If you’re a business owner who wants to build business credit, and you’re in need of any of Newegg’s range of electronics, you may be interested in Newegg net 30 payment terms. Using their net 30 terms responsibly, you can get your on-time payments reported to business credit bureaus…But, is it worth it?

Here, I’ll explain exactly what you can expect with Newegg net 30, from the product offer to how to apply, and how your payments can impact your business credit. I’ll share everything I know.

This is what’s in store:

- What is Newegg Net 30?

- How to Get a Newegg Business Account & Apply for Net 30 Terms

- What Does Newegg Net 30 Do?

- Frequently Asked Questions

- Final Thoughts

Now, let’s dive in!

What is Newegg Net 30?

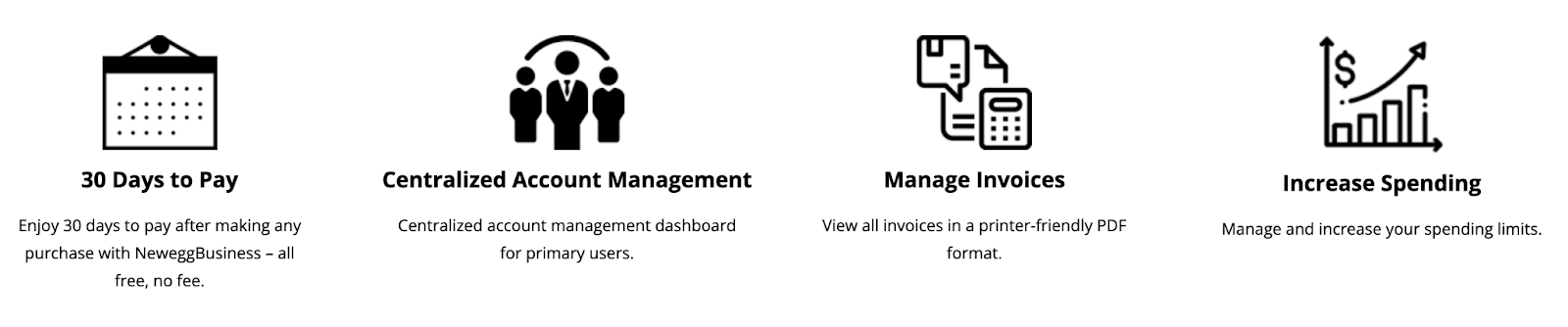

Newegg Net 30 is a “buy now pay later” credit line offered to businesses through Newegg Business, which allows you to manage your purchases with ease (and build credit). With Net 30 terms, you have 30 days to pay for any purchases, free of fees—This flexibility helps with managing your cash flow, giving you extra time to settle your invoices.

The service includes a centralized account management dashboard for primary users, which enables easy access to view and manage all your invoices in a printer-friendly PDF format. You can also manage and increase your spending limits as needed.

To apply for Newegg Net 30, you need a Newegg Business account. The application process takes approximately 3-5 business days, and approval notifications are sent via email.

After that, you can make purchases with net 30 terms (or net 55) and Newegg will report your on-time payments to Dun & Bradstreet and Equifax Business. In turn, on time payments will contribute to an increased business credit score.

Recommended: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

What Does Newegg Offer?

Newegg offers a comprehensive range of electronics and IT products tailored for businesses. Their selection includes:

- Computer hardware

- PCs and laptops

- Data storage solutions

- Networking equipment

- Servers

- IT solutions

They also provide computer peripherals, POS and digital signage, business software, and office supplies. Additionally, Newegg has products in the automotive and industrial sectors, as well as a variety of refurbished items.

Whether you need business laptops, desktops, docking stations, printers, or software, Newegg has a wide array of products to meet your business needs.

You might also like: Summa Office Supplies: Should You Leverage Net 30 Terms?

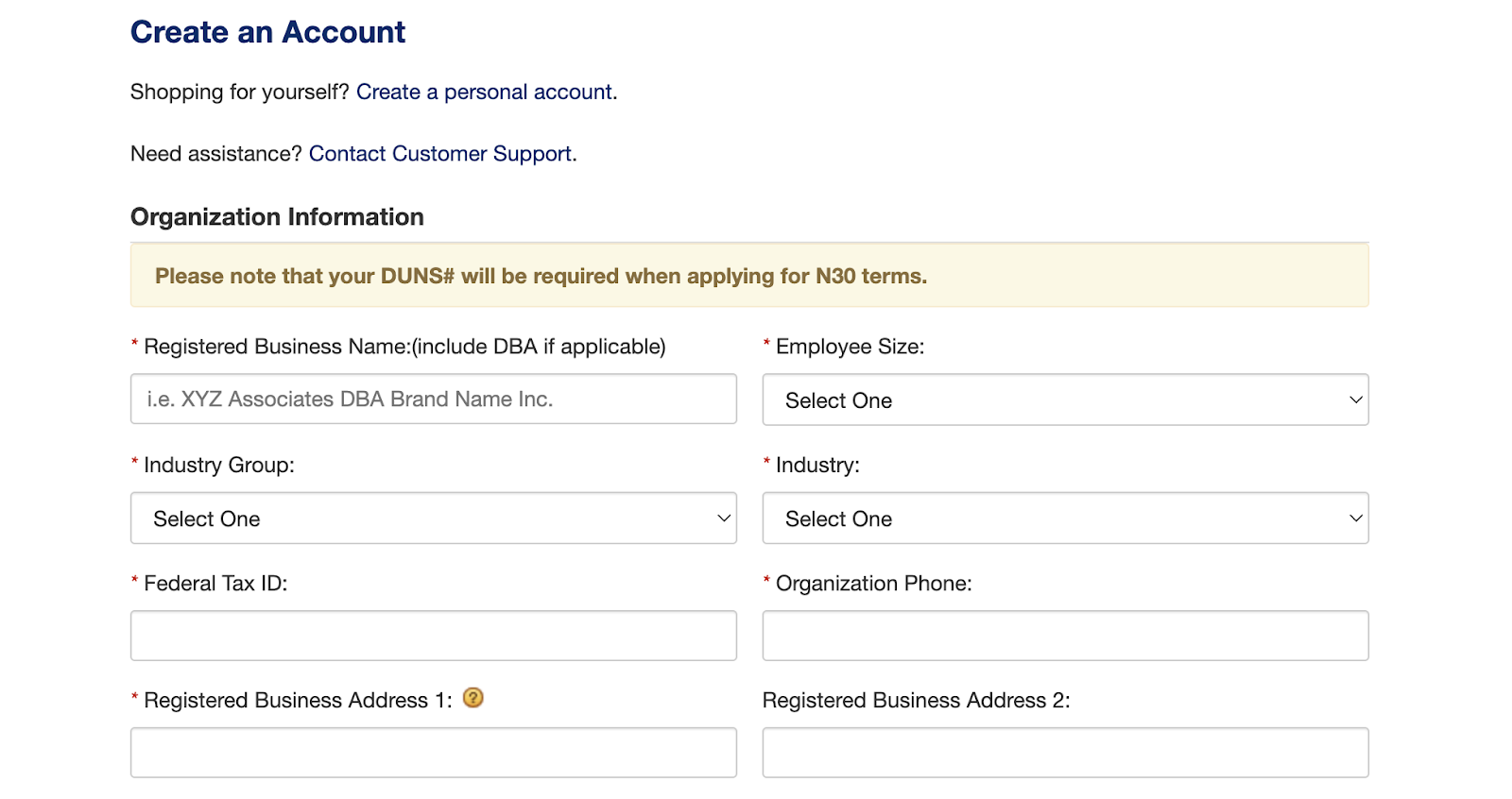

Newegg Net 30 Requirements

Newegg Business serves all sized businesses, education institutions, government entities, healthcare procurement, and VARs & SIs—To apply for Newegg Net 30 terms, you need to make sure you meet several key requirements.

First, you must have an active Newegg Business account—This account serves as the foundation for managing your transactions and credit terms with Newegg. Only the primary account holder is eligible to apply for Net 30 terms, although they can authorize sub-users under the account to use the credit line.

You will also need to provide your organization’s DUNS number, a unique identifier often required for business credit applications.

Moreover, gather essential business information including your:

- Registered business name (with DBA if applicable)

- Federal tax ID or Employer Identification Number (EIN)

- Organization phone number

Registered business address - Your organization’s website URL

You also need a business email address to create a Newegg Business account to apply for Net 30 terms. This email will serve as your login for the account and will be used for communication regarding your Net 30 terms application and other account-related matters.

Lastly, ensure you have user information ready for the primary user who will manage the account, including their first and last name, job title, a business email domain, and a chosen password.

You might also like: Free, Printable Business Credit Application Template (Plus, How to Use it)

Company Overview

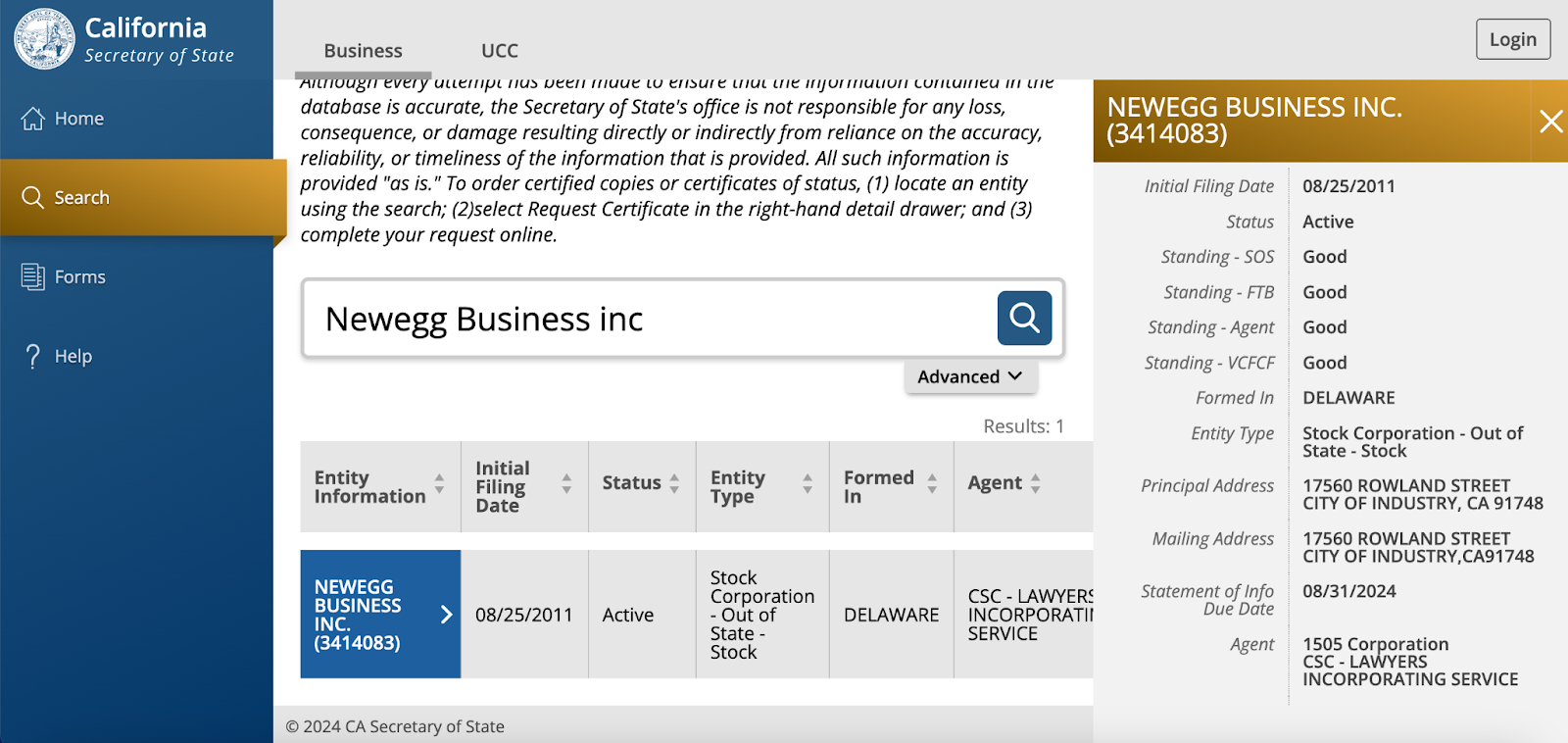

Newegg Business Inc. is a Los Angeles-based, for-profit eCommerce company that was founded in 2001 and officially established as a subsidiary of Newegg Inc in 2011. The company is currently active and in good standing with the California Secretary of State.

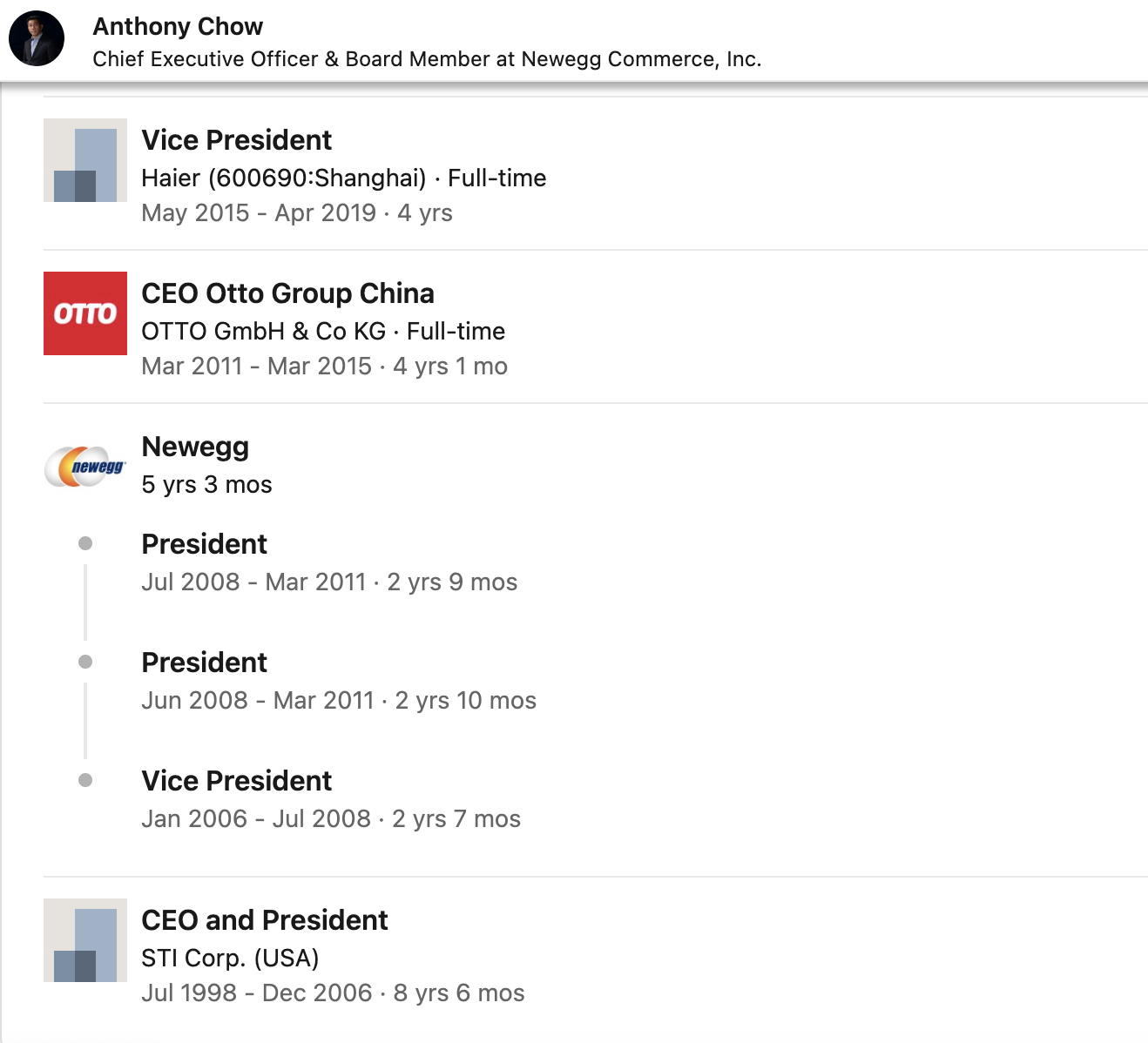

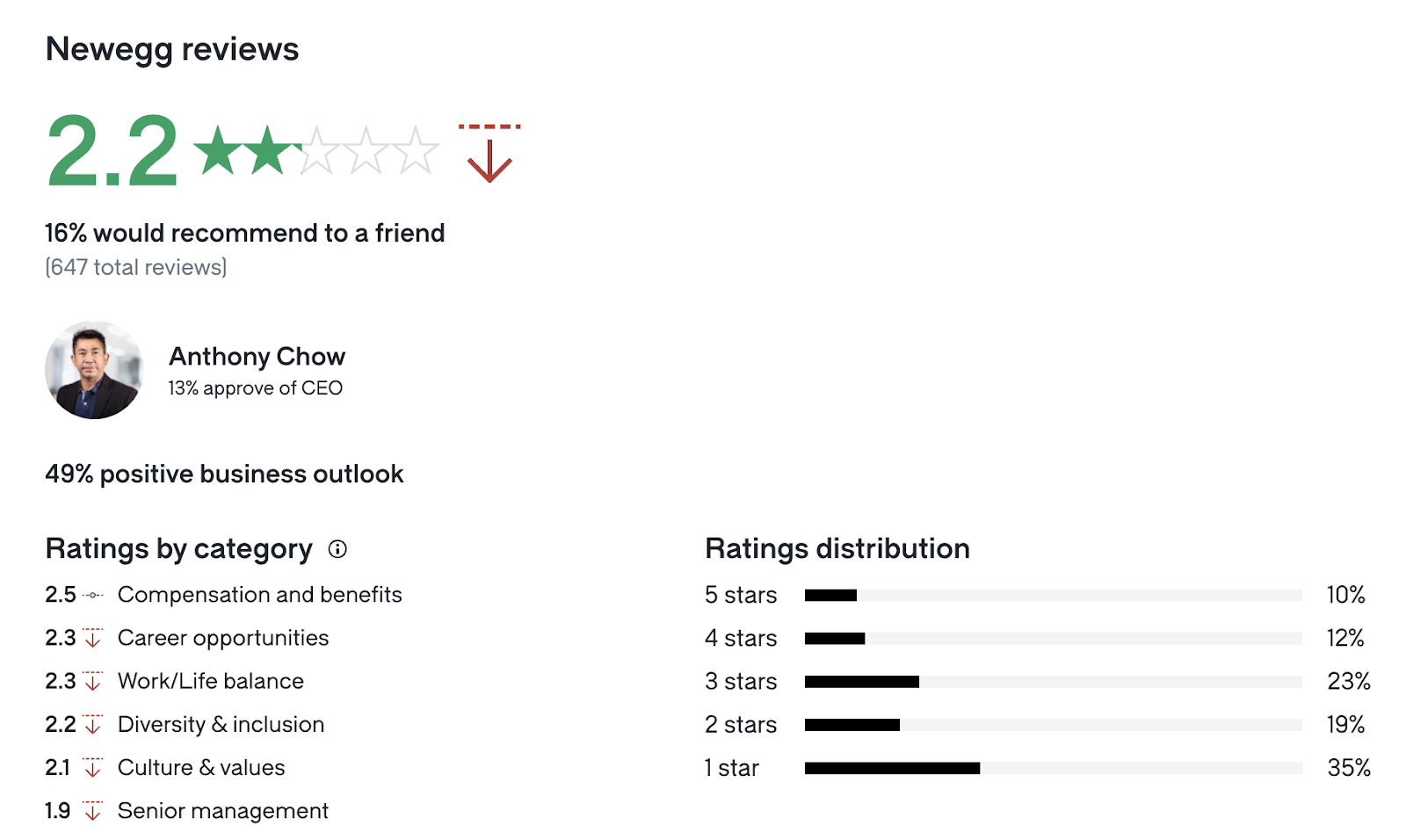

Newegg’s current CEO, Anthony Chow, has been with the company since 2006, and has a strong executive background, having previously worked with STI corp, Otto Group, and Haier.

However, they have a below industry average rating on Glassdoor, where employees are fairly unsatisfied with their treatment. Newegg has a 2.2-star rating on the platform, with particularly low senior management ratings.

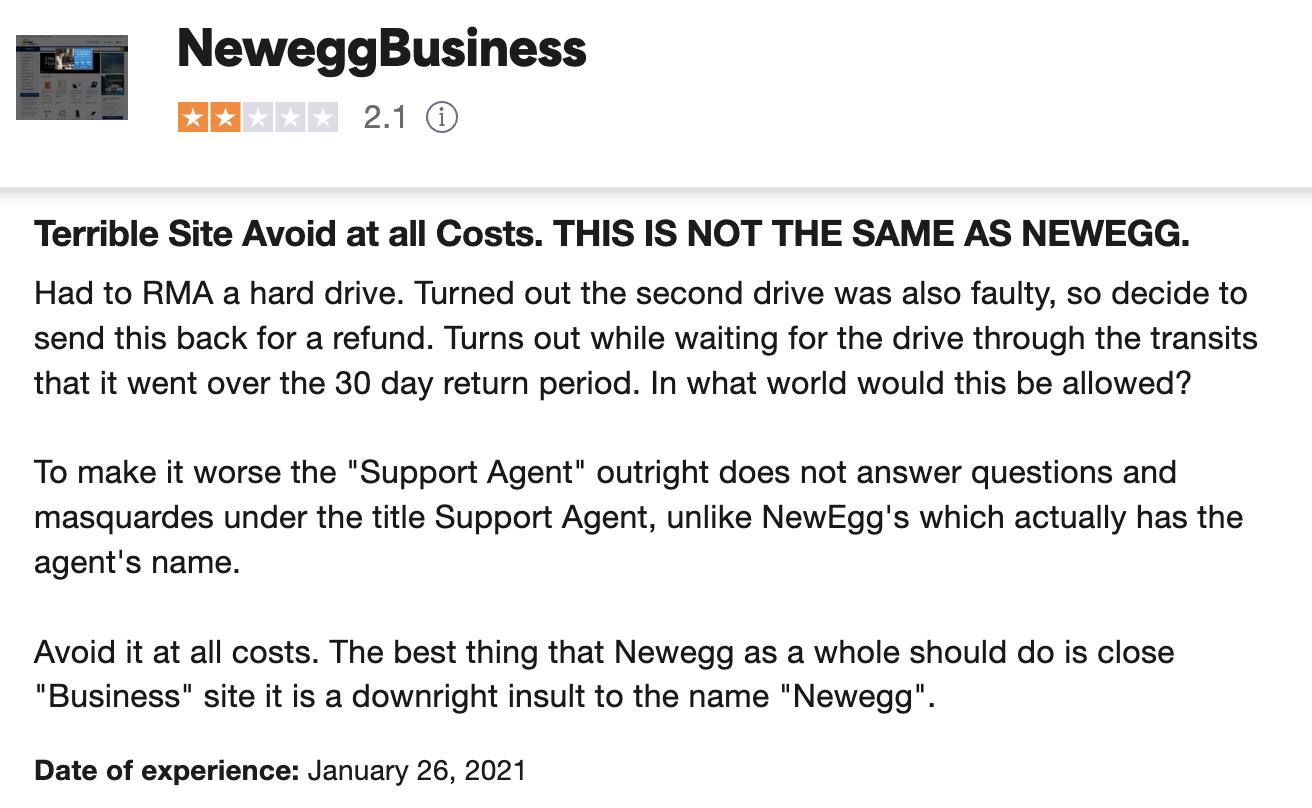

While staff opinions can tell you a lot about a company, customers are even more important to listen to. NeweggBusiness has garnered a poor TrustScore of 2 out of 5 on Trustpilot from 12 reviews.

Trustpilot complaints primarily focus on issues such as poor customer service, delays in order processing and delivery, product quality concerns, and difficulties with returns and refunds. Keep in mind, this sample is rather small, and people are more likely to leave a review when they’re upset than when they’re satisfied.

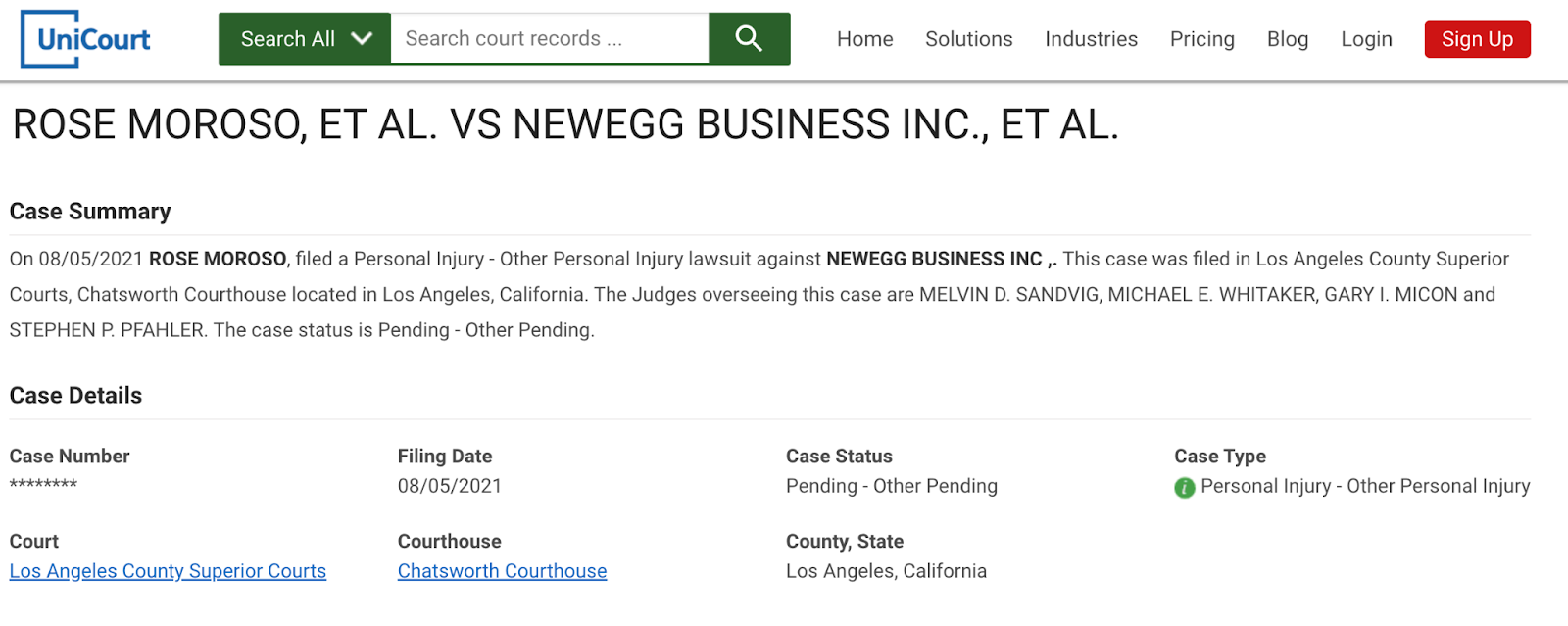

I found one lawsuit targeted at Newegg Business Inc., which was filed by Rose Moroso for personal injury that doesn’t fall under other specified categories. The case is currently pending in the Chatsworth Courthouse of the Los Angeles County Superior Courts in California.

Because the case is pending, I can’t speak to any conclusions that might be drawn.

In all, the Newegg Business Inc., the company that oversees Newegg Net 30, is a legitimate business, but they may have some issues with customer service and employee satisfaction.

You might also like: How to Use a Home Depot Business Account to Boost Your Credit

How to Get a Newegg Business Account & Apply for Net 30 Terms

Applying for Newegg Net 30 terms is straightforward if you follow these steps:

- Log into your existing Newegg Business account or create a new one if you haven’t already.

- Navigate to your account dashboard where you’ll find the “Apply” link within the Net 30 Term Account section. Click on this link to access the application form.

- Fill out all required fields accurately and completely, Make sure that all business and user information is correct and up-to-date.

- Submit the application form electronically through the provided interface.

Processing typically takes 3-5 business days, so you’ll have to wait—You will receive an email that notifies you of your application status. If Newegg requires additional information or verification, they will contact you using the primary email associated with your account.

For further assistance or questions about the application process, contact Newegg Business directly at (888) 482-6678 or email sales@Newegg Business.com.

You might also like: This is How to Get Grainger Net 30 Terms (+Build Business Credit)

What Does Newegg Net 30 Do?

Newegg Net 30 offers businesses a valuable financial tool by providing a flexible payment option for purchasing electronics and other essential products. This payment term allows businesses to manage their cash flow effectively, balancing immediate operational needs with financial stability. It’s akin to having a line of credit tailored to your purchasing needs, offering convenience and flexibility in procurement.

1. Comprehensive Product Offer

Newegg boasts a diverse array of electronics, hardware, and software products suited for businesses across various industries. From high-performance computing equipment to everyday office supplies, Newegg covers a wide spectrum of business needs.

Now, Newegg’s prices aren’t the best. To show you an example, I pulled two products at random:

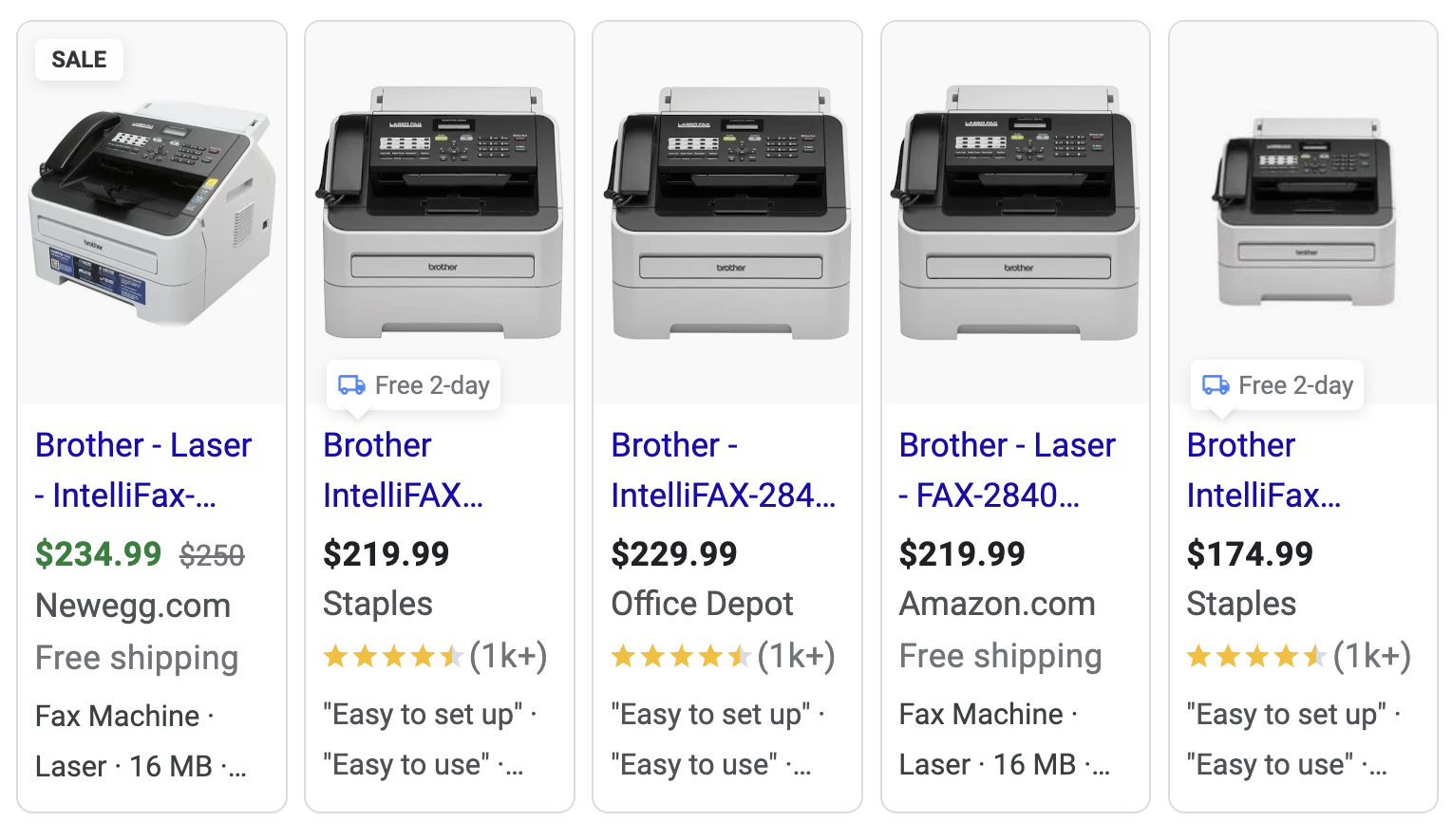

- Newegg has the highest advertised price on the Brother IntelliFax-2840 High-Speed Laser Fax.

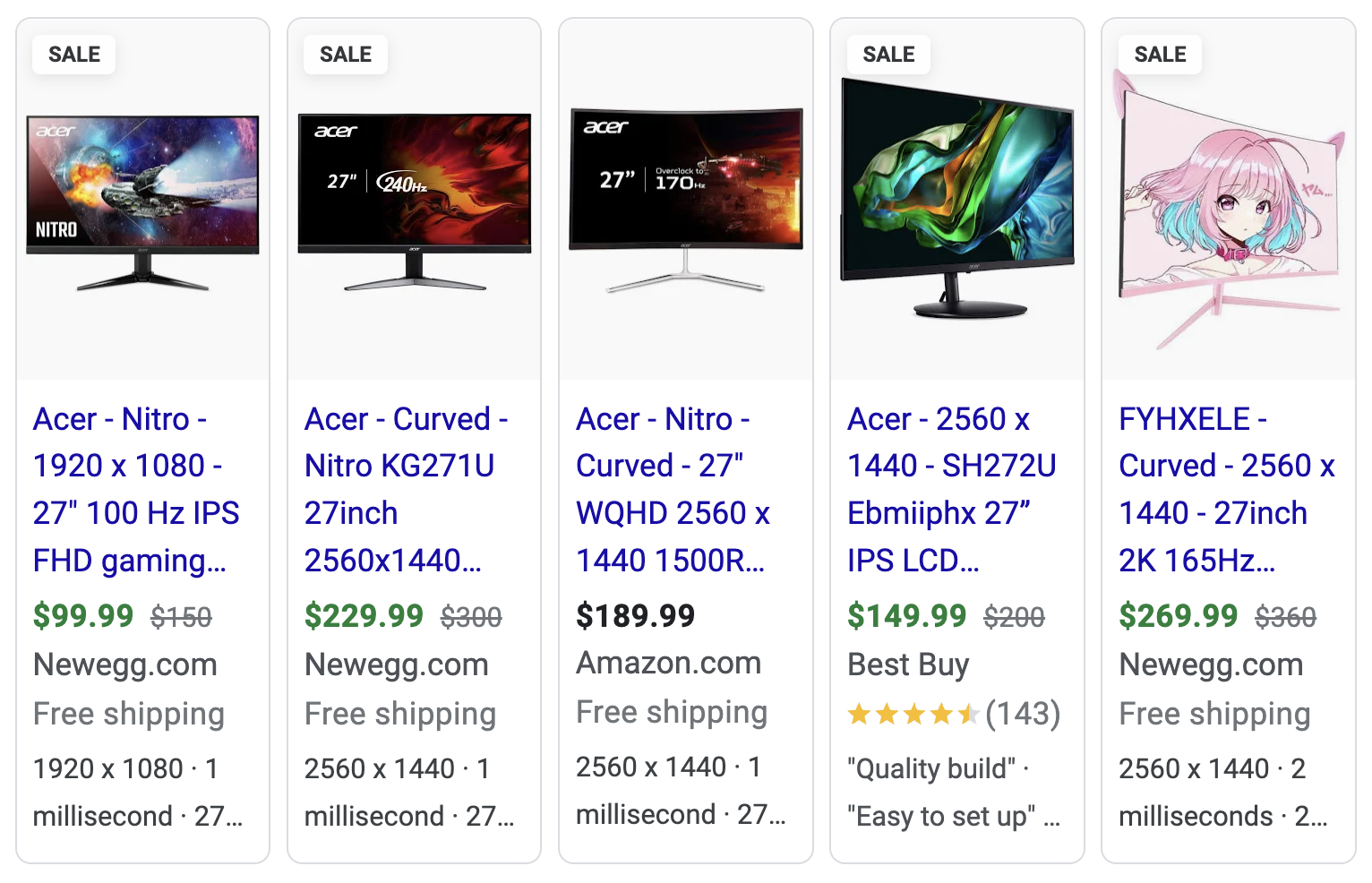

- But, their price for the Acer Nitro XZ271U 27″ 1500R Curved Zero-Frame Monitor is competitive.

While prices on Newegg may sometimes be higher, the convenience and deferred payment option can outweigh the slight premium. And, compared to other net 30 vendors I know of, their prices don’t seem to be marked up quite as much—I believe this is because they work with various vendors, which drives competitive pricing.

When shopping on Newegg, consider the total cost of ownership rather than just the upfront price. Factor in the convenience of deferred payment and the business credit-building potential, which has value in itself. And, keep in mind that you can probably write off some of these purchases, though you’ll have to ask your accountant to be sure.

You might also like: Is Dell Business Credit Worth Your Time?

2. 30 or 55 Days to Pay

The 30-day and 55-day payment windows that Newegg Business Net 30 and Net 55 offer can significantly impact your business finances by providing a buffer in cash flow management—This period allows you to procure necessary equipment or supplies without immediate financial strain. Buying now and paying later can preserve liquidity for other expenses.

However, it’s super important to honor payment deadlines diligently to avoid late fees and maintain a positive relationship with Newegg Business. When you don’t pay on-time, you’re at risk of having this reported to business credit bureaus as well, which can negatively impact your business credit.

Note: Newegg’s Net 55 terms are harder to come by and offered through Synchrony Bank (accessible after your business credit is established).

Use your 30-day or 55-day payment term strategically to optimize your cash flow. By timing your purchases and payments just right, you can synchronize cash inflows and outflows, which can make your business finances more stable. And, along with other vendor offers like Uline Net 30 or Amazon Net 30, you can use your purchases to boost your business credit score.

You might also like: Using 30 Day Net Vendors to Build Your Business Credit Score

3. Reasonable Application Process

While instant account approval isn’t an option, Newegg’s Net 30 application process is straightforward and typically processed within 3-5 business days. You are required to furnish basic business information and undergo a credit evaluation—This cautious approach helps make sure that credit terms are extended responsibly.

You can get your business matched with suitable purchasing power without unnecessary delays. You can also treat the application process as an opportunity to assess your business’s financial health—By understanding your creditworthiness and how it’s perceived by vendors like Newegg, you can proactively manage and improve your business’s financial standing over time.

You might also like: BILL Spend & Expense Card Review (Formerly Divvy Credit Card)

4. Reports to Business Credit Bureaus

One of the standout benefits of utilizing a Newegg Net 30 account is that they report on-time payments to business credit bureaus. This helps establish and strengthen your business credit profile, potentially opening doors to better financing options and vendor relationships in the future.

On the other hand, failing to pay on-time can negatively impact your credit score, limiting your access to favorable terms from other suppliers and financial institutions.

And, some people have cited that they don’t report frequently or that their payments weren’t reported at all. Whether this is true or not, I can’t personally speak to.

Look at your net 30 account, not just as a purchasing tool, but as a means to build long-term financial credibility. Consistent, timely payments demonstrate reliability and responsibility, which can enhance your business’s reputation and negotiating power in the marketplace.

You might also like: 2 Additional Vendors that Report to DNB Automatically

5. Affiliate & Reseller Programs

Newegg Business offers two key programs beneficial for small businesses interested in leveraging their offerings and utilizing Net 30 terms.

The Affiliate Program allows you to earn commissions by referring customers to NeweggBusiness through their websites. It’s free to join, requires no startup or maintenance fees, and provides easy-to-use marketing tools such as text and banner links.

You can promote a wide range of products including:

- Computer electronics

- Office supplies

- Networking gear

The Reseller Program enables you to sell directly on Newegg’s platform, which reaches over 350,000 verified business customers and taps into a global marketplace of over 37.3 million customers. Sellers benefit from low commission rates applied only to successful sales, along with tools like Shipped By Newegg (SBN) for streamlined fulfillment services.

You might also like: A Complete Fundwise Capital Review: Should You Apply for Funding?

6. Rewards Program

Newegg Business Rewards is a loyalty program where you earn “BizPoints” based on your purchases, with higher tiers offering increased benefits.

- At the Platinum level (for purchases over $20K), you earn 2 BizPoints for every $2 spent, along with perks like hassle-free returns and discounted Saturday deliveries.

- Gold level members (spending up to $5K), earn 1.5 BizPoints per $2, with benefits including free shipping on eligible orders over $500.

- Silver level (for purchases up to $4,999), earns 1 BizPoint per $2, and provides access to exclusive offers.

So, purchases on the platform are incentivised.

You might also like: Full Shopify Credit Review: Are the Cashback Rewards Legit?

Frequently Asked Questions

Can you finance a PC on Newegg?

Newegg offers financing options through partners, including terms like Net 30 and Net 55, allowing you to finance purchases, including PCs.

Does Newegg let you make payments?

Yes, Newegg accepts various payment methods, including credit/debit cards and financing options such as Net 30 and Net 55, tailored to different purchasing needs.

Does Newegg report to Dun & Bradstreet?

Yes, Newegg Business reports net 30 payment history to Dun & Bradstreet and Equifax Business. Timely payments can positively impact your business credit profiles with these bureaus.

How many Net 30 accounts should you have?

It’s recommended to have a few well-managed Net 30 accounts to build your business credit effectively. Aim for a manageable number, typically ranging from 2 to 5 accounts, depending on your business’s size and credit goals.

What is the Newegg scandal?

The Newegg scandal involved a situation where a customer returned an open-box motherboard to Newegg, but upon receiving it, Newegg claimed it was “damaged.” This assertion was contested and, despite the controversy, Newegg eventually resolved the issue by offering a refund to the buyer.

Final Thoughts

Newegg Net 30 offers a strategic way to manage cash flow while building your credit profile through timely payment and reporting to business credit bureaus—This service provides flexibility with 30-day repayment terms, which enables you to access a wide range of electronics and IT products without immediate financial strain.

Despite some concerns about customer service and employee satisfaction, Newegg Business Inc. remains a viable option for businesses seeking to optimize purchasing power and enhance their creditworthiness in the marketplace.

If you’re considering leveraging Newegg Net 30, weigh its benefits against potential drawbacks to make an informed decision for your specific circumstances.

Ready to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!