I ran across United Capital Source’s offer, which appears to be pretty popular in the business community. While I typically don’t recommend offers in this branch of finance (call me biased), I know that tons of business owners want to know if they should trust this company.

Here, I’ll help you find out — We’ll explore the offer in-depth, including company leadership and the features and benefits of United Capital Source’s funding products. I’ll direct you to some closely-related and not so closely-related offers and answer some common questions.

This is what’s in store:

- What is United Capital Source?

- Features & Benefits

- United Capital Source Alternatives

- United Capital Source Alternatives

- Frequently Asked Questions

- Conclusion: Is United Capital Source Legit?

Let’s go!

What is United Capital Source?

United Capital Source is a financial service that caters to small and mid-sized businesses – they dish out a variety of funding options including business lines of credit, term loans, and more.

Their website boasts a breezy application process, promising quick approvals and funds in just a few days for most programs. Apparently, business owners can snag up to $5 million in financing, and what’s cool is you get to choose between secured and unsecured options without having to throw in a personal guarantee.

However, it’s important to note that most of the funding offered by United Capital Source is considered alternative:

- Invoice receivables

- Merchant cash advances

- Working capital loans

- Equipment financing

- Revenue-based business loans

This means that they are not subject to usury laws because they are not technically “loans.” It’s like this: you’re selling the money you expect to get in the future for a bit less cash right now. This setup is often seen as a factoring deal.

Hence, the “factor rates” can be equivalent to 100% to 150% or higher interest rates – I never recommend this type of financing unless you are in a bind and have no other possible solution.

Still, United Capital Source claims to have hooked up funding for over $1.2 billion to small businesses, which is no small feat. Just keep in mind, as with any financial offer, it’s wise to dive into the nitty-gritty of the company and terms and conditions before you hitch your business to their funding train.

So, let’s do just that.

Recommended: This is How to Leverage Business Credit to Transform Your Life

United Capital Source Company Overview

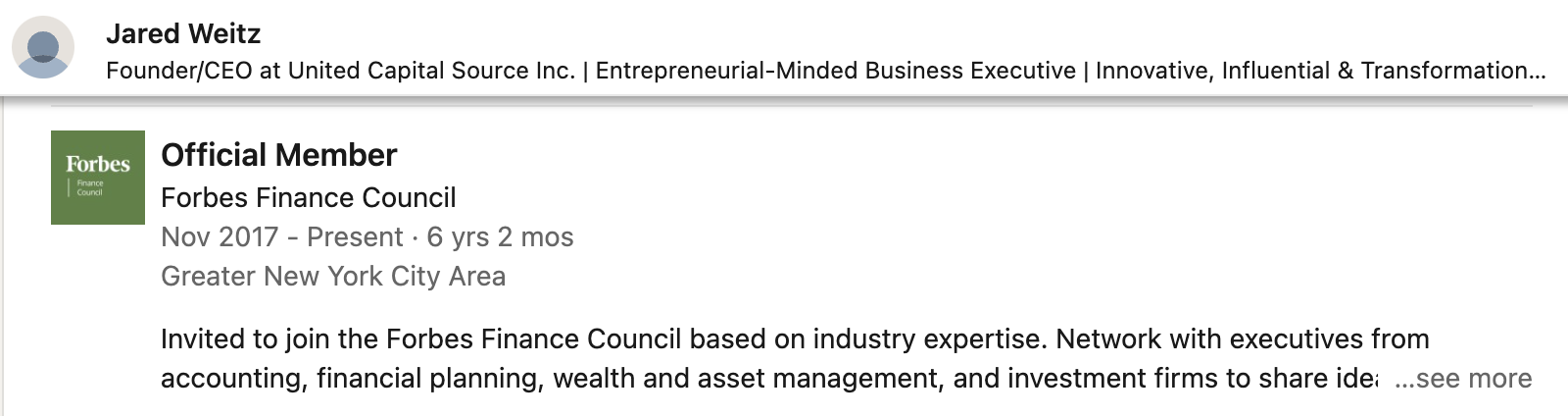

With a home base in New York, United Capital Source Inc. was founded by Jered Weitz in 2011. Weitz is the current owner and CEO of the company.

In addition to his role at United Capital Source, Weitz is a co-chairman of the Small Business Finance Association and an official member of Forbes Finance Council (both credible organizations).

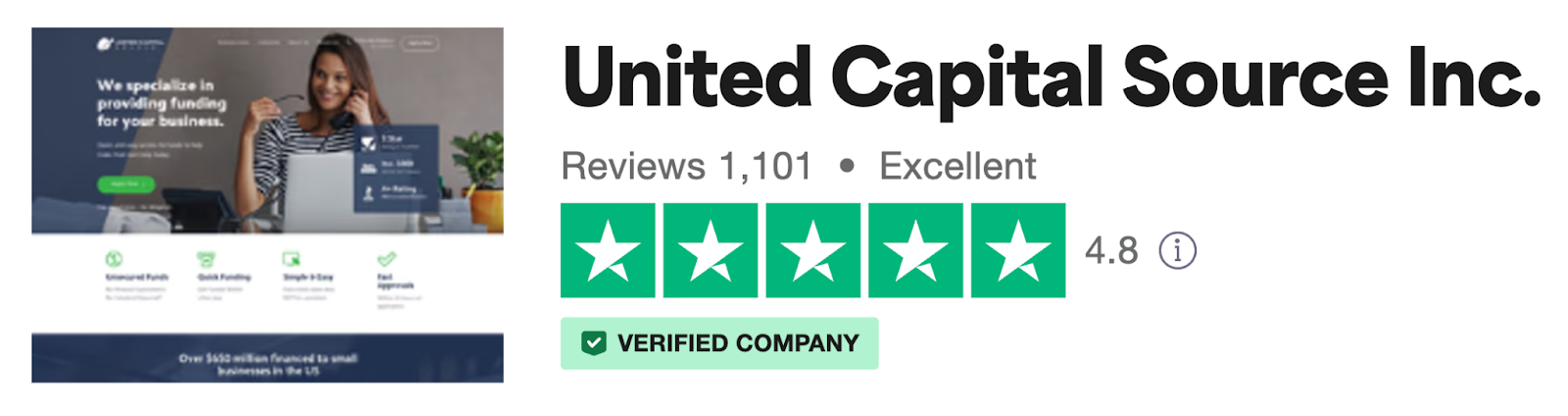

Despite a couple of complaints from unsatisfied business owners, United Capital Source maintains an A+ rating with the Better Business Bureau.

The company website showcases a solid 5-star Google rating with heaps of positive reviews that highlight efficient service and helpful reps like Matt Weimann and Sean Hutchinson – Since it’s not easy to trust brand advertising, I like to turn to Trustpilot and Reddit for more unbiased reviews.

And, since most Redditors advising on financial offers don’t recommend any type of factoring, I turned to the users posting on Trustpilot. Surprisingly, United Capital Source has maintained a 4.8-star rating on the platform (very impressive for any financial offer).

Keep in mind that, while Trustpilot aims to maintain an accurate overview of every company on the platform, no online reviews are 100% reliable. Still, in this case, I find the 4.8 star rating to be reasonable since other ratings for United Capital Source tend to be in the same range.

What Does United Capital Do?

Is this the moment you’ve been waiting for? Either way, take a look at a breakdown of the features and benefits you can expect from United Capital Source funding (so you can figure out if this is the right funding for your business). From their factor rates to speed of funding and beyond, here’s what the offer is all about.

1. Competitive Factor Rates

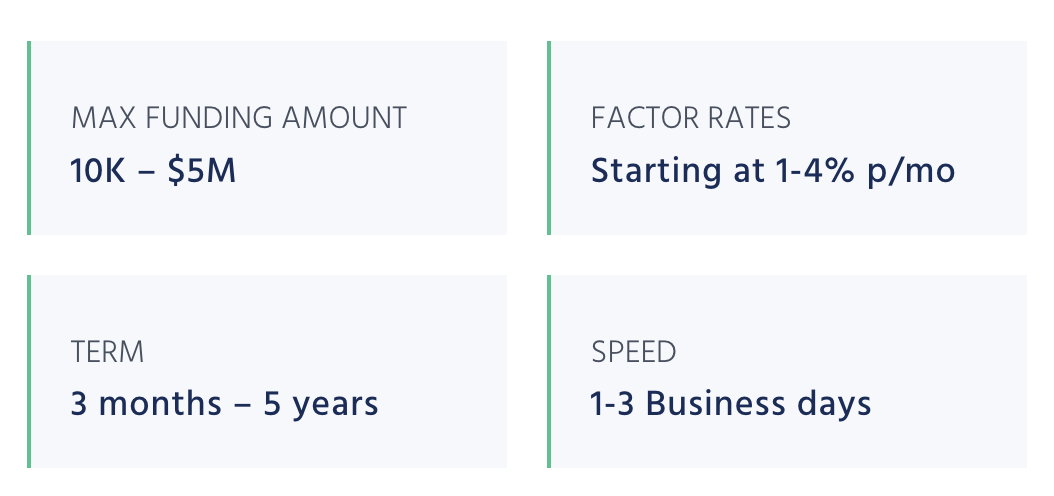

First off, United Capital Source offers factor rates as low as 1% (on their business lines of credit), which is competitive in the factoring realm. But, let’s put this number into perspective.

If you’re looking at a $5,000 loan with a 1% monthly factor rate, paid off over 6 months, the total cost would be calculated by multiplying the factor rate (1%) by the loan amount ($5,000) for each month. So, for the first month, it would be $50. Over six months, you’d end up paying $300 in fees.

Now, for a $50,000 loan with the same 1% monthly factor rate over 6 months, the fees would be higher at $500 per month, totaling $3,000 over the loan term.

To put this in perspective, let’s compare it with a traditional business loan with an 11% annual interest rate — The interest on a $5,000 loan over 6 months would be significantly lower than the factor rate, costing approximately $275. For the $50,000 loan, the interest would amount to around $2,750.

Plus, not all borrowers will qualify for the lowest factor rates – United Capital Source’s factor rates are typically 1.1% to 1.5%, which means you’ll likely pay even more than the examples above.

While factoring can provide quick access to funds, it usually results in higher overall costs compared to traditional business loans with lower interest rates – Carefully consider your financial situation and weigh the pros and cons of each financing option before you make a decision.

You might also like: Shopify Capital Review: What are the Benefits & is it Worth it?

2. Quick & Easy Access to Cash

United Capital Source prides itself on providing swift and hassle-free approvals for business owners in need of financial support — Their online application process is designed for efficiency, allowing businesses to submit their information quickly and easily.

So, you can get from $10K to $5M in a short time.

The emphasis on quick approvals is particularly beneficial for businesses that face urgent financial needs or time-sensitive opportunities. By streamlining the approval process, United Capital Source aims to provide you with timely access to funds, which can enable you to take the next step in your operations without unnecessary delays.

However, you need to review the terms and conditions carefully to ensure that the funding solution aligns with your specific requirements and financial goals — As a matter of fact, do this before you accept any financial offer.

You might also like: 6 Best Fintech Credit Cards to Apply for (Consumer & Business)

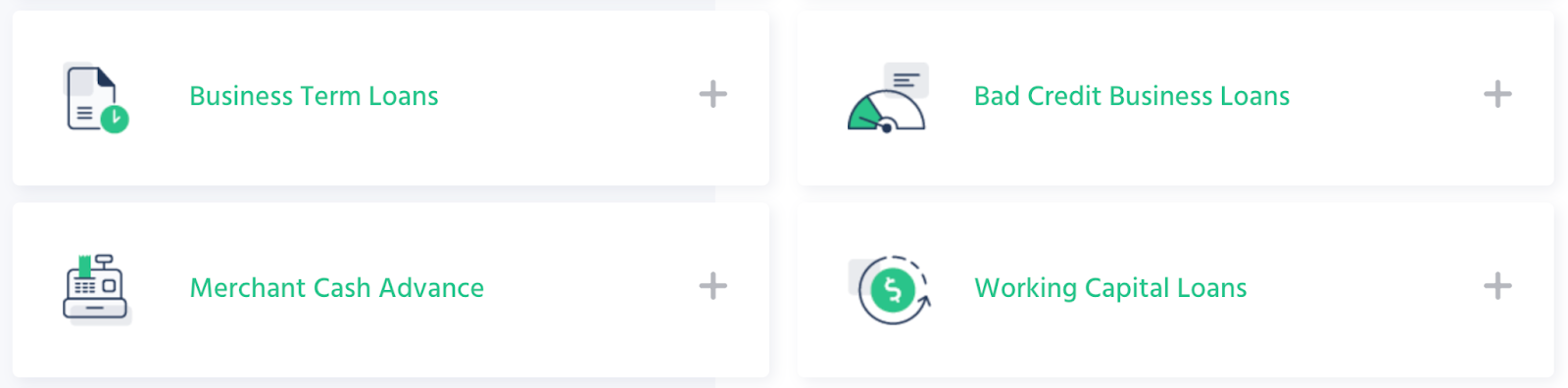

3. A Variety of Factoring Offers

Technically, United Capital Source is not a lender (they don’t finance the offers themselves). With connections to over 75 lenders, United Capital Source broadens the spectrum of choices for businesses — This means that United Capital Source can have your back with a bunch of funding options to fit any business need.

Here are the ways they might be able to help you:

- Got a rocky credit history? Check out their Bad Credit Business Loans.

- Need cash flexibility? The Business Line of Credit lets you draw funds as you go.

- Ladies in business, they’ve got special financing for you with Business Loans for Women.

- For a lump sum upfront with predictable payments, there are Business Term Loans.

- Need new equipment? Equipment Financing’s your go-to.

- Sorting out cash flow? Invoice/Receivables Financing and Merchant Cash Advance give you quick liquidity.

- Want your repayments linked to your revenue? Revenue-Based Business Loans are the way to go.

- Small Business Administration (SBA) backing for favorable terms? Yup, they’ve got SBA Business Loans.

- Short on operational funds? Grab a Working Capital Loan.

Whether it’s bad credit or big dreams, United Capital Source probably has a factoring solution.

You might also like: What is the Best Credit Card for Ad Spend? Expert Insights

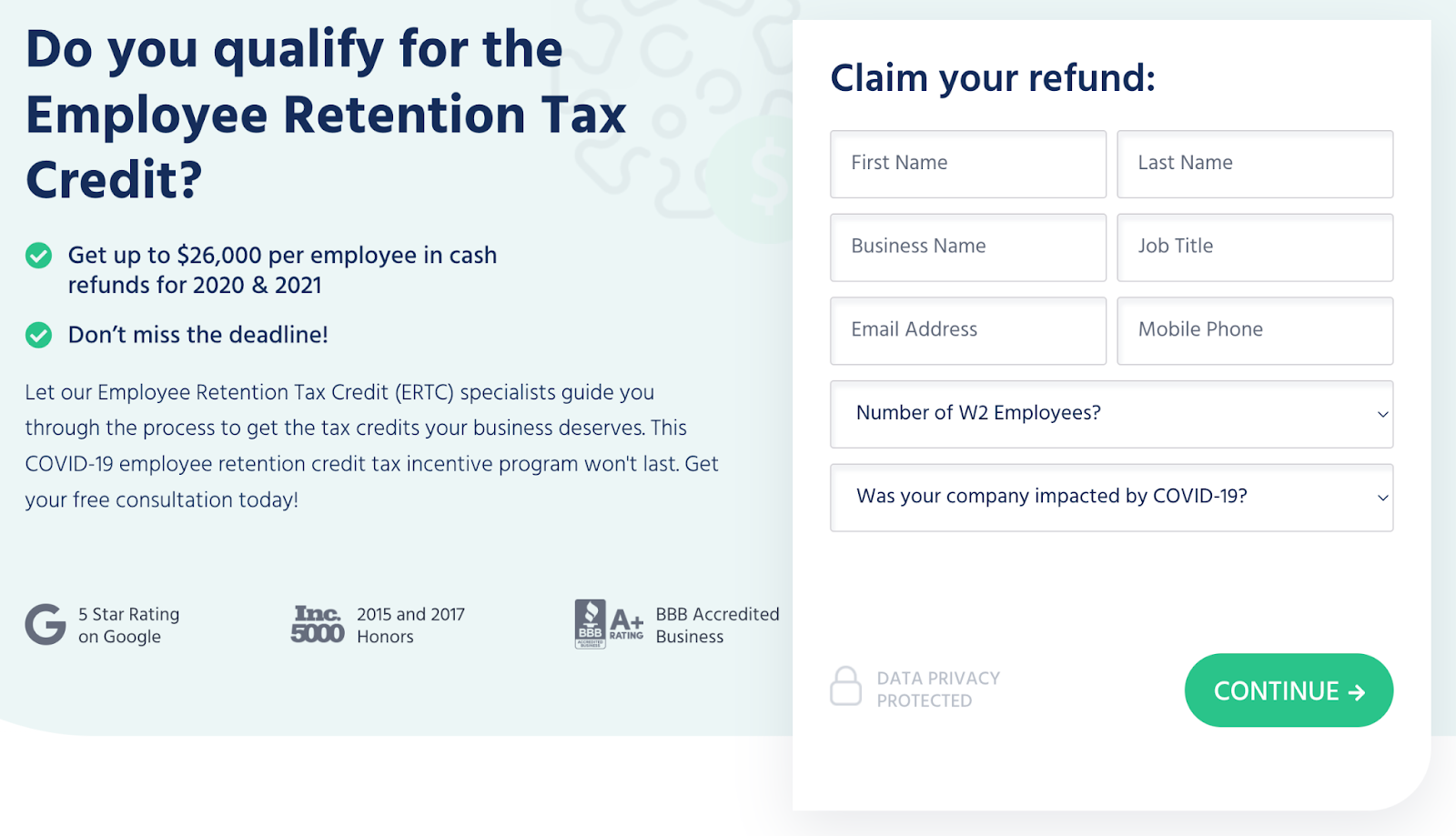

4. United Capital Source “Grants” (ERC)

So many people are interested in grants when researching this company, that I want to address this. While United Capital Source does not actually provide grants, they do offer help accessing Employee Retention Tax Credits (ERTC) for qualifying businesses. I think this is what business owners are looking for when they have this query.

So, let me explain.

ERTC is a tax break from the U.S. government to encourage businesses to keep their staff during tough times, like the COVID-19 pandemic. Essentially, eligible employers get a credit against certain employment taxes based on the wages they pay to employees and health plan expenses.

To qualify, businesses need to meet specific criteria, such as facing a significant drop in gross receipts or dealing with pandemic-related shutdowns – The goal is to provide financial support to businesses, helping them retain employees despite economic challenges.

Of course, details can change year by year, so it’s good to stay updated or consult a tax professional for the latest info. And, United Capital Source may be able to help you in this realm.

You might also like: Behind the Scenes of Become.co: A Comprehensive Review

United Capital Source Alternatives

There are plenty of funding sources, outside of factoring, that you can use to grow your business. Take a look at this list of funding channels without the immediate financial pressures associated with traditional factoring.

As you consider these alternative funding sources, choose the option that aligns with your specific needs, growth stage, and risk tolerance.

Business Credit Cards

Business credit cards are my favorite method to manage expenses. Businesses owners can use credit cards for immediate access to funds, with the flexibility to carry a balance over time.

While they provide quick access to capital, it’s important to note that credit card interest rates can be comparable to factoring if you don’t pay your account off right away. To avoid this, look for cards with introductory low or 0% interest — it will give you more time to settle up.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

Venture Capital & Angel Investors

Venture capital (VC) is an option where external investors provide funding in exchange for equity in the business. This form of financing is particularly suitable for businesses with high growth potential and a robust business model.

Angel investors are individuals who invest their personal funds in businesses — like VC funding —- typically in exchange for equity or convertible debt. This funding option is well-suited for startups and early-stage businesses with promising ideas.

While these options offer substantial funding without immediate repayment obligations, they come with the trade-off of relinquishing a portion of ownership to the investors. Still, it typically has the payoff of fresh insights and investors not only provide financial support but often offer valuable mentorship.

Recommended: Y Combinator: Fast Track to Success or Waste of Time?

Asset-Based Loans

Both a Home Equity Line of Credit (HELOC) and a Real Estate Investor Line of Credit allow homeowners to leverage the equity in their homes as collateral for a line of credit — Both require a high credit score and property ownership.

On these loans, the rates are lower than most other loan types, so they’re great for debt consolidation and big purchases.

HELOCs are available to homeowners with sufficient home equity. They generally come with lower interest rates compared to some business loans. However, they involve the risk of using personal assets as collateral. A Real Estate Investor Line of Credit is similar, but doesn’t require that the property you borrow on is owner-occupied.

Recommended: The BRRRR Method: A Real Estate Portfolio-Building Blueprint

Crowdfunding

Crowdfunding involves raising funds from a large number of individuals through online platforms. This method is accessible to businesses with compelling stories or products that resonate with the public. Crowdfunding minimizes immediate financial burden as funds are pooled from multiple contributors.

However, the success of a crowdfunding campaign depends on effective marketing and a compelling pitch, and it can take longer to access your funds.

Check out platforms like Indiegogo, Kickstarter, and Crowdcube to get a better idea how it works.

Frequently Asked Questions

What is a capital source?

A capital source refers to the origin or provider of funds that businesses use for various purposes, such as operations, expansions, or investments. It can include traditional sources like banks, alternative lenders, investors, or financial institutions that offer capital to businesses in the form of loans, credit lines, or other financing solutions.

How can I find out if a loan company is legitimate?

Verifying the legitimacy of a loan company is critical. Start by checking if the company is registered and licensed to operate. Look for customer reviews and ratings on trusted platforms, such as the Better Business Bureau. Legitimate companies are transparent about their terms, fees, and conditions. Avoid companies that ask for upfront fees or seem overly aggressive. Verify their contact information and physical address, and consider seeking recommendations from trusted sources or industry experts.

How many businesses has United Capital Source funded?

United Capital Source has funded a significant number of businesses. While the exact count may vary, they proudly showcase their extensive track record with over $1.2 billion funded to small businesses through their marketplace. This information reflects the impact they have had in support of businesses with their factoring options.

Is United Capital a hedge fund?

No, United Capital Source is not a hedge fund — It’s a financial service provider that offers funding solutions for small businesses. Unlike hedge funds that primarily engage in investment and capital appreciation, United Capital Source focuses on providing businesses with cash flow through various factoring options like loans, merchant cash advances, and other financial products.

Conclusion: Is United Capital Source Legit?

Yeah! United Capital Source is an (impressively) well-rated factoring platform. If you don’t mind the hefty fees involved with this type of business funding, I think this is one of the more trustworthy “lenders” in the realm.

However — unless you have no other option or you’re going to miss an important window if you don’t get a loan now — you might do best to look into solutions that come with lower long-term costs.

I prefer either business credit cards or traditional term loans (including asset-based) because you can access substantial credit lines with your business credit and you don’t have to give up control or ownership of your company.

Are you ready to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!