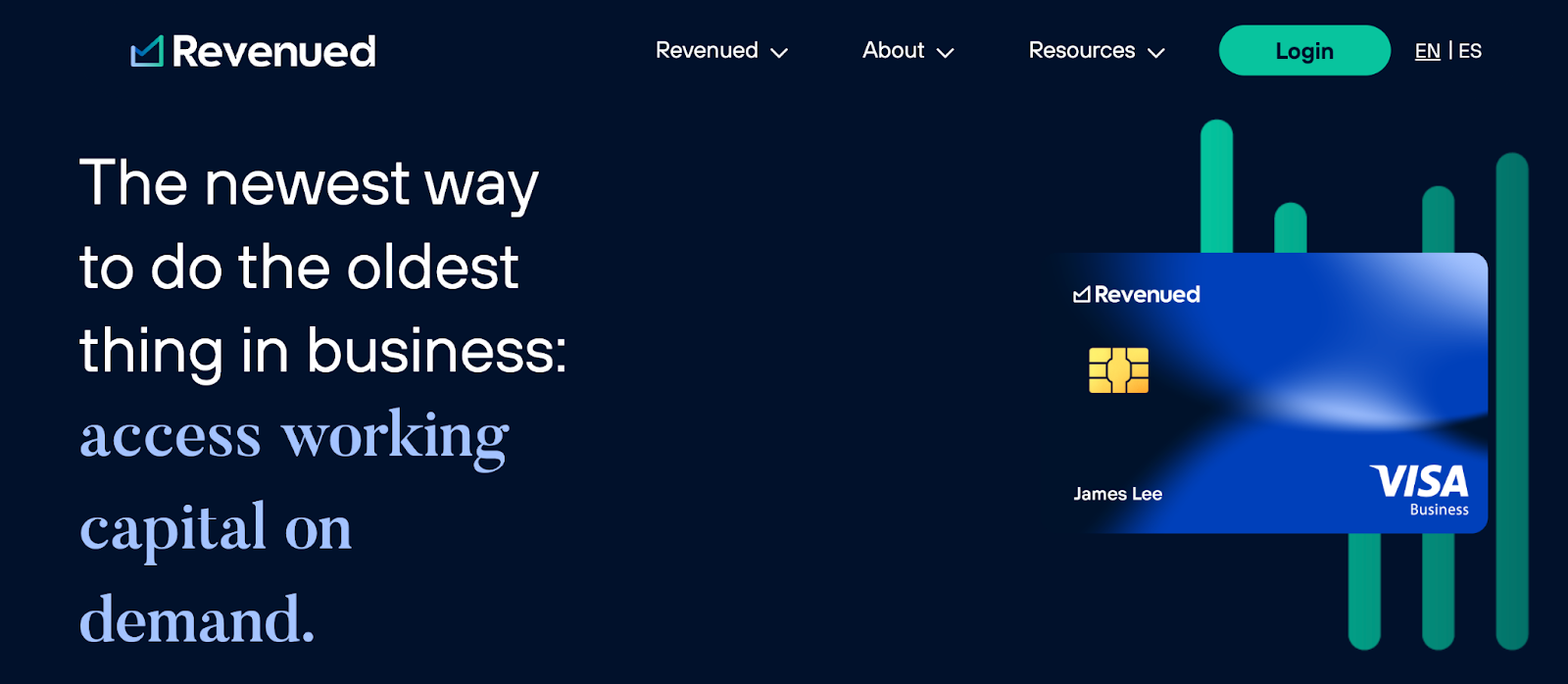

The Revenued business Visa® card is a popular new way for businesses manage their spending (and to get funding in as little as an hour after you apply). So, if not a loan or line of credit, what is it? And, is it worth it?

Here, we’ll look at the details of the offer including an overview of the company, rates and fees, limits, and get answers to questions you might have about the Revenued business card.

This is what’s in store:

- What is a Revenued Business Card?

- How Does a Revenued Business Card Work?

- Frequently Asked Questions

- Conclusion: Is the Revenued Business Card Legit?

Now, let’s roll!

What is a Revenued Business Card?

The Revenued business card is a “fee-free,” 3% cash back, commercial prepaid card issued by Sutton Bank, designed specifically for business needs—It’s not a credit card, loan, or a gift card, and it’s meant to purchase goods and services related to your business activities.

There are no:

- Monthly maintenance fees

- Card replacement fees

- Expedited delivery fees

- Statement fees

However, if you use an out-of-network ATM, additional fees might apply.

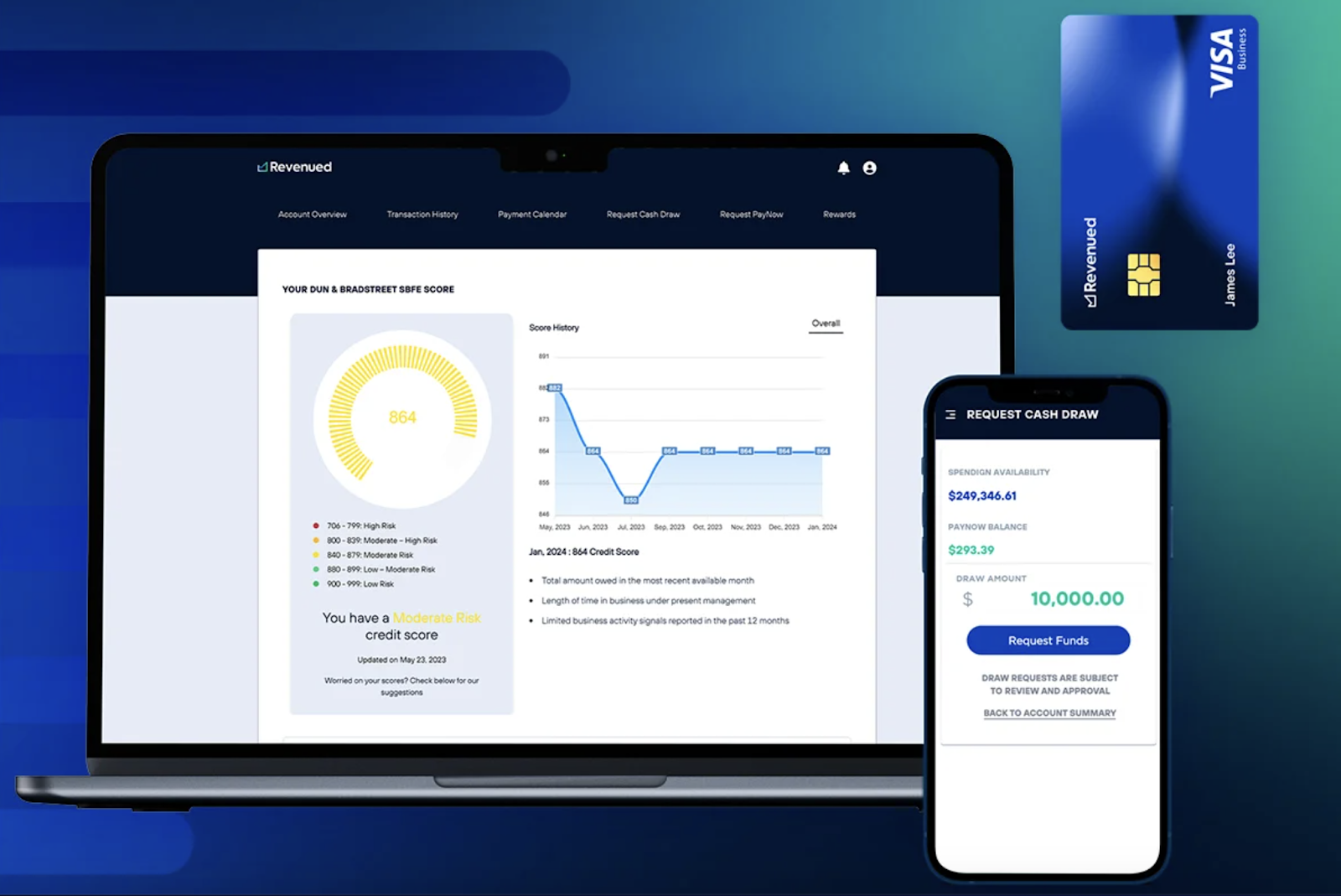

With the Revenued business card, you also get access to a “Flex Line” feature, providing you with a flexible “line of credit” up to $500K. And, it’s funded through a Pearl Capital account, using merchant cash advance (MCA) funds (Originally, this made me think the company was a white label solution for Pearl Capital funding).

Within the flexible line of credit, there are spending limits: you can spend up to $10,000 per day, $50,000 per month, and no more than $10,000 per transaction.

You might also like: Is Carputty Legit? A Complete Auto Financing Review

What is Pearl Capital MCA Funding?

For individuals considering a Revenued business card, Pearl Capital MCA funding offers a financial solution worth exploring. MCA, or Merchant Cash Advance, funding is essentially a factored loan, wherein a lump sum is provided upfront in exchange for a percentage of future credit card sales—This means that instead of a traditional loan with fixed payments, repayments are based on a percentage of daily credit card transactions.

It’s a quick and flexible option for businesses in need of immediate cash flow, although it’s important to note that MCA funding typically comes with higher fees and shorter repayment terms compared to traditional loans.

You might also like: A Deep-Dive Credibly Review: Is Their Financing Right for You?

Revenued Business Card Requirements

To obtain a Revenued Business Card, you’ll need to meet certain requirements—Firstly, you must have a valid email address and reliable access to the internet.

You also need:

- A legally registered LLC or corporation

- At least a year in business

- A dedicated business checking account

- At least $20K in monthly deposits

Other factors may limit your ability to obtain funding during the underwriting process. However, your credit shouldn’t impact your ability to obtain a Revenued business card.

You might also like: Could a Stripe Capital Loan Get Your Business Through a Rough Patch?

Company Overview

There are several companies at play here (Sutton Bank, Pearl Capital, Marqeta). For the sake of staying relevant, let’s peek behind the curtain at Revenued – the company presenting the actual product. According to their own marketing, “Revenued is a card that cares less about FICO and more about your business.”

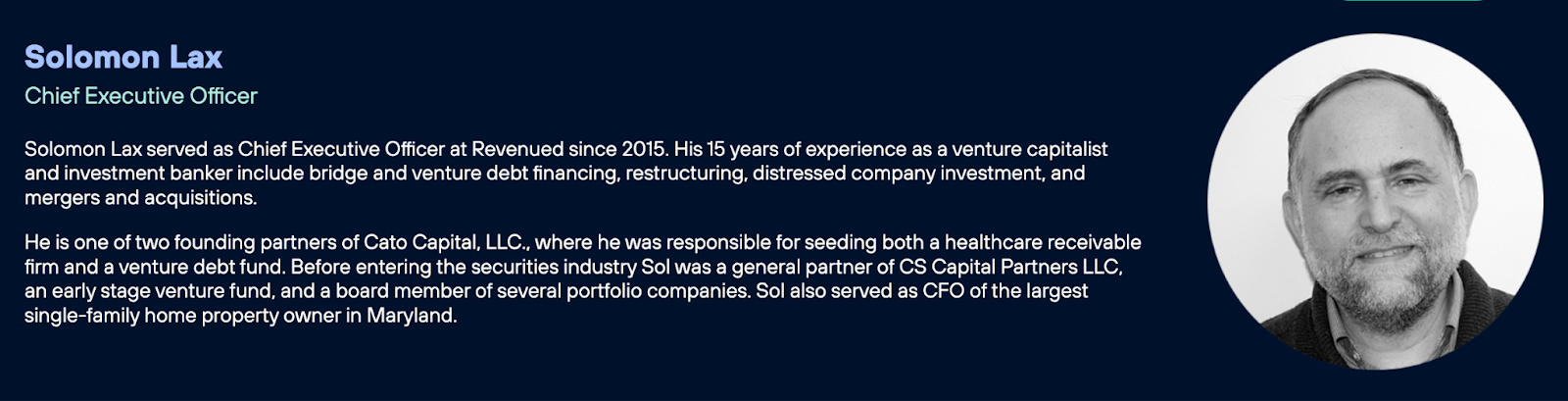

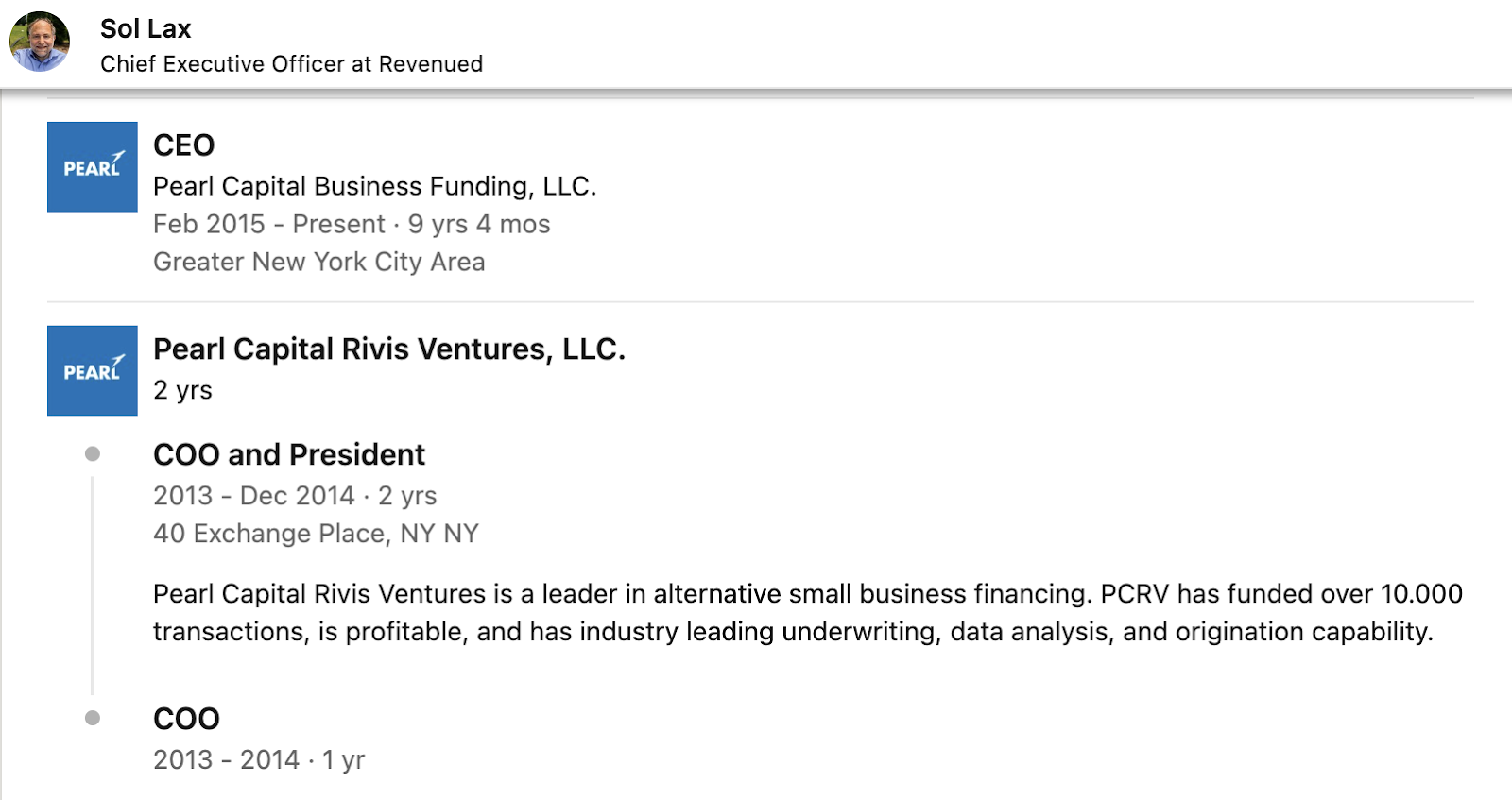

Revenued LLC is a New Jersey-based, private, for profit financial solution provider that was founded in 2017. The company’s current CEO, Solomon “Sol” Lax, is claimed to have been at his current position since 2015 (but the entity wasn’t officially established until a couple years after this).

Now, what’s interesting is that, according to his LinkedIn profile, Sol became the CEO at Pearl Capital in 2015, where he moved up from COO—This shows that the two entities are very connected.

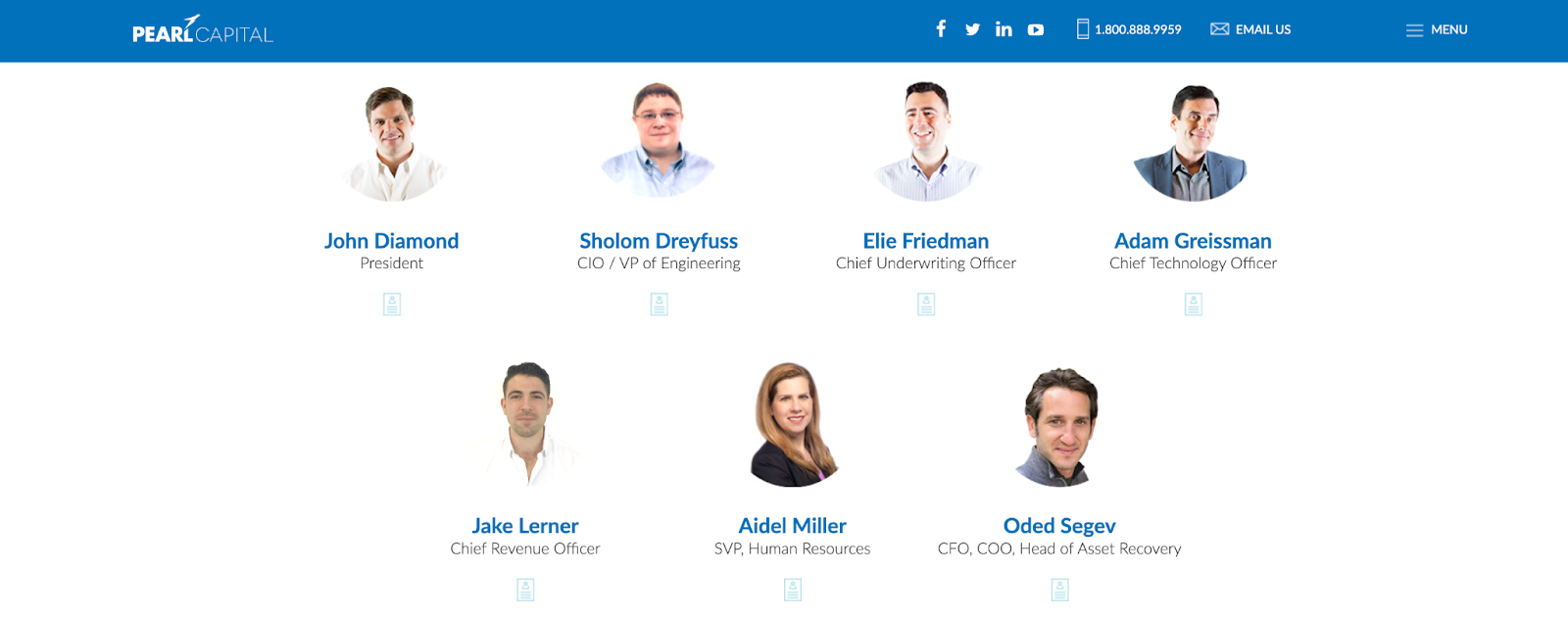

In fact, Revenued and Pearl Capital share most of the same company leadership.

Technically, they are two different entities, so let’s not dwell too long on that subject. For 6 bucks or so, we could pull more info about the companies from Secretary of State records or Open Corporates. But, I think we have enough info to dig up the dirt.

Revenued isn’t listed on Glassdoor, but Pearl Capital is. And, only about ⅓ of employee reviewers approve of Sol as the leader of the company. Staff rate diversity and inclusion efforts on the poor side and declining. What employees think of a company can imply a lot about the internal culture.

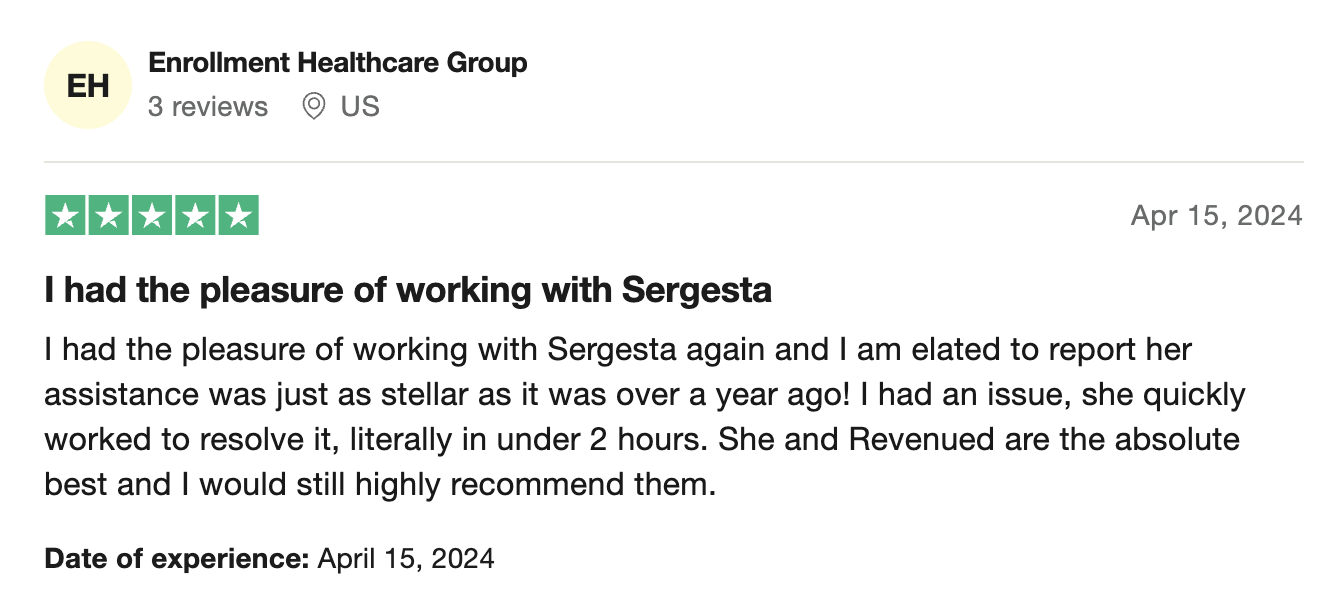

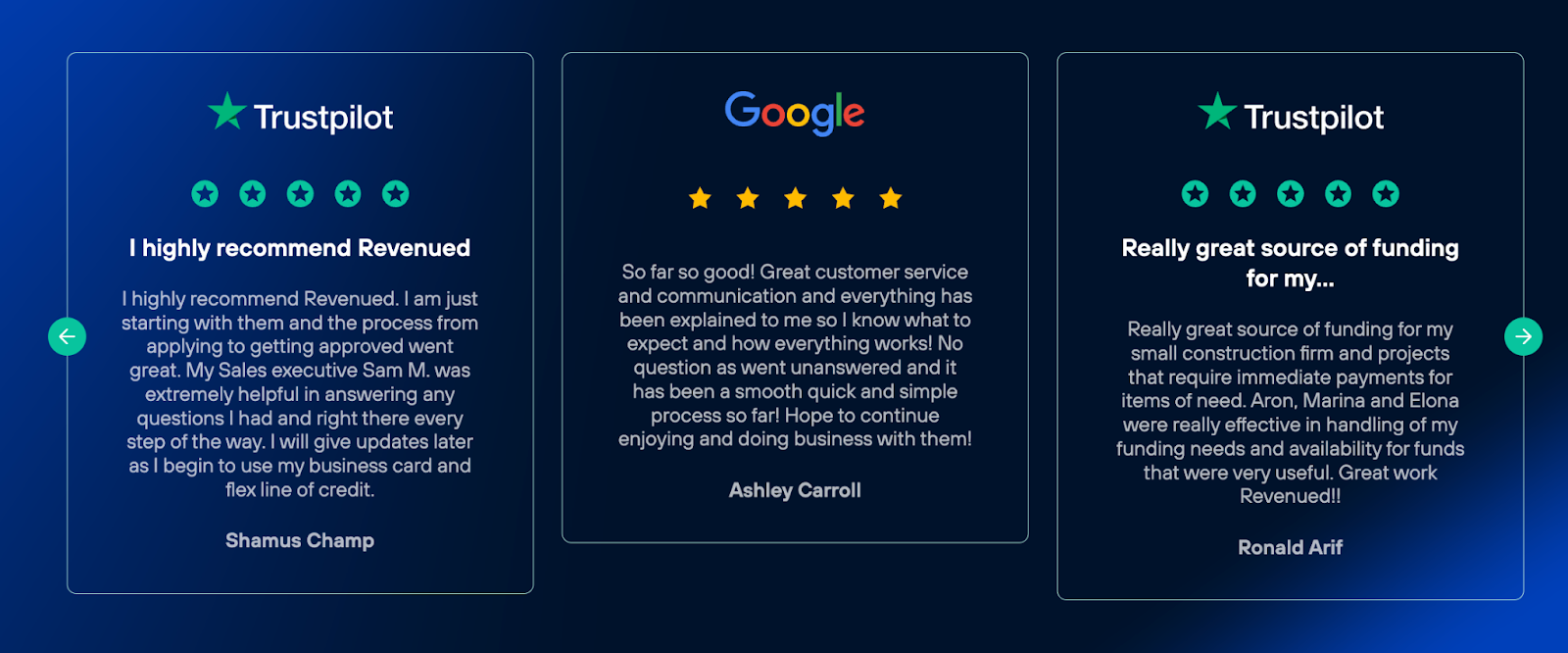

More importantly from a borrower’s perspective, existing customers can tell us more. On Trustpilot, The reviews for Revenued are overwhelmingly positive, with a TrustScore of 4.7 out of 5 and the majority of reviewers giving 5-star ratings. Customers praise the company for its easy application process, helpful customer service representatives, and quick issue resolution.

While they’re not accredited with the Better Business Bureau (BBB), they maintain an A- rating. Most if not all of their complaints must’ve been closed in a timely manner.

I ran across a few open lawsuits where Revenued LLC was a party—they appeared to be the company filing breach of contract against business borrowers. It’s worth noting that they do collect on debts owed to them, which is completely understandable.

In all, despite some internal concerns and a few disputes, Revenued LLC garners high customer satisfaction ratings for its efficient services, suggesting that it effectively meets the needs of its clientele.

You might also like: This is the Truth About LenCred’s Small Business Financing

How Does a Revenued Business Card Work?

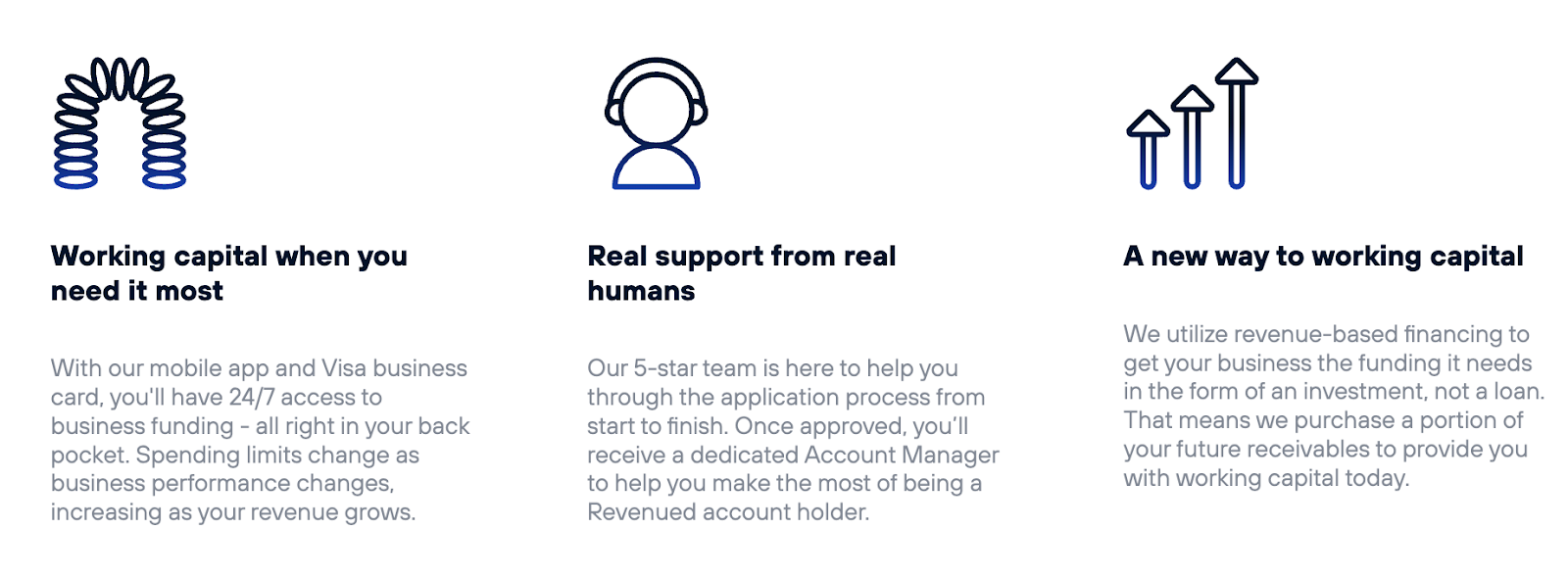

From the card itself to the Flex Line and more, A Revenued business card is a simple, but powerful offer. Let’s take a look at the features and benefits of a Revenued business card.

1. Flexible Line of Credit

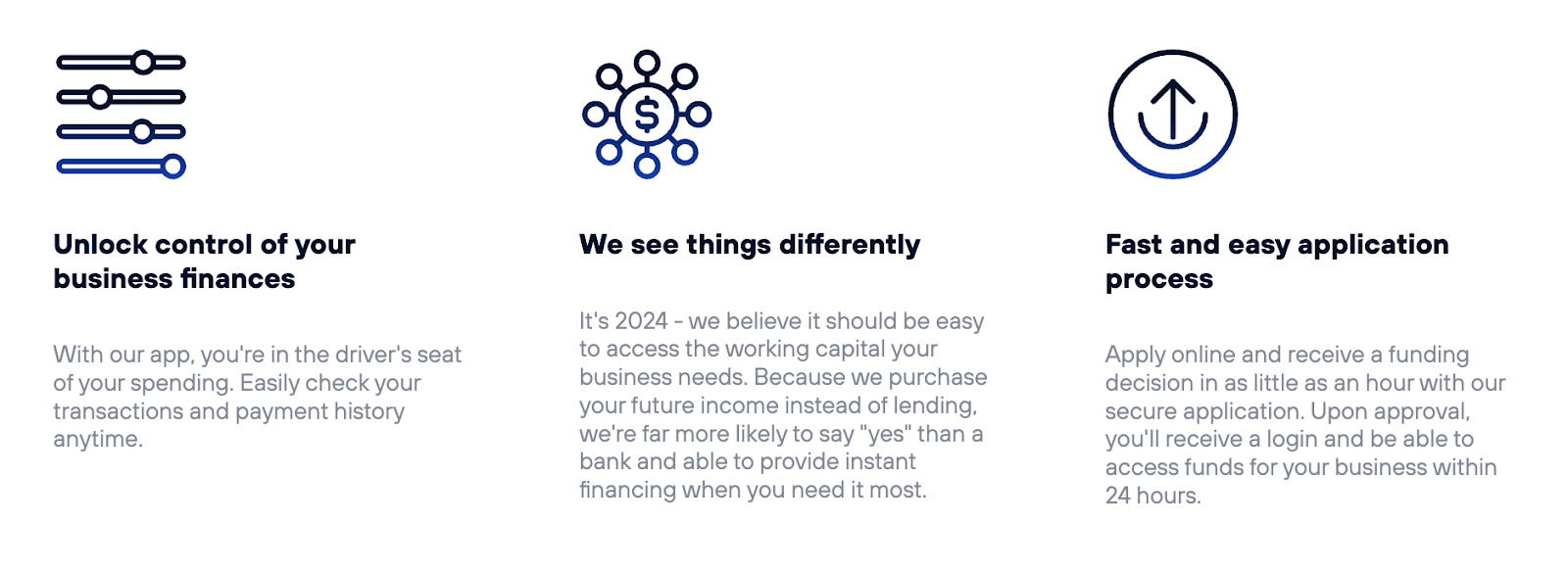

The Revenued business card offers access to a flex line of credit that adapts to your business’s revenue fluctuations. This feature allows you to borrow funds as needed, providing financial flexibility to cover unexpected expenses or seize growth opportunities.

Unlike traditional loans with fixed repayment terms, the line of credit adjusts based on your business’s performance, ensuring that you have access to the capital you need when you need it most.

Moreover, the factor rate remains constant throughout the repayment period and usually falls within the range of 1.1 to 1.5.

You might also like: How to Get Approved for Amazon Net 30 Terms (“Pay by Invoice”)

2. Control & Monitoring

Managing your spending and monitoring transactions is made simple with the Revenued business card. They use Marqeta (the same platform as Ramp and Divvy (Bill)) to issue cards and – in my experience – this technology is great.

Through an intuitive online dashboard or mobile app, you can track your purchases, review transaction history, and monitor your available credit in real-time—This visibility and control level can empower you to make informed financial decisions, identify trends in your spending patterns, and proactively manage your cash flow.

Moreover, authorized users are allowed, which could be convenient or needed for some borrowers.

You might also like: Can Tradeline Supply Reviews Be Trusted? The Full Picture

3. Super Quick Funding

One of the key advantages of the Revenued Business Card is its quick and streamlined funding process. When you apply for the card online, you can receive a funding decision in as little as an hour.

Once approved, you’ll gain access to your funds within 24 hours, allowing you to address pressing business needs promptly—This rapid funding turnaround time ensures that you can seize opportunities for growth and respond to unexpected challenges without delay, which can help you keep your business operations running smoothly.

You might also like: Is Biz2Credit Legit? A Complete Review

4. Dedicated Support

As a Revenued business card holder, you’ll have access to dedicated support from a team of experienced professionals. From the moment you apply for the card, you’ll be assigned a dedicated Account Manager who will guide you through the application process and provide ongoing assistance with managing your account.

However, live chat support is limited to certain hours and days of the week.

You might also like: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

Frequently Asked Questions

Does Revenued do a hard pull?

Revenued typically conducts a soft credit pull during the application process, which doesn’t impact your credit score. However, in some cases, they may perform a hard credit pull, which can affect your credit score.

Is there an annual fee for the Revenued business card?

As of January 2024, the Revenued Business Card is fee-free. It doesn’t charge an annual fee, monthly fee, application fee, or card replacement fee.

What is the minimum credit score for Revenued?

Revenued considers various factors beyond just your credit score when evaluating applications. While there isn’t a specified minimum credit score requirement, having a higher credit score may increase your chances of approval and potentially result in better terms.

Who does the Revenued business card report to?

The Revenued business card typically reports to the major credit bureaus, such as Experian Business, Equifax Business, and Dun & Bradstreet (D&B). This means that on-time payments can help you build business credit.

Conclusion: Is the Revenued Business Card Legit?

I almost never recommend MCA funding unless there is no other choice because they are typically too expensive. While MCAs may not always be the preferred option for financing, the Revenued Business Card stands out for its potential to serve dual purposes.

Not only does it offer a pathway to access working capital quickly, but it also presents an opportunity to build and strengthen your business credit profile. And, the potential for 3% cashback on MCA spending adds another layer of benefit, making it a compelling choice for businesses seeking flexible financing solutions while aiming to improve their creditworthiness.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!