“How can I pay off $5,000 (or more) in debt fast?”

“How can I raise my credit score 50 points fast?”

“What can I do to get out of credit card debt and take control of my finances?”

If you’re asking these questions, you may have found your way down the rabbit hole to the doors of debt consolidation lenders. One of these doors, naturally, leads to The Payoff™ Loan. So, should you open it?

Here, we’ll look at everything you need to know to decide if Payoff by Happy Money is the right option for you to pay off your debt. This is what’s in store:

Is Payoff™ any good? Read the full review to be 100% certain you’re making the right financial decision before you sign on.

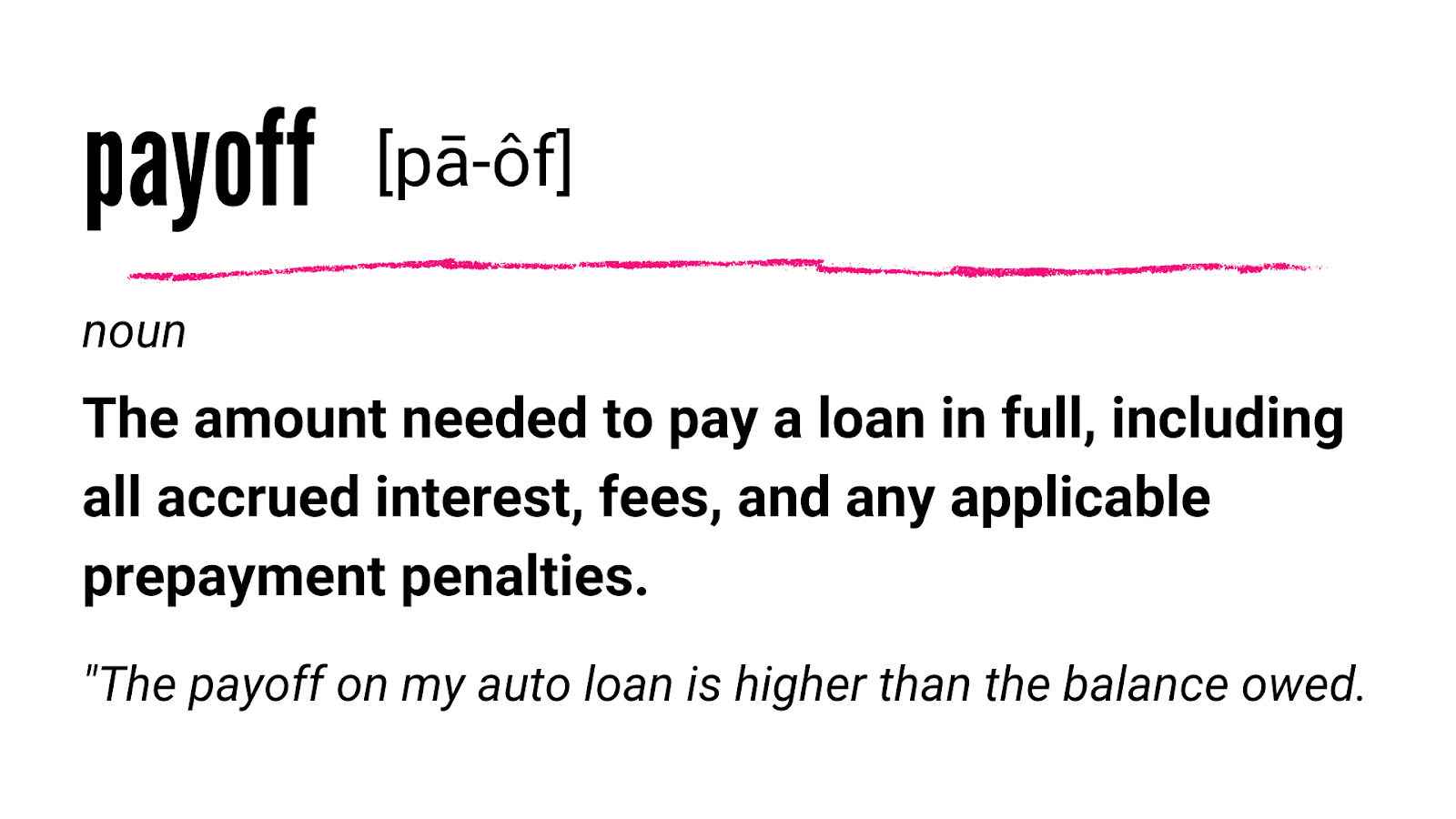

What is Debt Payoff?

The Happy Money brand, Payoff, got their name from the financial term. A debt or loan payoff is the act of paying off the full amount of a debt (in this case, several credit card debts). Keep in mind that the balance owed on a loan or line of credit is not always the same as the payoff amount.

At the end of each payment period, interest is often added to the outstanding balance of a loan. So, typically, the longer it takes to pay a loan off, the more you pay. A payoff ensures that the account is paid in full. You must always carefully read terms and conditions to understand what you will pay over the lifetime of funding.

How Does a Payoff Loan Work?

A payoff loan works by consolidating multiple debts into a single new loan. Once the payoff loan is obtained, other debts will be paid in full and the borrower will then have only one monthly payment. In a good scenario, a payoff loan carries a lower interest rate than the borrower’s original debts, which can mean less money owed in the long term.

If you’re still in a 0% introductory rate on credit cards, it’s not a good idea to obtain a payoff loan to consolidate them because the interest paid will be higher. However, if you can move balances to a new loan with lower rates, this type of funding can be beneficial.

You might also like: Torro Business Funding Review: Is This “Zero Hassle” Offer Legit?

What are the Disadvantages of Debt Consolidation?

Every financial decision you make will come with a unique set of pros and cons. The trick is to make sure the benefits outweigh the drawbacks. So, here’s the quick and dirty on the disadvantages of debt consolidation (Keep in mind, payoff loans/consolidation are not synonymous with debt relief).

- You may not always save money

- Sometimes it accomplishes a mere shift of your debt to a new account

- It has the potential to put you in debt longer than paying off your accounts

- Origination fees can incur upfront costs

The advantages are that you’ll owe one monthly payment instead of a payment for each debt owed. And, ideally, you’ll pay less interest over time.

| Q: Why did my credit score drop when I paid off debt? A: Sometimes paying off revolving debt can temporarily decrease your credit score if the paid-in-full account is closed. This happens when closing an account leads to an increased credit utilization ratio. Lenders prefer a utilization ration of 30% or less. It is always a good idea to pay off debt as soon a possible. Some borrowers opt to leave credit cards open, even after they are paid off. By doing so, their credit utilization ration is not negatively impacted when debt is paid off. |

How to Calculate Debt Payoff

When considering debt consolidation, before exploring your options, you need to fully understand your unique financial situation. A lack of understanding is part of what got you into debt in the first place.

So, before you sign anything, make sure you’re clear on each of your debts. For each credit card, gather the following information:

- What is your total balance owed?

- What is the interest rate on the card?

- What is the minimum monthly payment?

- What is the maximum payment you can afford?

The easiest way to find your answer is to then use a loan payoff calculator. For this, check out CreditKarma (just ignore their ads for new loans and lines of credit). You can use the calculator to determine the total payoff amount (full balance), estimated payoff time, and what you can expect to pay in interest and toward the principal.

Once you have all of this information, shopping for loans, you can determine whether a loan is even right for you. In some cases another debt repayment method like snowballing might be a better fit.

You’ll know if the cost and duration of any loan you might qualify for is higher and longer than what you can make happen on your own that debt consolidation isn’t the smartest move.

What is the Payoff™ Loan?

The Payoff™ Loan is one of many debt consolidation loans in today’s financial marketplace. They have a quick application process and prequalification with a soft pull of your credit. The offer is from Happy Money, a company with a mission to “turn borrowers into savers,” not a traditional lender.

In fact, Payoff is not a lender at all. Instead, they offer loans from partner institutions. Happy Money, Inc. earns a commission from their partner lenders for each loan obtained through their platform(s).

What to Expect When You Apply for a Payoff™ Loan

Checking your rate on the Payoff website will not affect your credit score. However, during the process you will consent to receive phone calls and emails from Payoff. So, even if you don’t follow through with your application or you can’t qualify for any reason, the company will likely contact you in the future, which can get annoying.

So, to be safe, find out whether or not you’re likely to qualify and if you even like the options they might extend. Learn more in the following sections.

- Payoff™ Loan Requirements

- Payoff™ Loan Terms and Fees

- Payoff™ Customer Service

- Frequently Asked Questions

Or, skip ahead: Payoff vs Upstart vs SoFi: Competitor Overview

Payoff™ Loan Requirements

One of the best features of Payoff™ is their transparency. It’s super easy to find anything you need to know about approval on their Getting Approved page. In a nutshell, here’s what you need:

- ≥ 640 FICO score (via Transunion)

- No current delinquencies

- ≤ 50% debt-to-income ratio (See Payoff’s™ Guide to Documents and Verification)

- ≤ 30% credit utilization ratio

Some reviewers have said that you also need an annual income of $40K.

Payoff™ Loan Terms and Fees

First of all, with this offer, you won’t pay for an application, early payoff, late payments, check processing, returned checks or annual fees. But, the loan won’t be free. Instead you can expect origination fees of up to 5% (On a $10K loan, you might expect to pay up to $500) and APR between 5.99% and 24.99%.

Terms for Payoff™ loans range from two to five years. So, that’s how long you’ll have to pay off your loan between $5K and $40K. In New Mexico and Maryland, loans must be at least $5.1 and $6.1K respectively.

Payoff™ Customer Service

Theres something to be said for the power of the customer experience. As humans, we’re often prone to spend more for better service, which doesn’t disclude our financial lives. So, will Payoff’s™ support meet your needs?

Most people seem to love the customer service. They have a live chat feature as well as publicly-displayed contact phone number, email address, and physical location, which indicates that their team is accessible.

Of course, not everyone will have a great experience, for varying reasons. Technical problems, system overload (It seems to me like most lenders has had a rough go with this surrounding the pandemic and PPP), and other problems with customer service exist with all funding providers.

In the case of Payoff, borrowers have cited problems with the website and contacting a representative in the recent past. We can hope that the company will address these issues moving forward.

Frequently Asked Questions

Now, let’s address some of the most common questions that are still unanswered.

- What bank does Payoff™ use? – As of November 2020, Happy Money,™ Payoff’s parent company, currently works with six partner lenders: Alliant, FirstTech Federal Credit Union, Technology Credit Union, Teachers Federal Credit Union, GreenState Credit Union, and First Electronic Bank.

- Does Payoff™ verify income? – Yes, most people will be asked to provide their two most recent paystubs. Self-employed individuals may submit their most recent tax Form 1040.

- Can you pay off a Payoff™ loan early? – Yes, you may. There will be no penalty for early repayment on a Payoff™ loan.

- Can I refinance my Payoff™ loan? – Yes, personal loans can be refinanced.

- How long does it take Payoff™ to review application? – The review process will typically take between three and seven business days.

Payoff vs Upstart vs SoFi: Competitor Overview

At the bottom of the debt consolidation loan rabbit hole, you’ll find an array of options. The closest comparisons to The Payoff™ Loan by Happy Money are Upstart and SoFi’s offers.

Payoff, Upstart, and SoFi have some commonalities:

- Competitive interest rates & fees

- Simple application process

- Cater to borrowers with fair to good credit

- Transparent terms and conditions

Then, they have some key differences. So, let’s look at how these three lenders stack up side-by-side.

Of the three, Upstart caters to borrowers with the lowest (fair) credit scores and SoFi has the largest personal loans, mortgages, and student loan consolidation offers. Payoff is still in the game with a decent offer for credit card debt with high or predatory interest rates.

Final Takeaway

Is The Payoff™ Loan a good idea? If you need a loan of less than $5K or more than $40K, your personal credit score is lower than 640, or you need money to pay off more than just credit cards, you should look elsewhere for financing. Otherwise, this credit card debt consolidation offer is legit. So, there’s no harm in checking your rate to find out what you might qualify for.

If you’re interested in learning how to obtain up to $100K in business credit in as few as 30 days, start here.