Can we talk about the crazy evolution the security industry has gone through recently? When you upgrade your security cameras, it’s like going from an old bicycle with training wheels to a turbocharged motorcycle that can navigate traffic and take you on epic cross-country adventures.

Today, with a new system, you can monitor your facilities from anywhere using your phone or laptop.

Whether you’re rocking a small coffee shop or running a mega-corporation, nailing down the right security cameras is like having your own fortress – it shields your assets, your staff, and your space.

Let’s learn how to pick out the slickest security cams for your business.

Here’s what’s in store:

- Why Do Businesses Need Security Cameras?

- How to Choose the Best Security Cameras

- Top Picks for Business Security Cameras

- Bonus: Secure Camera Installation Tips

- Frequently Asked Questions

- Conclusion

Ready to roll?

Why Do Businesses Need Security Cameras?

Business security is more than just a padlock on the front door.

Security cameras offer several advantages:

- Deter crime – Conspicously-placed cameras and signs deter intruders, thiefs, and vandals from targeting your business.

- Document incidents – Camera footage is valuable evidence for any investigations, insurance claims, and legal proceedings.

- Protect staff – Monitoring the work environment helps ensure employee safety and prompt response to emergencies.

- Monitor remotely – With remote monitoring, you can keep an eye on your operations from anywhere at any time.

What is the difference between home and commercial security cameras?

Home security cameras and commercial security cameras are designed for the specific needs of the end-user.

Home Security Cameras:

- Are tailored for residences and smaller spaces

- Emphasize easy installation and operation

- Include motion detection, night vision, and mobile app access

- Prioritize aesthetics for seamless integration into homes

Commercial Security Cameras:

- Are engineered for businesses and larger areas

- Offer advanced features like customizable motion zones

- Are designed to withstand harsh environments and weather

- Are scalable for businesses of all sizes

- Can integrate with access control and alarm systems

While both types of security systems protect property, they differ in scale, features, durability, and complexity – But, you may be able to use business and consumer systems interchangeably based on need.

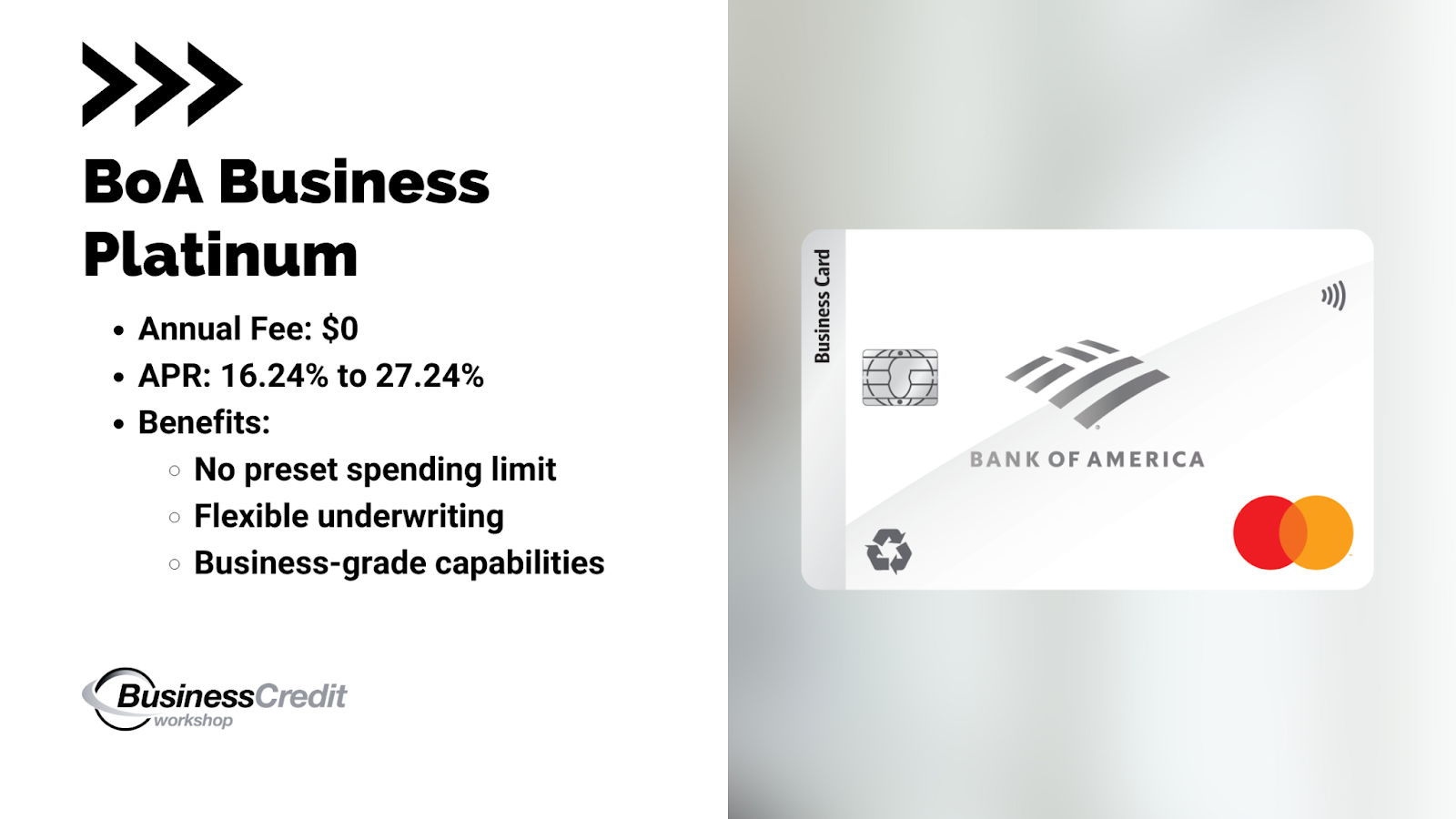

Recommended: How to Use Business Gas Cards to Build Your Business Credit

How to Choose the Best Security Cameras

When it comes to choosing the best security cameras for your business, you’ll want to look at the following features:

- Camera types – Dome cameras, bullet cameras, and PTZ (pan-tilt-zoom) cameras have distinct features and are suited for specific monitoring needs.

- Indoor vs. outdoor cameras – Determine whether you need cameras for indoor or outdoor monitoring, or a combination.

- Resolution and clarity – Opt for cameras with high-resolution (1080p or higher) for clear and detailed image quality.

- Low-light and night vision – If you need to monitor during nighttime hours, look for cameras equipped with good low-light performance and/or infrared night vision.

- Wide-angle coverage – Consider cameras with a wide field of view to cover larger areas with fewer devices.

- Power options – Choose between wired and wireless cameras based on the availability of power sources and your preferred installation method (I upgraded from Google Nest to Arlo, because it seemed like I had to charge the Nest too often).

- Remote access and alerts – Get a system that offers remote access through mobile apps or web browsers, and customizable alert notifications for real-time updates.

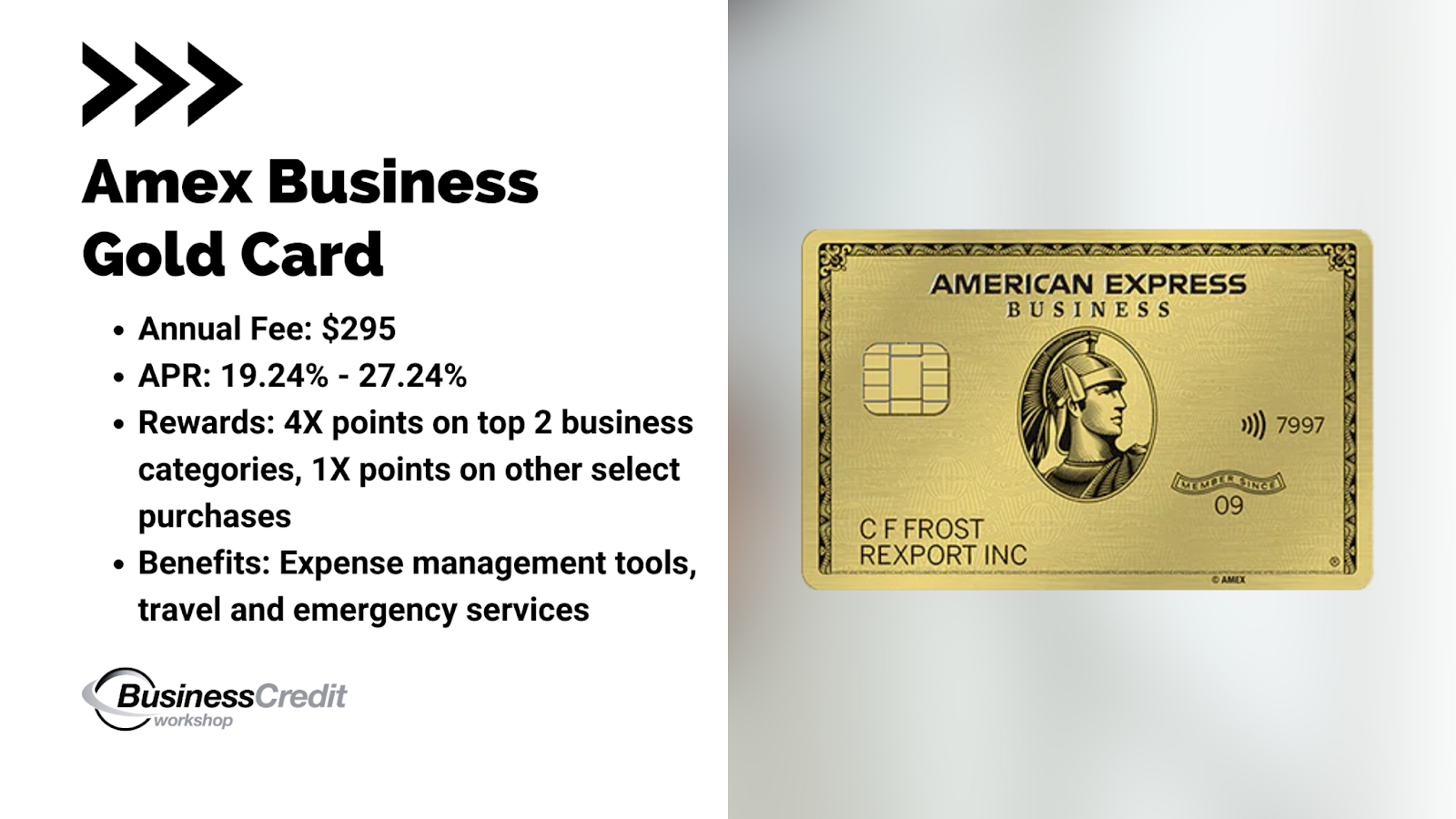

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN

Top Picks for Business Security Cameras

In the quest to beef up my security system, I decided to turn to the good folks over at Reddit for some guidance. With approximately 10 cameras to handle and a need for continuous 24/7 recording that’s easily searchable and downloadable, I wanted some practical advice.

Reddit delivered, and three names kept popping up in the conversation: Arlo, Ring, and Nest (now Google Nest). These brands seemed to offer promising solutions, and I’m about to break down why they stood out.

I used to use Nest, but I felt like I had to charge the cams too often.

Here, I’ll explore why one of these cameras could be just what your business needs. I’ll dig into their cool features, discuss how they fit into a business setup, and give you the lowdown on making the right choice to keep your premises secure.

So, grab a coffee, and let’s chat about Arlo, Nest, and Ring security cameras!

1. Arlo Pro 4 Security Cameras

Arlo Pro 4 cameras are the go-to for convenience. They’re wireless, run on a rechargeable battery (no need for power outlets), and offer crisp 2K resolution. Wide-angle coverage and enhanced night vision keep an eye on things 24/7. You can monitor remotely with the Arlo app, get motion alerts, and even have two-way chats.

Wireless Wonder – If hassle-free installation is your thing, Arlo Pro 4 cameras are a dream. They go wireless, powered by a rechargeable battery, making them perfect for businesses without nearby power outlets. No need to fuss with wires.

Crystal Clear – These cameras come with 2K resolution, which means sharp and detailed footage. Their wide-angle coverage ensures you won’t miss a thing, and even when the sun goes down, enhanced night vision keeps a watchful eye.

Pros:

- Hassle-free wireless installation.

- Crisp 2K resolution.

- Wide-angle coverage.

- No constant power required.

Cons:

- Slightly higher initial cost.

2. Google Nest Cam IQ

Google’s Nest Cam IQ Outdoor is all about premium quality. It rocks a 4K sensor, HDR imaging, and facial recognition tech. Tough enough for the outdoors, it’s got smart motion detection zones. It does need steady power, but the features and reliability make it worth considering.

Top-Tier Video – Google Nest Cam IQ Outdoor is for those who demand the best. It flaunts a 4K sensor and HDR imaging, guaranteeing top-notch video quality. When it comes to recognizing faces, it’s got that covered too.

Built Tough – This camera is designed to take on the great outdoors. Rain or shine, it can handle it. Plus, its advanced motion detection with customizable zones ensures you only get alerts when it matters.

Pros:

- Stunning 4K video.

- Facial recognition.

- Weather-resistant.

- Smart motion detection.

Cons:

- Requires a consistent power supply.

3. Ring Outdoor Security Kit

The Ring Outdoor Security Kit is a powerhouse. It includes indoor/outdoor cameras, doorbell cameras, and a base station. You’ll get real-time alerts, two-way chats, and it plays nice with the Ring app. Each component may have different specs, but together, they create a solid security setup.

All-in-One – The Ring Outdoor Security Kit is like a security buffet. It serves up indoor/outdoor cameras, doorbell cameras, and a base station. It’s a comprehensive solution that covers all the bases.

Pros:

- A complete security kit.

- Indoor/outdoor and doorbell cameras.

- Instant alerts and two-way communication.

- Works smoothly with the Ring app.

Cons:

- Features may vary depending on the component.

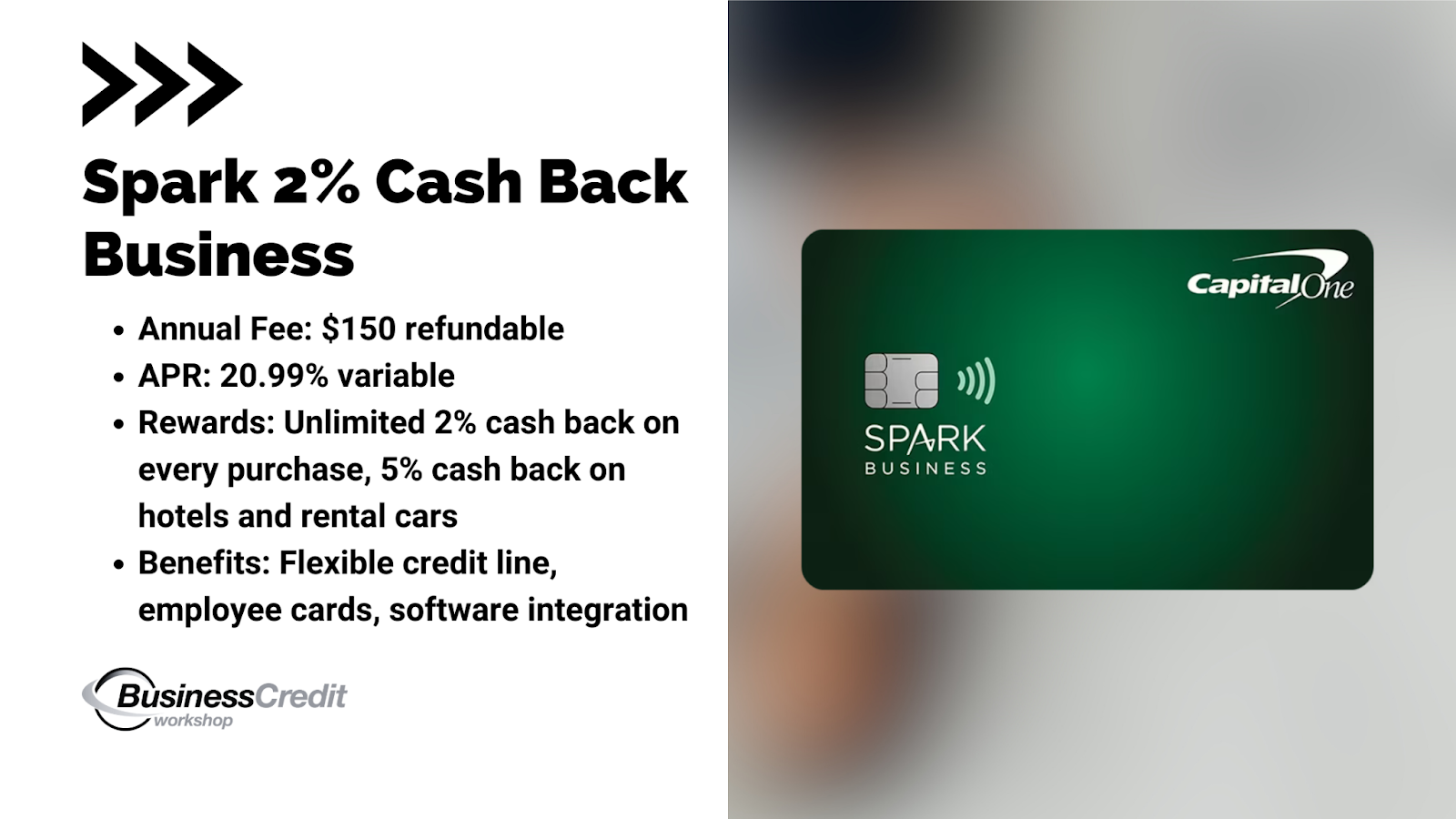

Recommended: 6 Best Business Credit Cards for Entrepreneurs

So, there you have it—three fantastic options, each with its own strengths and quirks. Your choice will depend on what fits your business like a glove. Let’s dive deeper into each option to help you make the right call and keep your business secure around the clock.

Bonus: Secure Camera Installation Tips

When possible, put your cameras on the ceiling. This way, they’re not easy to see, and it’s tough for anyone to mess with them.

If you can’t mount cameras on the ceiling, mount them up high, where people can’t reach them without permission. This keeps them safe from tampering.

Next, hide the wires that connect the cameras. This stops anyone from messing with them or causing problems.

If it makes sense, use protective boxes or enclosures to keep your cameras safe. It’s like putting them in a sturdy, locked box to protect them from any harm.

By following these simple steps, you can make sure your cameras stay safe and do their job without any trouble.

Frequently Asked Questions

What are the best security cameras for a small business?

The best security cameras for small businesses vary based on your specific needs. Options like the Arlo Pro 4, Google Nest Cam IQ Outdoor, and the Ring Outdoor Security Kit offer impressive features, such as wireless installation, high-resolution video, and advanced motion detection. It’s essential to consider factors like indoor/outdoor use, power sources, and remote access before making a decision.

Which security cameras have the best quality?

The Google Nest Cam IQ Outdoor, Arlo Pro 4 are known for their high-quality video and advanced features. Ring is known for its user-friendliness, but offers competitive quality. All of them offer superior image resolution and HDR imaging for awesome video quality.

Which security company has the best outdoor cameras?

Several companies offer top-notch outdoor security cameras. Google Nest, Arlo, and Ring are among the brands known for their quality outdoor camera options, each with its unique features and benefits.

What's the difference between surveillance cameras and security cameras?

The terms “surveillance cameras” and “security cameras” are often used interchangeably, but they can have nuanced differences – Security cameras are designed to monitor specific areas for security purposes, while surveillance cameras can include a broader range of applications, such as traffic monitoring or general observation.

How many security cameras do I need for my business?

The number of security cameras needed depends on the size and layout of your business. Conduct a thorough assessment of your premises, identifying critical areas that require monitoring, such as entrances, exits, and high-traffic zones. Consulting with security professionals can help you determine the optimal camera placement and quantity.

Can you write off security cameras for business?

In most cases, security cameras are considered a legitimate business expense and may be tax-deductible. However, tax regulations vary by location and business specifics. Consult a tax professional or accountant to understand any deductions applicable to your situation.

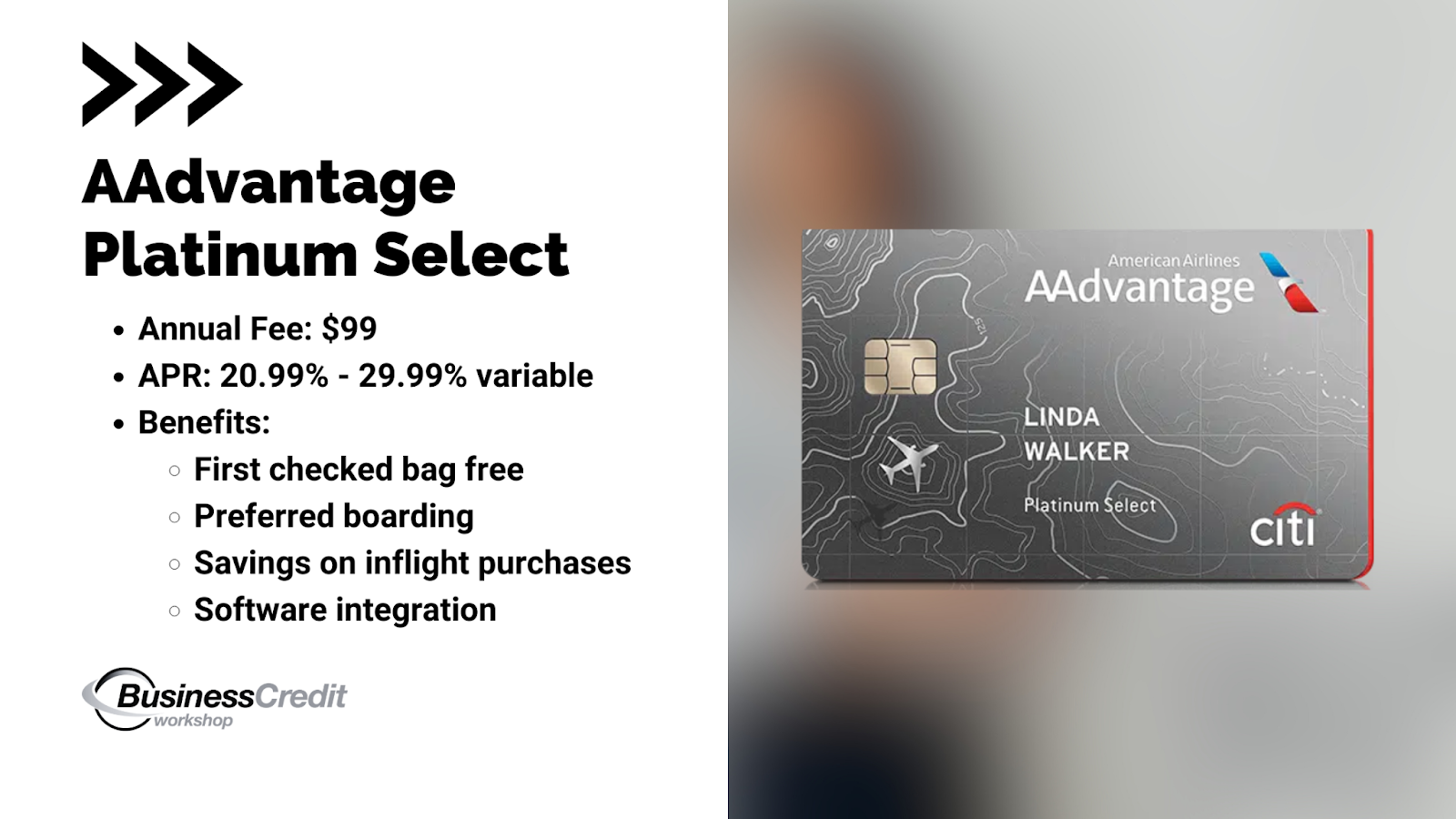

Recommended: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

Conclusion

In the ever-evolving landscape of business security, selecting the right camera system is akin to finding the perfect puzzle piece to complete your safety strategy. Arlo Pro 4, Google Nest Cam IQ Outdoor, and Ring Security Cameras are just a few of the best options available to safeguard your business.

Whether you’re drawn to Arlo’s wireless convenience, Google Nest’s high-tech intelligence, or Ring’s user-friendly approach, each choice represents a powerful tool in your hands. By considering factors such as camera type, resolution, power options, and integration capabilities, you’re setting the stage for comprehensive protection that aligns seamlessly with your business needs.

With the resources to invest in advanced security solutions such as upgraded camera systems, intrusion alarms, fencing, and barriers, you’ll fortify your business against potential threats.

→ Join Business Credit Workshop today to unlock up to $150K in business credit in as few as 30 days and take a confident step towards a safer, more secure business environment.