If you’ve come across Torro Business Funding, you may have been referred by a franchise or an Instagram influencer. And, they may be offering you the funds you need to start or grow your business…But, for some reason, you’re still wondering if they’re legit.

Here, you can find out what Torro Business funding is (how it’s different from a conventional lender), learn about the company, and explore what you can expect from their offer. You’ll even find answers to some common questions about this type of lending.

This is what’s in store:

- What is Torro Business Funding?

- What Does Torro Business Funding Do?

- Frequently Asked Questions

- Conclusion: Is Torro Funding Legit?

Now, let’s dive in!

What is Torro Business Funding?

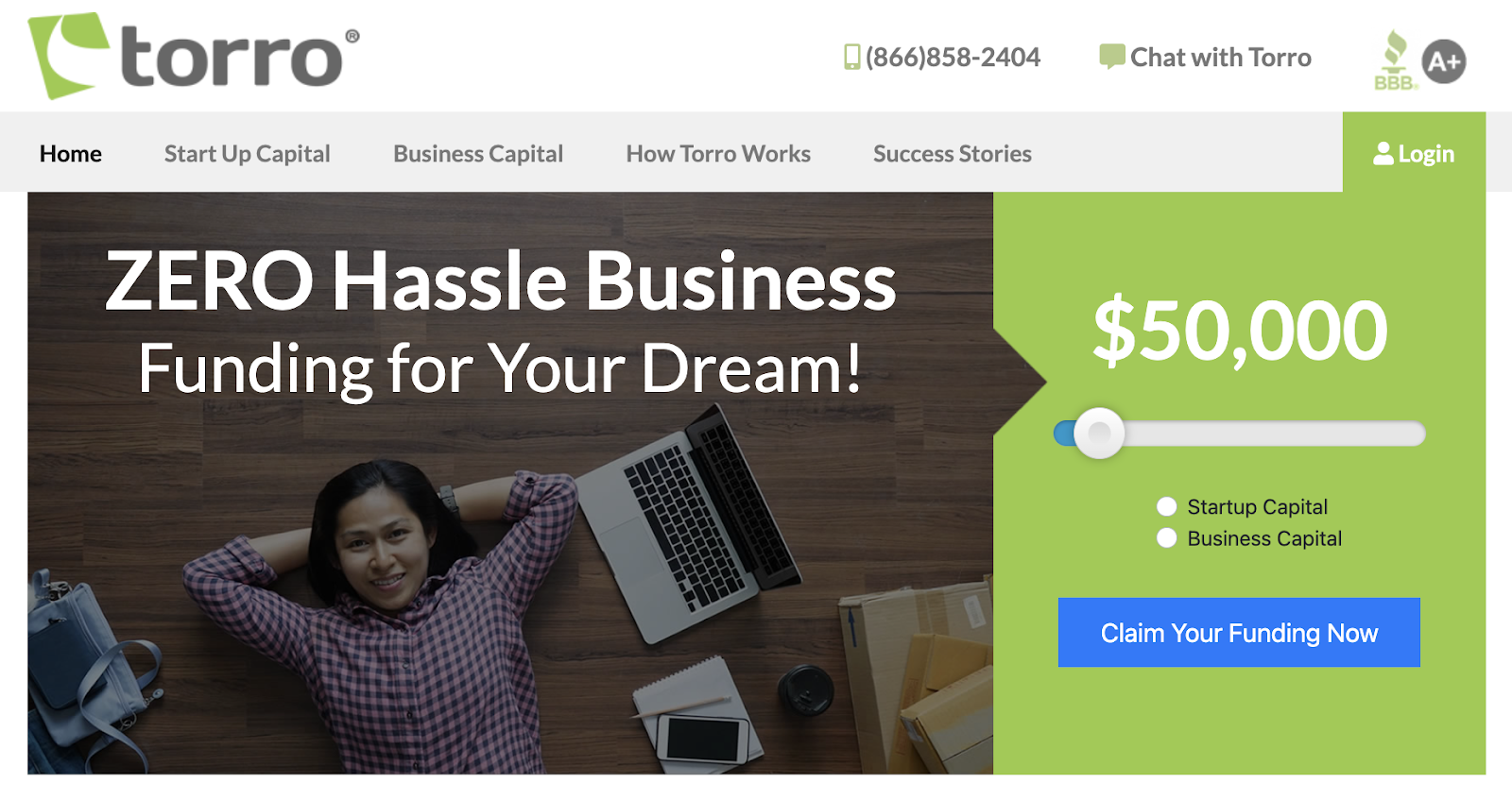

Torro is known as a source of “startup capital” and “business capital” – they offer hassle-free financing solutions geared toward small businesses. Torro is an alternative financial service provider that specializes in addressing cash flow and working capital needs.

Unlike traditional banks and lenders, Torro offers a streamlined approach to access funds, and they emphasize the convenience and efficiency this offers business owners.

Whether you’re a post-revenue business seeking expansion or a pre-revenue startup in need of initial capital, Torro has tailored funding options to help you get cash to expand your business.

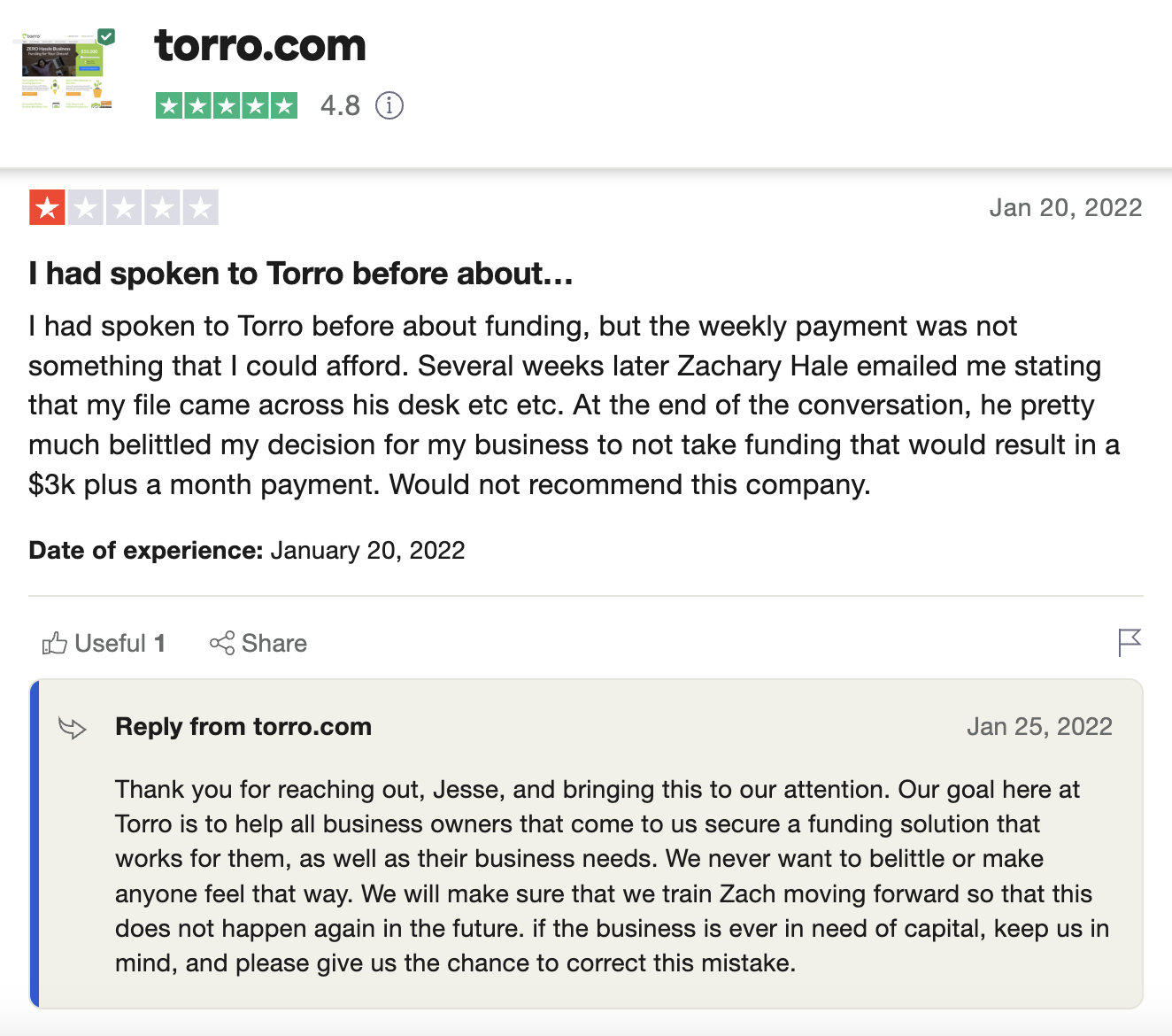

Interestingly, most of the small number of poor Trustpilot reviews seem to come from business owners who decided not to work with Torro after the initial consultation. Otherwise, they maintain a high rating on the platform (this is always impressive for a financial offer, as long as there reviews are real).

For pre-revenue businesses — which includes startups, franchises, or those looking to purchase a business — Torro offers a three-step process to obtain unsecured working capital (startup capital) between $5K to $125K to kickstart your business.

For post-revenue businesses, Torro claims to simplify the process with a quick online application (business capital) to help you grow your operations with $5K to $725K.

Within their wide funding range, they seem to have something for everyone.

You might also like: How to Interpret Lendio Reviews: Is This Funding Company Legit?

Torro Funding Requirements

Torro’s funding is considered working capital. With this type of loan, repayment can happen as a percentage of your daily sales, and is most often “factored.” Factoring involves selling accounts receivable to a third party (“lender”) at a discount for immediate cash, while interest loans entail borrowing a sum of money that must be repaid with interest over time.

So, working capital loans are kinda like a payday loan for business. Because of this, their requirements are a bit more lax than a traditional business loan.

When you come across an offer that seems like it could be too good to be true, it’s only natural that your hair would stand up on end. I never recommend this type of loan, unless a business owner absolutely has no other option. The reason is that they tend to be the quickest and easiest funding you can get, but they are more expensive.

Bear in mind, Torro is not the only alternative lender with relaxed requirements, and this isn’t a “scam,” it’s just a more expensive loan — i.e. not the most financially sound option you can take advantage of.

Recommended: Could a Stripe Capital Loan Get Your Business Through a Rough Patch?

Company Overview

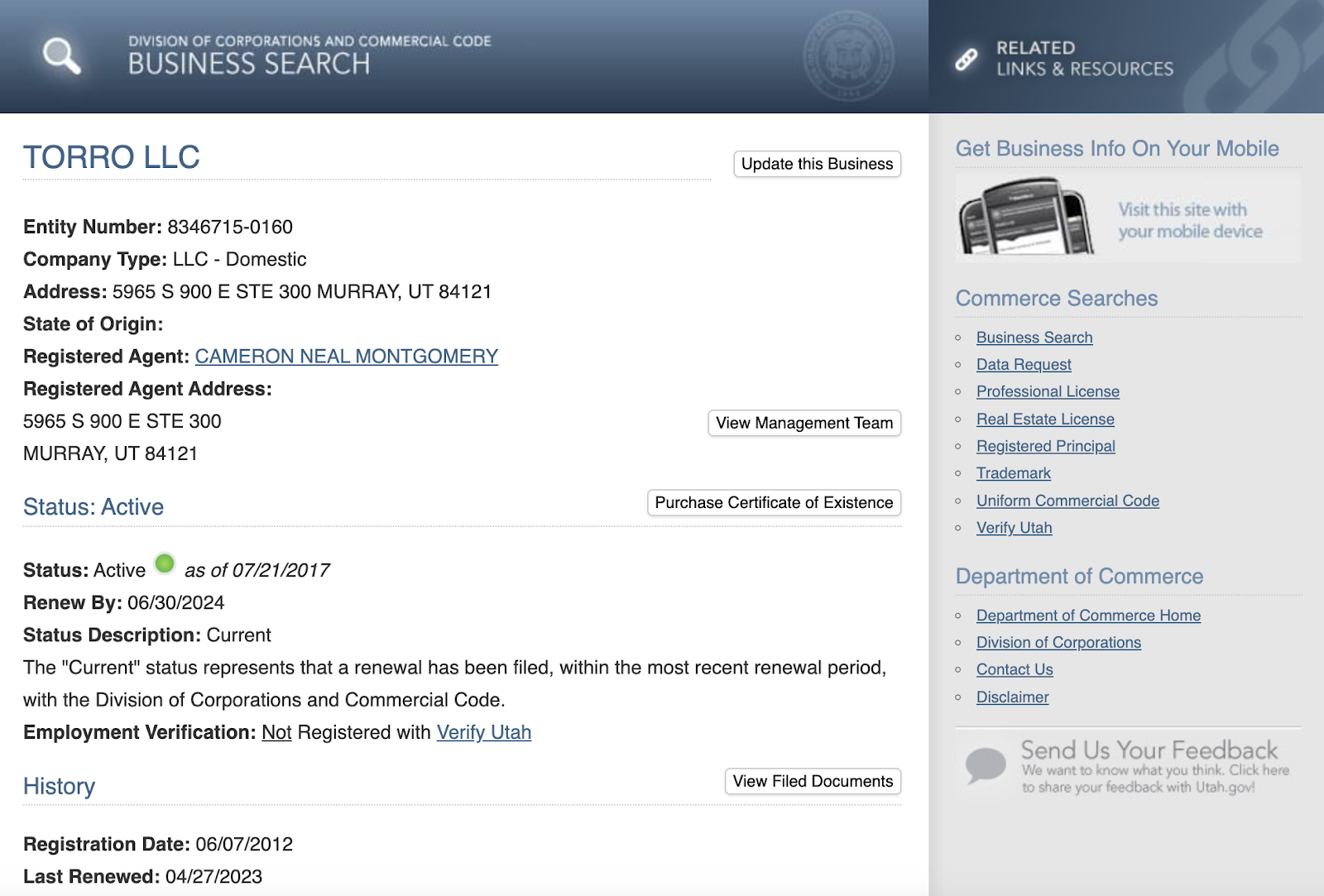

Established in 2015 and based in Salt Lake City, Utah, Torro LLC is an online funding platform, founded, owned, and managed by Cameron Montgomery. The company is in good standing with the Utah Division of Corporations and Commercial Code.

As the current CEO, Montgomery officially registered the company in 2012, and also does business as “The Broker Blueprint” – a training program that empowers individuals to become business loan brokers, connect borrowers with lenders, and secure financing for small businesses.

Prior to launching Torro, Montgomery didn’t share any work or education experience on LinkedIn.

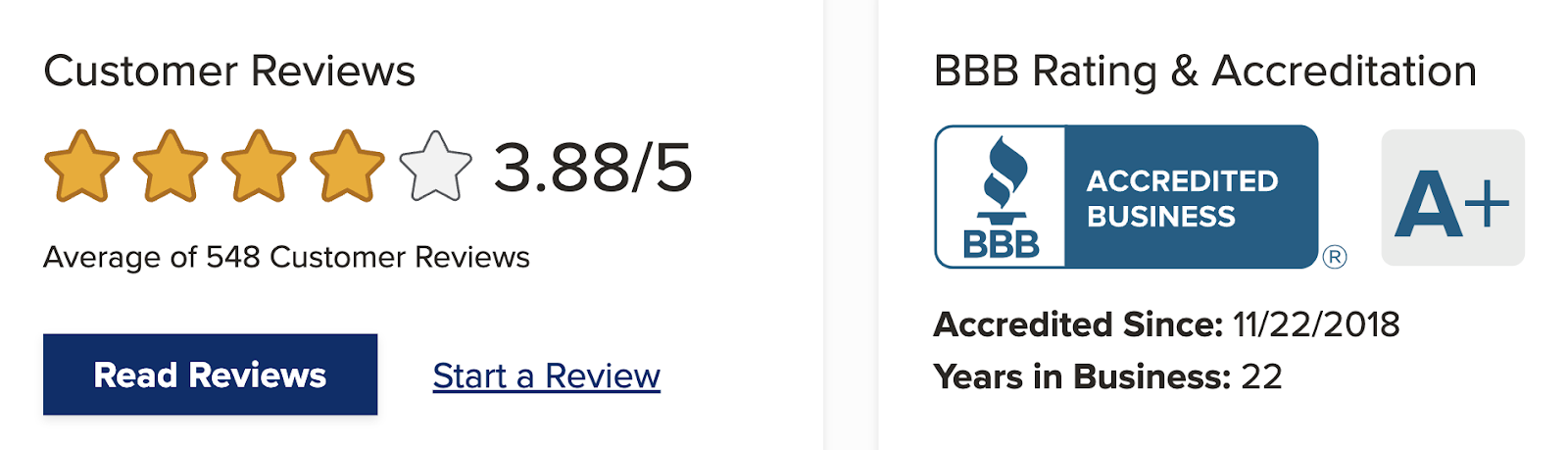

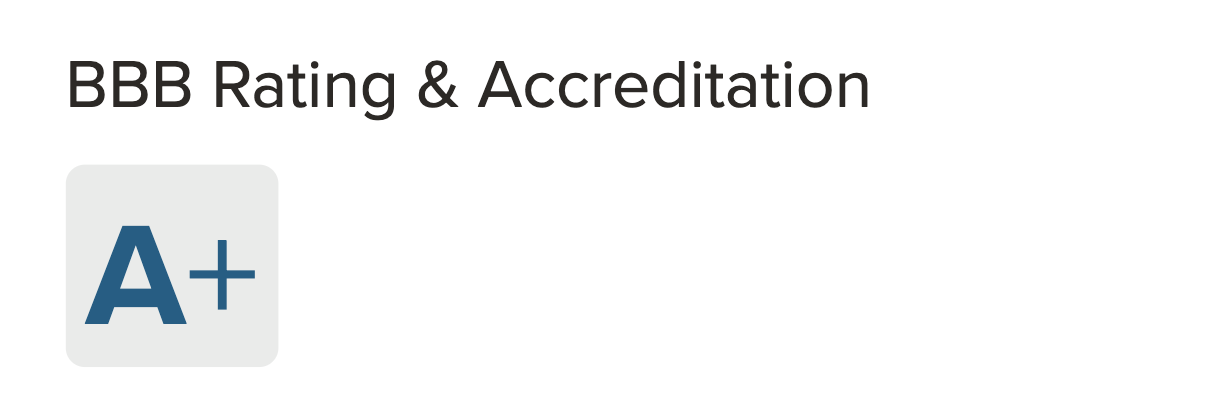

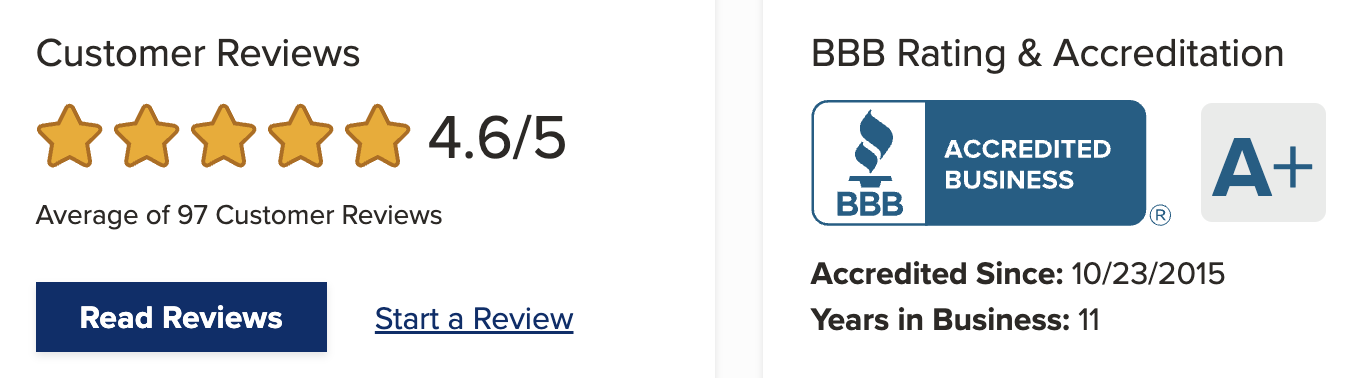

Torro is accredited with and maintains an A+, 4.6-star rating with the Better Business Bureau (BBB). I almost never see any positive reviews on the BBB website, let alone almost 90 of them. I’ll leave you to your own discretion on this one.

What I can say is that there have only been 7 complaints with the BBB in the past 12 months – It’s not uncommon to see 50+ for a financial offer.

I found one thing particularly odd – the company seems to have two websites that are exactly the same – one is at torro.com and the other at gotorro.com. It doesn’t seem like one of them is fake (Trustpilot cites torro.com and Crunchbase cites gotorro.com), so I have no idea why this would be.

In all, Torro Funding has been in operation for nearly a decade, and they’re in good standing in the areas where it’s necessary. However, this isn’t the most transparent company I’ve ever seen — I would like to have seen more information about loan rates and terms on the company website and the founder’s previous experience on LinkedIn.

You might also like: Superior Tradelines Review: Is it a Scam or Legit Way to Build Credit?

What Does Torro Business Funding Do?

In a nutshell, Torro small business funding is a means to get the capital you need quickly. Let’s take a look at their application process, speed of funding, and what you can expect from this offer.

Compared to other, comparable funding products, this one is pretty simple.

1. Quick, Online Application

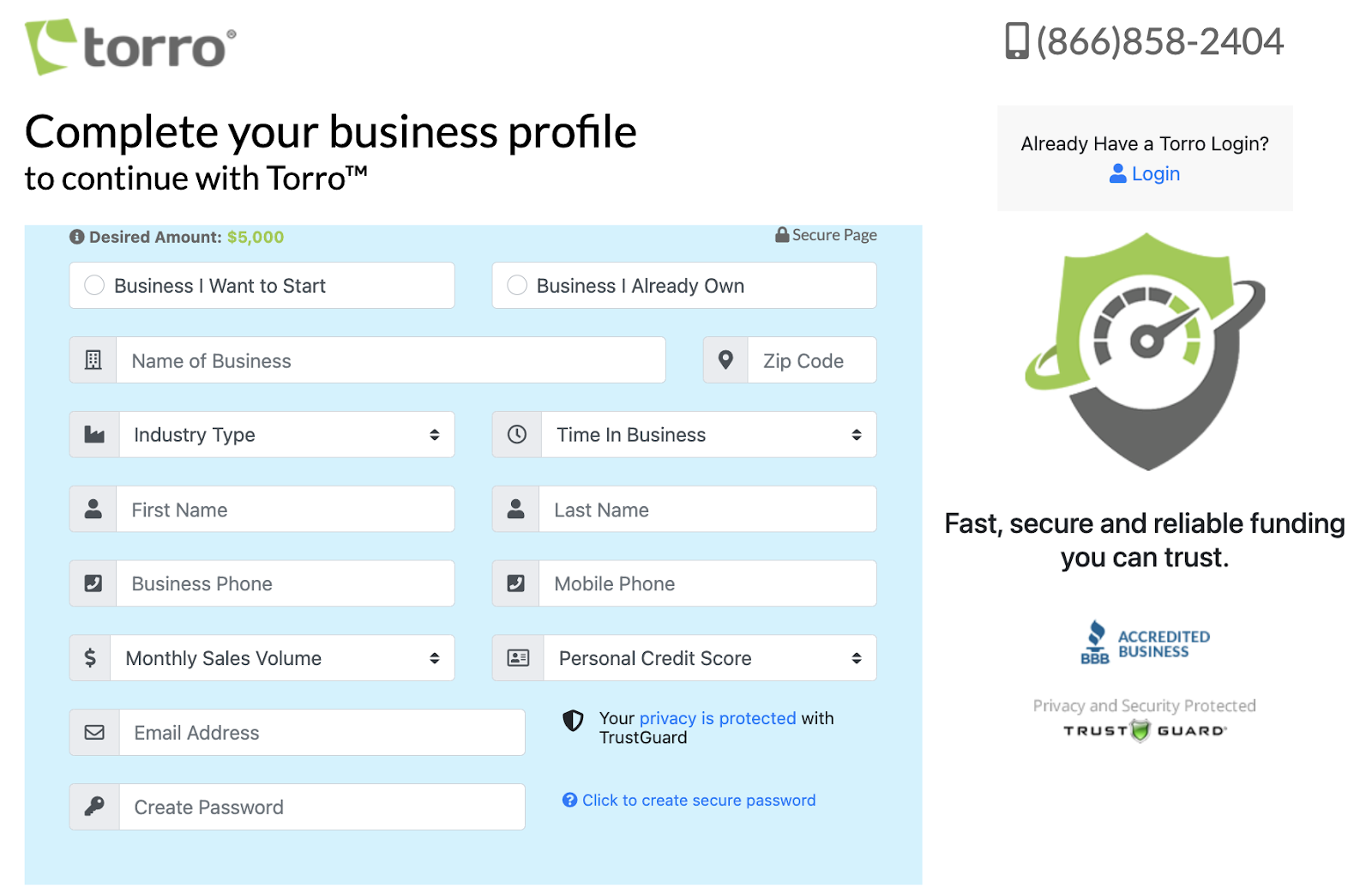

Torro’s online application asks only for the basic info about your business, like name, years in business, and your personal credit score. Of course, they want your income and contact info, but the pre-authorization doesn’t require that you enter your social security number.

You can supposedly create an online account during the application process, but it has to be manually approved. This probably helps weed-out the people who are just here to spy, and aren’t actually interested in business capital.

After you apply, you should get a call back within one business day.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

2. Funding Within a Week

With their proprietary QuickWrite® system, underwriting typically occurs within the same day, and approved businesses can access funding within 24 hours. To avoid unrealistic expectations, the video you’re taken to after you submit your application makes it clear that funding happens within a week.

This is pretty quick, as far as business loans are concerned, though there are competitors who offer funds with the same urgency.

Recommended: This is How to Build Business Credit Fast [Step-by-Step Guide]

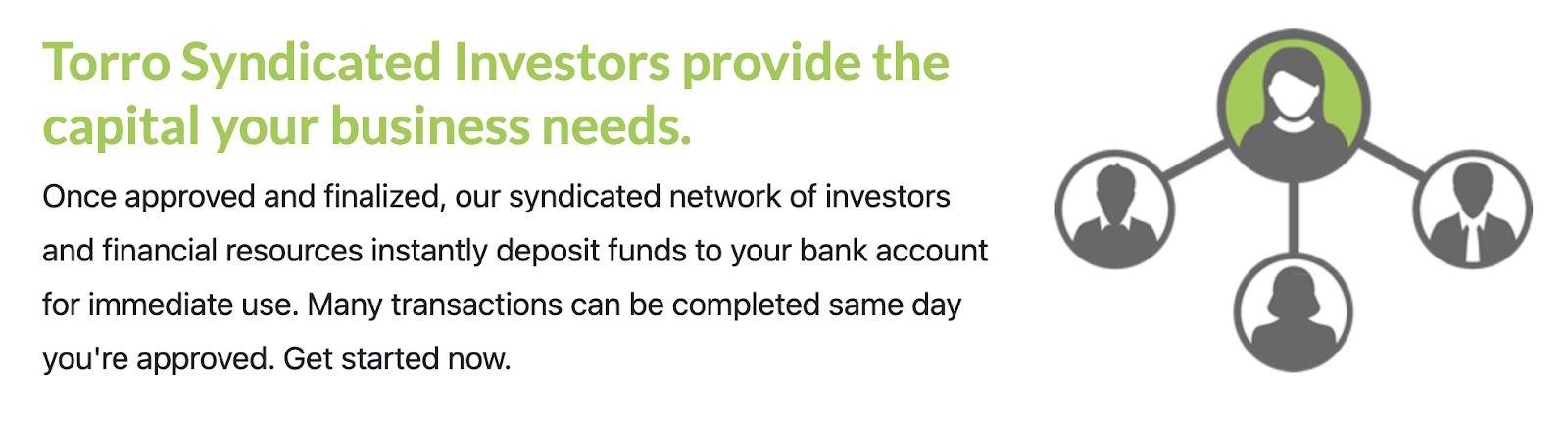

3. Syndicated Investor Financing

Torro has a network of investors who collectively provide the capital required by your business. Once the approval process is complete, these investors swiftly deposit funds into your bank account, often on the same day as approval, allowing you to utilize the funds immediately.

The loans are funded by a syndicated network of investors and financial resources associated with Torro – though, Torro doesn’t expressly state who these investors are. This is likely somehow related to Montgomery’s other program, The Broker Blueprint.

You might also like: This is How to Leverage Business Credit to Transform Your Life

Frequently Asked Questions

How can you get a business line of credit with no revenue?

To obtain a business line of credit with no revenue, you typically need to explore alternative financing options such as secured credit lines, personal guarantees, or presenting a strong business plan and credit history.

How do you know if a loan company is scamming you?

You can identify potential loan scams by researching the company thoroughly. Check for legitimate accreditation, verify contact information, read reviews, avoid upfront fees, and be wary of promises that seem too good to be true.

Are money loan apps safe?

Money loan apps can be safe if they are reputable, regulated, and adhere to strict security measures for handling personal and financial information. It’s crucial to review the app’s privacy policy, user reviews, and security features before using it.

Are cash advance loans safe?

Cash advance loans can be safe if obtained from reputable lenders and used responsibly. However, they often come with high interest rates and fees, you need to fully understand the terms and conditions before agreeing to a cash advance loan.

Are online loan requests legit?

Online loan requests can be legitimate if they are from reputable lenders or financial institutions. It’s essential to verify the credibility of the website, review customer feedback, read the terms and conditions carefully, and ensure the website is secure before submitting any personal or financial information.

Conclusion: Is Torro Funding Legit?

Again, Torro Funding is meeting the necessary requirements for a financial offer:

- Registered, active, and in good standing with the state of Utah

- Good ratings on Trustpilot and BBB

- Transparent ownership documentation

Plus, I like that they’re a privately-owned business, which has some appeal over doing business with a big bank (there are pros and cons to each.

Now, I would never step into a factored working capital offer unless it’s absolutely necessary — there are too many options that are much easier on your business budget. And, I wish there was more transparency into the loan rates and terms.

Whether or not this is an offer you want to take advantage of, I’ll let you decide.

Want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!