If you’re here, your credit profile might leave something to be desired. So, you’re presumably looking for a way to boost your score. Maybe you want to buy a house or obtain financing for another major purchase in the near future. Or, maybe you own a company, and you need to build out your credit profile to obtain business credit.

Either way, Credit Strong’s name is floating around in your world, and you’re kicking the tires because you want to know if their offer is legit and helpful (or if it’s just another new gimmick). Here, you’ll find out about both their personal and business credit builder offers.

This is everything I know about Credit Strong’s big-picture offer — which includes more than typical credit builder loans — so that you can find out if signing up is in your best interest.

Here’s what we’ll look at:

- What is a Credit Strong Account?

- Credit Strong Terms & Fees

- Credit Strong Account Requirements

- Frequently Asked Questions

- Credit Strong Company Overview

- Credit Strong Competitors

- More Answers to Related Questions

- Conclusion: Is Credit Strong Legitimate?

Now, let’s get the show on the road.

What is a Credit Strong Account?

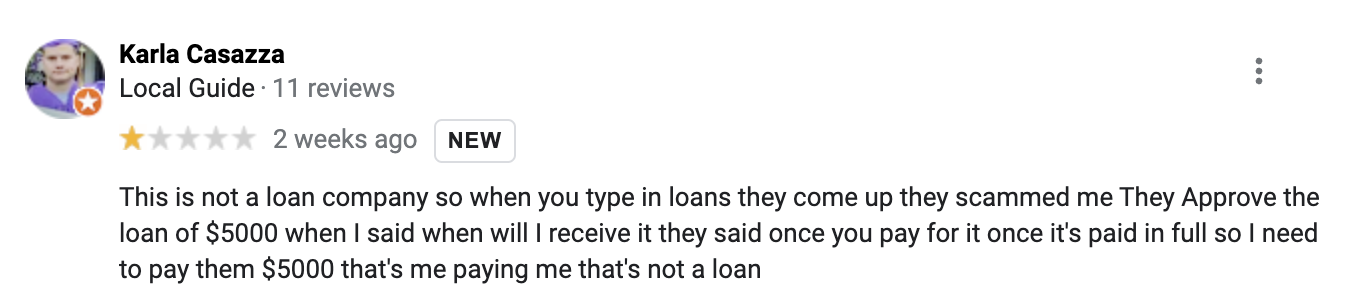

According to the company website a Credit Strong account is “the first fusion” of savings at an FDIC-insured bank and credit building. In my opinion, this isn’t a super clear value proposition. And, after reading user reviews, I think some account holders who have unsuccessfully tried to leverage the offer would agree. So, what does the company mean when they say “first fusion?”

Some users say that the offer appeared in search results when seeking out a loan — it’s crucial to understand that Credit Strong’s credit builder offer is not a traditional loan. So, the generally-expected financing terms don’t apply.

In a nutshell, Credit Strong provides a way to simultaneously build credit and fund a savings account with four secured-type financial product options:

- Revolv. – Add $500 to $1K revolving credit line to your credit profile without a credit card. Send “payments” to a savings account and get them reported to all three major consumer credit bureaus. Withdraw funds when your account is mature or after you cancel.

Cost: $99 per year, plus monthly account payments

- Instal. – Add a $1K or $2.5K installment account to your credit profile. Send “payments” to a savings account and get them reported to all three major consumer credit bureaus. Withdraw funds when your account is mature or after you cancel.

Cost: $15 or $30 per month, plus monthly account payments.

- Magnum – Add a $5K or $10K installment account to your credit profile. Send “payments” to a savings account and get them reported to all three major consumer credit bureaus. Withdraw funds when your account is mature or after you cancel. This plan can be leveraged by small business owners, with no EIN, who want to establish a larger credit line.

Cost: $55 or $110 per month, plus account payments

- Business – Build $2.5K, $5K, or $10K of commercial credit. Send “payments” to a savings account and get them reported to all three major consumer credit bureaus. Withdraw funds when your account is mature or after you cancel. You’ll need an EIN to open a business account.

Cost: $149 to $749 account setup fee, and $100 to $440 per month

Note: The business offer is not easily found on Credit Strong’s website main navigation — You can find more information here.

How Does Credit Strong Work?

Credit strong accounts establish a credit line on your consumer credit profile without a loan or credit card. When you make monthly payments on time, they are reported as “pays as agreed,” to the credit bureaus. In the meantime, those payments go into an escrow account that you may withdraw from later — this offer gives you a chance to save money while building your credit.

Funds saved in a Credit Strong account may be withdrawn if you choose to cancel your account. But, if you withdraw before the end of the amortization period (10 years on standard personal installment accounts), you will still have to pay the interest owed.

This is standard with most credit builder financial offers and Credit Strong is transparent about amortization schedules.

Credit Strong Terms & Fees

Here’s a breakdown of the fee structure for Credit Strong’s personal and business accounts.

Personal Terms & Fees

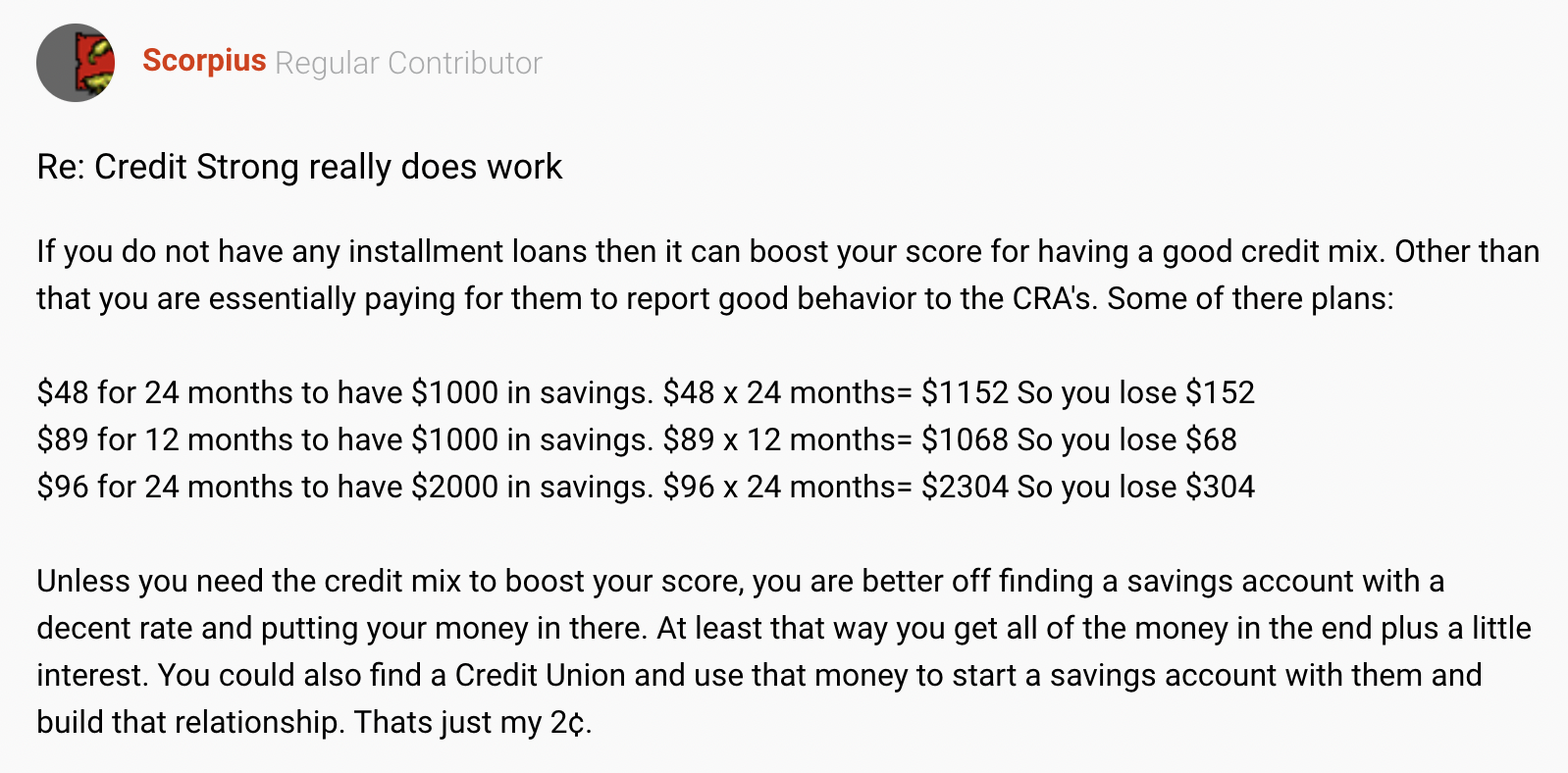

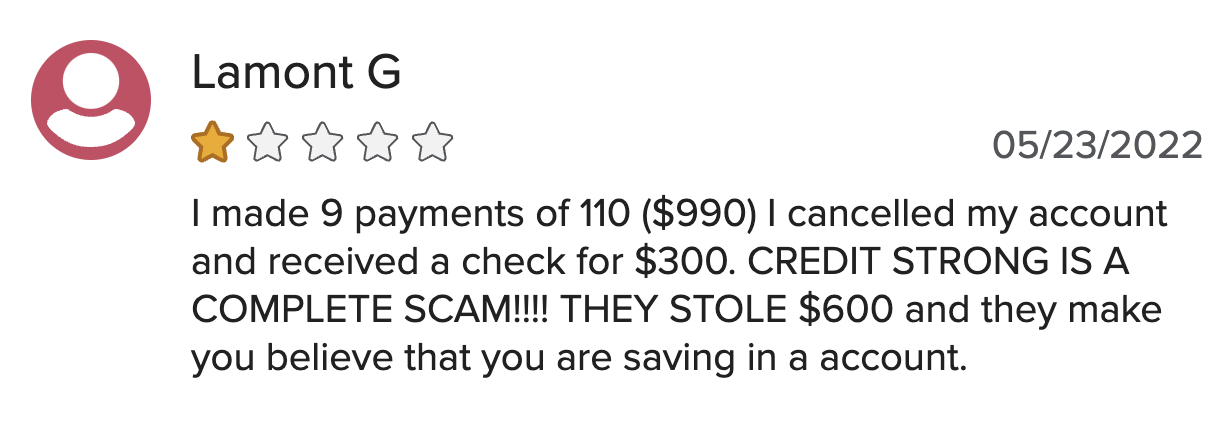

Credit Strong’s personal account cost structure seems to be unpopular with many users who have canceled their accounts.

These unsatisfied users tend to expect traditional loans or traditional savings offers. But, what they’re actually getting is something different: a distinctive “credit-builder” offer with an escrow account. Many credit builder loans and secured credit cards come with high fees, as with most products and services designed for individuals with poor credit.

Here’s a breakdown of terms & fees for personal Credit Strong accounts:

If you have a difficult time saving money on your own and need to diversify the type of accounts on your credit profile to boost your score, a credit builder option like this can help. Expectedly, you will be charged for the service.

After looking at the offer from a bird’s eye view, an Instal. account doesn’t seem like a good idea to me, simply because the standard loan term is 10 years, and payments toward savings are amortized. So, if you open an installment loan with Credit Strong, it could take a decade to save $1K to $2.5K — And, in the end, you will pay quite a bit to make it happen. With that said, you can always make additional payments to fulfill the terms early and save on interest (plus, Credit Strong does not charge prepayment penalties).

Business Terms & Fees

There are two fee options with Credit Strong’s business offer: (1) with interest or (2) without interest.

Of course, the interest accounts end up costing more than the no-interest accounts, but the initial account setup fees are lower than the latter. So, if you have the cash to pay the fees upfront, it’s best to go with the interest-free option.

Here’s an overview of Credit Strong’s business terms & fees:

By the end of two years and one month, if you pay as agreed, you could have up to $10K in savings with a Credit Strong™ business account.

Note that with the interest business accounts, payments are split between interest and “principal,” which means you’ll probably pay more toward the interest you owe during the first ¼ of your loan term. Toward the end of the terms, more of your payments will be applied toward principal — this is called amortization and is how most installment loans work.

Credit Strong Account Requirements

To apply for a Credit Strong account, you should meet specific minimum requirements:

Personal Requirements

To qualify for a personal Credit Strong account, you must meet the following requirements:

- US resident with a physical US address (other than Vermont & Wisconsin)

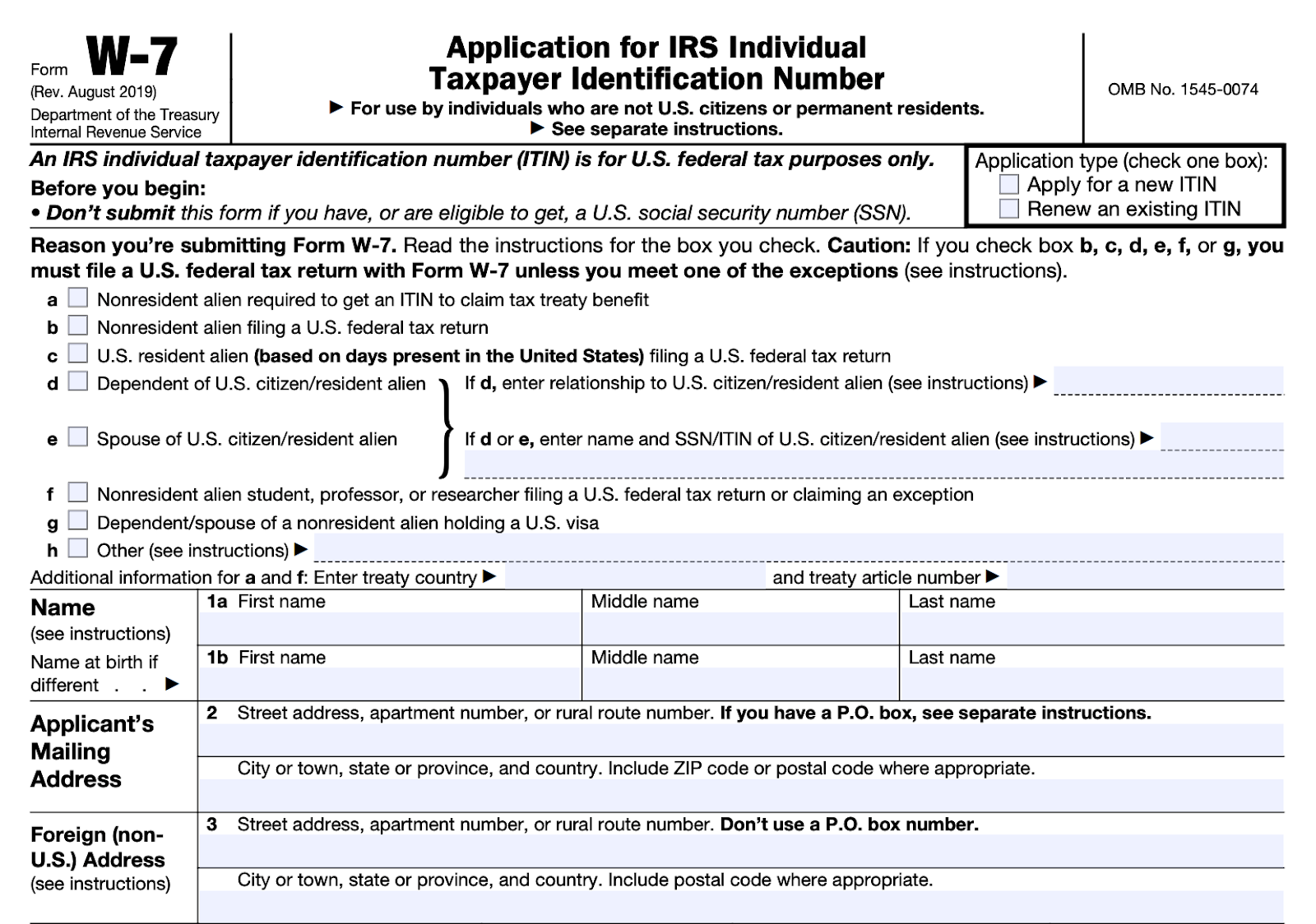

- Valid SSN or ITIN (individual taxpayer ID)

- Good-standing checking account, debit card, or prepaid card

- Working mobile phone number or Google Voice account

- Valid email address

Credit Strong will not use a credit pull or consider your income to determine eligibility for an account — basically, they only need to properly identify who you are and where you live.

Business Requirements

To qualify for a business Credit Strong account, you and your company need to meet certain requirements.

Individual requirements are as follows:

- At least 18 years of age and a permanent US resident

- US resident with a physical US address

- At least 25% ownership in the company

- No other co-owners that individually own 25% or more of the company

- Valid SSN or ITIN

- Valid, state-issued identification

And, here are the company requirements:

- Registered EIN

- At least 3 months since the business was legally established

- LLC., Partnership, or Corporation

- Located in the US with a valid, physical business address

Additionally, you must not take part in any prohibited business activities.

Frequently Asked Questions

Does Credit Strong Raise Your Credit Score?

Credit Strong’s offer gets mixed reviews. Depending on why a credit score is low, on-time payments on a Credit Score account may improve account holders’ credit scores by reporting on-time payments to credit bureaus. However, unpaid accounts can be reported as delinquent. So, it is only one piece of the credit-building puzzle.

Does Credit Strong do a hard pull?

No, Credit Strong does not do a hard pull to the applicants’ credit to approve accounts. So, if you apply for an account (so long as you make responsible payments) your credit score is safe.

Is Credit Strong a tradeline?

If you open a Credit Strong Business account, you can establish a financial tradeline in the form of a secured (pre-paid) installment loan. However, the company doesn’t yet report to business credit bureaus but does claim that they plan to in the future.

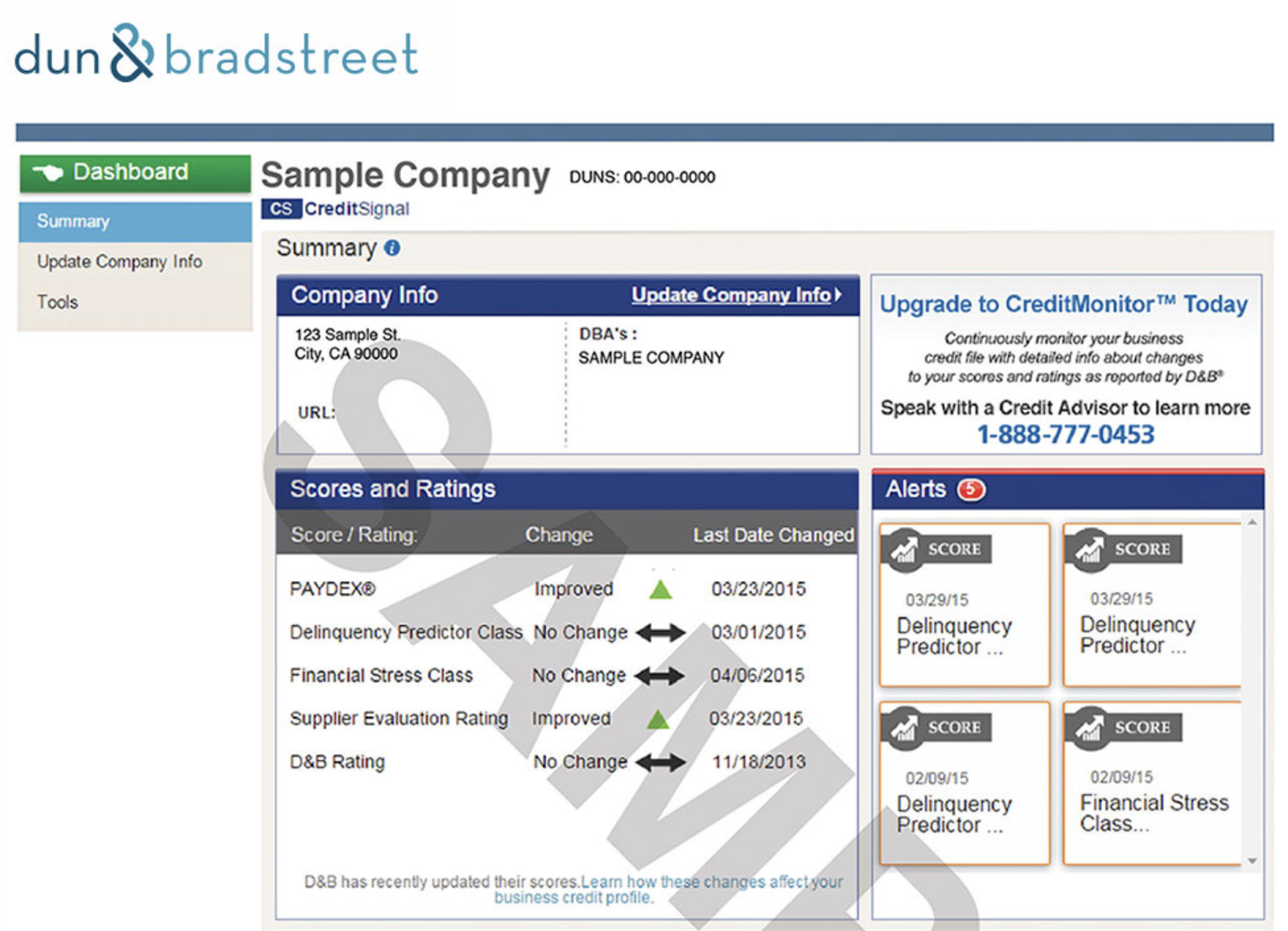

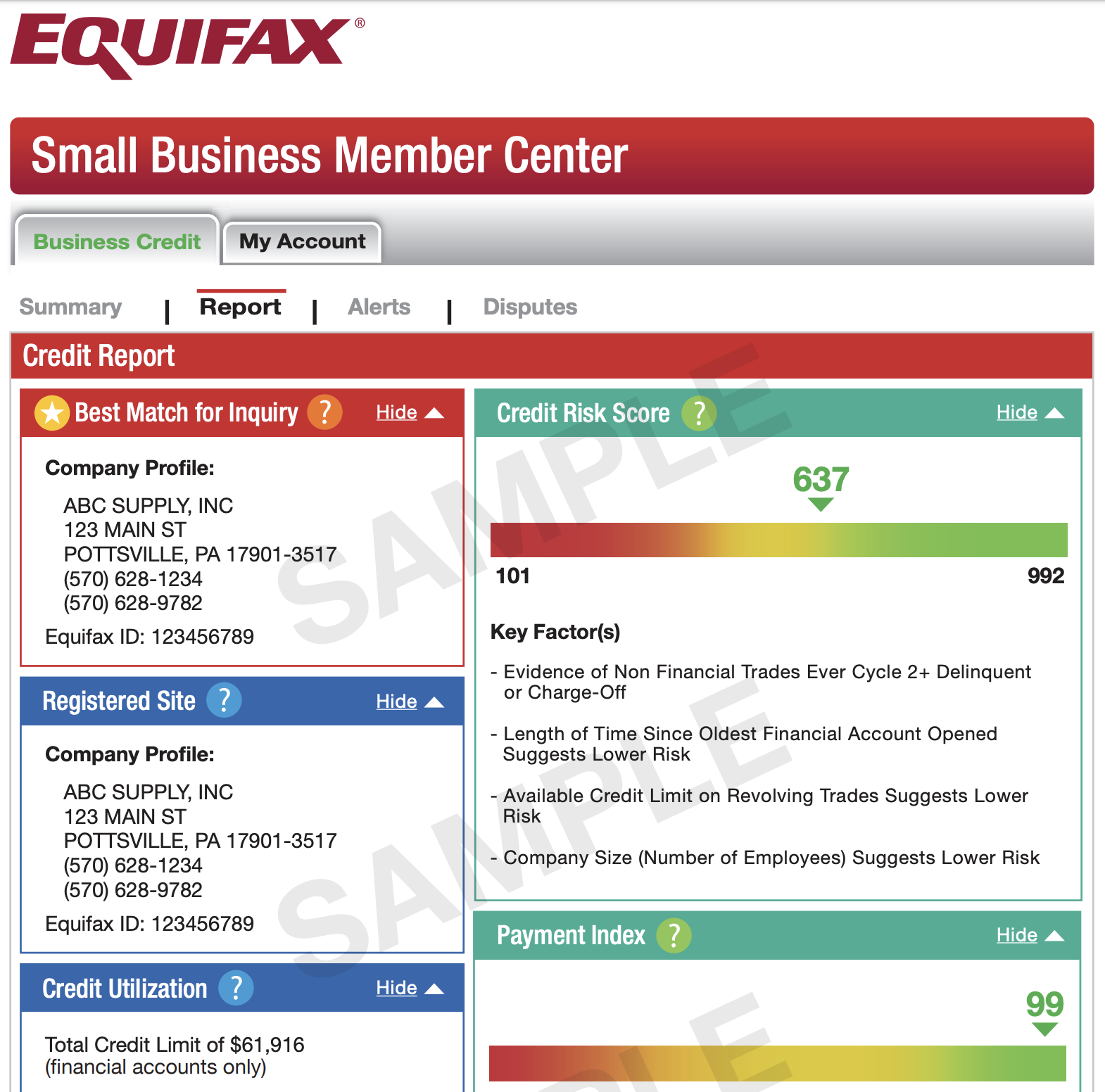

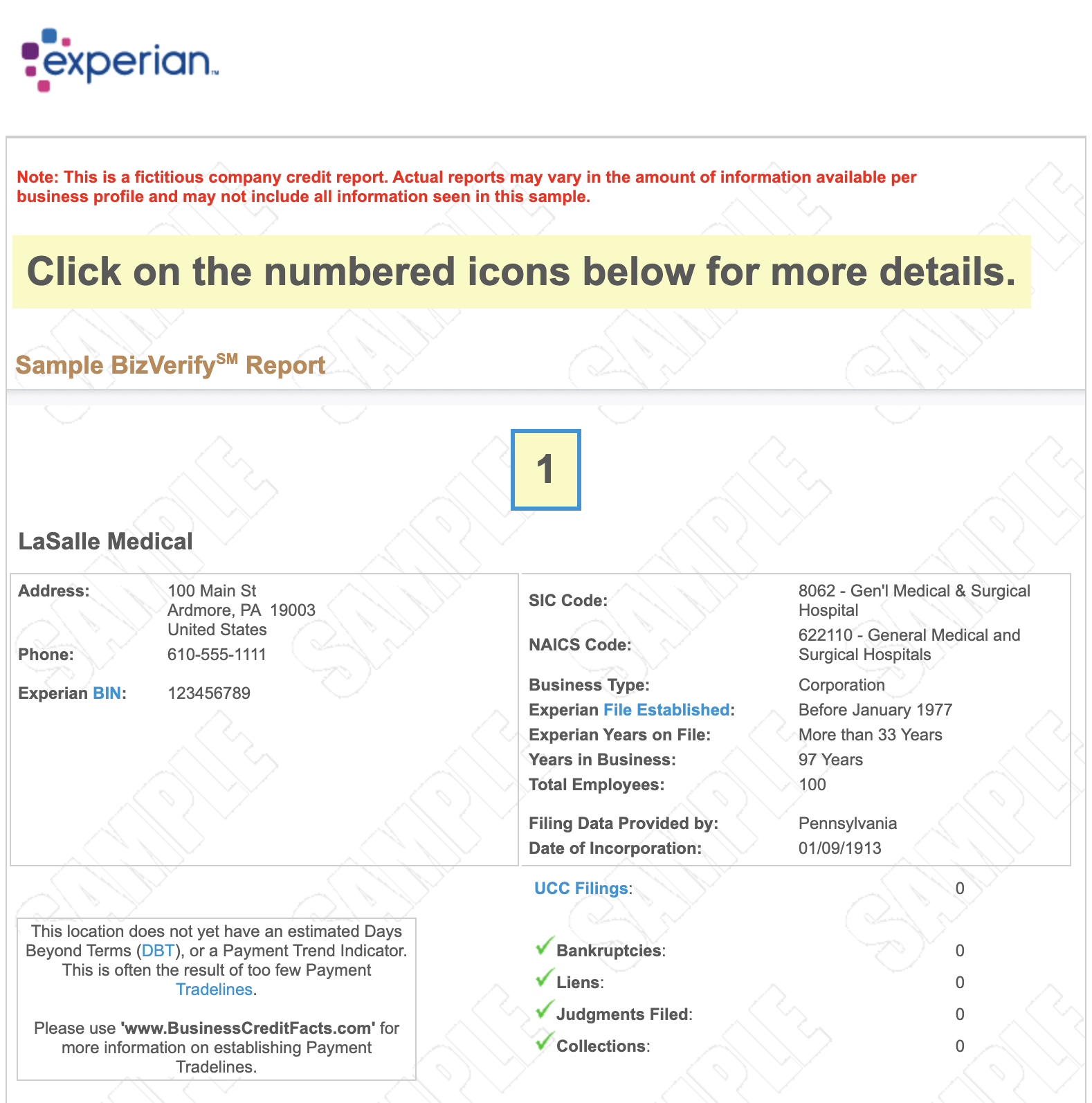

Does Credit Strong report to Dun & Bradstreet?

As of September 2022, Credit Strong does not report to Dun & Bradstreet (D&B) or any other business credit bureaus. The company reports to consumer credit bureaus Equifax and Paynet and claims that they do plan to eventually include Experian, D&B, and SBFE. So, the only way that Credit Strong might help build business credit currently is through helping to improve a business owner’s personal credit score and fund their savings account up to $10K.

It takes a bit of work, and specific qualifications for lenders to report to business credit bureaus. So, I choose to be optimistic and assume Credit Strong is working on building its user base to meet these requirements, and that they will start reporting to the business bureaus soon.

How many points does Credit Strong give you?

The number of points your credit score will increase with Credit Strong’s offer depends on the account holder’s current credit profile and their ability to make on-time payments on their account. There are several factors that influence credit scores:

- Payment history

- Amounts owed & utilization

- Length of credit history

- New credit applications (inquiries/hard pulls)

- Types of credit used

So, Credit Strong is merely a tool that can be used to build credit, but must be part of a comprehensive strategy — I recommend Credit Secrets for credit-building advice.

What happens if you stop paying Credit Strong?

If you stop paying Credit Strong as agreed, they can report negative information to credit bureaus. However, you may terminate your account at any time with no fees or prepayment penalties.

If you stop paying because your account terms are fulfilled, you can either leave your money in the savings account to accrue interest or transfer the funds to your bank account — getting your money from Credit Strong can take about a week.

Credit Strong Company Overview

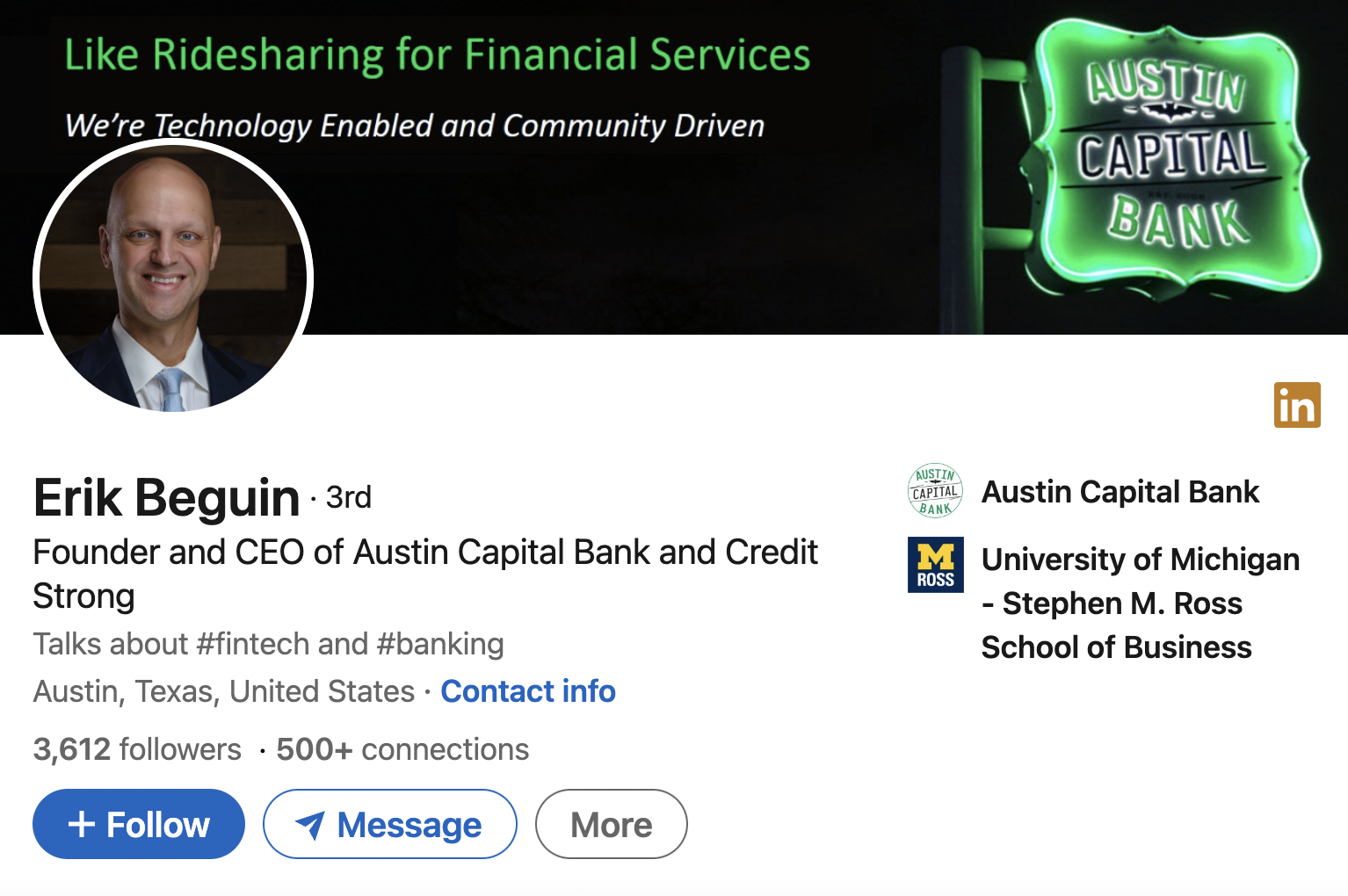

Credit Strong was launched in 2019, so the offer is pretty new. However, the parent company, Austin Capital Bank, has been around for a decade and a half, since 2006. Austin Capital Bank is a trusted community bank in Austin, Texas.

The bank’s founder and CEO, Erik Beguin, was previously a member of the Federal Reserve Board in Washington DC and served as a Chairman for the Federal Reserve Bank of Dallas before that, so he definitely knows finance.

Credit Strong Competitors: Side-by-Side Comparison With Self & Kikoff

Here’s a quick view of how Credit Strong, Self, and Kikoff compare, side-by-side, as accounts that build credit.

Credit Strong, Self, and Kikoff have credit builder offers that report payments to consumer credit bureaus with no hard pull to the applicant’s credit report. And, each of them offers an escrow/savings account.

None of the above companies report payments to any business credit bureaus, but Credit Strong promises that they will in the future.

Credit Strong is the only company, from the list above, that has an offer for businesses, and their account options are quite a bit more robust than the other two. Furthermore, they have more options for larger accounts. Nevertheless, the offers from Self and Kikoff might be better for individuals that would prefer a simple setup.

While these competitors seem to get the most interest in the credit builder and savings space, they are not your only options for credit builder loans or savings offers. Before you sign up for a Credit Strong account, I recommend you research offers from local community banks, such as a shared-secured loan, secured credit cards, and Individual Development Accounts (IDAs or “matched savings”) before you commit to anything new and shiny.

Recommended: 3 Best Credit Unions for Small Business Banking

More Answers to Related Questions

For those considering an individual credit builder offer, I feel like I should answer some general and more fundamental questions before I wrap up. But, if you’re a company owner exploring Credit Strong’s business offer, you might want to skip to the end.

What is considered a good credit score?

A FICO score between 670 to 739 is considered “good.”

What is an excellent credit score?

A FICO score of 800 and up is considered “excellent.”

How long does it take to build credit to 700?

The duration that it takes to increase a credit score to 700 depends on the individual’s existing credit profile and the tactics used. It can take from 60 days to several years to boost a score into this range.

How can you raise your credit score by 200 points in 30 days?

If you paid your credit down to utilization in the 30% range or lower, optimized your debt-to-income ratio, and had always made on-time payments to diverse accounts, it’s possible you could raise your credit score by 200 points in 30 days. But, this answer is highly broad — it could take some people many years to grow their score by 200 points, and others might be able to do it by removing discrepancies from their credit report (which can be done in 30 days).

How long does it take to build credit from 500?

Many people build credit from 500 within a few months. Again, this answer varies from credit profile to credit profile.

How fast can you build credit?

You can build credit in as little as 30 days, which is how long it takes most reporters to notify credit bureaus of changes to a credit profile (including payments made).

How fast can you rebuild credit?

If you have a smart strategy and funds, and your profile isn’t too messy, you can rebuild your credit in a month, but it often takes longer.

How can you raise your credit score in 90 days?

The best way to raise your credit score is to make on-time payments to all lenders, keep your utilization below 30%, and include a diverse array of accounts (revolving, installment, etc.). You should also monitor your credit report to watch for discrepancies and mistakes, and report them when they arise.

How long does it take to build credit to buy a house?

To buy a house, the credit score needed varies from lender to lender. It could take a few months or a few years to build a credit score high enough to qualify for a mortgage.

Recommended: Credit Secrets Book Review: Can You Erase Bad Credit History?

Conclusion: Is Credit Strong Legitimate?

From my research, I gather that Credit Strong is absolutely a legitimate company with an honest offer, which is intended to simultaneously build credit and savings. Secured loans and lines of credit are often used to build credit while savings are difficult for some people to manage on their own, so it’s natural that an offer like this would exist.

While there is a wave of poor Credit Strong reviews flooding the web, these seem to primarily come from account holders who did not understand the offer when they applied.

This tells me that the company might be better off if they clarify the details upfront, for those who might not understand what they’re signing up for. While I found Credit Strong to be pretty transparent, I can see how someone without a lot of credit-building knowledge would have a contrary opinion.

With that said, since they don’t yet report on-time payments to business credit bureaus, I don’t consider Credit Strong to be a particularly powerful offer to build business credit, but I look forward to watching that side of their offer evolve.

Now, if you’ve made it this far into this review, you should understand everything you need to decide whether the offer is right for your situation. Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today.