Since the Great Recession of 2008, small business owners have had a difficult time securing financing, and that’s made it nearly impossible for many to to start or grow a business. As a result, many alternative financing companies have popped up, but unless you take precautions, you can end up paying exorbitant amounts of interest with these types of loans. Luckily, the Small Business Administration (SBA) is still in the market of helping entrepreneurs and small business owners get the cash they need.

Since the Great Recession of 2008, small business owners have had a difficult time securing financing, and that’s made it nearly impossible for many to to start or grow a business. As a result, many alternative financing companies have popped up, but unless you take precautions, you can end up paying exorbitant amounts of interest with these types of loans. Luckily, the Small Business Administration (SBA) is still in the market of helping entrepreneurs and small business owners get the cash they need.

But in order to be successful with an SBA loan application, you must understand the process and have a firm grasp of the steps you’ll need to take. Here’s a breakdown of the entire process.

What Role Does the SBA Play in Lending?

It’s important to note that the SBA doesn’t actually grant loans to businesses, but instead guarantees most of the loan (75-85 percent) to the lenders who do. Because of this guarantee, lenders have less risk so they are typically able to relax their loan guidelines and extend lower interest rates. The SBA currently works with about 500 banks in the U.S. that lend to small businesses. When looking for an SBA small business loan, it makes sense to start with your local bank if you have a good relationship with someone there, and ask if they’re an SBA lender. If not and you need to expand your search, the SBA offers a lender search tool and a current list of the top 100 most active SBA lenders in the country.

What Types of Loans Does the SBA Guarantee?

No two businesses are the same—they vary in size, years in business, and financial obligations and needs. In order to support all types of businesses, the SBA backs three specific types of business loans.

- Basic 7(a) Loan Program. If you’re just starting a business, plan to purchase one, or are expanding your current business, this is the loan you should apply for. It’s the most common of the loan programs offered by the SBA. You can find out more information about these types of loans by visiting the SBA’s general loan page.

- Microloan Program. If you need $50,000 or less to start or grow a business, a microloan will likely fit your needs. These loans are made by nonprofit community lenders, but are backed by the SBA. Borrowers typically need collateral in order to secure these loans, and many lenders ask for a personal guarantee from the business owner. The typical microloan amount is $13,000. You can learn more about microloans on the SBA microloan program page.

- Certified Development Company (CDC) 504 Loan Program. The CDC 504 Loan Program offers loans to business owners who need to purchase fixed assets in order to expand or modernize their business. Its goal is to promote economic growth in communities across the country. Find out more on the SBA website.

What are the Eligibility Requirements to Get an SBA Loan?

While the above types of loans can apply to most business owners, the SBA has certain requirements that generally must be met in order to qualify for a loan. For instance:

The business must be small and operate to make a profit.

The business must be small and operate to make a profit.- You must do business in the United States.

- Personally invest a reasonable amount of equity in the business.

- Utilize other financing methods, such as using your personal assets, before applying for the loan.

- Demonstrate a need for the loan and use the loan proceeds for a sound business purpose

- Not be delinquent on any debt obligations to the U.S. government.

Check Your Credit Reports before You Apply

Once you’ve determined the type of loan you want to apply for and confirmed that you meet all the eligibility requirements, it’s time to begin the process of applying for your loan.

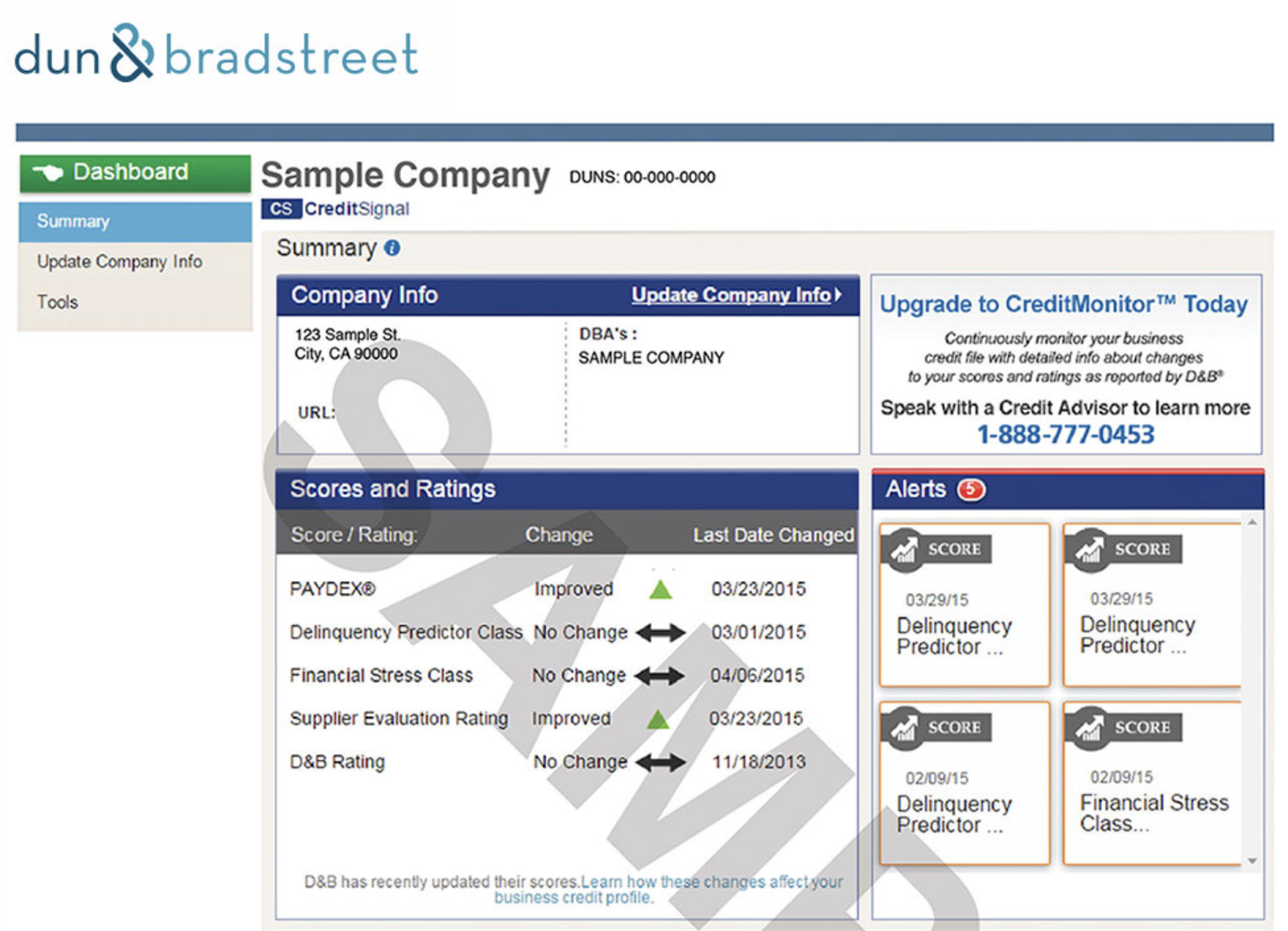

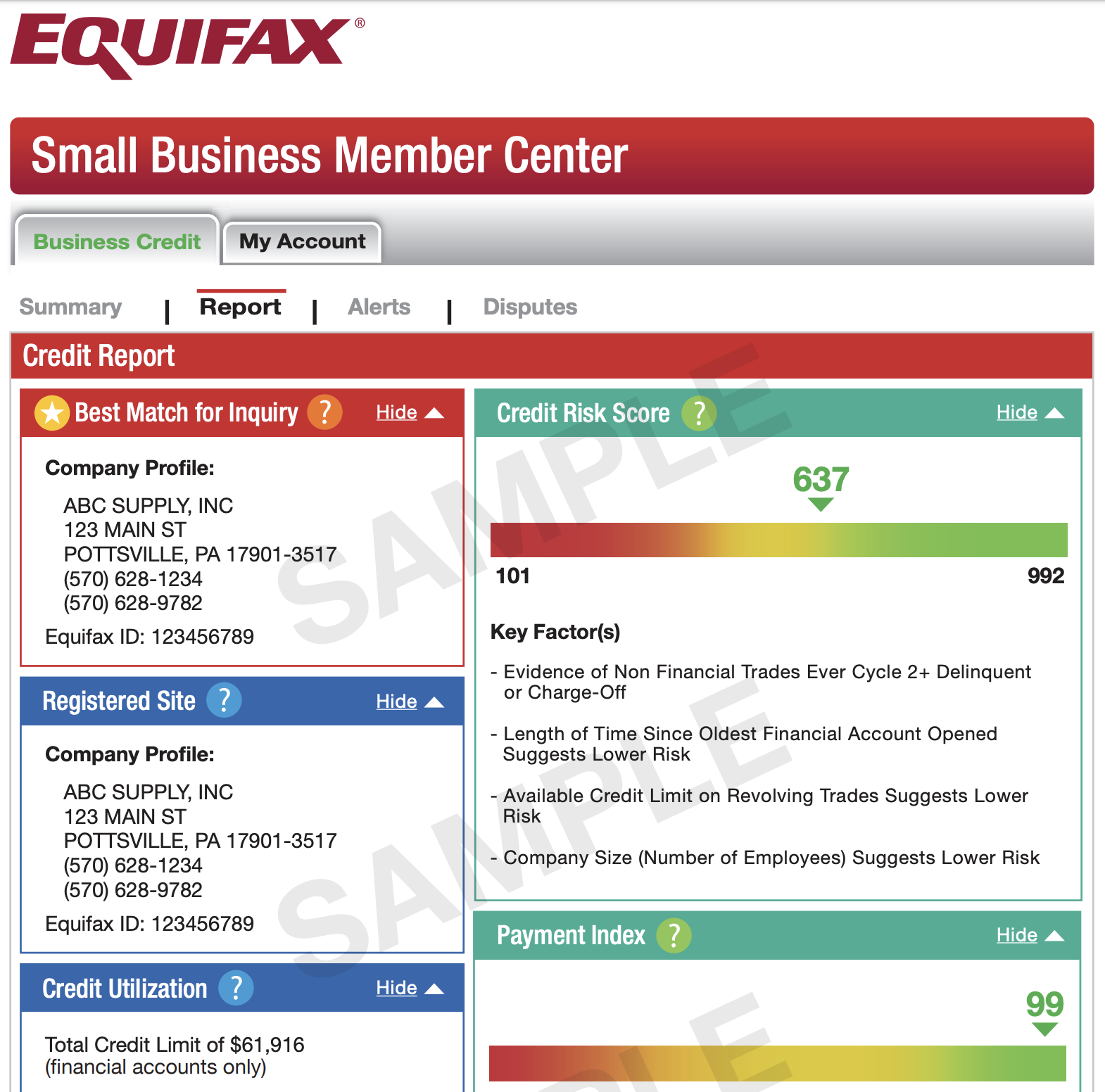

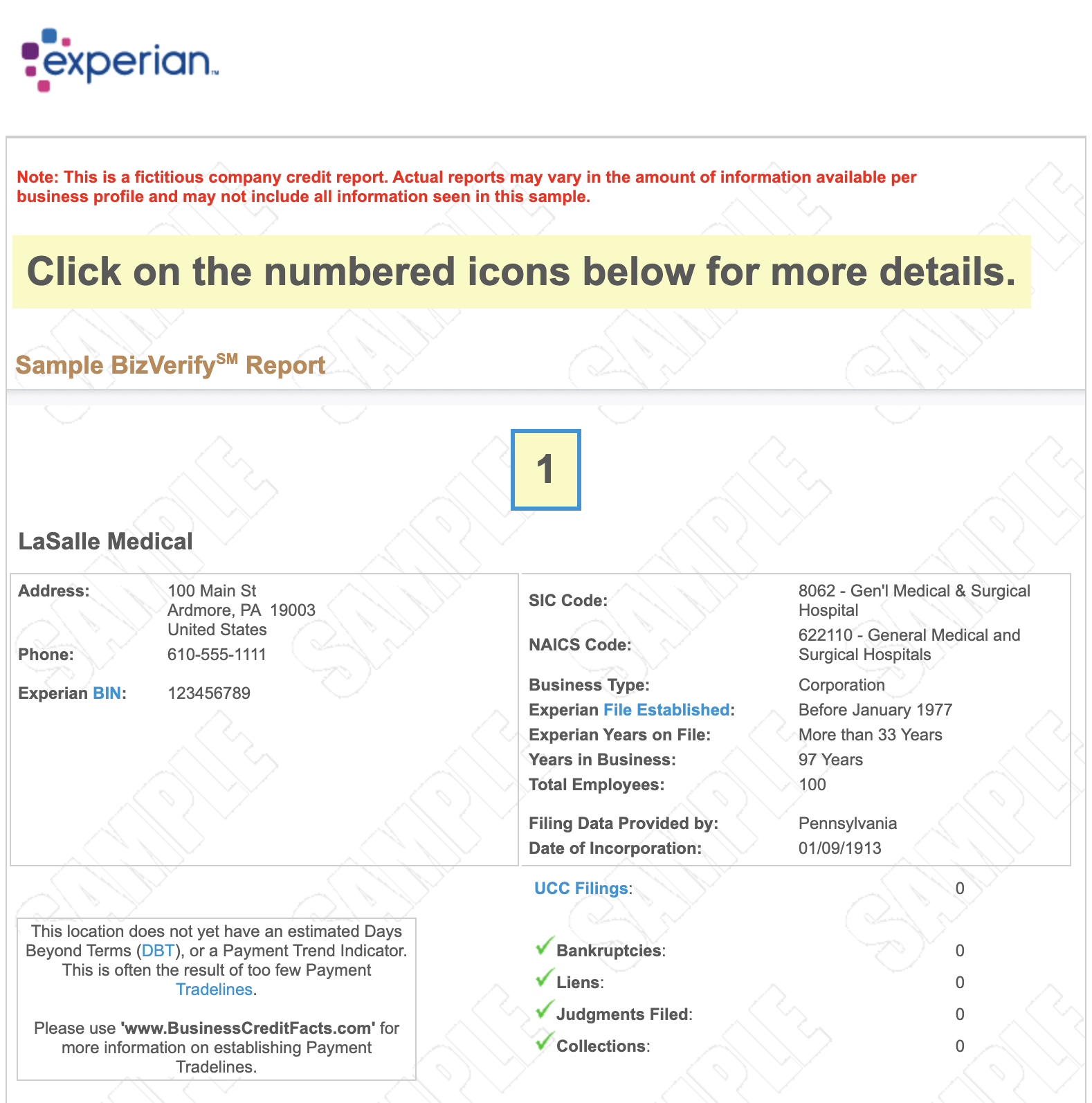

When you apply for an SBA backed loan, the lender will ask to see both your personal and business credit reports. Before you begin the loan process, it’s wise to request copies of your report so you can clear up any inaccuracies before the lender sees them. Although the reporting agencies have great systems in place, sometimes mistakes happen and errors can end up on your report, which could hamper your ability to get a business loan. You can get copies of your personal credit report for free from all three reporting agencies, and you can purchase your business credit profiles from Dun & Bradstreet, Experian, and Equifax. In order to understand the process of checking your business credit profiles, read our post on the subject.

What Documentation Do You Need to Apply for an SBA Loan?

Next, you’ll need to gather all the documents you’ll need in order to submit your application to the lender. Not every lender requires the same information, but in general, here’s what you’ll need to provide:

- Personal background information. The lender will ask you to provide personal information for each partner, such as former addresses, other names used, criminal histories, and educational backgrounds.

- The personal and business credit histories for every owner of the business.

- Many lenders ask for at least one year of bank statements.

- Expect to provide the lender with a minimum of three years of income tax returns.

- Depending on how your business is structured, a lender may ask you to provide certain legal documents, such as business licenses or certifications, articles of incorporation, ongoing contracts with third parties, commercial lease contracts, and franchise agreements.

- You’ll need to provide the lender with a thorough and well thought out business plan. Your plan should include all of the typical components, such as an executive summary, company overview, product or service description, market and competitor analysis, marketing plan strategy, organization and management team, and your financial plan for the business.

- The lender will also want to see projected financial statements and cash flow projections for at least one year, as well as your personal and business financial statements.

- Most lenders will ask for a personal guarantee from you and your partners, especially if they own more than 20 percent of the business.

- If you’re starting a new business, the lender may ask for a resume for you and any partners to judge your experience in relation to the business you plan to start.

- If the lender requires collateral, you will be asked to provide a collateral document that outlines the details of the personal or business property you intend to use to secure the loan. You’ll need to provide the value of the items.

There are many forms to fill out with an SBA Loan, since it’s government backed financing!

Fill out the Required Lender Forms

Next, you’ll be asked to complete some documentation for the lender in order for your loan to be processed. The forms you’ll be asked to complete are:

- Application for Business Loan. This is the main loan document, and you will have to provide many attachments to complete it.

- Schedule of Collateral. This document details the personal assets you plan to use as collateral.

- Statement of Personal History. The lender will use this form to evaluate your character.

- Personal Financial Statement. The lender will use this form to evaluate your financial health.

- Fee Disclosure and Compensation Agreement. If you hired someone to help you submit your SBA loan application, you’ll need to fill out this form and state how much you paid for those services.

Don’t Be Afraid to Ask for Help

Although applying for an SBA loan comes with less stringent requirements than with a traditional lender, the process can be cumbersome. If you need help with the process, the SBA partners with a variety of organizations that can walk you through the process.

- This is a national organization that provides counselors, mentors and advisors to small business owners free of charge. Visit this page to find a SCORE office near you.

- Small Business Development Centers (SBDCs) offer free business consulting services and low cost training to aspiring entrepreneurs. There are about 900 locations nationwide. You can find a list of them by state on the SBA website.

- SBA District offices. You’ll find at least one of these in each state, and they can help guide you through the loan process. Visit this page to find an office located in your area.

- Women’s Business Centers (WBCs). There are over 100 of these centers across the country, and they exist to help women who are starting or running a business. You’ll find a state-by-state list on the SBA website.

Applying for SBA financing is just like any other loan application process—you’ll need to be prepared and armed with the facts in order to convince the lender you’re a good candidate for a loan. Do some preliminary work before you begin the application process, such as checking your credit reports and gathering the documentation you need, and you’ll be one step ahead of the game. And don’t forget, in today’s economy with so many banks refusing to lend to business owners, SBA loans can be your ticket to a brand new business or an expansion of your current one.

When searching for the best business credit cards for your small business, it is crucial to be aware of what is currently happening right now in today’s business lending environment. Frequently, advice offered today is no longer valid in many aspects of current business because so much has changed from years ago in the business lending environment. Even six months can make a difference in the world of business lending and the best routes to take. For example months ago, it was suggested to visit Bank of America for unsecured business loans of credit if you are trying to get a new business started. However, this is only a valid option today if you have an established business that can show income verification (tax returns) from the past two years or more.

When searching for the best business credit cards for your small business, it is crucial to be aware of what is currently happening right now in today’s business lending environment. Frequently, advice offered today is no longer valid in many aspects of current business because so much has changed from years ago in the business lending environment. Even six months can make a difference in the world of business lending and the best routes to take. For example months ago, it was suggested to visit Bank of America for unsecured business loans of credit if you are trying to get a new business started. However, this is only a valid option today if you have an established business that can show income verification (tax returns) from the past two years or more.

Best Regards,

Best Regards,