance properties like offices, warehouses, or retail spaces. SCCU provides loans for owner-occupied and investor-owned properties, as well as commercial construction. There are no application fees or pre-payment penalties, and terms vary based on the project.

For construction loans, you can expect a structured draw schedule tied to construction milestones.

Commercial vehicle & business equipment loans are ideal for purchasing or refinancing business vehicles or equipment—They offer low credit union rates and flexible terms. Like real estate loans, there are no application fees or pre-payment penalties. Terms range from 24 months to 10 years or more, depending on the equipment and the lender.

For commercial vehicles and equipment loans, the benefits include separating personal and business finances, potential tax deductions, and full ownership of the vehicle or equipment.

SCCU offers fixed- and variable-rate loans, with specific rates based on creditworthiness and loan type. While they don’t disclose their commercial loan rates, comparable consumer loans come with rates as low as 6.25% for mortgages and 6.24% for auto loans.

Recommended: 6 Best Business Credit Cards for Entrepreneurs: Fuel Your Growth

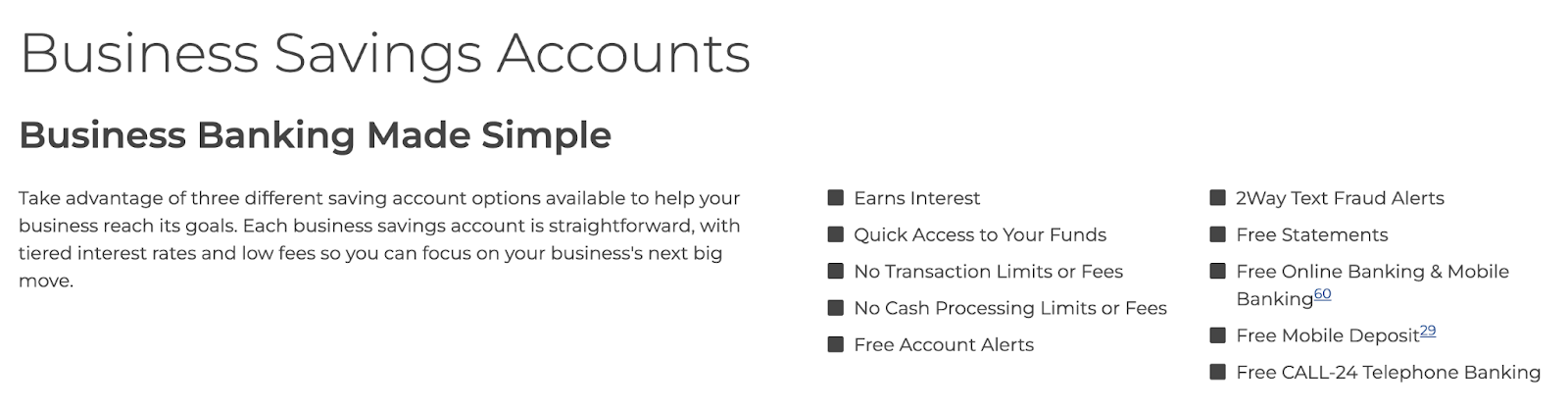

4. Business Savings & Investment Opportunities

SCCU has a variety of business savings and investment options tailored to help your business grow while earning competitive returns.

The Business Savings Account and Business Money Market Savings both offer attractive interest rates that vary based on the balance maintained, starting from 0.04% APY for balances under $100K up to 1.25% APY for balances of $250K and above—These accounts come with:

- No transaction limits or fees

- Free account alerts

- Easy access through online and mobile banking

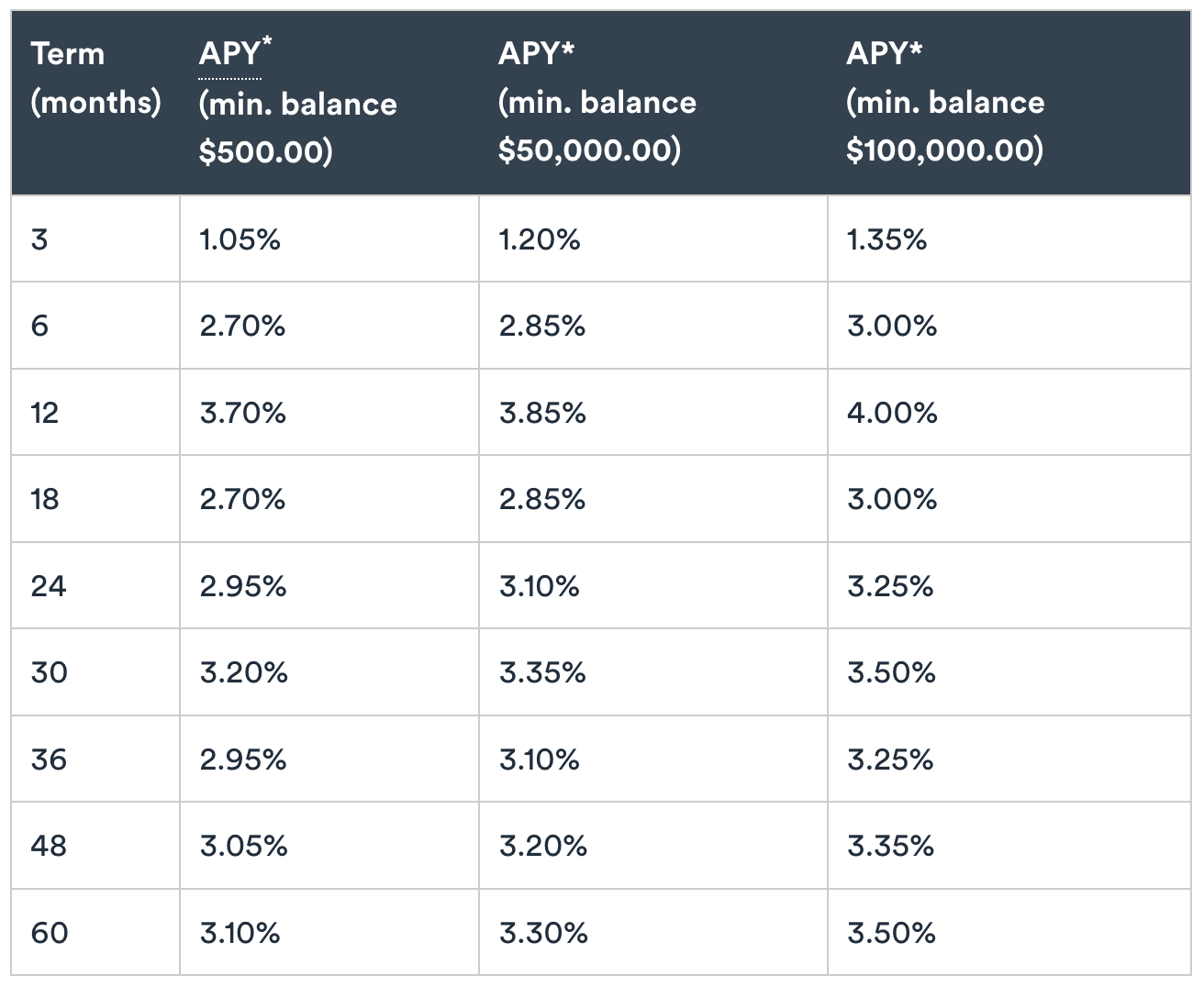

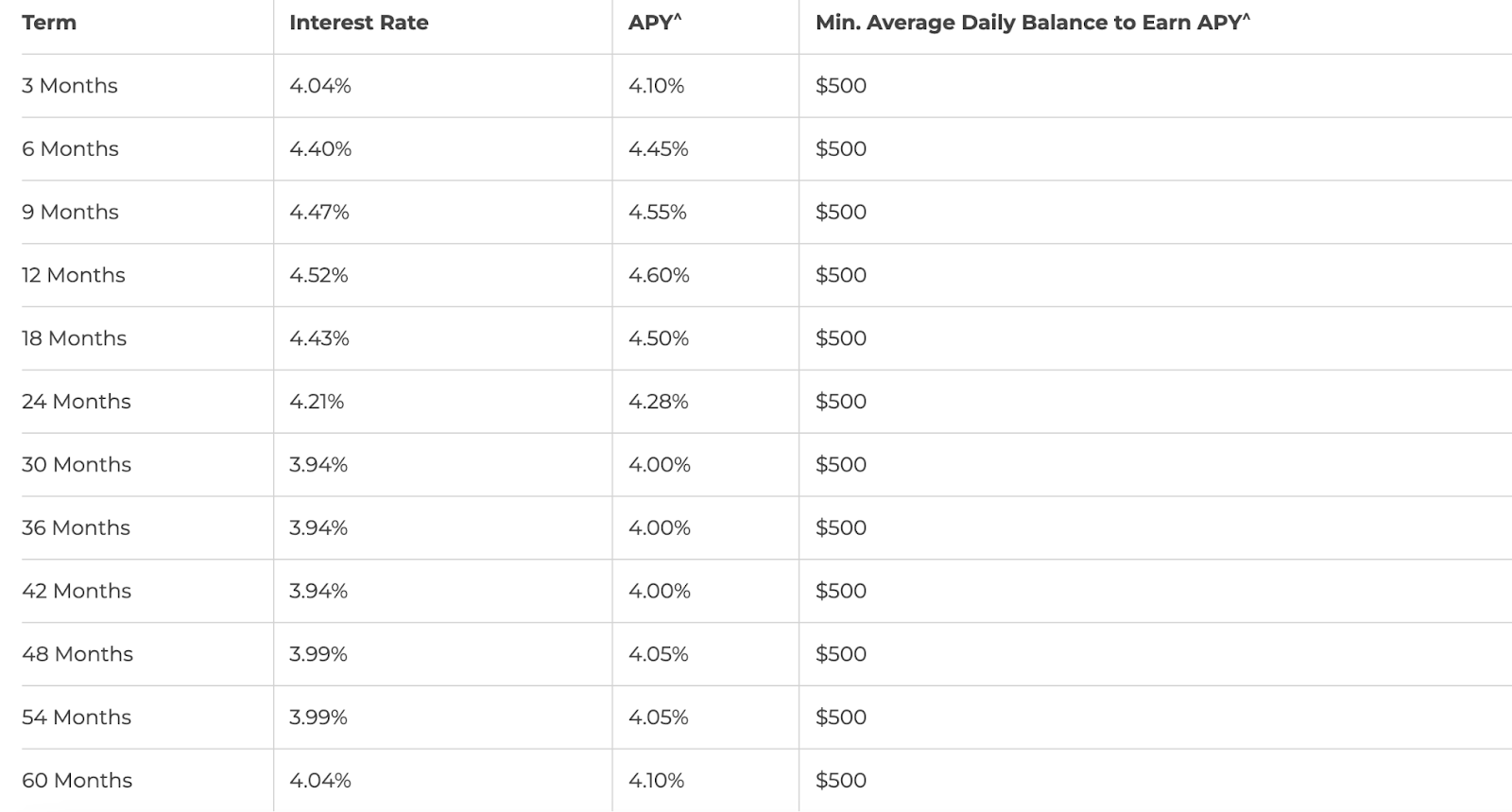

Additionally, their Certificates of Deposit (CDs) offer fixed interest rates ranging from 3.94% to 4.60% APY, depending on the chosen term length from 3 to 60 months. CDs have a $500 minimum deposit requirement.

5. Treasury Services

Finally, SCCU offers comprehensive merchant services through a partnership with BancCard. Through this partnership, they’ve made it more convenient and efficient for business members to process credit payments.

By accepting all major card types (including Visa, MasterCard, American Express, PIN Debit, Fleet, and foreign cards), SCCU enables you to expand your customer base and improve cash flow.

The services feature:

- Cost-effective processing programs with no hidden fees

- Innovative payment options like gift cards and electronic check acceptance

- Modern equipment including EMV/NFC terminals and smartphone/tablet functionality

Whether you operate online or have physical locations, SCCU’s merchant services provide flexibility and next-day availability of funds, ensuring businesses can operate smoothly and securely.

You might also like: Should You Accept a Square Business Loan Offer?

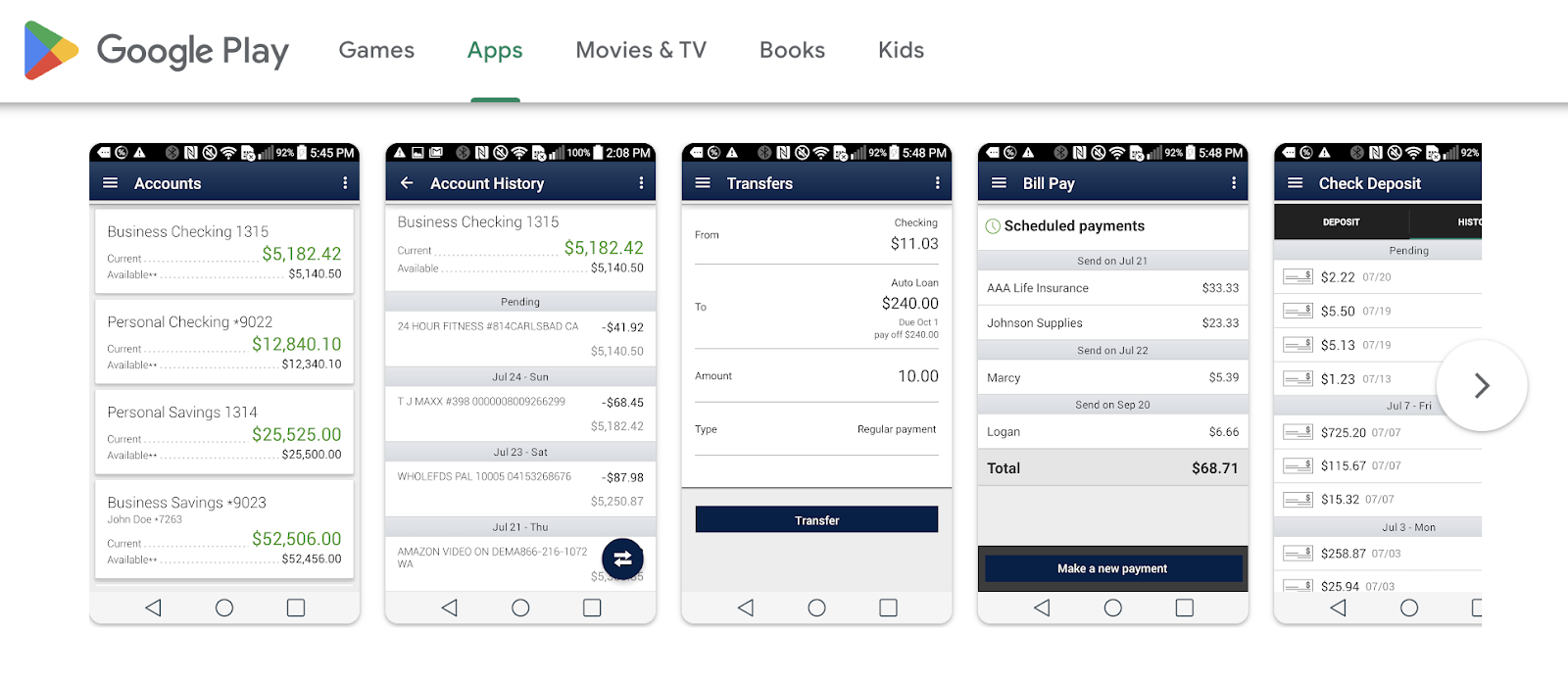

6. Mobile App

The SCCU Mobile app is available for both iOS and Android, and gives you a free and secure way to manage your accounts on the go. With a rating of 3.8 stars from over 4.4K reviews on Google Play and 4.8 stars from 29.6K ratings on the Apple Store, the app is well-received.

In the app, you can:

- Deposit checks remotely from your mobile device

- Get help on the go with live chat

- Monitor your account with customizable alerts

- Securely access your accounts using fingerprint or Face ID

- Check balances, view transaction history, and pay bills

- Transfer funds and make person-to-person payments

- Locate SCCU branches and ATMs near you

While the app is free for SCCU members, enrollment in SCCU’s Online Banking service is required. Users benefit from data encryption during transmission and can request data deletion.

However, some users have reported issues like crashes during check deposit and interface navigation challenges (which the developer continues to address through updates and user feedback).

SCCU Customer Service

SCCU offers pretty solid customer service for business members.

First, they have dedicated ‘Business Advisors’ who are meant to understand the unique financial needs of businesses and offer personalized guidance.

Next, With extended service hours during the week and on Saturdays, SCCU makes sure you can get jelp when it’s convenient for your busy schedule—They provide multiple ways to connect, whether through phone, email, or visiting a branch, so you can choose the method that suits you best. And, SCCU aims for prompt responses to your inquiries, which will help you manage your business finances efficiently.

Additionally, they offer educational resources like financial estate guides, articles, calculators, and detailed product information to empower you to make informed financial decisions—Their business-centered customer service approach is designed to be supportive and informative.

SCCU Community Involvement

Space Coast Credit Union (SCCU) is really into giving back and being part of their community. They’re all about “People helping people,” which sums up how they roll. They’ve been nominated for Business of the Year, which shows they’re making a real impact locally.

They’re active in lots of charity work, from supporting cancer foundations to helping out with school supplies. When hurricanes hit, like Irma, SCCU stepped up big time, keeping their ATMs and online services running to support their members. They also donated over $76K to the American Red Cross after multiple storms.

SCCU isn’t just about money—they’ve given over $1 million to causes they care about. Whether it’s helping out during disasters or supporting local initiatives, they’re there. Recently, they donated $38k for Hurricane Dorian relief in the Bahamas, showing they’re ready to pitch in when needed.

Overall, Space Coast Credit Union isn’t just about banking; they’re about making their community stronger. Their motto isn’t just words—they live it through their actions, from helping small businesses to lending a hand when things get tough.

Frequently Asked Questions

Does Space Coast Credit Union have monthly fees?

Space Coast Credit Union offers various accounts and services with different fee structures. Many accounts are fee-free, but some accounts may have monthly fees.

How much does Space Coast let you overdraft?

Space Coast Credit Union allows up to $500 in overdraft protection, but charges $30 per item. And, the specific amount allowed for overdrafts can vary based on your account type and individual circumstances.

How much can you withdraw from a Space Coast Credit Union ATM?

You can typically withdraw up to $500 per day from a Space Coast ATM. However, you may be able to speak to a banker to get your limits increased, particularly for business accounts.

Is Space Coast FDIC insured?

No, Space Coast Credit Union is not FDIC insured. Credit unions are insured by the National Credit Union Administration (NCUA), which provides similar coverage up to $250K per depositor.

Conclusion

In all, SCCU offers personalized business financial solutions with competitive rates and flexible terms. They excel in community engagement and social responsibility, contributing actively to local causes.

While their branch network may be somewhat limited, SCCU provides robust business credit cards, loans, and merchant services. And, you can take advantage of the credit union’s educational resources whether you are a member or not. SCCU stands out for its commitment to supporting local businesses and fostering lasting relationships with its members.

If your business operates or plans to expand outside of Florida, SCCU might not be the best fit for you. The credit union primarily serves Florida, so if you need extensive branch access beyond this state, their geographic coverage is limited. So, if your business requires convenient physical banking locations across multiple states, consider a financial institution with a broader network.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!