The Divvy card has been making waves as a high-tech, free, business credit card since it first launched. Now, the card has been acquired by Bill.com and rebranded as Bill Spend & Expense — And, as I’m about to show you, it’s even better than that.

This business funding solution offers powerful budgeting software, virtual cards, rewards, and more. But, do they truly deliver on all of their promises, and is the BILL Spend & Expense credit card right for you?…Here, you’ll find the answer.

This is what’s in store:

- What is a BILL Card?

- How Does a BILL Card Work?

- BILL Card Customer Service

- BILL vs Ramp vs Brex vs Stripe Capital

- Answers to Common Questions

- Takeaway: Should You Get a BILL Card?

Plus receive $200 by opening a new account.

What is a Bill Spend & Expense (Divvy) Card?

The Bill Spend & Expense card (previously Divvy Visa) offers fast and flexible business credit for “all-sized companies.”

And, there are a handful of edges this card has over most of its competitors:

- A user-friendly platform for expense management, budgeting, and bill-pay

- The Spend & Expense virtual card offers a modernized credit solution

- More frequent payments lead to higher bonus rewards

- All services are free for the cardholder (Divvy used to charge for reimbursements — Now that Bill has taken over, those fees are gone)

Since they don’t charge the usual fees to cardholders, the offer makes money by taking a portion of transaction fees charged to the merchant for each purchase.

(When you hear the name, Divvy, you might think of the bike subscription service, stock purchase product, or homebuyer program. The Divvy business credit card was an unrelated offer.)

Recommended: 7 Best Cash Back Corporate Cards to Explore

Bill Spend & Expense Card Requirements

While the talking points above are genuinely exciting, this card (like all financial services) has it’s pitfalls for some people. In the past, Divvy was somewhat elusive about their qualification requirements, but they did share some things about what makes a successful applicant.

- At least $20K in an active bank account

- A “good” to “very good” credit score

- Company based in the United States

Bill Spend & Expense has not likely veered far from these requirements. I would recommend a credit score of 670 to 850 before you apply. Bill is also going to look at your time in business and your company revenue when they consider extending a line of credit.

Recommended: This is How to Build Business Credit Fast [Step-by-Step Guide]

Divvy Credit Card Limit

Divvy’s credit card limit was $15 million and based on your business cash flow. The system’s algorithm determined the amount that you are likely to be able to afford in full each month, which would typically be about ⅓ of your monthly revenue. If you were offered a lower limit initially, credit limit increases were offered after consistent on-time payments.

Bill Spend & Expense offers credit limits from $500 to $5 million, based on your revenue at the time of applying. With Bill, you have the option to seek a credit limit raise every 90 days — If your request exceeds $150K, you’ll need to connect your bank account to the platform. And, you may have to provide supplementary financial documents.

Recommended: No-Doc Business Loans: Get Funds Without Proof of Income

Bill Spend & Expense App Overview (Used to be ‘the Divvy App’)

Android users loved the final updates to the Divvy app. In the beginning, their app rating wasn’t so high, but Divvy listened to early user complaints to enhance their mobile features to most cardholders’ liking.

Bill Spend & Expense has left users even a little more satisfied!

People love the app layout and visibility into their expenses. They also appreciate that they can upload and store receipts, categorize business transactions, and manage virtual cards from any device.

Now, let’s dive deeper.

What to Expect When You Apply for a Bill Spend & Expense Card

Your first step on the path to a Divvy account used to be checking out the demo or to applying for business credit. The application process was pretty thorough, yet easy.

With Divvy, you’ll were asked to provide banking information, income, and details about your business to determine the credit limit you could qualify for. I loved their application process because it left no stone unturned and gave you the option to include documentation upfront for a faster decision (But, I was so excited that I didn’t want to wait the three days it took to hear back from an account manager.).

Back then, Divvy assessed income by analyzing business checking transactions and averaging deposits to offer a credit limit of around 30%. No credit score was required; spending limits were based on bank deposits. Some applicants with past overdrafts or high-risk spending behavior were asked for a cash deposit. Even if denied a line of credit, they were typically offered a prepaid option. Upon approval, it took a couple of weeks to receive the card.

The original Divvy card did not require a personal guarantee (it wasn’t backed by the business owner’s credit or assets). Now, the Bill Spend & Expense card pre-approval application does ask for the owner’s credit score, which indicates that a personal guarantee is required. I reached out to confirm, and Bill’s customer service let me know that, “the signer is liable for the account.”

Now, the application process for Bill Spend & Expense card is said to be just as smooth as the original DIvvy card—Though some users have gotten stuck during the app authentication process.

Overall, the application process is said to be similar to how it was when it was Divvy. The major changes are in the card now requiring owner liability and I can’t remember if they charged foreign transaction fees — but they do now.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN

How Does a BILL (formerly Divvy) Card Work?

If you qualify for a Divvy account, in addition to a new line of business credit, you’ll get access to some helpful tools. Learn more about their exclusive spend and expense management, AP automation, virtual card(s), and above-average rewards.

1. Bill Divvy Spend & Expense Management

Divvy’s spend and expense management platform empowered users to manage business and employee finances efficiently, particularly within specific categories, a feature highly praised by most users. The platform assigned each employee a card with a budget, allowed staff budget limitations on a case-by-case basis, enabled budget increase requests for unexpected expenses, automatically categorized spending, and facilitated receipt uploads within the app. Real-time access to spending reports was also available.

However, to access these tools for free, users needed to spend a minimum of $5,000 of their Divvy credit each month, potentially excluding those with lower budgets.

Payments were automatically withdrawn on the due date, coinciding with statement generation, although some users desired more flexibility, such as payment grace periods and additional time for invoice review.

ApBoth Divvy and Bill Spend & Expense have robust expense management solutions with features such as real-time expense tracking, automated categorization, and integration with accounting software — While the updated platform provides similar functionalities, the specific implementation and user experience will vary from person to person.

You might also like: Corporate vs Business Credit Card: What’s the Difference?

2. Bill.com Accounts Payable Automation

In addition to spend and expense management in the Divvy dashboard, cardholders can leverage Bill’s AP automation technology to streamline their entire accounts payable process.

- Import or manually enter your recurring and one-time bills

- Simplify your payment approval procedures

- Automate payments via ACH, credit card, check, or wire transfer

- Sync with your budgeting software

Of course, the AP automation system from Bill is designed to work effortlessly with Divvy’s platform (what the Bill Spend & Expense system is based on), but it can also be used as a standalone service.

You might also like: Is BHG Financial Legit? Business Loans, VC, +More

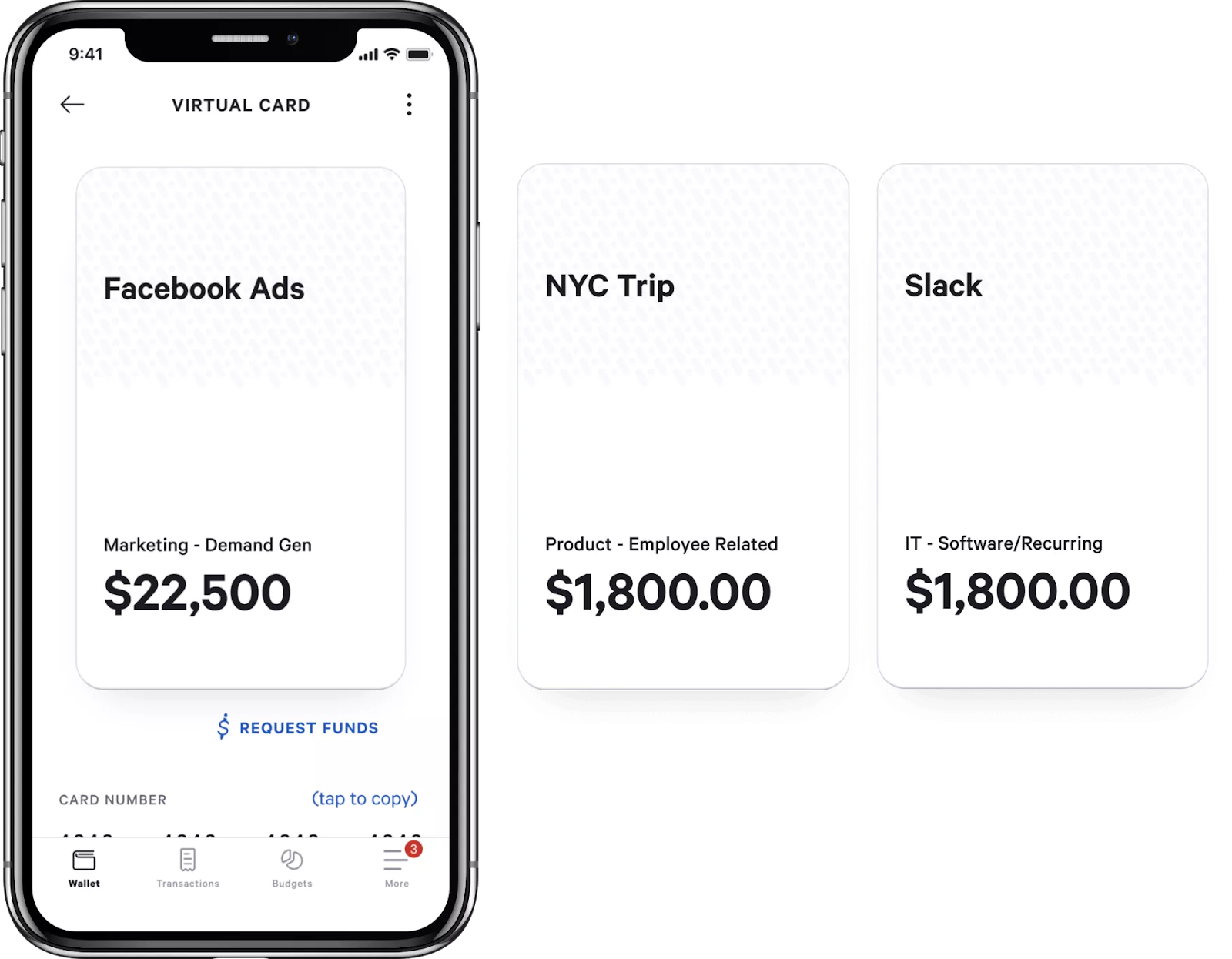

3. Bill Divvy Virtual Cards

In addition to your physical card, each user can access virtual cards on their mobile device. Instead of a carbon copy of their original card, virtual cards act as a “burner credit card.” These can be particularly helpful for temporary subscription offers where a staff member could forget to cancel their account at the right time.

They’re also handy for high-risk situations wherein a card could be compromised.

Rather than wait a week or more for a new card or multiple cards to arrive in the mail, users can generate a new, 16-digit card number to use immediately for purchases. Plus, virtual cards can make the general business spending experience super secure.

4. Bill Divvy Card Reward Points

Reward points on Divvy card spending have three tiers. Each tier is based on how often the credit is paid off and earned points increase with frequent payments.

- Weekly Rewards

- 7X on restaurants

- 5X on hotels

- 2X on recurring software subscriptions

- 1.5X on everything else

- Semi-Monthly Rewards

- 4X on restaurants

- 3X on hotels

- 1.75X on recurring software subscriptions

- 1X on everything else

- Monthly Rewards

- 2X on restaurants

- 2X on hotels

- 1.5X on recurring software subscriptions

- 1X on everything else

Rewards can then be redeemed as cash back, gift cards, statement credit, or travel (formerly Divvy Travel). Travel rewards can now be redeemed through Bill’s TravelPerk partnership for double rewards.

$1,500 in restaurant spending for an account paid weekly can earn card users roughly $100 for travel, $51 for gift cards, $49 for statement credit, or $52 cash back.

You might also like: What is the Best Credit Card for Ad Spend? Expert Insights

Divvy Card Customer Service

The customer service at Divvy used to receive mixed reviews. Front-end communication was automated through Intercom™. One feature of the platform was that customers had access to their entire conversation, without logging in, from the company’s main website — and the customer service team had access to these conversations as well, which was appreciated.

Bill Spend & Expense utilizes Drift® for their AI chatbot. So, the customer support experience is comparable to how it was with Divvy. It’s not my favorite and support staff isn’t the fastest at responding. But, they do eventually respond.

Additionally, Divvy’s help center was a pretty extensive knowledge base designed to help users with everything from managing cards to reimbursements and more. Now, Bill’s help center is equally robust.

You might also like: Free, Printable Business Credit Application Template

Bill Divvy vs Ramp vs Brex vs Stripe Capital

Now, let’s just take a quick look at how Bill Divvy stacks up next to Brex, Stripe, and Ramp (all of which are free). Find out if this offer holds its ground.

|  |  | ||

| APR | 0% | 0% | 0% | 0% |

| Fees | $0 | $0 | $0 | $0 |

| Pay in Full Terms | Monthly | Monthly OR Daily | Monthly | Monthly |

| Virtual Cards | ✅ | ✅ | ✅ | ✅ |

| No Personal Guarantee | ✅ | ✅ | ✅ | ⛔ |

| No BusinessCredit Check | ✅ | ✅ | ✅ | ✅ |

| Cashback Rewards | 2% on two top spend categories | 1-7X Points on all spending | 2% on all purchases | 1-7X Points on all spending |

| No Foreign Transaction Fees | ✅ | ✅ | ✅ | ⛔ |

| Reports to D&B | ✅ | ✅ | ✅ | ✅ |

And, while Stripe and Brex don’t have the same level of built-in advanced expense tracking as Bill (Divvy), they provide other standout features — For example, Brex can be used like a bank account with no ACH transfer fees and Stripe enables you to see your business income and expenses in one unified dashboard.

Bill Spend & Expense charges foreign transaction fees and requires a personal guarantee, which takes it down a couple notches compared to competitor offers. But, if these things aren’t important to you, the high rewards could make it the right pick.

You might also like: Brex Card Review: Is This Corporate Card Offer Too Good to Be True?

Frequently Asked Questions

Does Divvy report to credit bureaus?

Yep. An awesome feature of Bill Divvy Spend & Expense is that they do report on-time payments to the Small Business Financial Exchange (SBFE). The SBFE then reports your payment behavior to Dun & Bradstreet, Equifax, Experian, and Lexis Nexis Risk Solutions.

What kind of card is Divvy? Credit card or charge card?

Divvy (now Bill Spend & Expense) is a corporate credit card, which means that payments are made in full shortly after the funds are used.

Is Divvy a line of credit?

As a corporate card, Divvy Bill pend & Expense offers credit, but the terms are not revolving, and used funds must be repaid in full each billing cycle.

Do you have to pay Divvy in full?

Yes, all payments must be made in full, since Bill Spend & Expense does not offer revolving terms.

Is Divvy a Visa or Mastercard?

The Divvy Bill Spend & Expense card is powered by Visa.

What bank does Divvy use?

Bill.com (previously Divvy) issues Spend & Expense cards in partnership with Cross River Bank out of Ft. Lee, New Jersey. The bank was founded in 2008 and is a subsidiary of CRB Group, Inc.

How much money do you need for Divvy?

Your business deposits should exceed $5k per month to qualify for a Bill Divvy card.

What credit score is needed for a Divvy card?

Bill Divvy cards now requires a personal guarantee, so there is a minimum FICO score required for qualification. Authorized signers should have “good to very good” credit to qualify. And, they report accounts to business credit bureaus, so you can build your business credit score with responsible payments.

Does Divvy check your bank account?

Yes. During the application process, Bill.com looks at historical deposits made to your business bank account when determining whether you are eligible for credit. They require a minimum of $5k in monthly revenue.

Can you withdraw money from a Divvy card?

No, you can’t draw a cash advance on a Bill Divvy card, nor can you withdraw funds out of a Bill Spend & Expense account from an ATM.

Takeaway: Should You Get a Divvy Card?

Like all financial offers, Bill Divvy Spend & Expense has its own set of pros and cons. So, if you’re wondering if you should take advantage of the offer, ask yourself the following:

- Does your monthly business spending exceed $5K?

- Does your business employ multiple staff members with spending privileges?

- Are you able to pay your expenses in full each month?

If you answered “yes,” the Bill Spend & Expense credit card could be great for you. I love this card, and do recommend you check it out. So, sign up now to view the credit line you could qualify for.

And, if you’re interested in learning how you can obtain up to $100K in business credit in as few as 30 days, join Business Credit Workshop today.