When you’re in a pinch or you want to scale your business operations, you might turn to online lenders for working capital. Fundbox loans (which are actually revolving lines of credit) are a popular option right now. You may even be considering applying with the company. Before you do, read this.

Here, you’ll learn everything you need to know before you make a critical business financial decision. This is what we’ll cover:

- What is Fundbox?

- Fundbox Line of Credit Requirements

- Does Fundbox Report to Credit Bureaus?

- Final Takeaway

Now, let’s get to it!

What is Fundbox?

In a nutshell, Fundbox is a fintech company that extends working capital in the form of revolving credit lines to companies that make at least $50K per year.

Frequently Asked Questions:

Where is Fundbox located?

Fundbox is headquartered in San Fransisco, California.

Who owns Fundbox?

Eyal Shinar is Fundbox’s founder and executive chairman, previously CEO.

How big is Fundbox?

According to Crunchbase, Fundbox currently has 17 team members, 25 investors, and $453.5 million in funding as of September 2020.

Where does Fundbox funding come from?

Lines of credit and loans are made directly by Fundbox and by First Electronic Bank.

How much is Fundbox worth?

Fundbox valuation was estimated at $750 million in 2020, according to Forbes.

How Does Fundbox Work?

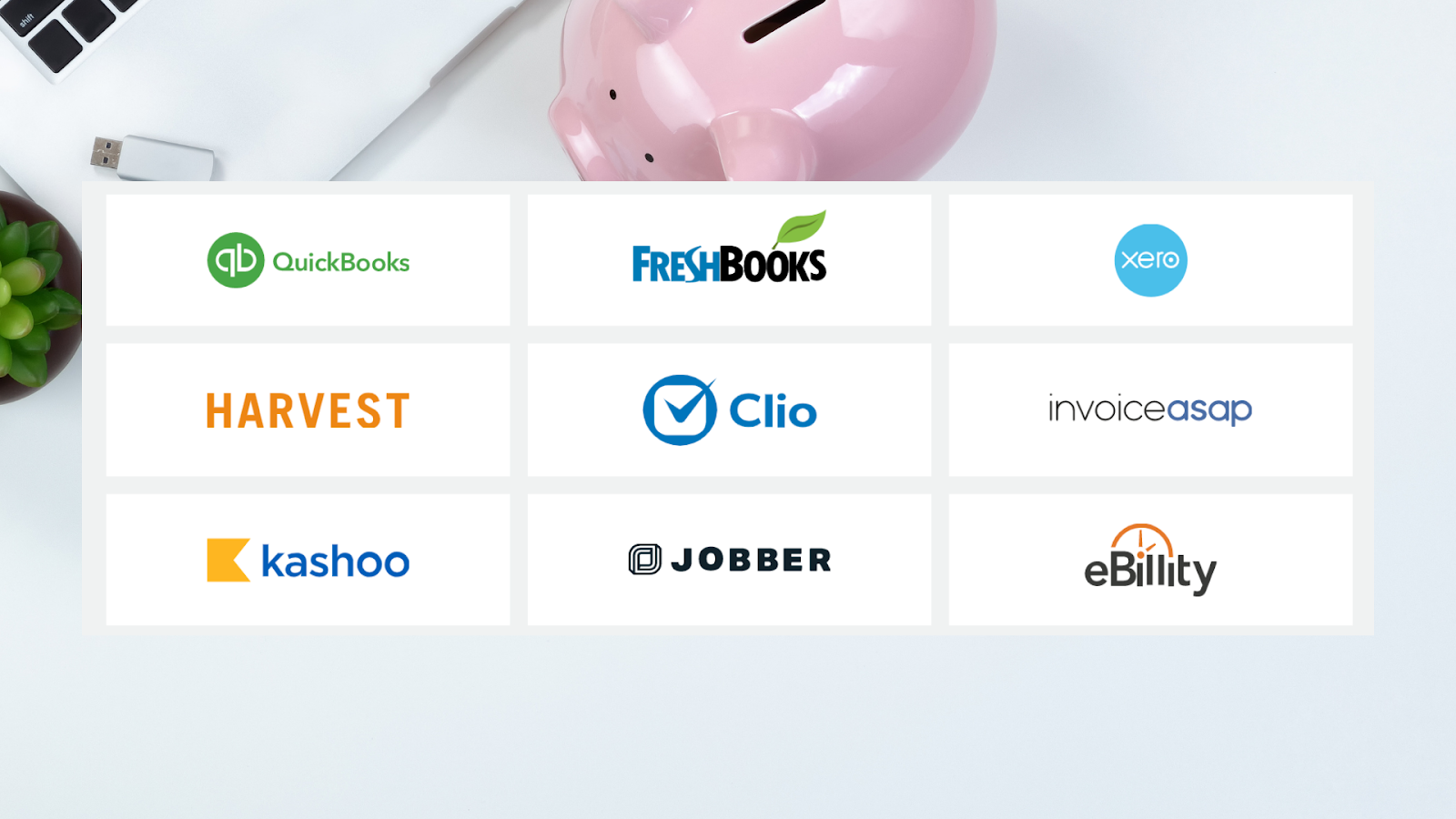

Fundbox uses predictive modeling to help small businesses and freelancers optimize their cash flow. Essentially, a company connects Fundbox to its accounting or invoicing platform and business bank account to prove cash flow. The system analyzes accounts, which takes a few minutes. After that, the business is automatically approved or denied access to funding through the platform.

While the database of supported online banking software is massive, not all banks are accessible through the platform. So, some users who do their business banking at very small community banks or credit unions may not have access to Fundbox’s financial services for this reason alone.

Furthermore, only business bank accounts qualify. So, freelancers or contractors who use a personal checking account for both personal and business use will be unable to use the service (yet another reason why you must have a business checking account).

Once you’re set up in the platform, you may qualify for business credit. Learn more about each offer below.

You might also like: Torro Business Funding Review: Is This “Zero Hassle” Offer Legit?

1. Fundbox Credit

After your account is set up, you may get an offer for a revolving credit line in hours or minutes. You can then draw funds directly from your Fundbox dashboard to your business checking account for a maximum of $50K on your first draw. These funds must then be repaid weekly within the set repayment period.

Repayment periods on Fundbox credit might be 12-24 weeks. And, if you repay early, you will save on interest, which starts at 4.66% for a 12-week plan and goes up from there. And, “revolving” means that once your funds are replenished, you can draw from your limit repeatedly.

Periodic account reviews may increase or decrease your funding limit and/or interest rate over time.

2. (Previously) Fundbox Pay Net Terms

Typically, net 30 vendors that report to business credit bureaus are one of the first stops when establishing business credit. With Fundbox Pay, businesses could apply to send or accept payments for products and services with net terms.

Vendors who wanted to accept payments with net terms could apply as a merchant on the platform. Or, buyers could invite their vendors to the platform for the ability to buy now and pay later. It was a convenient funding option for businesses who were temporarily tight on cash.

Unfortunately, as of about a month ago, Fundbox no longer offers a net terms product.

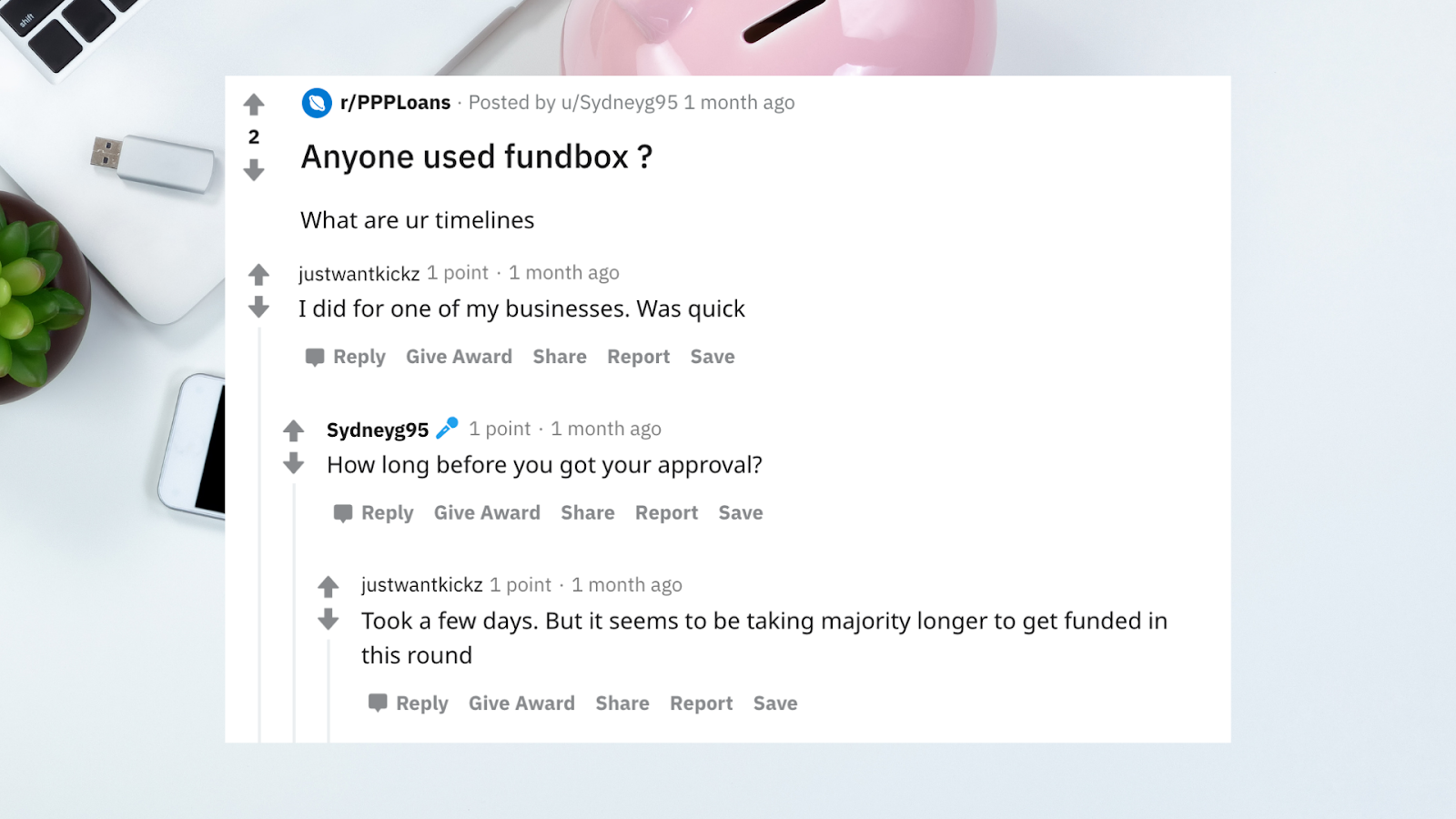

3. (Previously) PPP Loans

While the application period for PPP loans, as outlined in the 2020 US stimulus, has passed, we should still acknowledge this offer. The reason it’s important to note is that if there is another round of similar financial offers in the future, Fundbox could be a potential funding source.

Fundbox PPP loan reviews are pretty much unanimously positive. The only complaint that applicants seemed to have was that the process took awhile. But, while these applicants waited from a couple of weeks to a month for approval, we’ve all heard of others who waited even longer.

Fundbox Line of Credit Requirements

As stated above, Fundbox borrowers must have a business checking account. In addition, the platform has other (relatively relaxed) requirements. If you have at least three months of business checking transactions that show activity that proves around $50K or more in annual revenue, a soft pull to your credit report that shows a minimum 500 personal credit score can qualify you.

In some cases, the platform may conduct a one-time hard pull. And, at least two months of history in a compatible accounting software might allow you to bypass the three-month banking history condition. But, if you connect the platform to a personal bank account, you will not be approved.

Personal Guarantee Requirements

These loans/credit lines do not require a personal guarantee. So, if your business defaults, you will not be held personally responsible. However, the proprietary algorithm that makes funding approval decisions makes it unlikely that this will happen — only companies who show the likelihood of repaying the loan will be approved.

Prohibited Businesses

If you’re in a questionable line of business, you already know that some major platforms might reject you. And, that could be the case with Fundbox as well.

Businesses in the following industries are prohibited:

- Adult services and entertainment

- Weapons and firearms

- Gambling and online gaming

- Drugs, dispensaries, and paraphernalia

- Money service businesses

- Not-for-profit organizations

Unfortunately, if your business falls under one of these umbrellas, you’ll need to look elsewhere for capital.

Does Fundbox Report to Credit Bureaus?

Business owners who receive funding might want to know if Fundbox reports to major credit bureaus. This is important because loans that are not reported will not have a positive impact on your business credit score.

Unfortunately, at this time, Fundbox does not report to D&B or any other business credit bureaus. So, any payments you make toward funding will not have an impact on your business credit.

Final Takeaway

So, yes, Fundbox loans and lines of credit are completely legit. The proprietary software can help businesses access working capital fast without too many hoops to jump through. But, there are some limitations that might lead business owners in another direction. If you’re interested in learning how to get $100K in business lines of credit in 30 days, sign up for Business Credit Workshop.