If you want a way to improve your business’s cash flow while better marketing your business, NAMYNOT’s Net 30 account could be what you need—This option lets you defer payments for up to 30 days, providing more financial flexibility.

Curious about how their Net 30 terms work and how they might benefit your business? Keep reading to find out everything you need to know.

This is what’s in store:

- What is NAMYNOT?

- What is a Net 30 Account?

- NAMYNOT Net 30 Features & Benefits

- How to Qualify for NAMYNOT Net 30

- Final Thoughts

Now, let’s roll!

What is NAMYNOT?

NAMYNOT, aka “nmi,” offers businesses a range of marketing services to support growth and visibility. According to their own marketing message, they focus on clear communication and create strategies that fit each client’s specific needs. Whether you want to strengthen your online presence or reach new customers, NAMYNOT can help with practical marketing solutions.

Here’s a quick look at what they offer:

- Organic lead generation with content marketing.

- Email marketing campaigns.

- Custom marketing strategies, both online and offline.

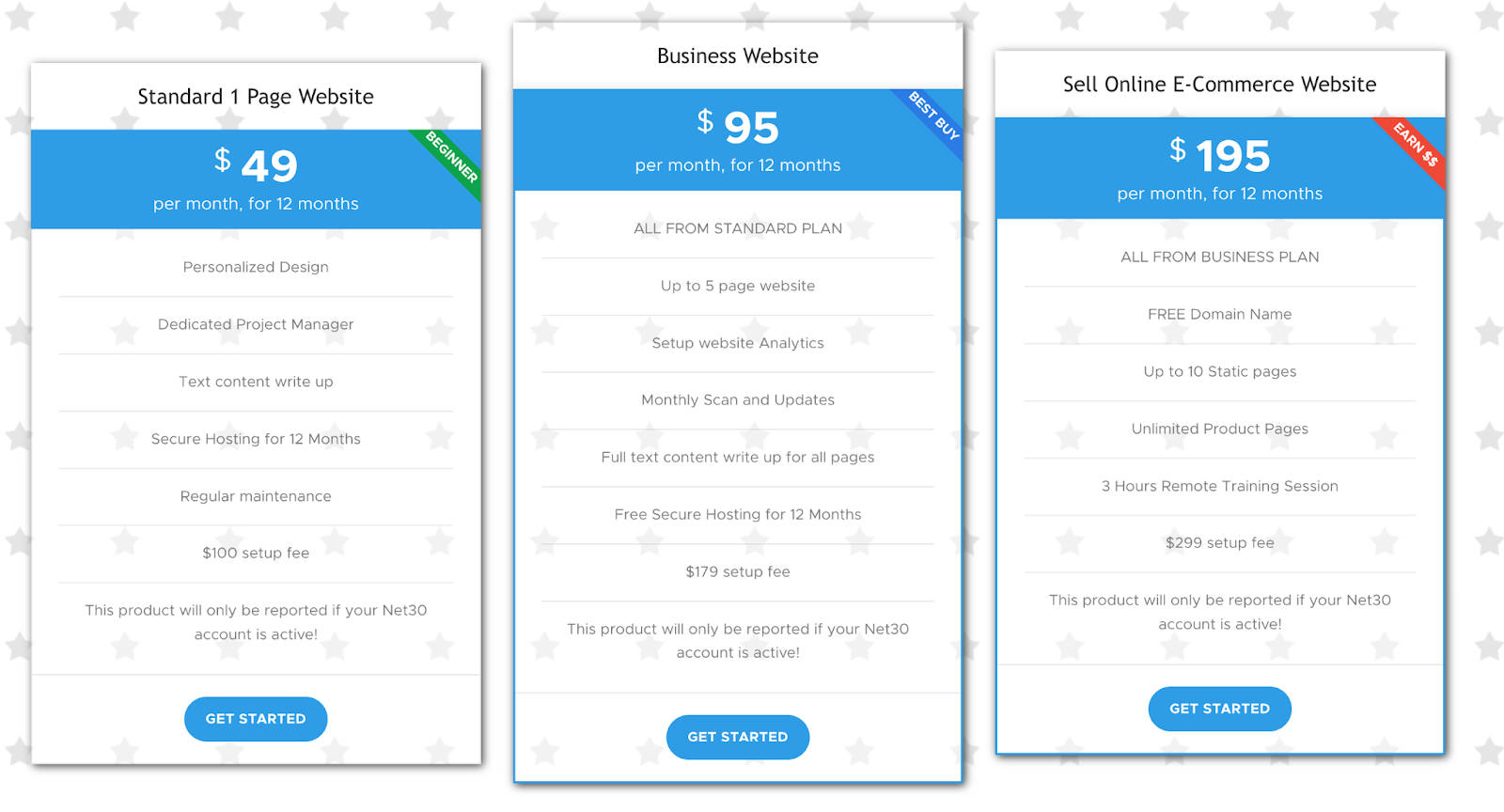

- Professional website design and maintenance.

- Ad management.

With experience across various industries, NAMYNOT works with businesses of all sizes—They provide straightforward, adaptable solutions that can help your business move toward their goals.

And, they offer business bureau reporting, which means that you may be able to have your payments reported to help you establish or improve business credit.

You might also like: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

Company Overview

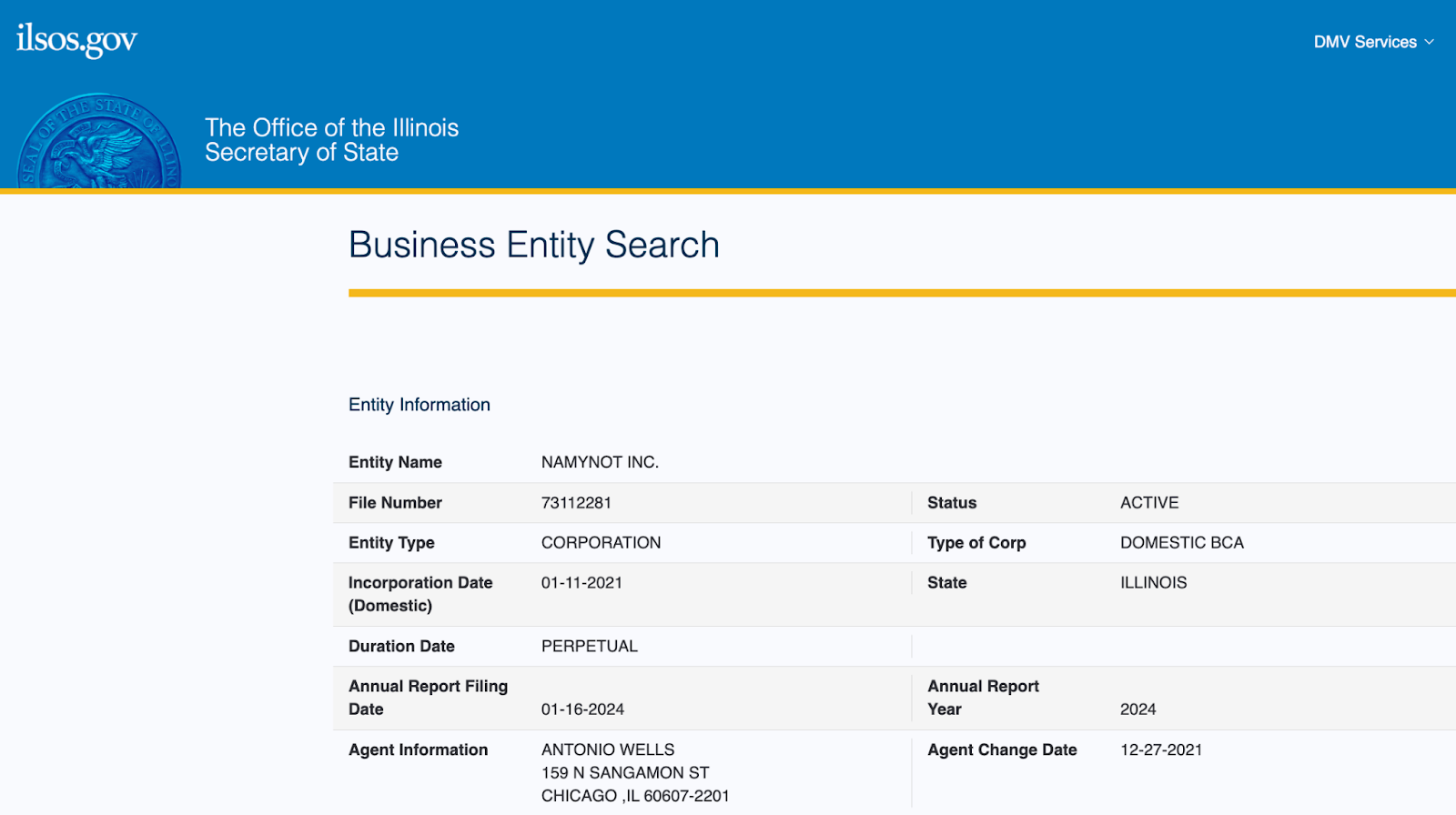

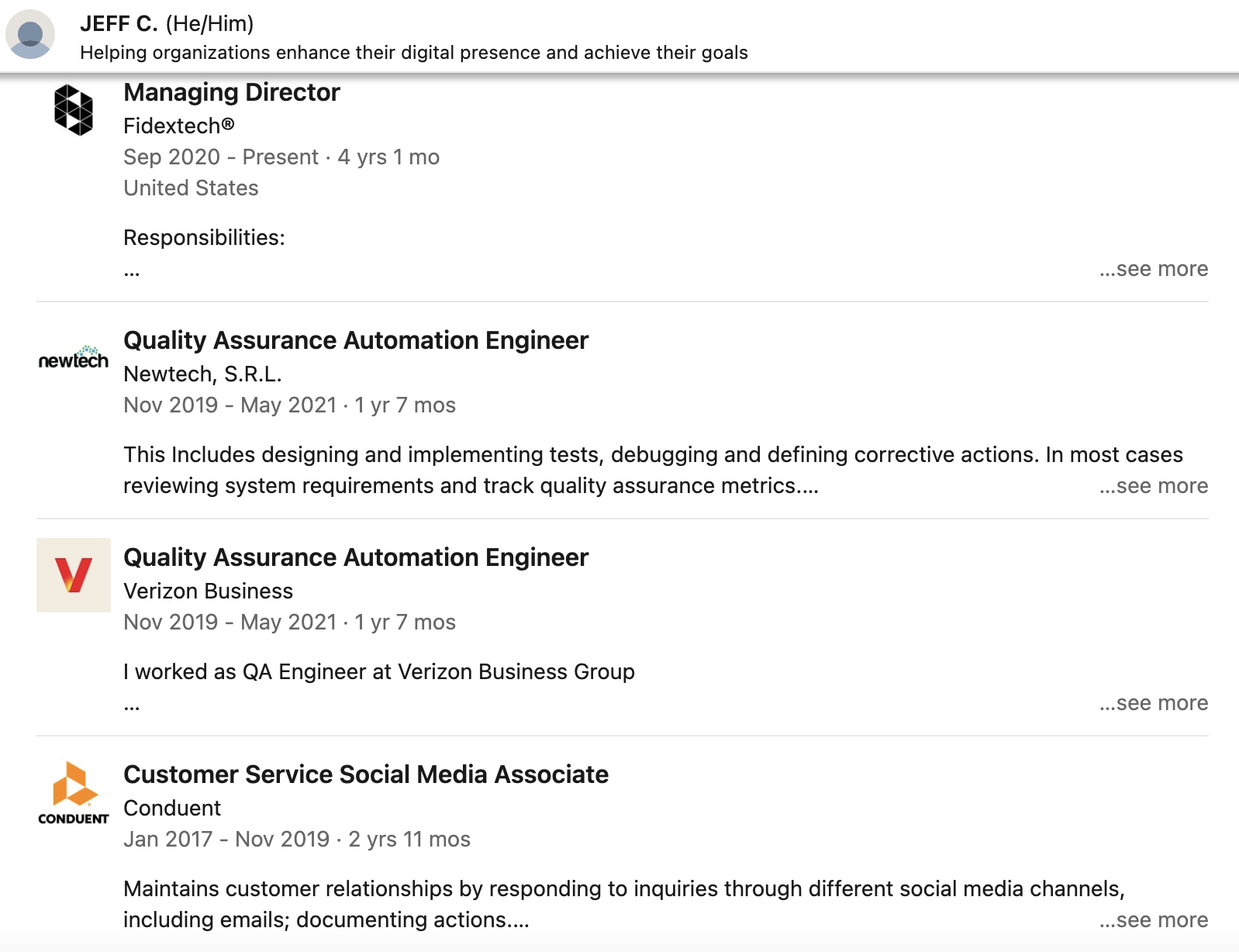

NAMYNOT Inc. is a Chicago-based web services company that was allegedly founded in 1999 (according to Crunchbase) or 2000 (according to LinkedIn) by Antonio Wells. The company is active and in good standing in the state of Illinois, but their incorporation date was in 2021.

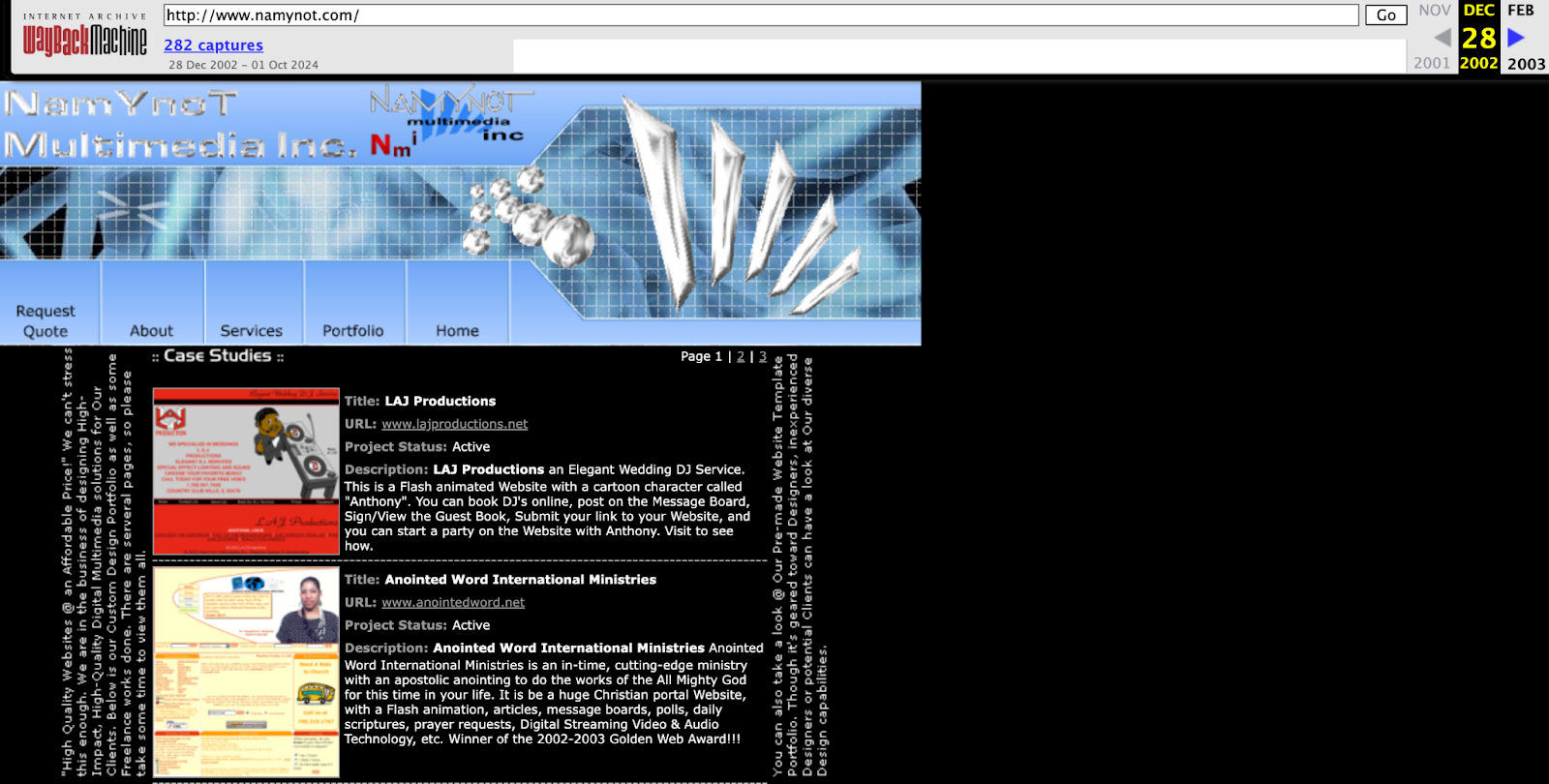

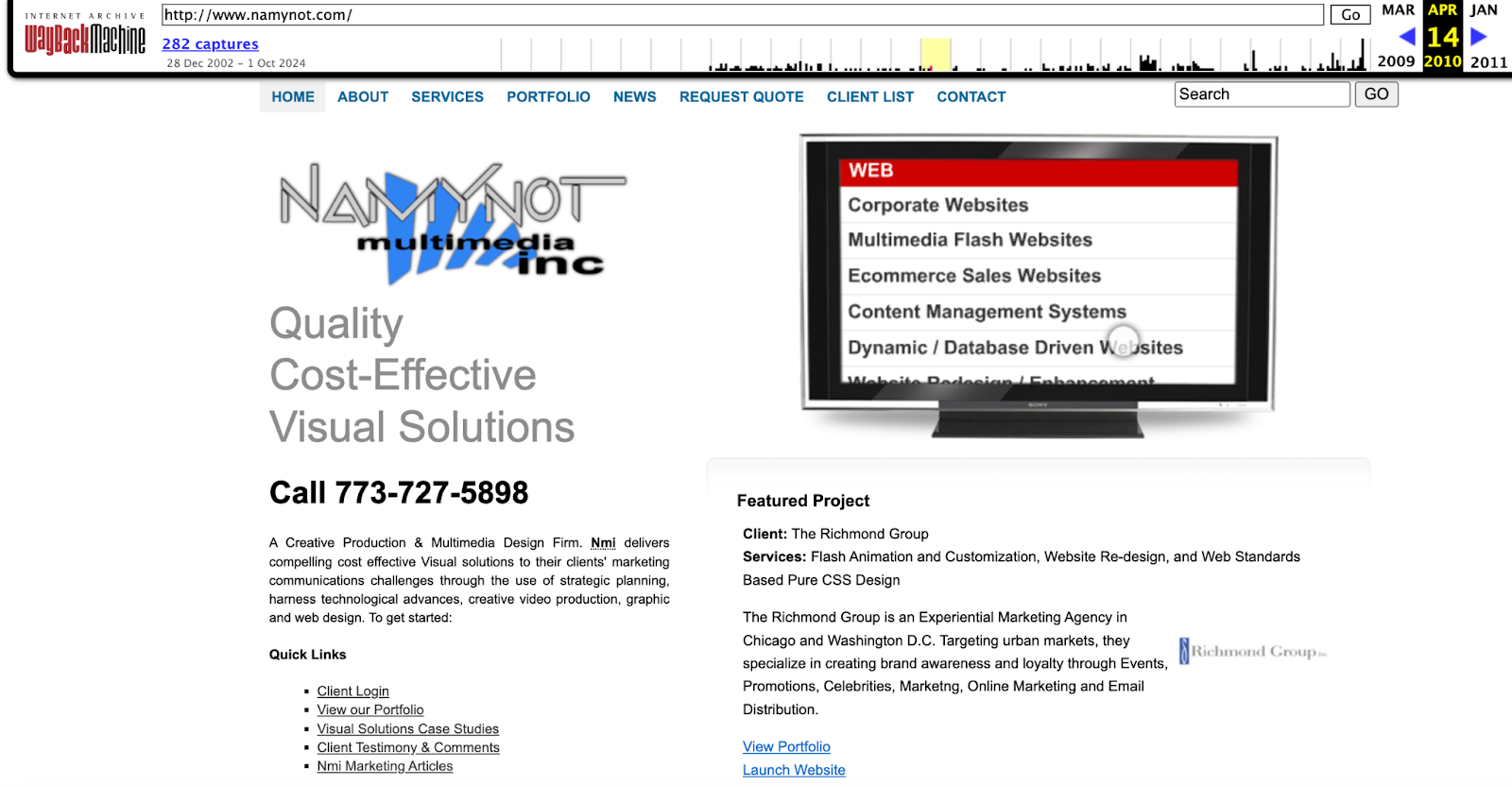

Now, I did find namynot.com in the Wayback machine as early as 2002, which indicates that the company was probably in operation before that time. Based on the homepage screenshot saved over 20 years ago, the brand’s design trends were quite different at that time, with a focus on flash animation web design.

For fun, I popped in to see what NAMYNOT’s website looked like in 2010, and there had been quite an improvement.

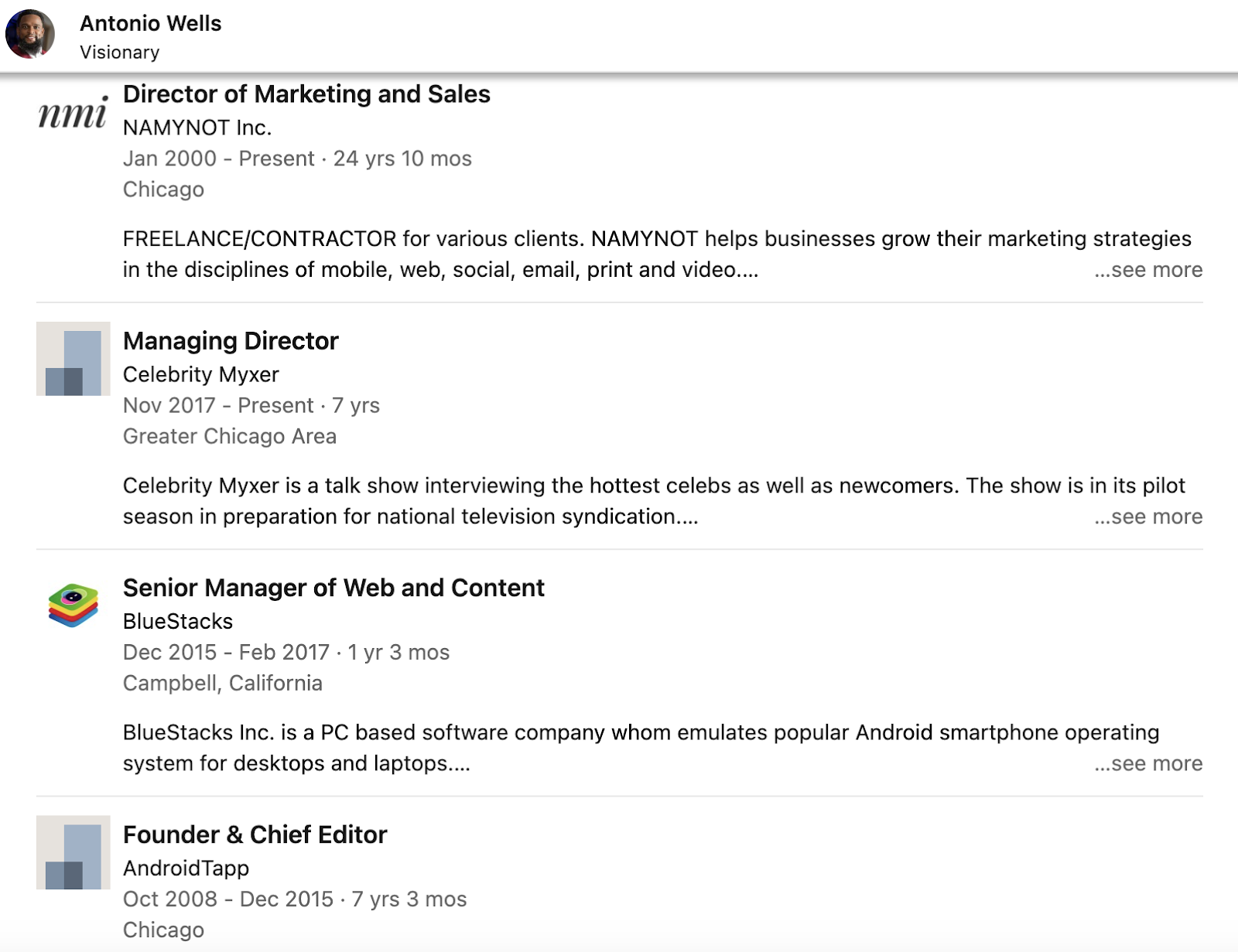

Since the company’s launch, Wells has worn many hats. From 2017 to present, he’s been the Managing Director at Celebrity Myxer. From 2015 through 2017, he served as the Senior Manager of Web and Content at BlueStacks, and he was the Founder & Chief Editor at AndroidTapp for over seven years. It seems he’s an experienced entrepreneur with a focus on marketing. And, NAMYNOT is his longest-standing venture.

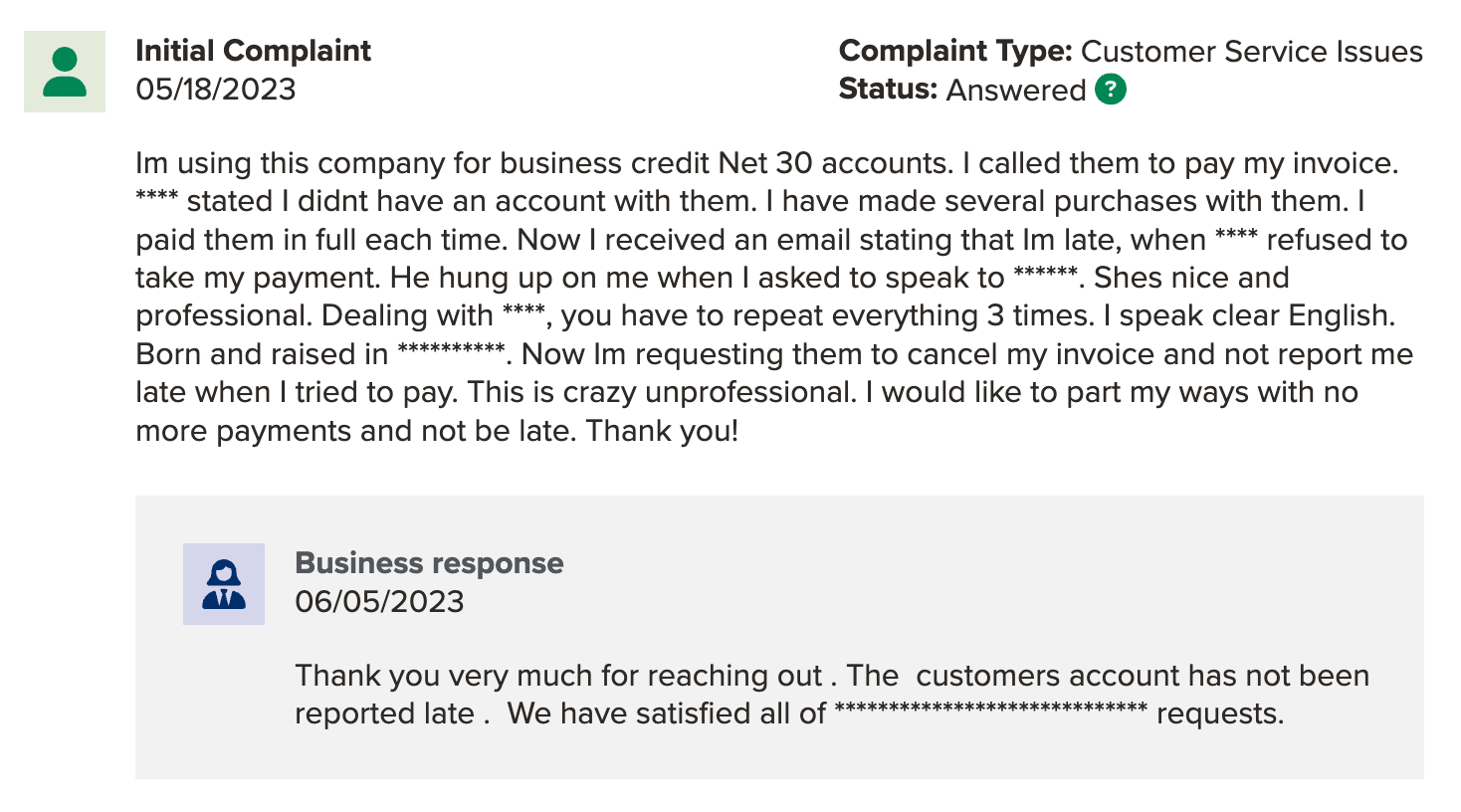

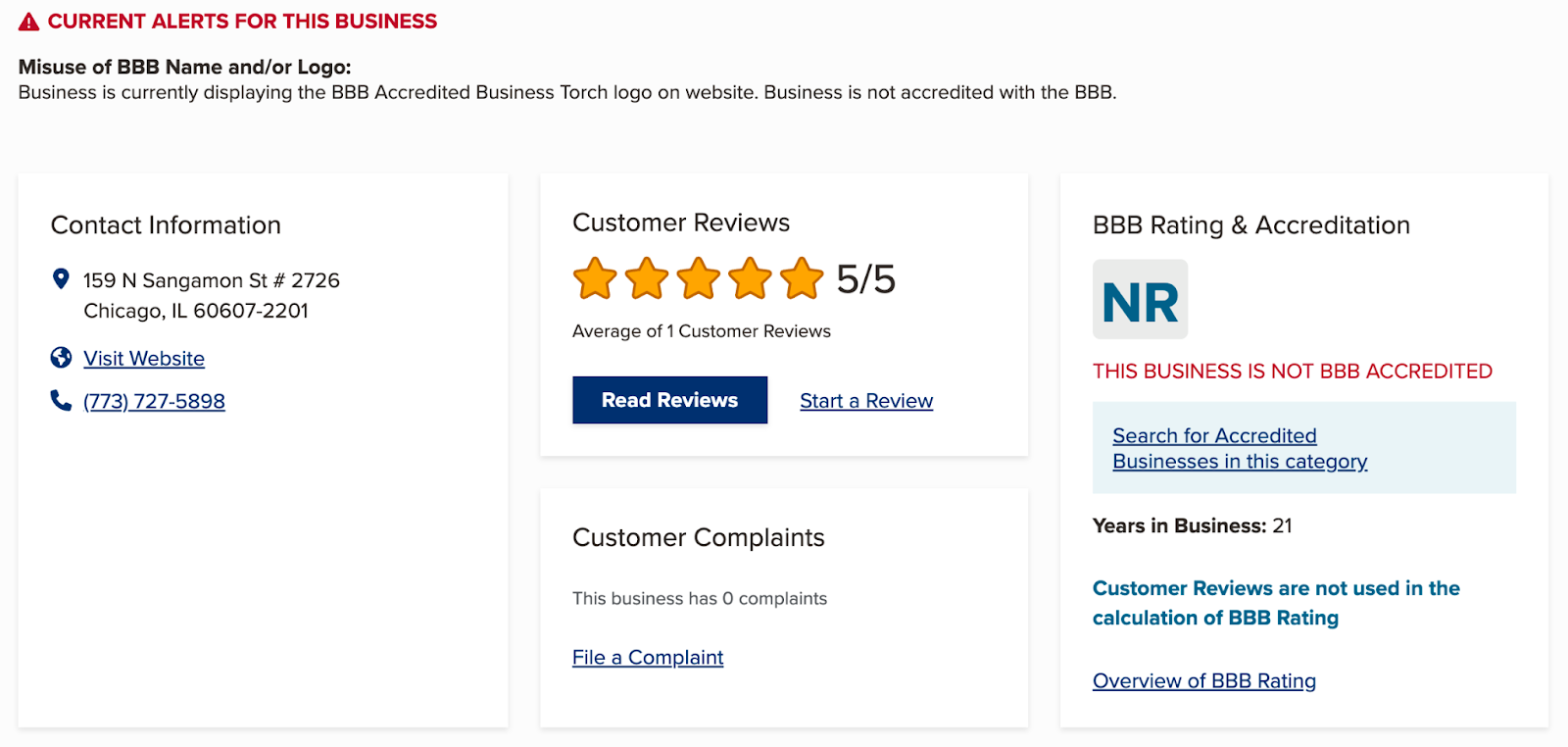

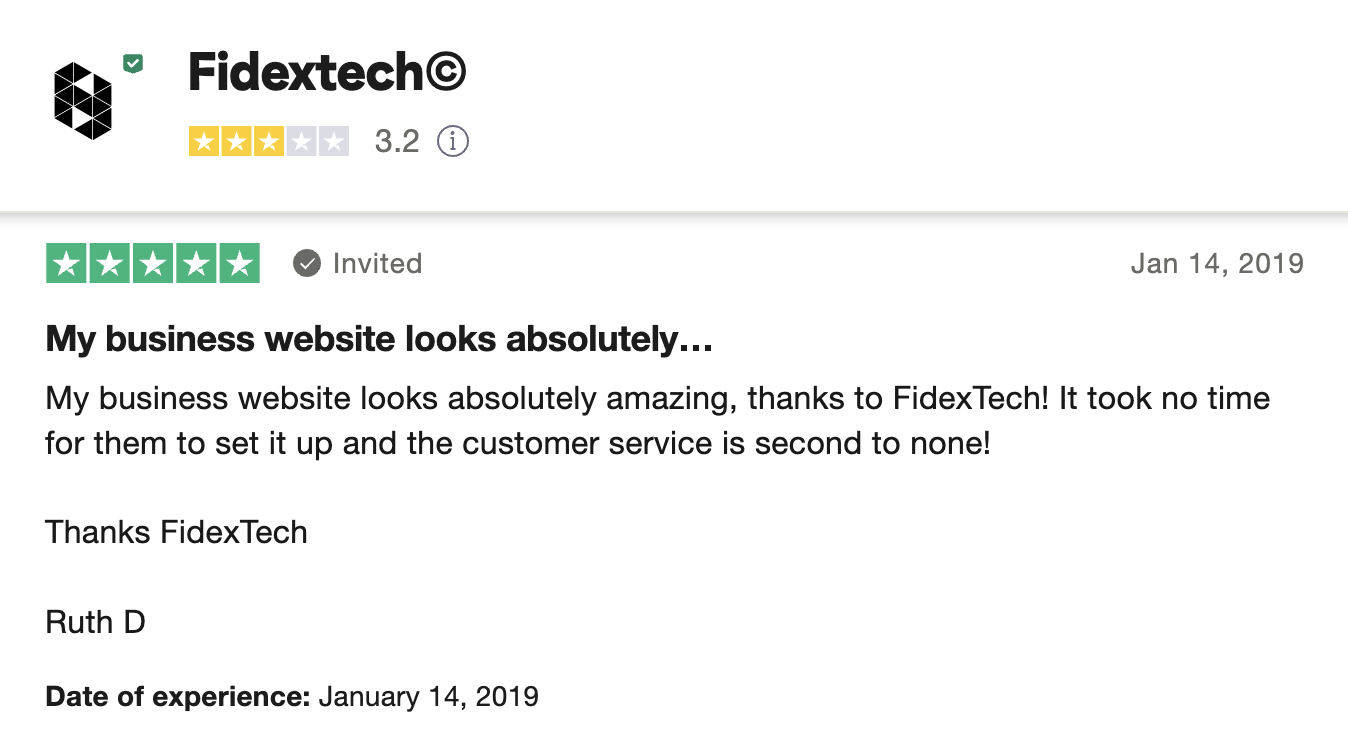

While I didn’t see any past or open lawsuits against the company, the Better Business Bureau (BBB) warns that they misused the BBB brand logo in that they are not accredited with the BBB. Still, they maintain 5-star reviews on the platform.

While I didn’t spend too much time searching for business aliases, I did not see NAMYNOT or nmi listed Trustpilot or Reddit. With a marketing service, this isn’t super alarming, but made me wonder if Wells had been freelancing through another platform to build clientele.

I did find wells on Upwork with 100% job success and great client reviews as far back as 2019. Clients consistently commend Antonio Wells for his SEO expertise, thorough research, and ability to create high-quality content that drives lasting results.

Upwork clients also value his professionalism, clear communication, and strategic insights, often noting how his work positively impacted their businesses. Many clients say that they plan to rehire him, describing him as reliable, knowledgeable, and easy to work with.

So, despite some ambiguity around its founding date and lack of BBB accreditation, the brand maintains a strong reputation. With consistent positive feedback and a focus on marketing, NAMYNOT has quietly built trust and credibility over the years. In short, they’re likely legit.

You might also like: How Can Crown Office Supplies Help You Build Business Credit?

What is a Net 30 Account?

A net 30 account is a type of credit account that gives you 30 days to pay off a purchase after receiving an invoice. It’s pretty common in business-to-business transactions.

For example, if a company buys supplies from a vendor with net 30 terms, they don’t have to pay upfront—they’ll get an invoice and have 30 days to settle it. It helps businesses manage cash flow by giving them more time to pay for goods or services while still keeping operations running smoothly.

And, many contemporary net 30 vendors offer payment reporting to business credit bureaus.

Recommended: How to Use 30 Day Net Vendors to Build Your Business Credit Score

NAMYNOT Net 30 Features & Benefits

Again, NAMYNOT has a net 30 offer that’s worth a look. Here, explore the features and benefits of being approved for their net 30 terms.

1. Pay Later

With NAMYNOT’s net 30 business line of credit, you have the flexibility to purchase digital marketing services now and defer payment for up to 30 days—This means you can invest in essential services, like a website redesign or social media advertising, without immediate financial strain.

For example, if you need to launch a marketing campaign to promote a new product but are short on cash this month, you can use the net 30 option. You can focus on growing your business while managing your cash flow more effectively.

2. Build Business Credit

Timely payments on your Net 30 account contribute positively to your business credit profile. When you pay your invoices on time, your payment history is reported to Dun & Bradstreet (the leading business credit bureau).

This can improve your creditworthiness and open doors to better financing options in the future. As a business owner, you might become able to secure a higher credit line or more favorable loan terms, which makes it easier to fund your growth ambitions.

Recommended: Everything You Need to Know About a DUNS Number – and Why You Should Care

3. No Personal Guarantee Required

One of the significant advantages of our Net 30 account is that it does not require a personal guarantee or a credit check. This feature protects your personal credit score and separates your business finances from your personal finances.

For instance, if your business faces a financial hiccup, your personal assets remain safe. This can give you peace of mind as you focus on running and scaling your business.

You might also like: Here’s How to [Actually] Get Business Credit With Just an EIN +More

4. Up to $10K Credit Line

You can qualify for a credit line of up to $10,000, giving you ample resources to invest in your business. Whether you want to launch a new marketing initiative, hire freelance talent for a project, or upgrade your office equipment, a credit line can give you the flexibility you need.

Imagine having the capital to execute a comprehensive digital marketing strategy without immediate cash outflow—this could significantly boost your business visibility and sales.

You might also like: What is the Best Credit Card for Ad Spend? Expert Insights

5. Easy Application Process

Applying for a Net 30 account is straightforward and free of charge. This means you can get access to critical funding without the burden of complicated applications or hidden fees. The streamlined process allows you to focus on what matters most—growing your business.

Once your application is approved, you can start using your credit line almost immediately, which enables you to act quickly on new business marketing opportunities.

You might also like: Free, Printable Business Credit Application Template (+How to Use it)

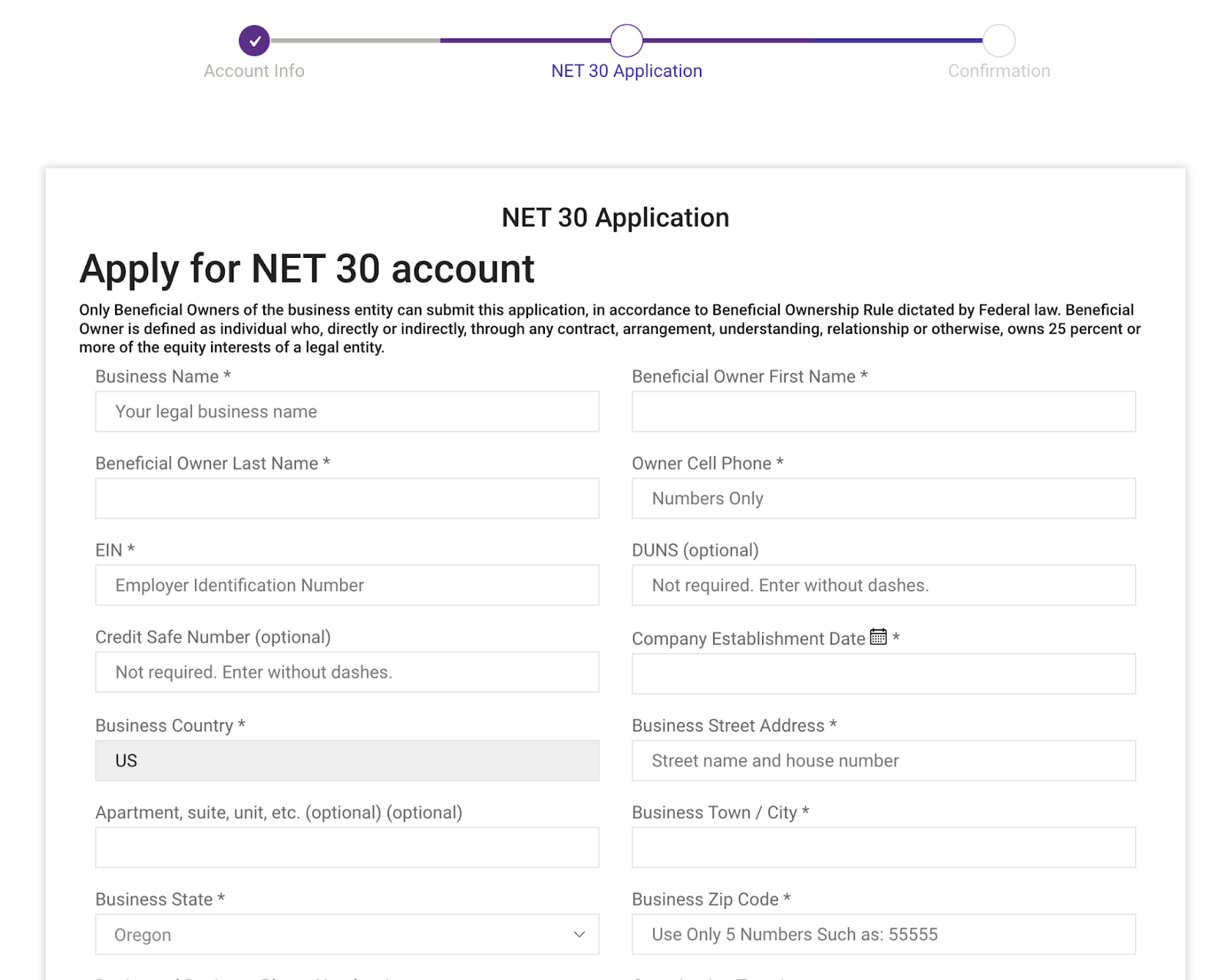

How to Qualify for NAMYNOT Net 30

To qualify for a NAMYNOT net 30 account, make you meet the following requirements:

- You own a profitable, U.S.-based business.

- Your business is active and was registered at least 90 days ago.

- You want to take advantage of NAMYNOT’s services.

- You own at least 25% of the business.

- Your business has an EIN and a DUNS Number.

- No past, negative payment history has been reported about your business.

- You have a professional website.

If you run a profitable business, have the title of Authorized Officer, and meet all the above requirements, you can confidently apply for a NAMYNOT Net 30 account.

Note: If you don’t yet have a professional website, NAMYNOT might be able to help.

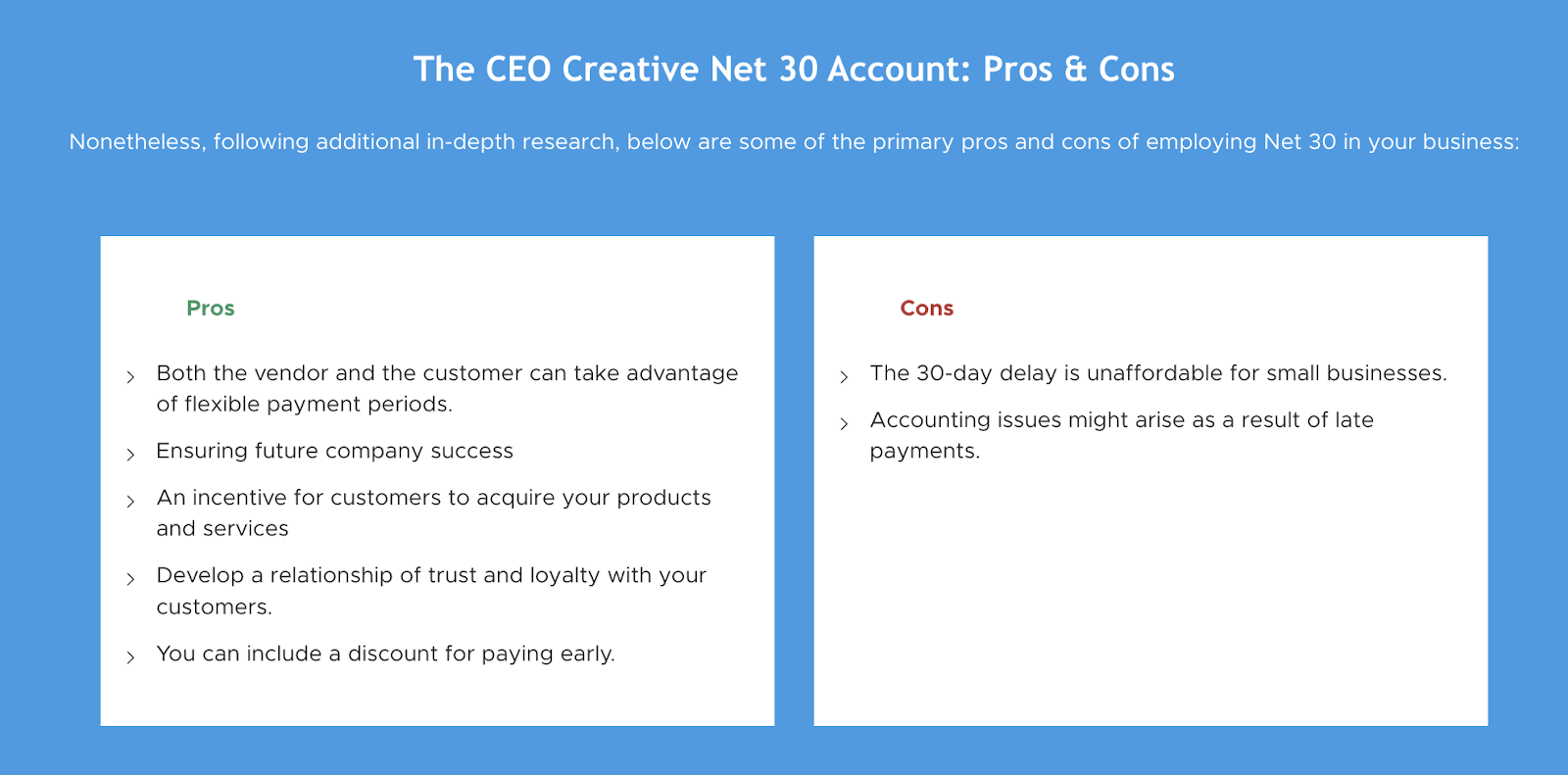

You might also like: The CEO Creative Net 30 Review: Is it Worth Your Time?

Final Thoughts

NAMYNOT offers marketing services alongside a net 30 payment option, which can help you manage cash flow while investing in your business. Whether you need digital marketing, a website redesign, or want to build your business credit, their flexible terms can help without the pressure of upfront payments.

With an easy application process, no personal guarantee, and credit lines up to $10K, NAMYNOT’s Net 30 option could be a practical choice if you’re looking to expand your marketing efforts. What do you think?

Do you wanna learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!

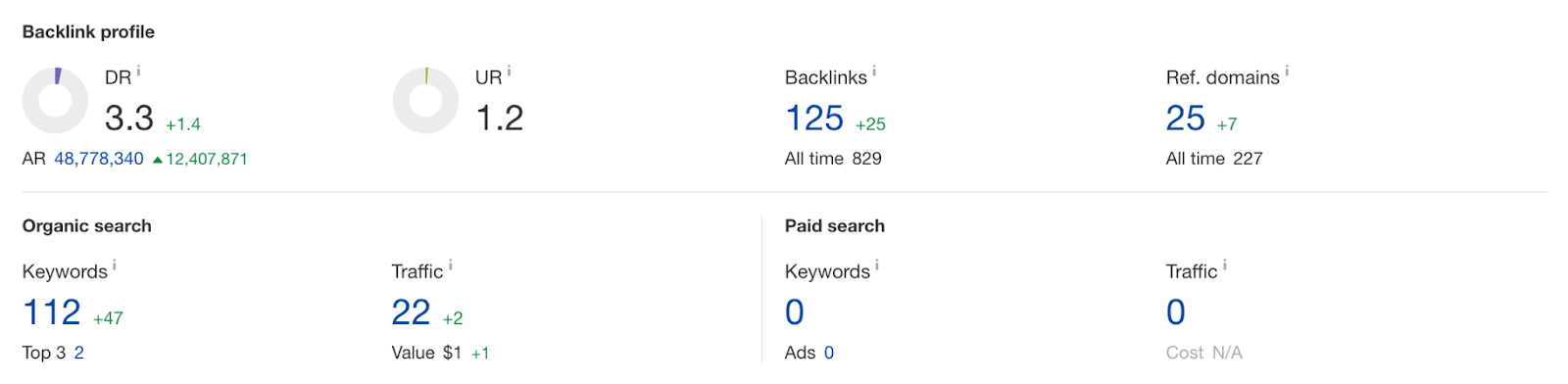

The lower Domain Rating of Fidextech’s website (3.3 out of 100, according to Ahrefs) suggests that they may not have so-called “expert” SEO marketing skills. Or, to be fair, maybe they don’t implement their skills to the fullest for their own brand…

The lower Domain Rating of Fidextech’s website (3.3 out of 100, according to Ahrefs) suggests that they may not have so-called “expert” SEO marketing skills. Or, to be fair, maybe they don’t implement their skills to the fullest for their own brand…