As a business owner, there’s no end to how you can use credit to grow your business. But, one of the downsides to using credit versus cash is the fact that it can cost you. If you fail to pay credit in full each billing cycle, annual percentage rate (APR) interest can add up fast—But, not if the APR is 0%.

0% APR business credit cards can save you a ton of interest, if used responsibly. But, where can you find them? There are needles in a haystack with no interest ever, and others you can leverage at 0% introductory rates. Simply put, here are the top business credit cards with 0% APR that I know of right now.

This is what’s in store:

- What is a Good APR for a Business Credit Card?

- The Best Business Credit Cards With 0% APR

- Frequently Asked Questions

- Final Thoughts

Now, let’s roll!!

What is a Good APR for a Business Credit Card?

Generally speaking, the lower the APR on a business credit card the better — this is if you plan to carry a balance. The lower the rate, the less you’ll pay. Think of it like this: With credit cards, you’ll be charged interest on any money that you owe at the end of a billing cycle.

So, if you spend $1,000 on your credit card, and you only pay $100 at the end of the month, you will still owe $900 to the card issuer. The issuer will charge interest on that $900. The lower the interest rate/APR the less you will pay.

According to data collected by the Federal Reserve, the average interest rate on credit cards issued by commercial banks was 21.47%, which increases over time – So, anything lower than this might be considered a “good” APR. However, this doesn’t account for cards issued by credit unions nor separate business products from those issued to consumers.

Keep in mind, if you pay the balance on your business cards in full each month, you won’t have to worry about APR.

You might also like: 3 Best Credit Unions for Small Business Banking in 2024

Can You Get a Credit Card with 0% APR?

You can absolutely get a credit card with no annual interest rate—Both 0% APR business credit cards and 0% APR consumer credit cards can be found on the market.

In most cases, when a business credit card comes with no annual fee, this is an introductory rate…A 0% introductory rate means that you will pay no interest for a specified period, which is usually 6, 12, 18, or 24 months. After this, the interest rate will revert back to its normal rate. At this point, you will be charged the full interest for any balance still owed, no matter when the debt accrued.

Another business financial product that people sometimes refer to as a business credit card is a corporate card. Many corporate cards come with 0% APR, and several even offer cash back on purchases. However, a corporate card is not technically a business credit card.

You might also like: Corporate vs Business Credit Card: What’s the Difference?

The Best Business Credit Cards With 0% APR

Let’s take a look at the top business credit cards you can get today with 0% APR.

Note: Credit cards rates can vary – always check with the card issuer before you apply.

You might also like: 6 Best Business Credit Cards for Entrepreneurs: Fuel Your Growth

1. PNC Cash Rewards Visa Signature Business

The PNC Cash Rewards Visa Signature Business Credit Card offers a $400 bonus when you open a new account and make at least $3,000 in qualifying purchases within the first three billing cycles—It also features an introductory 0% APR for the first 9 billing cycles (9 months), with a variable APR of 19.24% to 27.24% afterward.

With this card, you earn 1.5% cash back on net purchases, with no limits on your earning potential. You can easily manage your account online with various tools provided. Additionally, as a Visa Signature cardholder, you’ll enjoy travel benefits and purchase protection.

There’s no annual fee, and for balance transfers, you’ll pay either $5 or 3% of the transfer amount, whichever is greater. Cash advance fees are either $10 or 4% of the advance amount, with a maximum fee of $75. Late payment and over-the-credit-limit fees may apply.

A noteworthy perk: if you have a PNC business checking account, using this credit card could help offset your monthly maintenance fee.

Recommended: PNC Bank Business Credit Card Review & Comparison

2. U.S. Bank Business Platinum Card

The U.S. Bank Business Platinum Card offers a 0% introductory APR on purchases and balance transfers for 18 billing cycles (a year and a half), making it ideal for managing expenses and consolidating debt. After the introductory period, a variable APR applies.

This card comes with a low annual fee and provides cards for both you and your employees–This U.S. Bank business credit card gives you access to a dedicated domestic servicing center with 24/7 customer support, which ensures assistance whenever you need it.

With Visa Spend Clarity™, you can track spending and manage expenses more effectively. The card has received honors, including being named Best 0% APR Credit Card by WalletHub and Best Business Cash Back Card for Gas by Forbes.

Furthermore, the U.S. Bank Business Platinum Card allows you to pay over time with U.S. Bank ExtendPay® Plan, and new cardmembers can take advantage of a $0 fee offer on ExtendPay Plans opened within the first 60 days after account opening.

You might also like: What are the Best Unsecured Business Credit Cards for Startups?

3. Capital One Spark Business 1.5% Cash Select

The Spark 1.5% Cash Select credit card from Capital One is tailored for businesses with good credit. It offers unlimited 1.5% cash back on all purchases, with no category restrictions, and an additional unlimited 5% cash back on hotels and rental cars booked through Capital One Travel.

There’s a $0 annual fee, and for the first 12 months, there’s a 0% introductory APR, followed by a variable APR ranging from 21.24% to 29.24%, based on your creditworthiness.

The card provides benefits like:

- Automatic payments

- $0 fraud liability

- Year-end summaries for simplified budgeting and tax preparation

- Account managers for assistance with purchases and payments

- Purchase record downloads in various formats

- Virtual card numbers for enhanced online security

The application process takes about 10 minutes, and decisions are typically made in seconds.

To apply, you’ll need to provide information about all business owners, including legal names, addresses, and Social Security Numbers, as well as details about your business, such as its legal name, address, and tax identification number (EIN).

You might also like: What are the Best Business Credit Cards for Travel?

4. BofA Business Unlimited Cash Rewards

The BofA Business Unlimited Cash Rewards credit card by Bank of America offers a $300 online statement credit bonus after spending at least $3,000 within the first 90 days of opening an account. It allows you to earn unlimited 1.5% cash back on all purchases, with no annual cap and no expiration on rewards.

Moreover, if you have a Bank of America business checking account and qualify for the Preferred Rewards for Business Platinum Honors tier, you can earn up to 75% more cash back, up to an unlimited 2.62% cash back on purchases.

This card features flexible redemption options, including depositing cash rewards into your Bank of America checking or savings account, receiving a statement credit, or getting a check mailed to you.

There’s no annual fee, and it offers a 0% introductory APR on purchases for the first 9 billing cycles, followed by a variable APR ranging from 18.49% to 28.49%—The card provides various features to manage cash flow, online and mobile access for account management, travel and emergency services including travel accident insurance, free access to business credit scores, security measures such as zero liability protection and fraud monitoring.

Notable: It also offers Balance Connect® for overdraft protection when linked to a Bank of America business checking account.

Recommended: What is the Best Bank of America Business Credit Card You Can Get?

5. Chase Ink Business Unlimited

The Ink Business Unlimited® Credit Card from Chase offers a substantial new cardmember bonus of $750 cash back after spending $6,000 on purchases within the first 3 months of opening an account. With no annual fee, this Chase business credit business card allows you to earn unlimited 1.5% cash back on every purchase made for your business.

For the first 12 months from account opening, there’s a 0% introductory APR on purchases, which then transitions to a variable APR of 18.49%–24.49%. You can redeem your rewards on this card for cash back, gift cards, travel, and more through Chase Ultimate Rewards®.

Employee cards come at no additional cost and allow you to set individual spending limits while helping you earn rewards faster. Additionally, until March 2025, you can earn a total of 5% cash back on Lyft rides with your Chase Ink Unlimited card, which includes an extra 3.5% on top of the 1.5% you already earn on travel.

Chase also offers referral incentives for existing cardholders, allowing them to earn up to 200,000 points per year by referring businesses for any Chase Ink® Credit Card.

You might also like: Chase Ink Business Preferred Credit Card: A Deep Dive Analysis

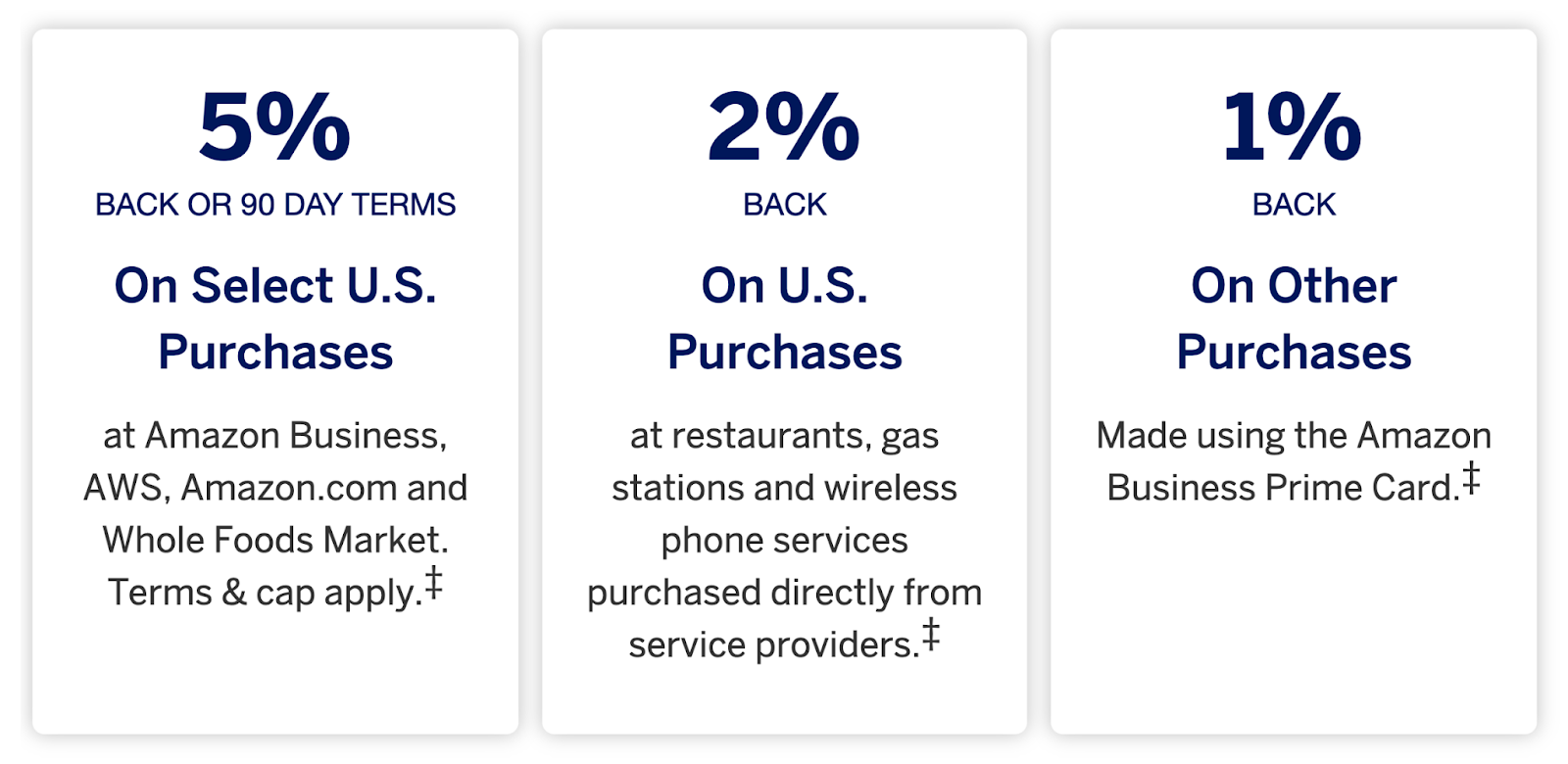

6. Amex Amazon Business Prime

The Amazon Business Prime Card, offered by American Express, comes with a $0 annual fee and offers a $125 Amazon.com Gift Card upon approval. It features a variable APR ranging from 19.49% to 27.49% on purchases, based on creditworthiness.

This card rewards your business with:

- 5% cash back or 90-day terms on select U.S. purchases at Amazon Business, AWS, Amazon.com, and Whole Foods Market, with a cap of $120,000 in purchases each calendar year with eligible Prime Membership, and 1% back thereafter.

- 2% cash back on U.S. purchases at restaurants, gas stations, and wireless phone services purchased directly from service providers.

- 1% cash back on all other eligible purchases.

Additional benefits include Amazon Business Enhanced Data Views for detailed expense tracking, Amazon Shop with Points for flexible reward redemption, and no foreign transaction fees.

You can manage expenses efficiently with features like Account Manager, Employee Cards with spending limits, and integration with QuickBooks® for auto-expense categorization – Moreover, cardholders receive baggage insurance, car rental loss and damage insurance, extended warranty protection, purchase protection, and access to Amex Offers for additional rewards.

Recommended: Amazon Business Prime Credit Card: Full Review +How to Get One

Frequently Asked Questions

What credit score do you need for 0% APR?

Typically, you need a good to excellent credit score (usually 670 or higher) to qualify for a 0% APR offer on a credit card. Each card issuer has their own underwriting and qualification terms.

Why 0% APR offers might not be good for your credit?

0% APR offers can impact credit negatively if not managed properly. They may encourage overspending, leading to higher debt levels. Additionally, opening new credit accounts can temporarily lower your credit score due to inquiries and reduced average account age.

Is 23% APR high for a credit card?

Yes, a 23% APR is slightly above the average for credit card APRs, which was around 21.47% according to Federal Reserve data.

Is 29% APR high?

Yes, a 29% APR is significantly higher than the average credit card APR, indicating high-risk lending.

Final Thoughts

Leveraging 0% APR business credit cards can be a savvy financial move for entrepreneurs – It provides a valuable opportunity to manage expenses without accruing interest. With a clear understanding of what constitutes a good APR for a business credit card, the availability of 0% APR cards, and the top options currently on the market, you’re better equipped to make informed decisions tailored to your business needs.

Remember to consider factors like introductory periods, ongoing APR rates, and additional perks and benefits when selecting the right card for your business. With careful management and responsible use, these cards can serve as valuable tools for financial flexibility and growth.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!