Torpago is a newer player in the corporate credit card game. And, they’re starting to pick up some traction in the business credit world. So, we’ve decided to examine their corporate credit card offer under a microscope and share our findings so that you can decide if this is the right option for you.

Here’s what we’re going to cover:

Now, let’s get to it!

What is the Torpago Business Credit Card?

For those who haven’t heard of it, the Torpago Business Credit Card is a corporate credit card and expense management platform. Corporate credit cards like this are designed for companies with multiple employees to enable staff to use a line of credit on authorized spending.

When I first landed on Torpago’s website, it put me in mind of Divvy — both have a corporate credit line, expense management, and virtual cards among other shared features. You’ll see a side-by-side comparison of the two offers before we wrap up.

Who Owns Torpago?

Torpago was founded by Brent Jackson in October 2018. Before launching this company, Jackson worked as the Operations Manager at Accrualify for a year and as a Senior Consultant at Deloitte for nearly half a decade. Jackson has a strong background in the business and finance industry.

Torpago Business Credit Card Benefits

In addition to 1% cash back on all spending, Torpago partners with other brands to deliver savings to their cardholders. So, if you use Quickbooks, Carta, Plastiq, or Doordash, and pay for these services with a Torpago card, you can get added discounts from 2.25% up to 40%.

The company will likely continue to partner with more brands, so users will be able to access more markdowns on other future services (though, we’re not certain what those will be).

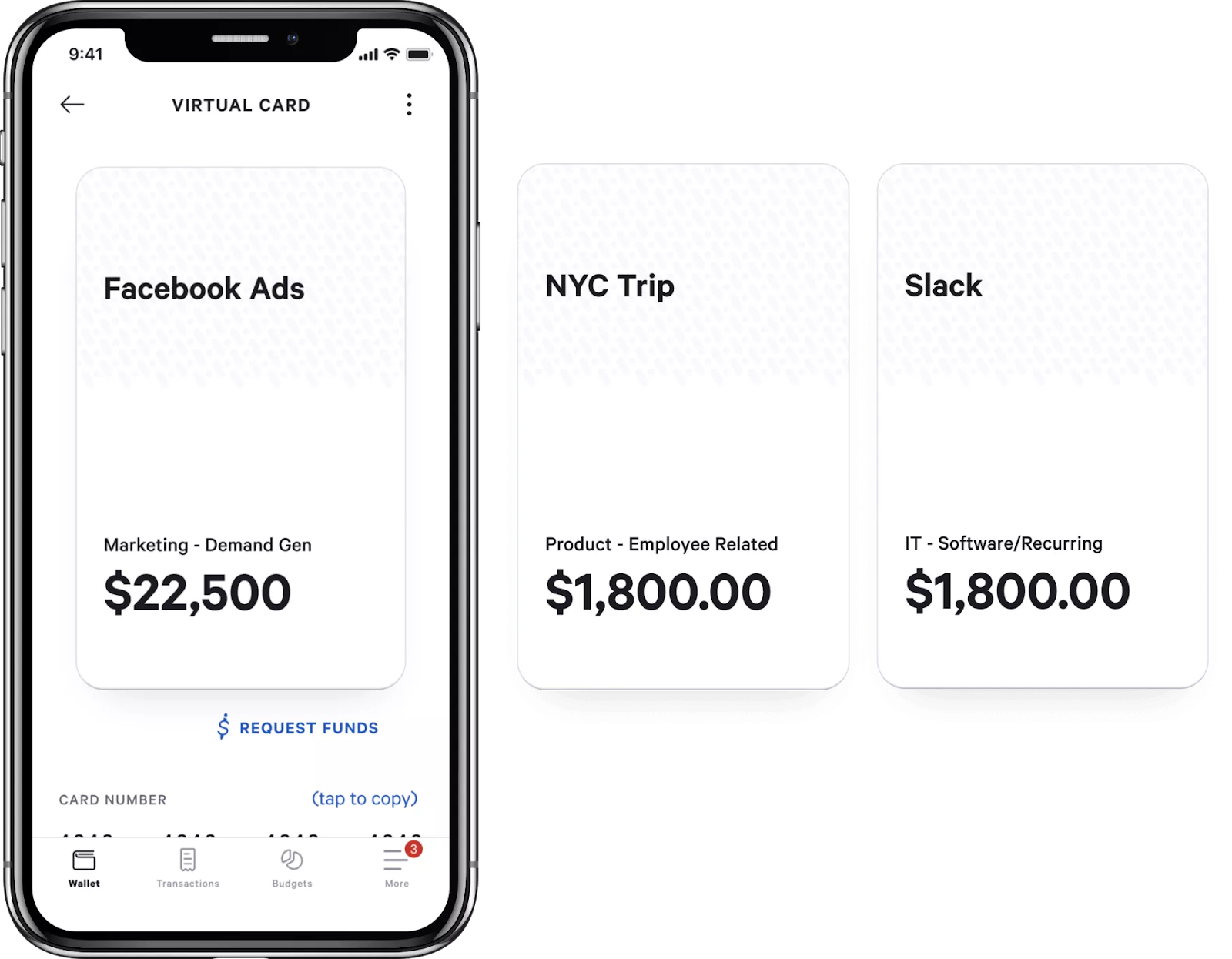

As mentioned above, Torpago gives cardholders both physical and virtual cards. Physical cards are Visa credit cards that can be assigned to multiple staff members for each corporate account. Virtual cards are digital credit cards that can be assigned instantly without the need to wait for a physical card to arrive in the mail. And, both physical and virtual cards can be assigned to an unlimited number of staff members (as long as the credit limit is not exceeded).

Automated expense tracking is another highlight that should get account holders excited. Each time a Torpago card is ran, data is sorted, synced, and accounted for. So, ideally, manual expense reports are eliminated.

Since the company is new, you can probably expect to see more future benefits.

Torpago Expense Management Features

One of the highlights of Torpago’s expense management platform is that it integrates with four other financial management platforms.

- Quickbooks Online

- Oracle Netsuite

- Financial Force

- Acumatica

So far and to my knowledge, no other corporate credit line and expense management platform has this many integrations (aside from maybe Stripe).

Torpago Customer Service

I did call the Torpago customer service number to ask if they have plans to add Quickbooks desktop to their integrations list. On that note, the Torpago phone number was a bit tricky to track down. If you are looking for it, they can be reached at 1 (650) 623-5429.

I was disconnected the first time I tried calling in, but only spent a few seconds on the phone. The second time I called, I was told that I was the next caller in line. There was an option to leave a voicemail, which I didn’t take advantage of.

After about 12 minutes of holding, I opted to reach out via the instant messaging option on the Torpago website. The reply time was advertised to be “under 6 hours.” I left my email address in the chat box (1:21 pm) and went back to what I was doing.

I only ended up waiting 20-30 minutes for the first reply, but I still had more questions — I should have asked everything in one swoop. The user answering my questions was named Brent (I assume it was the founder himself, which leads me to believe the company is still very small).

By the next morning around 10:30 am, all of my questions had been answered.

How to Qualify for a Torpago Corporate Card

If you are ready to try to obtain a Torpago corporate credit account, first look over the qualification terms. First of all, only US registered companies (sole proprietors, LLPs. LLCs, S-Corps, or C-Corps) can apply. So, if your company isn’t organized, you won’t be able to get a credit line.

Next, you need an EIN and business checking account. Your account will be linked to the Torpago platform to verify businesss income. At this point, Torpago wants to see your monthly business income, but they do not publicly state the amount needed to qualify. My assumption is the higher the better… I wouldn’t apply without at least $10K in documented monthly revenue.

Finally, you must not participate in prohibited activities.

- Sale of Schedule-I or Schedule II-V controlled substances without a pharmaceutical license

- Production, sale, or distribution of marijuana, guns, ammunition, or other weapons

- Gambling, betting, lottery, sweepstakes, or games of chance

- MLM, cryptocurrency, counterfeit products, escort services

- Professional services including law and consulting

See the full explanation in the above link if you aren’t sure or your business tends to fall into a gray area. Torpago seems to be designed for tech startups, but many other businesses can still qualify for an account.

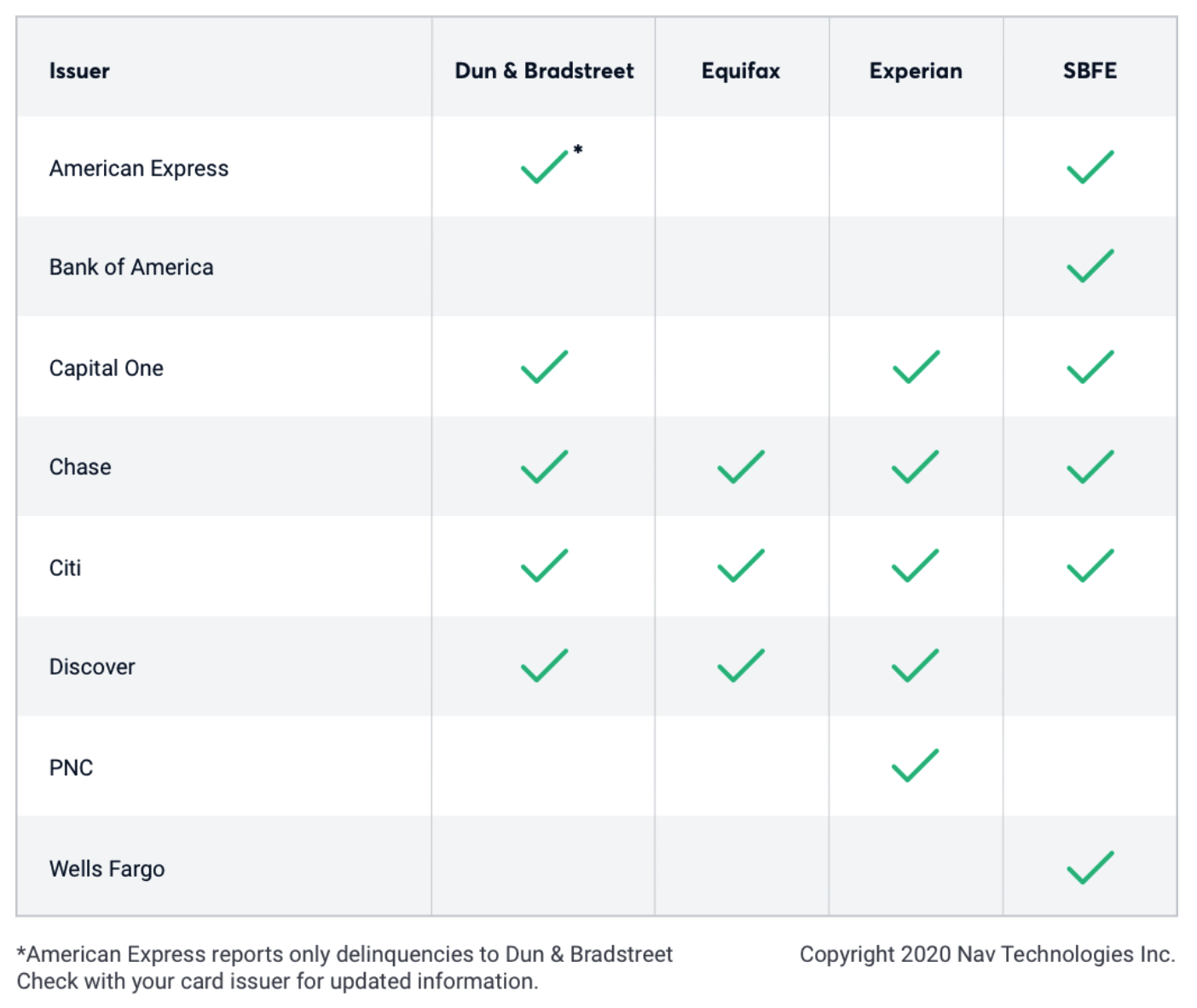

Does Torpago Report to Business Credit Bureaus?

Most of my students and clients want to know if Torpago reports to business credit bureaus like Dun & Bradstreet. The reason this is important is because when on-time payments are reported to credit bureaus, it has a positive effect on a company’s business credit score.

According to Torpago, on-time payments are reported to business credit bureaus. This is good news for anyone looking to build their business credit score.

Recommended: This is How to Build Business Credit Fast [Step-by-Step Guide]

Competitor Overview: Torpago vs Divvy

Both Torpago and Divvy are free corporate lines of credit that require no personal guarantee, a rare offer. And, while they share these commonalities, they aren’t one in the same. Below are the key differences between the two offers.

If you’re interested in one of these credit lines because of the automated expense management, you might look at available integrations. For now, Torpago is the clear winner on this front if you use either Financial Force or Acumatica. However, Divvy currently offers the best rewards by a long shot.

Learn about corporate card offers from Ramp, Amazon, Brex, Stripe, and Divvy.

Final Thoughts

While Divvy has a similar offer with higher rewards, a more established partner base, and a more robust customer service team, Torpago is still a new player and has plenty of time to catch up. While I might not recommend applying for this credit line above other contemporary corporate offers, I wouldn’t rule them out as a legit and convenient option for business cash flow management.

If you want to learn how to obtain $100K in business credit in 30 days, join the Business Credit Workshop today.