PayPal LoanBuilder is advertised as a quick, convenient way to get up to $100K in business funding. The company is more than reputable, and their marketing makes it sound like the easiest financing option in the world. But, what are the terms, how much does it cost, and is this really the best loan for your business?

Let’s find out what LoanBuilder is, how it works, and explore exactly what you can expect if you apply.

This is what’s in store:

- What is PayPal LoanBuilder?

- How Does PayPal LoanBuilder Loan Work?

- Frequently Asked Questions

- Final Thoughts

Now, let’s get to it!

What is PayPal LoanBuilder?

PayPal’s LoanBuilder is a service that offers fixed-term small business loans from $5,000 to $100,000 for first-time borrowers and up to $150,000 for repeat borrowers—the financing option is designed to be fast and flexible, with funds potentially available in your business bank account as soon as the next business day after approval.

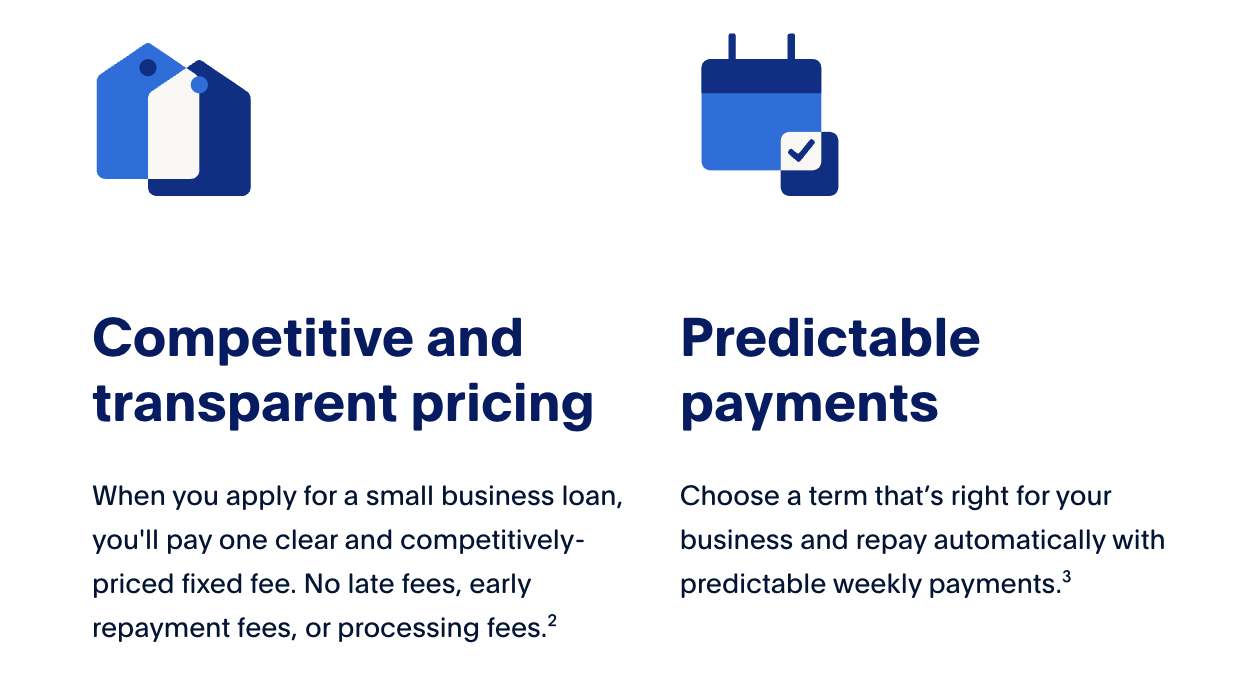

The loan comes with transparent pricing, where you pay a clear, fixed fee along with a $20 Returned Item Fee if a payment is returned. There are no late fees, early repayment fees, or processing fees. You can choose a repayment term that suits your business needs, and payments are automatically deducted weekly.

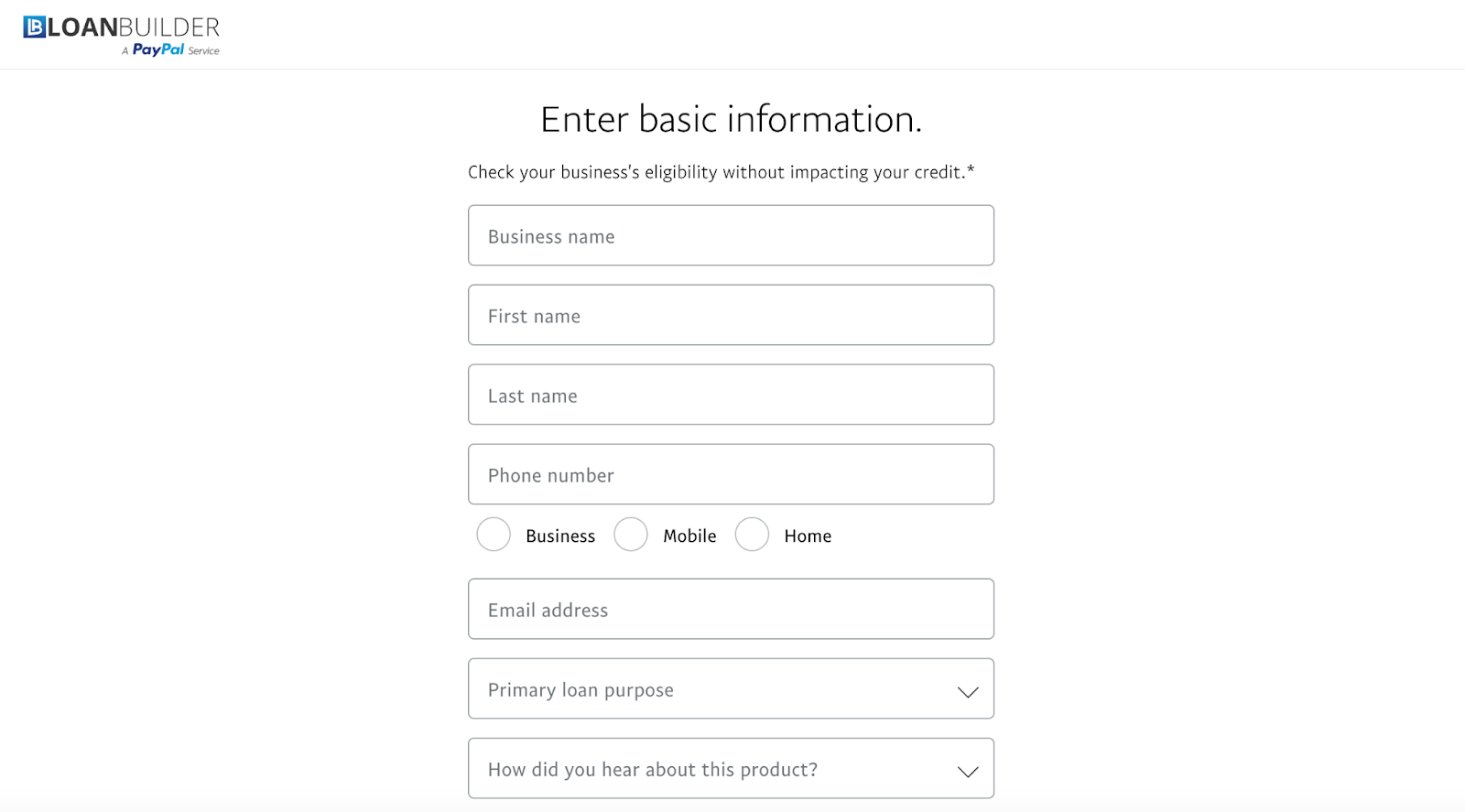

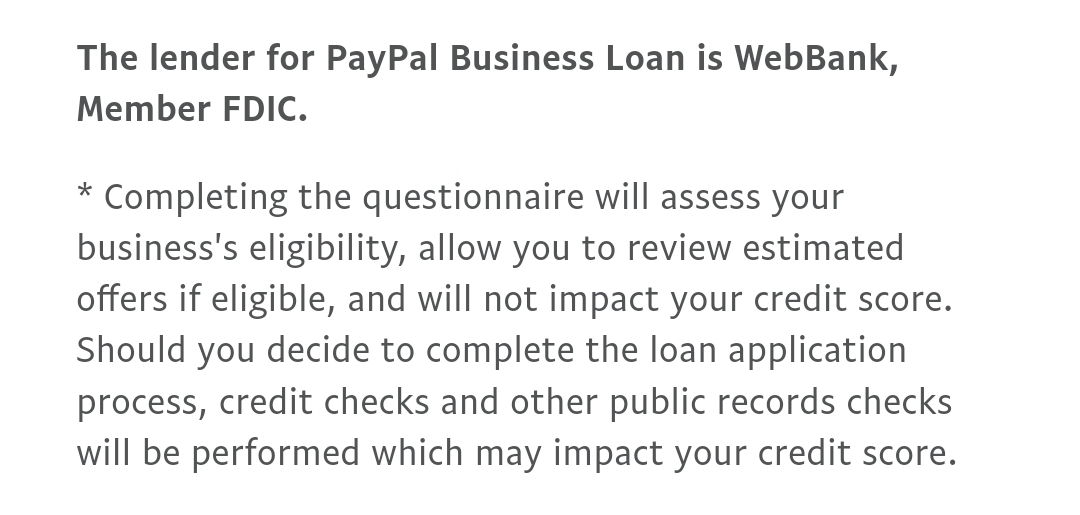

To check if your business is eligible for a LoanBuilder Loan, you can complete a quick online questionnaire. This process won’t impact your personal credit score. If eligible and approved, you can customize your loan amount and term, sign the contract electronically, and receive the funds quickly.

To qualify, your business needs to have been operational for at least nine months with an annual revenue of at least $33,300. Keep in mind that LoanBuilder is a service provided by PayPal in partnership with WebBank. The loan application and approval process is designed to be straightforward and streamlined, aimed at helping businesses manage cash flow, finance projects, or tackle other business challenges.

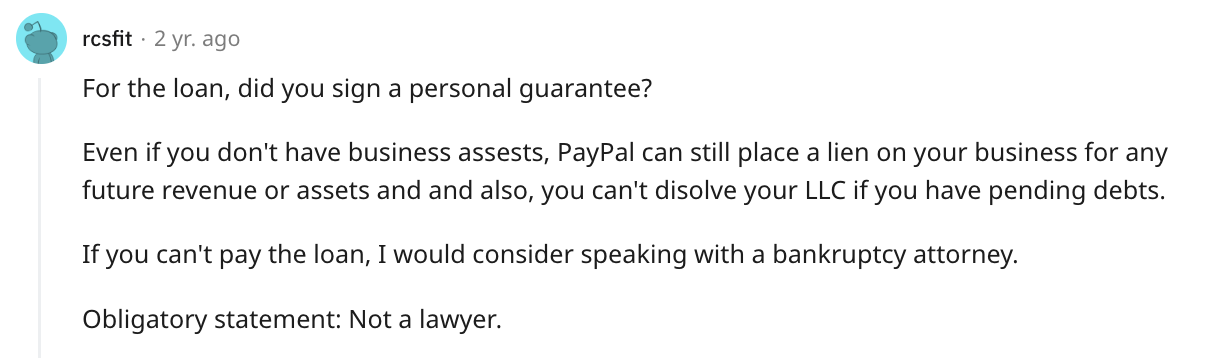

A LoanBuilder loan does require a personal guarantee.

You might also like: Business Credit Cards without Personal Guarantee

How Much Does PayPal LoanBuilder Cost?

The cost of a LoanBuilder loan is determined by a single fixed fee known as the Total Loan Fee, which will be disclosed at the time of loan approval and remains consistent throughout the loan term.

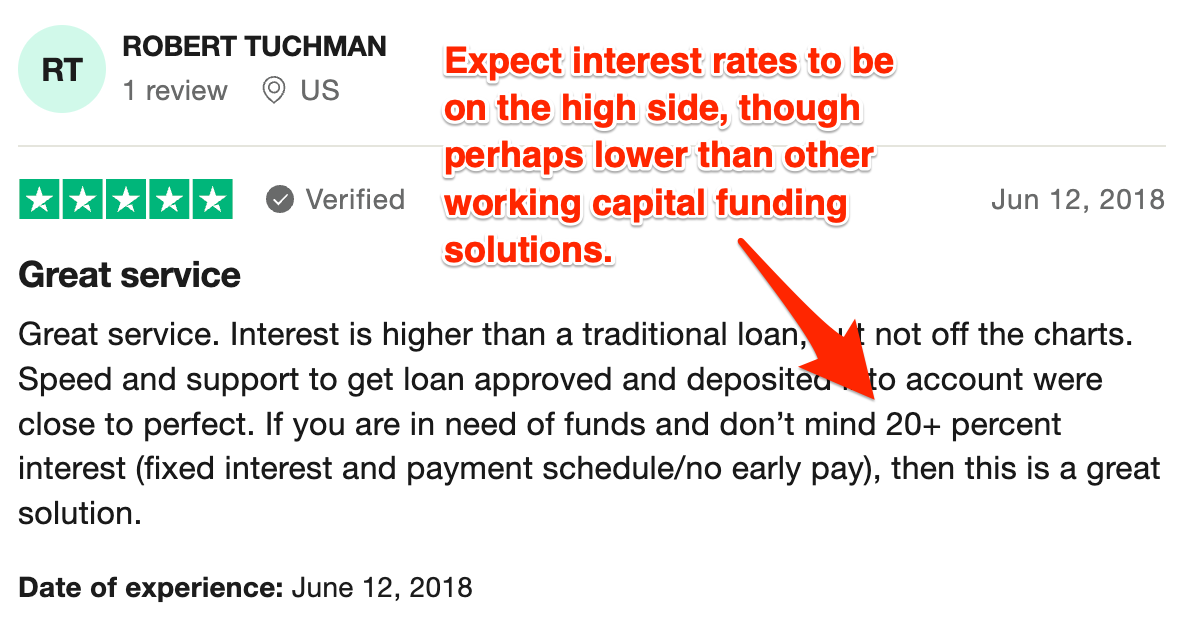

However, since this is a working capital-style loan, you should expect interest rates higher than you would get via, say, your business credit union. Still, they may be lower than other working capital solutions.

The specific amount of the Total Loan Fee varies based on:

- The loan amount

- Repayment term

- Financial risk

LoanBuilder Loans do not have additional fees such as late fees, early repayment fees, or processing fees—The Total Loan Fee is the primary cost associated with borrowing and is included in your repayment schedule.

To see your LoanBuilder cost, you’ll need to complete the loan application process and review the personalized terms.

Recommended: 3 Best Credit Unions for Small Business Banking

How Does PayPal LoanBuilder Loan Work?

LoanBuilder from PayPal offers a pretty simple approach to business financing, providing you with a customizable loan experience tailored to your business needs.

With LoanBuilder, you have the freedom to:

- Access funds quickly

- Repay with clarity

- Benefit from straightforward terms

Let’s delve into the key features that will help you decide if LoanBuilder is the best choice for your business funding.

You might also like: A Deep-Dive National Funding Review: Should You Accept an Offer?

1. Apply With No Impact to Your Credit

The PayPal LoanBuilder “application” is pretty straightforward. The questionnaire asks you for contact information, how you plan to use the funds, how you heard about the loan, business location, and business details.

Details to have on-hand about your business include:

- Legal business name & DBA (if applicable)

- Business address & website address

- Entity type & state of incorporation

- Annual revenue

- Business start date

- Number of employees

- Industry & sub-industry

- Percentage of ownership

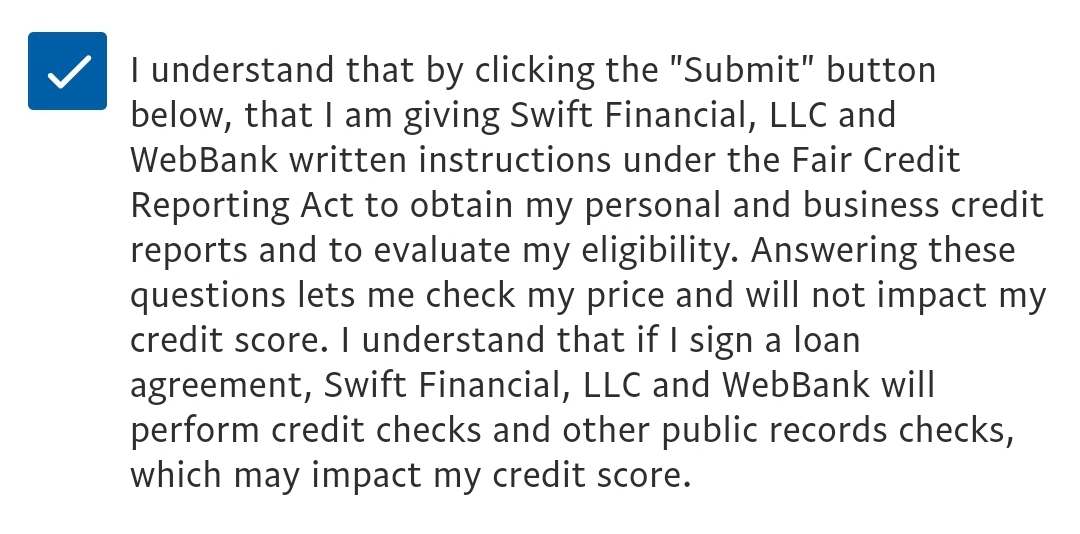

The application also asks for your Social Security Number and Employer Identification Number. Luckily, they do a soft inquiry into your personal credit for pre approval, which won’t negatively impact your credit score.

However, you will probably have to approve a hard pull for final approval.

Don’t move forward with that until you’re absolutely sure you want this loan.

You might also like: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

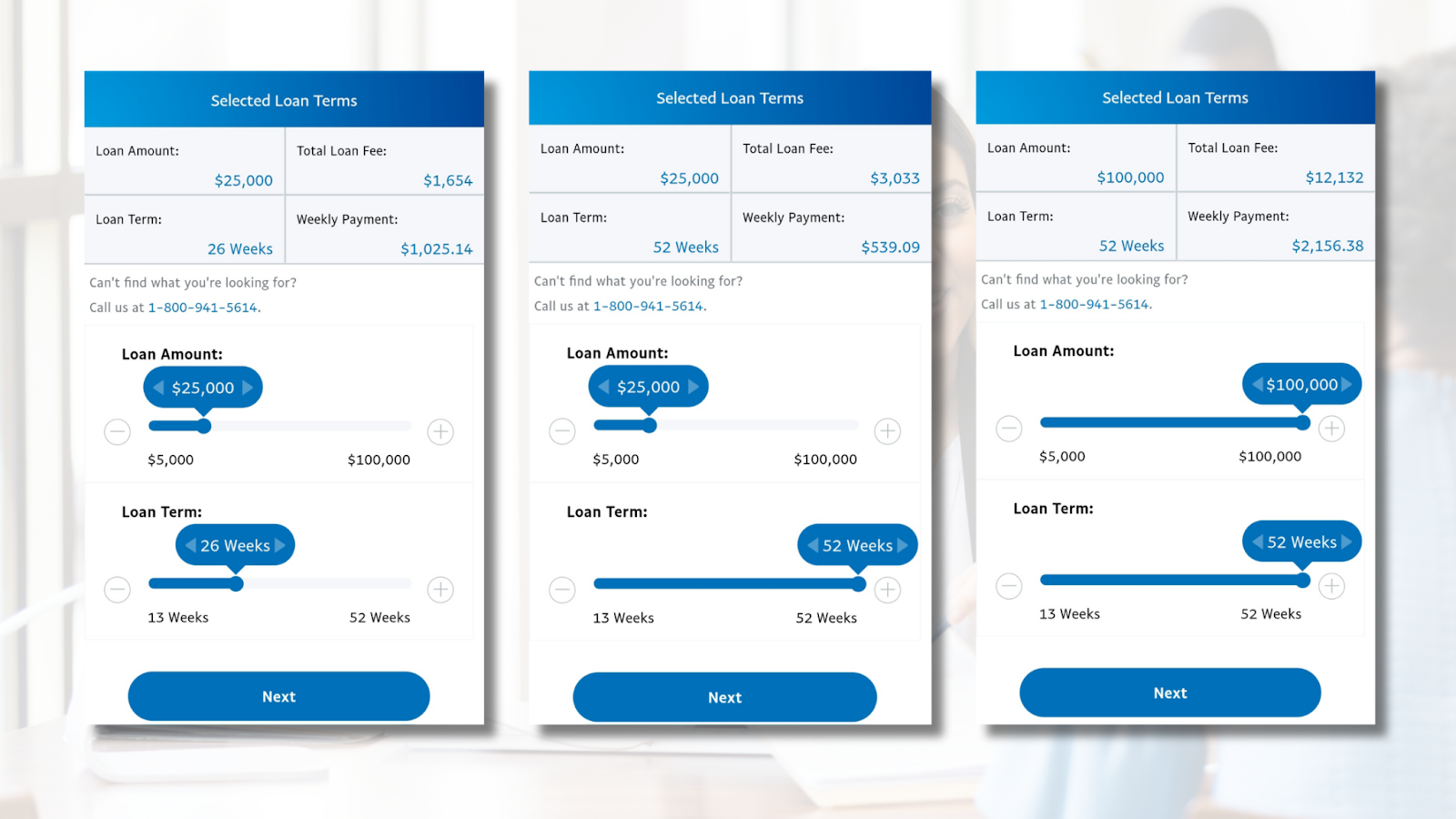

2. “Customizable” Funding

LoanBuilder advertises a “customizable” loan—This makes it sound as if you might get to choose your amount, terms, and rate, which would be pretty exciting.

However, that’s not a realistic way to think about lending; lenders need to assess the financial risk before approving any type of financing.

Still, after you’re pre-approved for a loan, you can choose your loan amount and repayment term. Your loan fee percentage will increase as your terms are extended. So, the longer you give yourself to pay off the loan, the higher your Total Loan Fee.

If you do opt for this loan, consider giving yourself some extra time to pay it just in case something unexpected occurs, as you could be charged penalties for failing to pay on-time.

3. Fixed-Fee Loan

When you take out a LoanBuilder Loan, you won’t have any upfront fees deducted from the loan amount you receive. Instead, the cost of borrowing—the single fixed fee, known as the “Total Loan Fee”—is spread out and paid gradually over the entire duration (life) of the loan.

Here’s a breakdown of what this means:

- When you receive the loan amount, the full sum is deposited into your business bank account without any immediate deductions for fees or charges. This ensures that you have access to the entire loan amount upfront to use for your business needs.

- The cost associated with borrowing the money is represented by a single fixed fee—This fee is agreed upon and disclosed at the time of loan approval; it does not change over the course of the loan.

- Rather than paying a fee upfront or separately, it is integrated into your loan repayment schedule. Each time you make a repayment towards your loan (typically on a weekly basis), a portion of that payment goes towards covering the Total Loan Fee. This fee is gradually paid down along with the principal amount of the loan.

By structuring the loan this way, you get clarity on the total cost of borrowing from the outset, and you can plan your repayments knowing how much will be allocated towards the loan principal and how much towards the fixed fee.

4. Fast Access to Funds

The LoanBuilder lending process is designed to be fast…

First, when you check your eligibility, it’s done through a quick online questionnaire. This initial eligibility check does not involve a hard inquiry on your personal credit report, which means it won’t affect your consumer credit score—This is helpful because you can explore loan options without worrying about potential negative impacts on your credit rating.

If your LoanBuilder Loan application is approved, the funds are transferred directly to your business bank account, often by the next business day after approval—This rapid transfer ensures that you can access the funds quickly to address business needs or capitalize on opportunities right away.

5. Accessible Business Funding

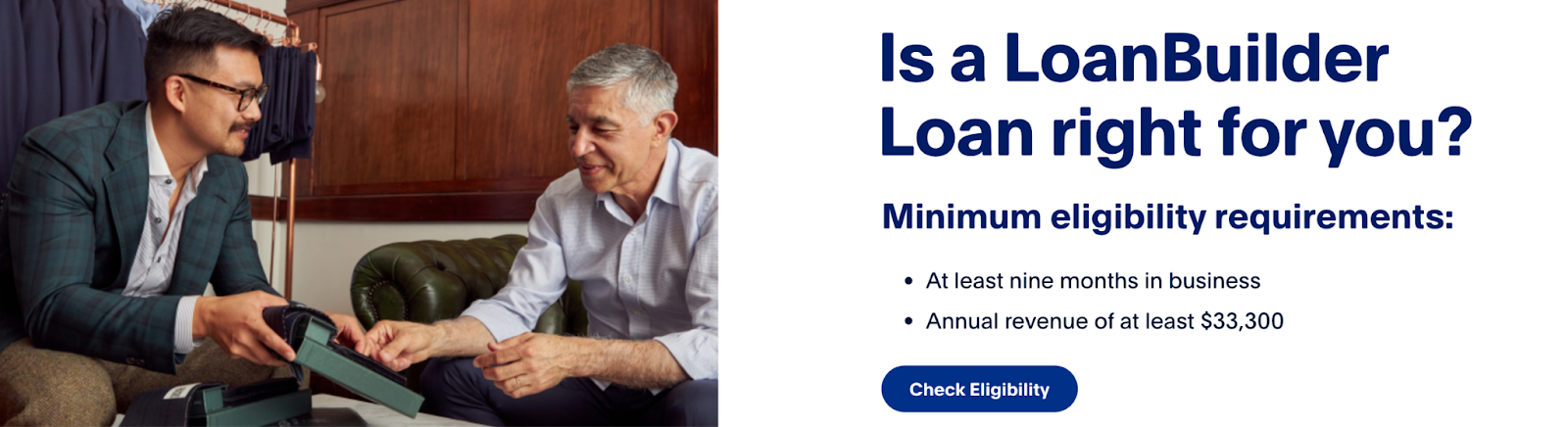

The eligibility requirements for a LoanBuilder Loan can be considered relatively low compared to some traditional business loans:

- At least nine months in business

- $33.3K annual revenue

Requiring a minimum of nine months in business is relatively short compared to other types of business loans that might need several years in operation. Newer businesses can access financing sooner in their development stages.

While this amount varies depending on the size and industry of your business, $33,300 annual revenue is a moderate threshold—It’s achievable for many small businesses, including startups and those in their early stages of growth.

These requirements are inclusive and accessible to a wide range of small businesses, including startups and those with modest revenue streams.

You might also like: Y Combinator: Fast Track to Success or Waste of Time?

6. Weekly Repayment Terms Up to 12 Months

The repayment period for LoanBuilder Loans ranges from 17 weeks (approximately 4 months) to 52 weeks (approximately 12 months), depending on your eligibility and the loan amount you qualify for.

During the repayment period, you will make weekly payments towards your loan balance.

The amount of each weekly repayment will be set based on:

- The total loan amount

- The fixed fee associated with the loan

- The chosen repayment term

The weekly repayment amount remains consistent throughout the repayment period, providing predictability in your loan payments.

For example, if you have a loan with a 26-week repayment term, you will make 26 weekly payments until the loan is fully repaid. The amount of each weekly repayment is calculated to cover both the principal loan amount and the fixed fee—this helps you make sure the loan is paid off by the end of the chosen repayment term.

Frequently Asked Questions

Is PayPal legally a bank?

No, PayPal is not a bank. It is a technology company that provides online payment services and financial solutions.

What bank does PayPal use for loans?

LoanBuilder loans are provided by WebBank®, Member FDIC, in partnership with PayPal.

What is the minimum credit score for LoanBuilder?

LoanBuilder does not disclose a specific minimum credit score requirement. Instead, eligibility is determined based on various business factors such as revenue and operational history—but the do require a personal guarantee

Does PayPal LoanBuilder report to credit bureaus?

Yes, PayPal LoanBuilder reports payment activity to business credit bureaus, not personal credit bureaus. This can help businesses establish and build their business credit profile.

Final Thoughts

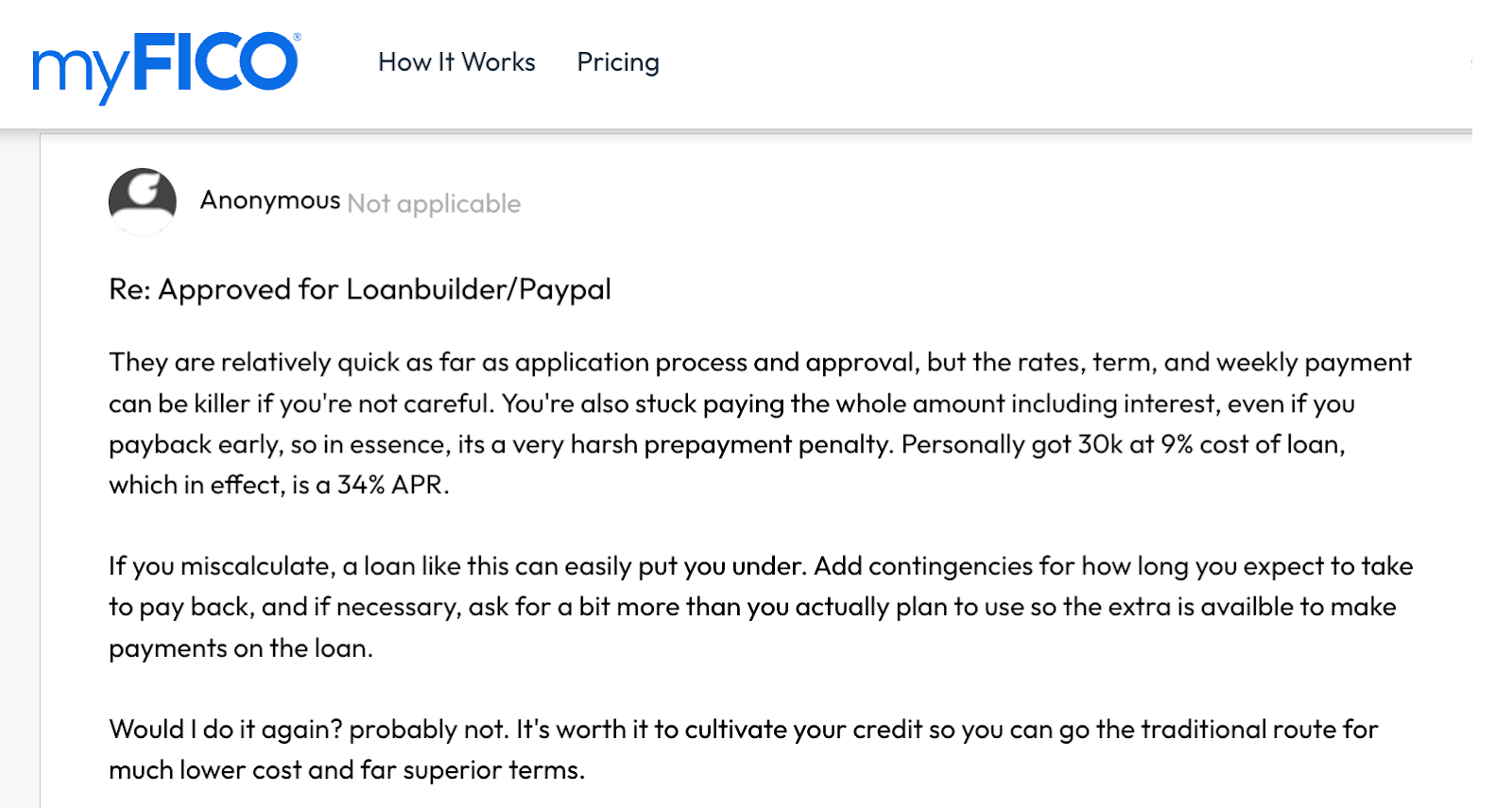

PayPal is a trustworthy financial company, with LoanBuilder being backed by a reputable bank. The loans they offer are pretty competitive in the working capital realm, but the high rates are a red flag for me. I never recommend my students take out a loan like this unless there is absolutely no better option—even with a flat fee, weekly repayments can eat at your profits.

But, if you need to take out a high-interest loan and you’ve explored all of your options, this might be the way to go. If you have some time, I recommend you put some effort into your business credit so you can get loans and lines of credit with (much) better terms…it’s a game changer.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!