If you use a Square card reader, they may have offered you a business loan. If you’re trying to grow your business or you’ve got an immediate opportunity that you’d need financing to afford, you may be considering it. But, you want to know more about Square business Loans.

How long does it take to get a Square business loan? Do Square loans affect your credit? What percentage do they take for repayment? I answer these questions and more here.

This is what’s in store:

- What is a Square Business Loan?

- How Do Square Business Loans Work?

- Frequently Asked Questions

- Conclusion: Are Square Business Loans Legit?

Now, let’s dig in!

What is a Square Business Loan?

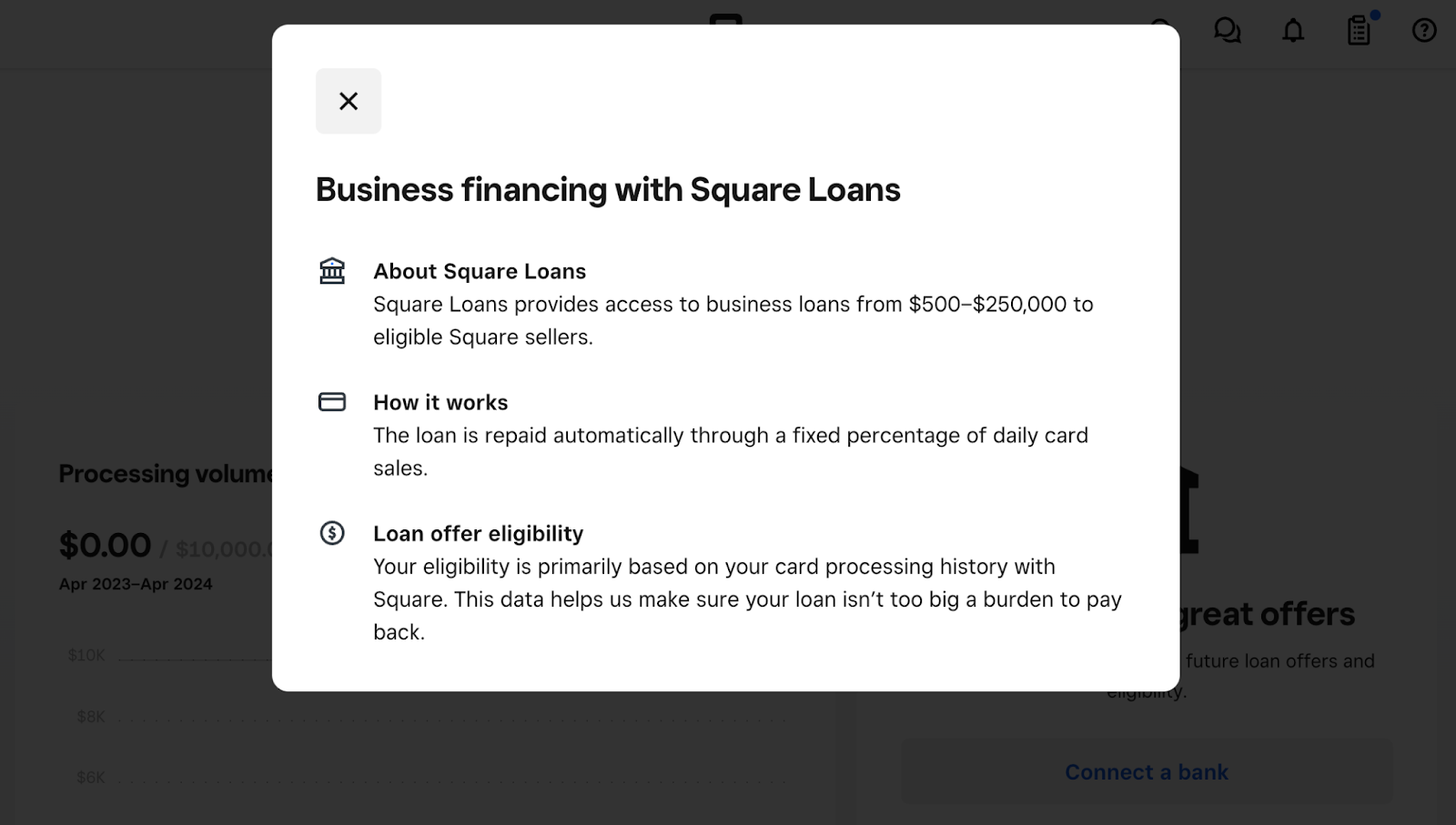

In a nutshell, a Square business loan is a cash advance financing offer for small businesses that use Square for payment processing.

It’s designed to provide quick access to capital for business needs like:

- Purchasing inventory

- Covering operating expenses

- Investing in growth opportunities

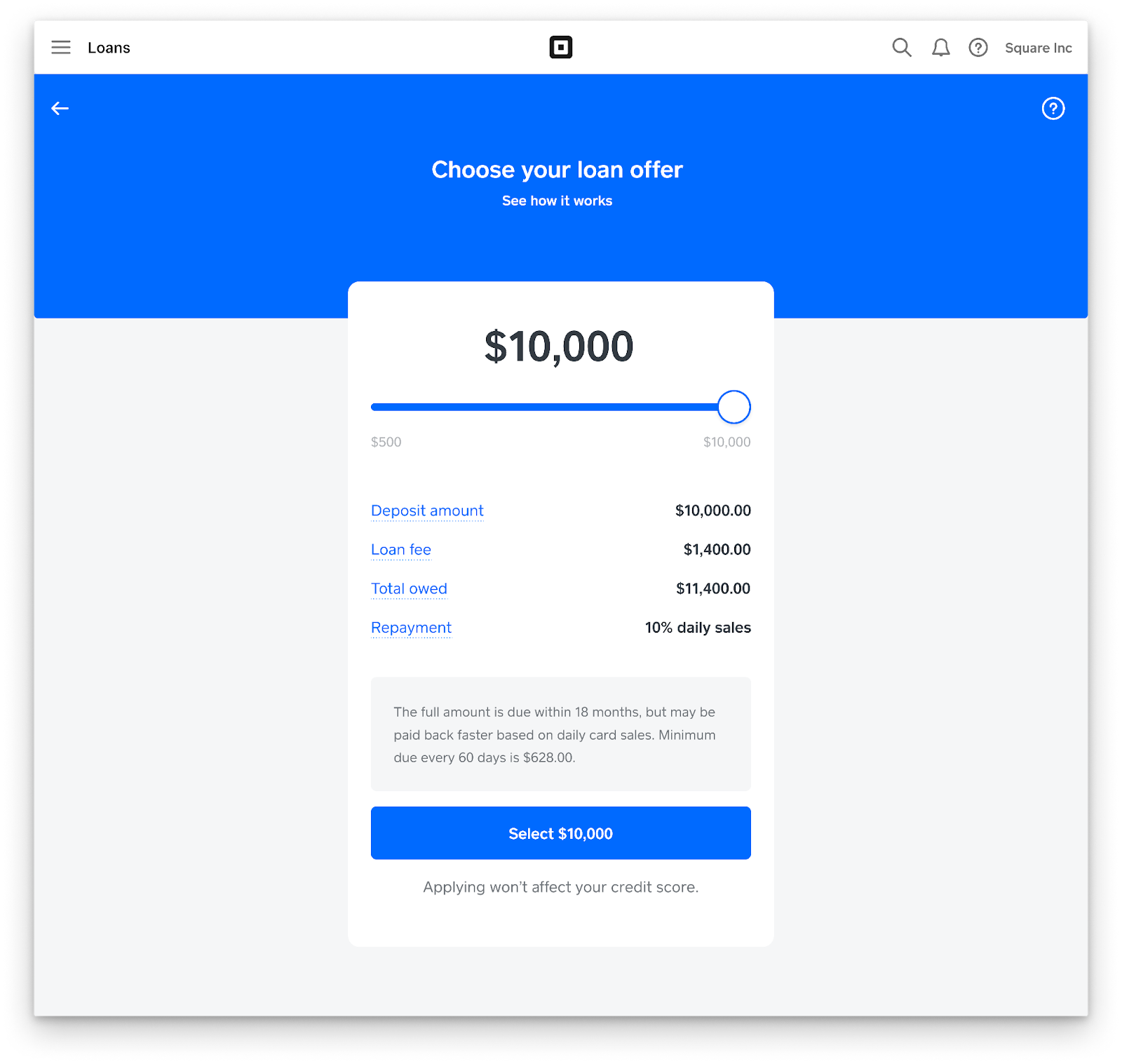

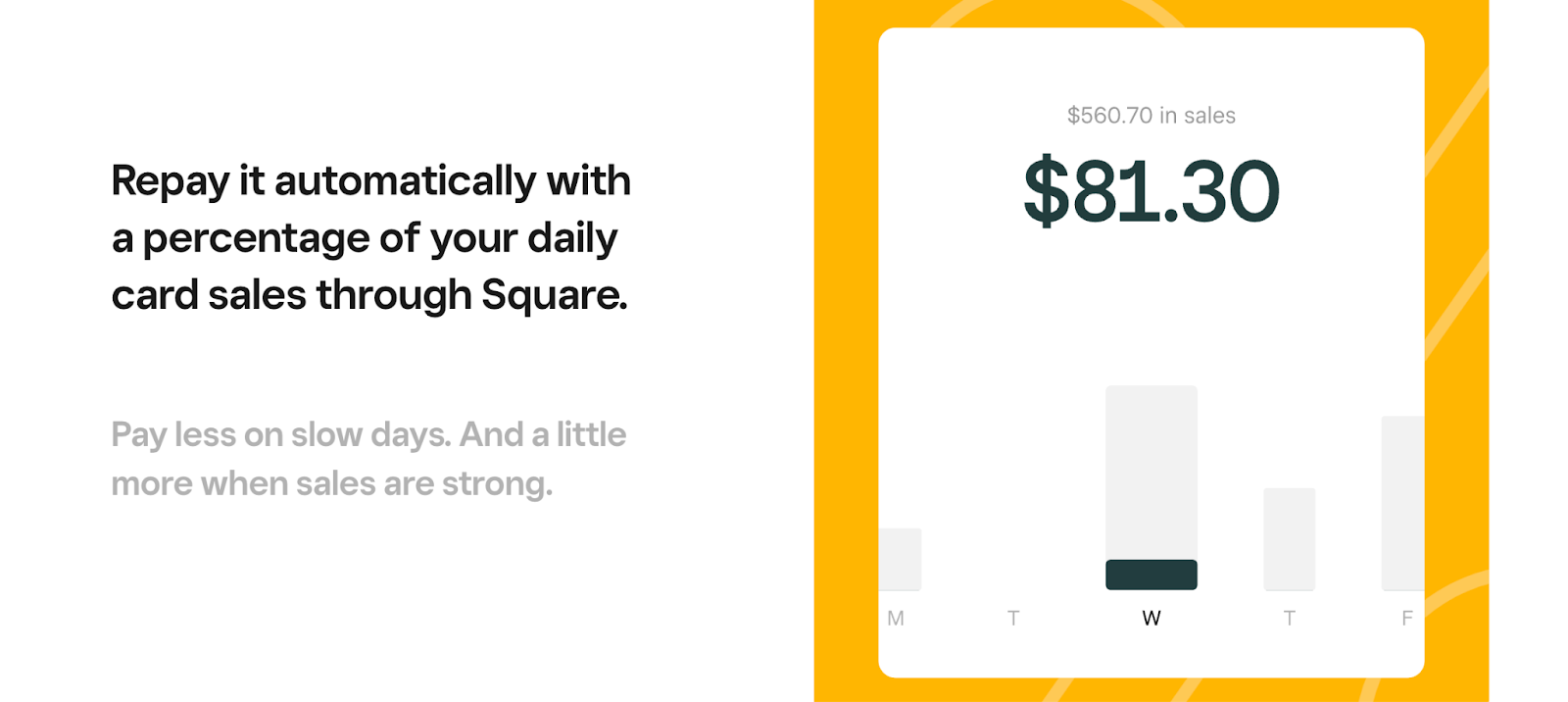

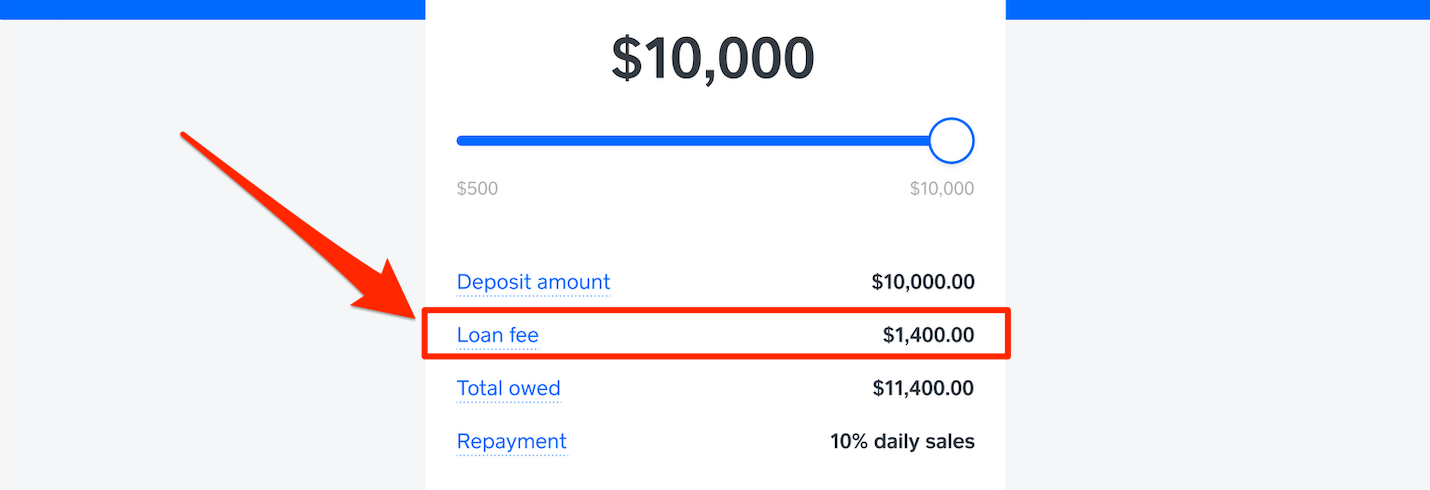

The loan amount can range from $300 to $250,000, and the repayment structure is straightforward: instead of traditional interest, there’s a flat fee, and you pay back a fixed percentage of your daily card sales through Square until the loan is fully repaid.

On days when your sales are high, you pay more towards the loan, and on slower days, you pay less. The loan offer is based on factors like your business’s payment processing volume, account history, and payment frequency.

You can make prepayments without any penalty. Square loans do not require a personal guarantee. And, there are no late fees or additional charges apart from the initial flat fee associated with the loan amount.

You might also like: What’s the Best Payment Processor for a Small Business? Really

Square Business Loan Cost

Square loans don’t have a traditional interest rate. Instead, they charge a flat fee – “factor rate” – and then automatically deduct a percentage of your daily sales until the loan is paid off. For example, if you took an $8K loan with a $1K fee, Square might deduct around 15% of your daily sales to repay the loan, which is an example from a real borrower.

Business owners have reported varying factor rates on Square loans:

- 1.13 (13.68% on a $95K loan)

- 1.14 (14% on a $1K loan)

- 1.135 (13.56% on a $31.7K loan)

Editorial reviewers have reported Square business loan factor rates between 1.10 and 1.16 (10-16%). Again, this is not the same as APR and does not represent an interest rate.

You might also like: The Payoff Loan Review: Is This the Debt Consolidation Option for You?

Company Overview

Square Inc. is a San Francisco-based, private, for-profit company that was founded in 2009 by Jack Dorsey and Jim McKelvey. The mission was to make it easier for small businesses to accept credit card payments.

Their key industry markets are, restaurants, retail, and beauty. Square’s first product was a credit card reader that could be plugged into an iPhone to process cards on the go.

Now, they offer a large vast range of business products including:

- Commerce solutions like payment hardware and POS, invoicing, an online ordering platform, and shoppable websites.

- Customer marketing products including email and SMS marketing, loyalty programs, customer management, gift cards, and photo studio.

- Staff management tools like scheduling and time tracking, team accounts, and human resources.

- Business banking that includes checking, savings, loans, and credit cards.

- Technology and development including dev specialists, access to APIs (for integration with business software), and a dedicated app marketplace.

Jack Dorsey remains in the driver’s seat as the company’s current CEO (he stepped into this position in 2022), and is also the co-founder and chairperson of Block Inc.

Block® is the parent company of Square®, Cash App®, Spiral®, and Tidal®.

So, Square’s leadership is pretty corporate-minded, and employees seem to like that. According to Glassdoor®, most staff would recommend working at Square to a friend (72%) and approve of the CEO (74%).

The majority of Square’s business customers seem to approve as well, with a 4-star trust rating on Trustpilot. Overall, Square receives positive feedback from users who appreciate its easy-to-use platform and helpful customer service. Customers value features like simplified navigation, quick deposits, and convenient payment options.

Many have remained loyal to Square for years, citing its reliability and integrated functionalities for managing listings, reporting, and website credit card processing. However, some users have encountered issues with account deactivation and slow customer service response times, indicating areas for improvement in Square’s service experience.

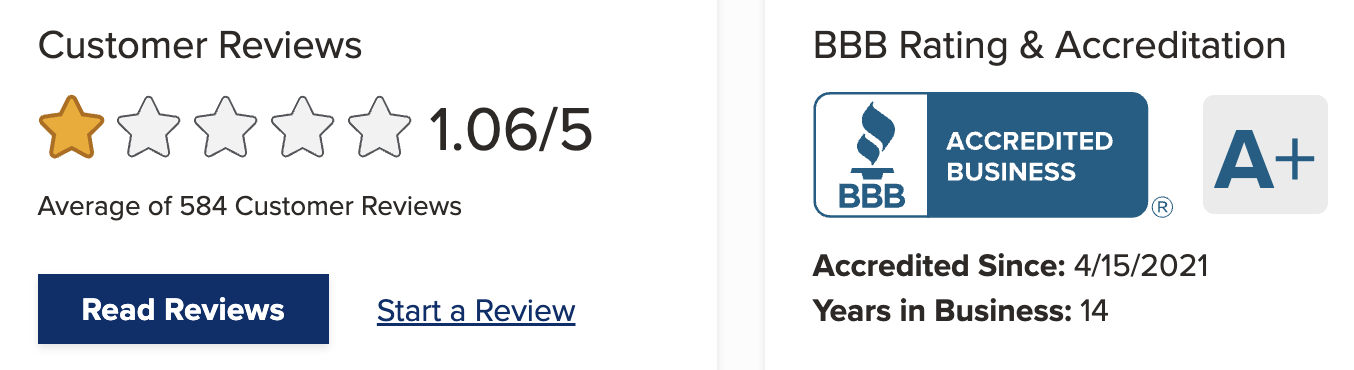

Meanwhile, Square Inc. has a 1.06-star customer rating and A+ rating with the Better Business Bureau (BBB).

It always surprises me to see how BBB grades are issued. Square Inc. has had 1,041 complaints closed on the platform in the past 12 months and 3,255 in the past 3 years—This seems high to me.

As of January 26, 2024, Block is facing a class action over a provision in its terms of service barring users making any “objectionable” statements about the company in public. The parent company is actually party to several ongoing legal cases, both as a plaintiff and defendant across the country. But, I didn’t see anything to make me think that the company is conducting fraudulent business.

Finally, Square business loans are issued by Square Financial Services, Inc., a Utah-Chartered Industrial Bank. Member FDIC.

You might also like: Novo Bank Review: First-Rate Small Business Banking or Scam?

How Do Square Business Loans Work?

Now that we have all the fine details out of the way, let’s explore the features of a Square loan and what you can expect if you decide to accept an offer. In all, the process is pretty automated and convenient, but there are caveats you should be aware of.

1. Automated Offers

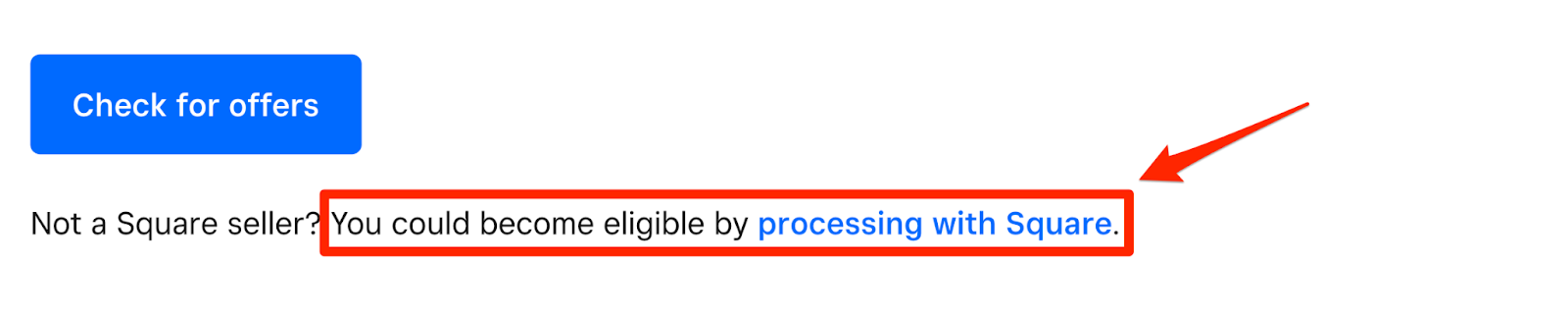

With Square business loans, you don’t apply for a loan—instead, you accept an offer through your dashboard. The platform looks at the eligibility factors, then lets you know if you can secure extra funds for your business.

Qualified businesses will receive an offer through their dashboard and via email if their account looks like a good fit for funding. Then, all you need to do is accept it.

You might also like: Y Combinator: Fast Track to Success or Waste of Time?

Square Business Loan Requirements

To get an offer, you will need to meet certain requirements. First of all, you need to use the Square payment processing platform.

Then, Square looks at several performance-based factors to determine loan eligibility:

- You should process at least $10,000 in a year through Square to be eligible for a loan offer.

- Your Square account should show consistent payment processing to show that you can repay the loan through your account transactions.

- A good mix of new and returning customers will strengthen your ability to qualify.

- Payment disputes and chargebacks can make you ineligible for a Square loan.

- Your bank account will be reviewed for insufficient funds, which will impact your eligibility.

- Payment limits or reserves on your Square account could disqualify you.

If you have multiple Square accounts or locations with outstanding Square loans, they should all be in good standing, actively processing transactions, and loan repayment needs to be current.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

2. No Personal Guarantee

There is no personal guarantee (no PG) on a Square business loan—This means that Square won’t come after your personal assets if the loan defaults. And, no PG typically means no hard credit pull, and no impact to your credit score.

For loan amounts up to $100,000, Square doesn’t need any collateral.

However, for loans that exceed $100,000, they may secure your business assets and file a Uniform Commercial Code (UCC) statement with the Secretary of State (SoS) in your business’s jurisdiction.

Filing a UCC statement with the SoS creates an official record that establishes a Square’s interest in your business assets. This filing serves as a public notice to inform others, such as potential lenders or buyers, that the creditor has a security interest in your assets.

By filing a UCC statement, the lender is protecting their interest in case you default on the loan—It establishes a legal claim or lien on specific business assets like:

- Inventory

- Equipment

- Accounts receivable

This process is important for secured transactions and helps lenders secure their position in case of business insolvency or default…you won’t have to worry about this at all if your loan is less than $100K.

You might also like: No-Doc Business Loans: Get Funds Without Proof of Income

3. Quick Funding

Square’s funding process is streamlined for speed and efficiency, aiming to deposit funds into your account as quickly as the next business day.

When you apply for a loan, you’ll usually receive an immediate decision on approval, and this won’t have any impact on your credit score.

Recommended: How Long Does It Take to Build Business Credit? Fast Guide

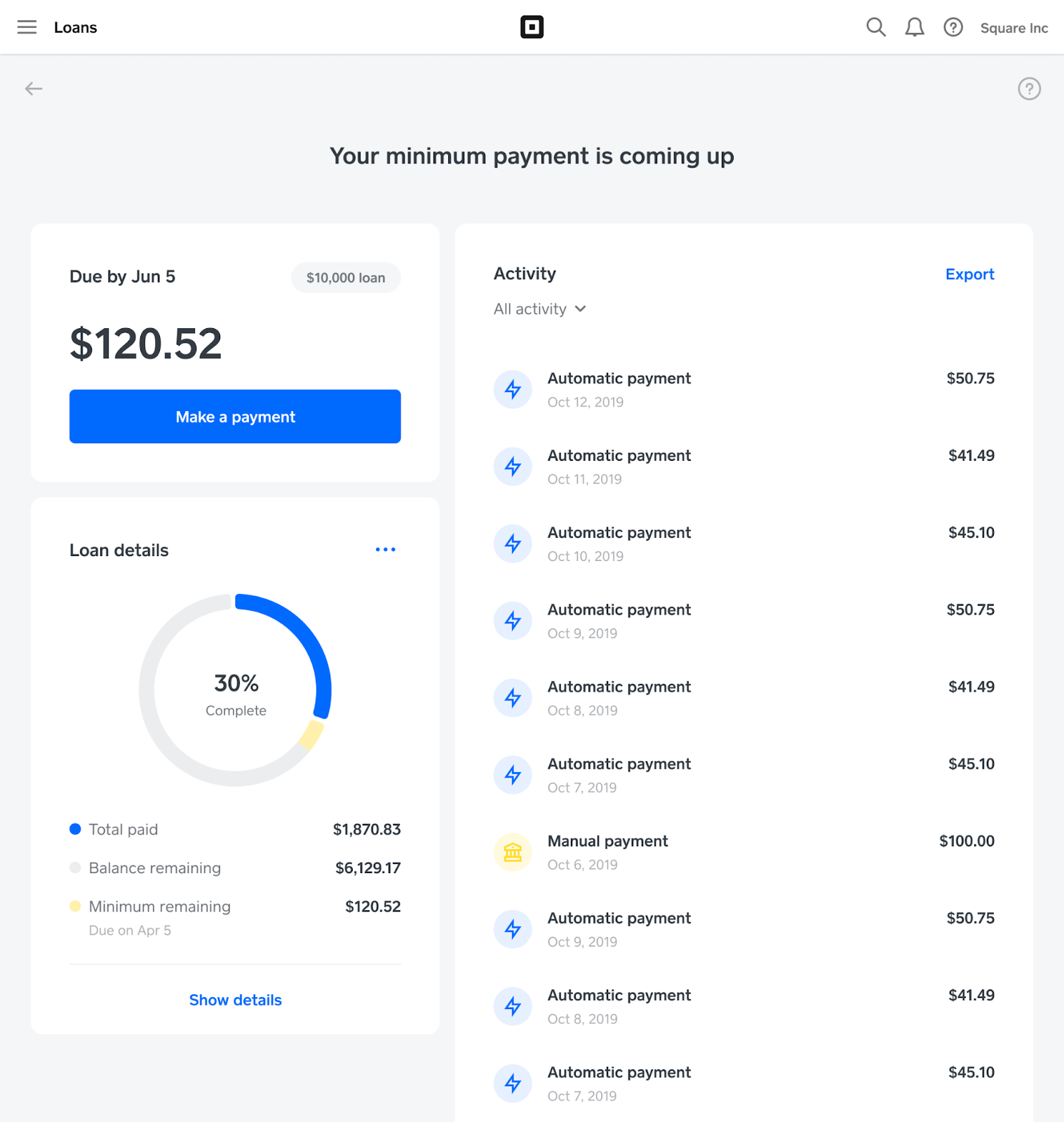

4. Automatic Repayment

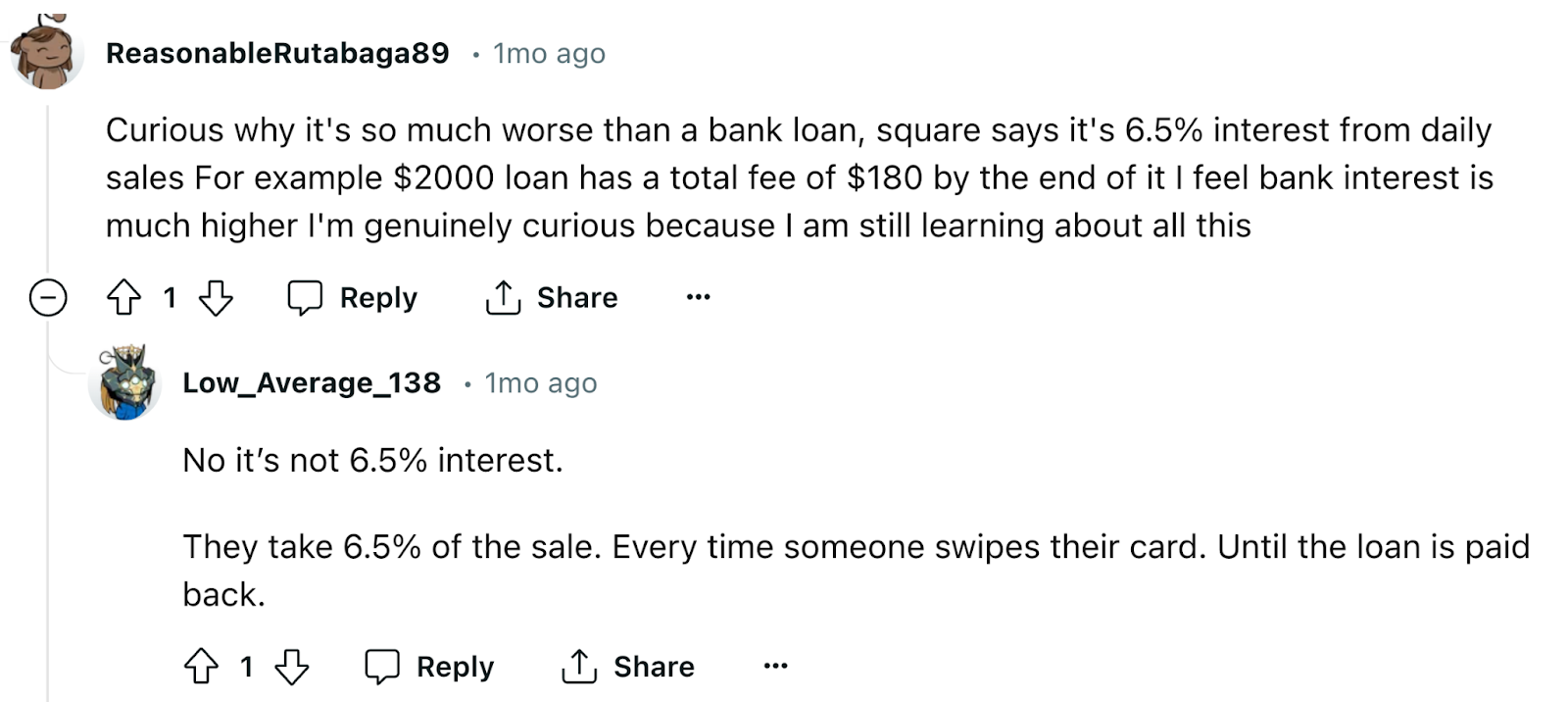

Square loans are repaid as a percentage of your daily sales. When business is good, payments are higher and on slow days, payments are lower—This is typical with a cash advance versus a fixed payment with a traditional business loan.

The daily repayment method can result in an effective rate that’s higher than what you would probably find with a bank loan or credit card. While this type of loan can be convenient, it’s important to understand the total cost and impact on your cash flow, especially during slower months.

Anecdotally, I’ve seen borrowers mention repayment terms with percentage of daily sales as low as 6.5% and as high as 21%. If your repayment plan is charging too much, you may be able to negotiate lower daily repayment.

Moreover, Square loans require a minimum payment of 1/18th of the initial loan balance every 60 days, and the full loan amount must be repaid within 18 months. With this structure, for an $8K loan with a $1K fee, you would need to make a payment of at least approximately $444.44 every two months, and the total loan (including the fee) would need to be repaid within a year and a half at a rate of approximately $500 per month.

You might also like: Could a Stripe Capital Loan Get Your Business Through a Rough Patch?

5. Transparent, Fixed Costs

Before you accept a loan, you will see the loan amount, fees, and repayment percentage upfront. It’s pretty straightforward.

But, on top of the loan fee, you will pay processing fees on each transaction—all payment processors charge these fees in addition to any loans you might be repaying.

Square’s processing fees differ based on the payment method:

- For in-person transactions, 2.6% of the transaction amount plus 10 cents per transaction.

- For online payments, 2.9% of the transaction amount plus 30 cents per transaction.

- For invoice payments, 3.3% of the transaction amount plus 30 cents per card transaction, or 1% with a minimum of $1 per transaction for ACH bank transfers.

- For manually entered transactions, 3.5% of the transaction amount plus 15 cents per transaction.

So, between the loan repayment and processing fees, you could pay upwards of 12.6% to 19.5% of each transaction until your loan is settled.

You might also like: What You Need to Know About PayPal LoanBuilder for Business

6. The Square App

The Square Point of Sale (POS) app is available in the Google Play and Apple app marketplaces. It lets you accept payments easily using credit cards, contactless payments (like Google Pay and Apple Pay), gift cards, and invoicing right from your phone or computer.

Within the app, you can:

- Manage your inventory

- Track sales

- View reports

Plus, you’ll have funding options such as next-day transfers to your bank account for a fee or free transfers in one to two business days.

Many users find it straightforward to use and appreciate its integration with other Square tools like eCommerce and team management. However, some people have experienced issues with customer support and account deactivation, so it’s important to keep that in mind.

You might also like: Expensify Card Review: A Detailed Expense Tracking Analysis

Frequently Asked Questions

When does Square offer you a new loan?

Square offers loans through its Square Capital program based on your account activity and sales performance. Eligible sellers are notified of loan offers within their Square Dashboard or through email. Some borrowers have been offered new loans while still in repayment for a current loan.

What is the limit on Square business?

The loan amount offered by Square Capital varies based on your business’s processing history, sales volume, and account activity. Square does not publicly disclose a fixed maximum limit, but you can check your eligibility and view loan offers in your Square Dashboard or contact Square Support for more details.

Conclusion: Are Square Business Loans Legit?

In short, yeah, Square business loans are cash advances that are offered by a legitimate, trusted company. Cash advances have been known to get businesses through a rough patch or quickly fund short-term needs.

However, they have always been the business equivalent of a personal payday loan. I never recommend that business owners take out a cash advance, or any other factored loan, unless there is absolutely no other alternative—This is because the costs are too high.

Instead, I suggest you research all of your options and take advantage of the offers that charge the lowest rates to optimize your business finances.

Do you want to learn how to obtain up to $100K in as few as 30 days? Join Business Credit Workshop today!