Fora Financial is a pretty well-known source of small business funding. And, according to Trustpilot and other review sources, they’re also super well-rated. But, you and I both know that you can’t necessarily trust that all user reviews you see online are real…and not all online loans are legit.

So, let’s dive deep into Fora Financial’s offer, and see if we can get to the bottom of the issue. Find out if Fora’s offer is right for you.

Here’s what’s in store:

Now, let’s go!

What is Fora Financial?

Fora Financial is a financial services provider or alternative lender that specializes in funding solutions for small and medium-sized businesses — They provide options like small business loans with fixed payback schedules and revenue advances that adjust based on sales.

The application process is straightforward, typically involving an online application followed by a discussion with a “Capital Specialist” and, upon approval, receiving funds within a few days.

Their funding amounts range from a few thousand dollars up to $1.5 million (with no restrictions on how you use it). You might be able to qualify for 75 percent to 125 percent of your monthly gross sales.

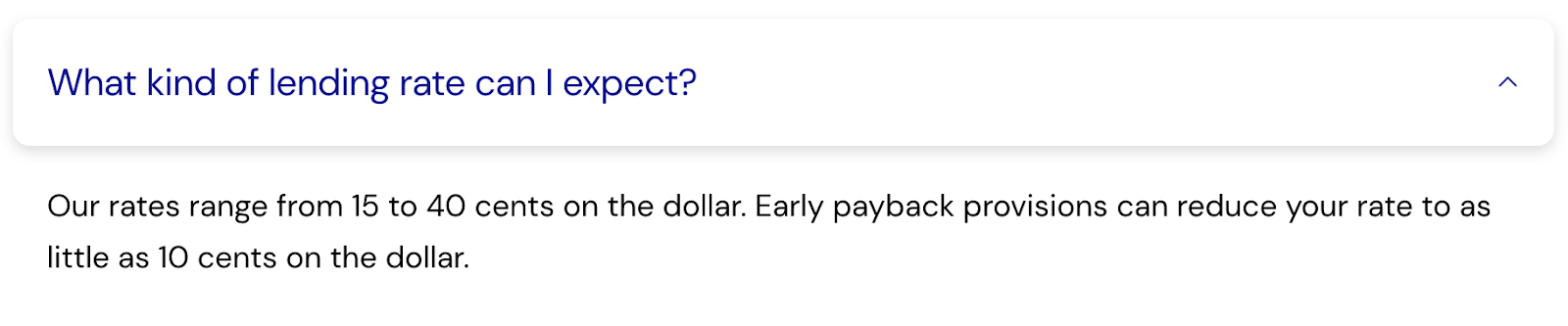

And, you’ll probably pay between 15 and 20 cents per dollar with their repayment terms.

Fora Financial caters to various industries and business needs, including cash flow management, equipment purchases, expansion, and more. Overall, they provide accessible financing options for businesses looking to address their funding needs.

You might also like: Could a Stripe Capital Loan Get Your Business Through a Rough Patch?

Fora Financial Loan Requirements

Like other alternative funding, and compared to traditional business loans, Fora Financial’s requirements are fairly relaxed. You do need to meet some requirements, but the appeal is that these loans are pretty easy to get (In exchange, you pay higher fees over the duration of the loan).

You will need a personal credit score of at least 500 (with no open bankruptcies) to qualify. Most people can meet this requirement easily.

And, according to anecdotal evidence (what I found in various forums), your business must have at least $12K to $15K in gross monthly income and to have been established for at least three months.

Some lenders require several years in business, so their business requirements are nice. However, conventional business loans look at your business credit score, so there’s no impact to your personal credit utilization as long as you pay as agreed.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

Is Fora Financial a Real Company?

I was surprised that people are wondering if the company is real. This one is easy to answer – yes, Fora Financial is an established business.

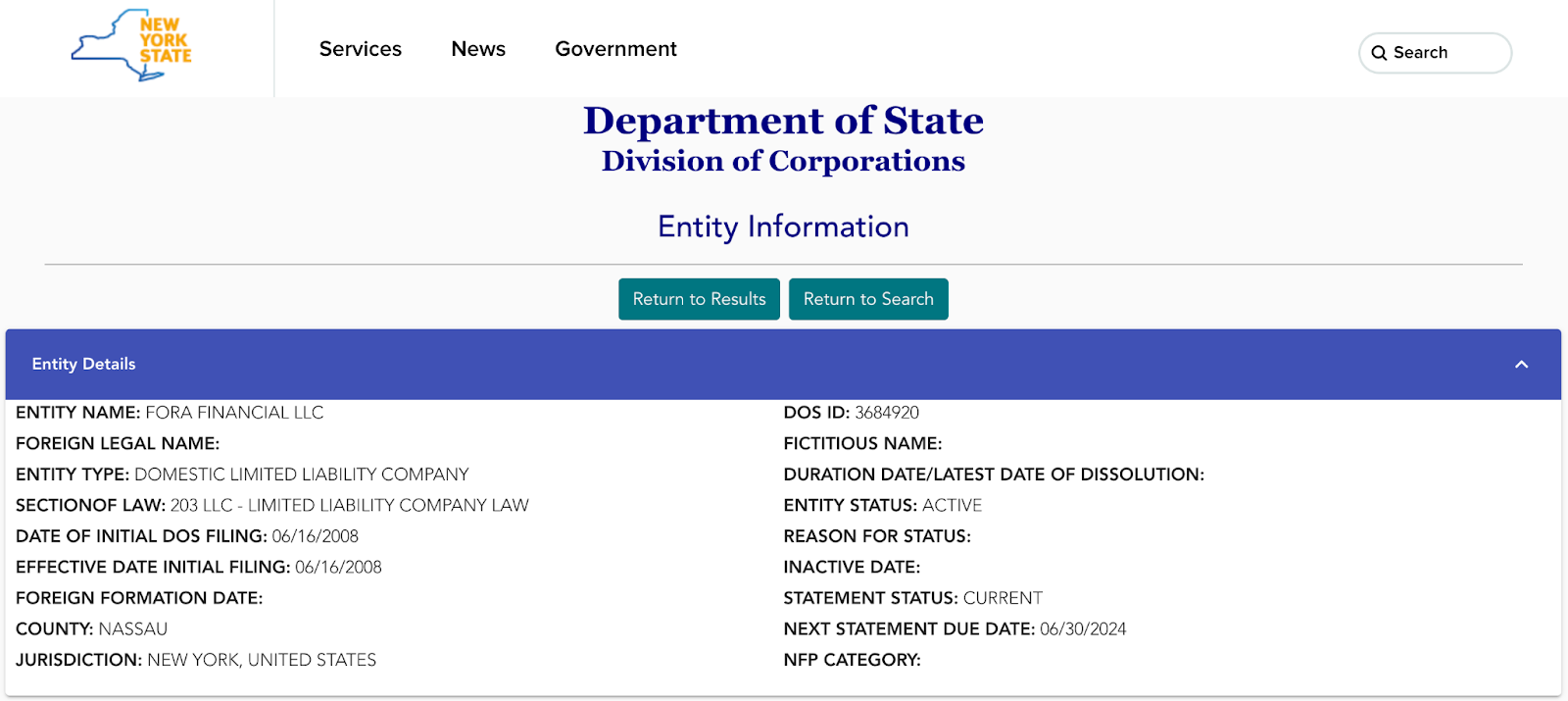

In fact, New York-based Fora Financial LLC was founded in 2008 by Daniel Smith and Jared Feldman. Back then, it was called Paramount Merchant Funding LLC (no relation to Paramount Payment Systems), and the name was changed in 2013.

Today, it’s a private-equity backed company that seems to be thriving.

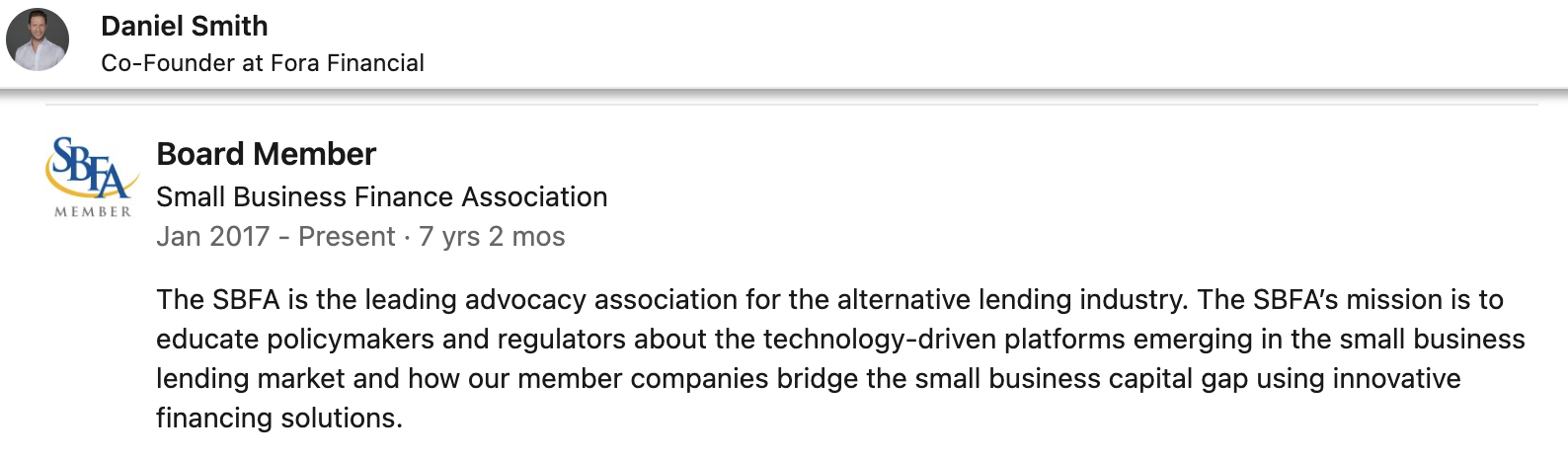

Feldman is the current CEO of Fora, where he’s been for almost 16 years. Smith is also still with the company and previously spent 7 years as a board member of the Small Business Finance Association.

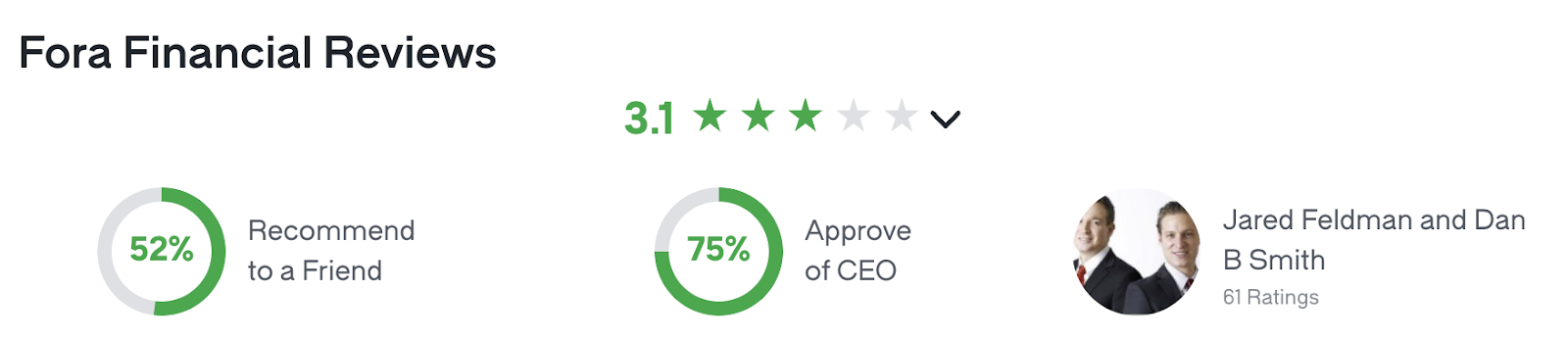

And, according to Glassdoor, most of Fora’s employees would refer a friend to the company and even more approve of company leadership.

How employees view a company really says a lot about its practices and overall internal ethics – in general, this one seems to have strong leadership.

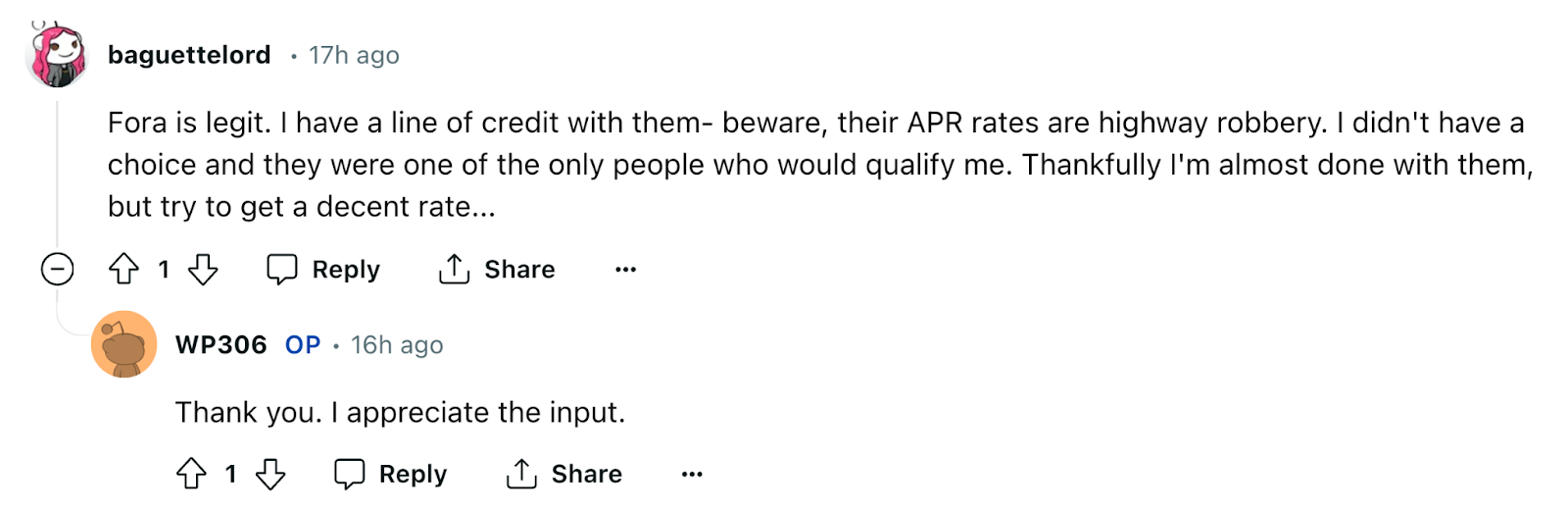

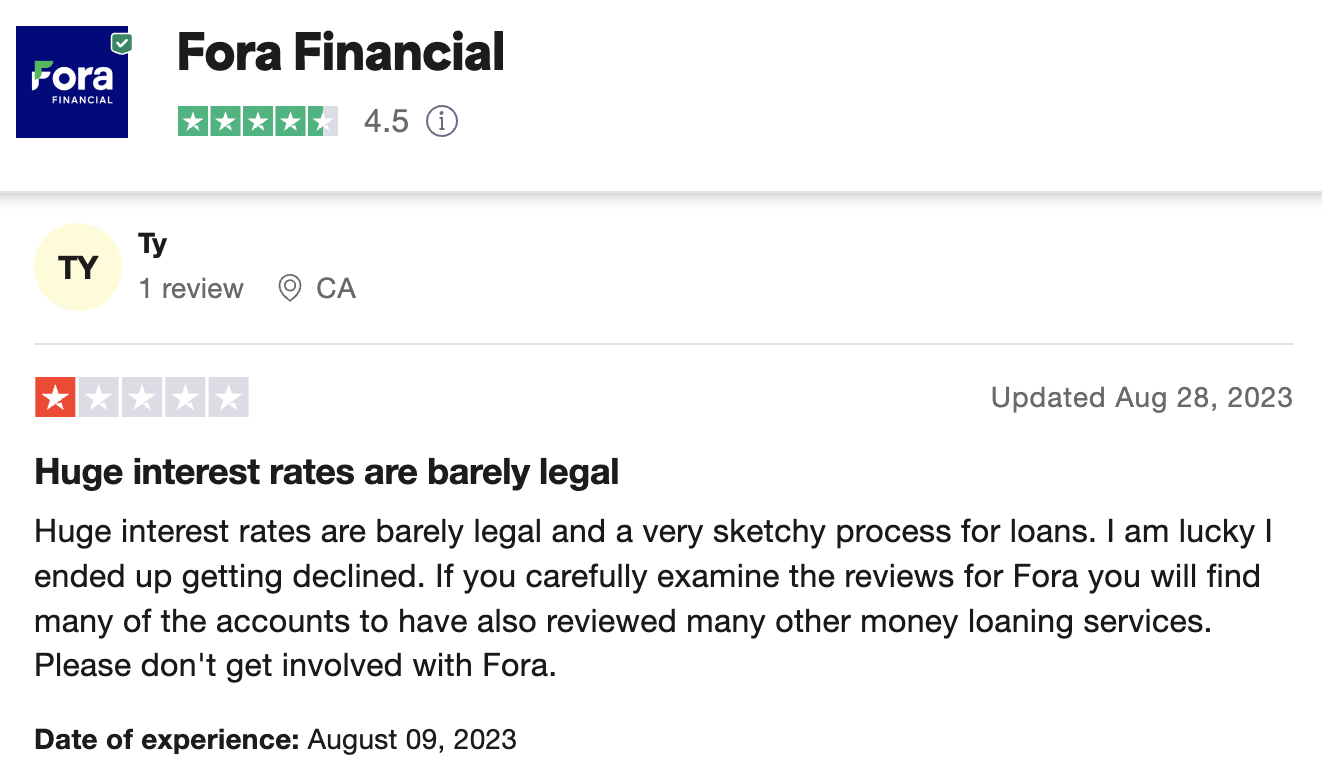

But, how customers see a business can tell us even more. With that said, Fora maintains a 4.5-star rating on Trustpilot, where most of the poor reviews come from people who don’t have loans with the company.

On this platform, the most common complaints are the loan interest rates and difficulty getting in touch with a representative.

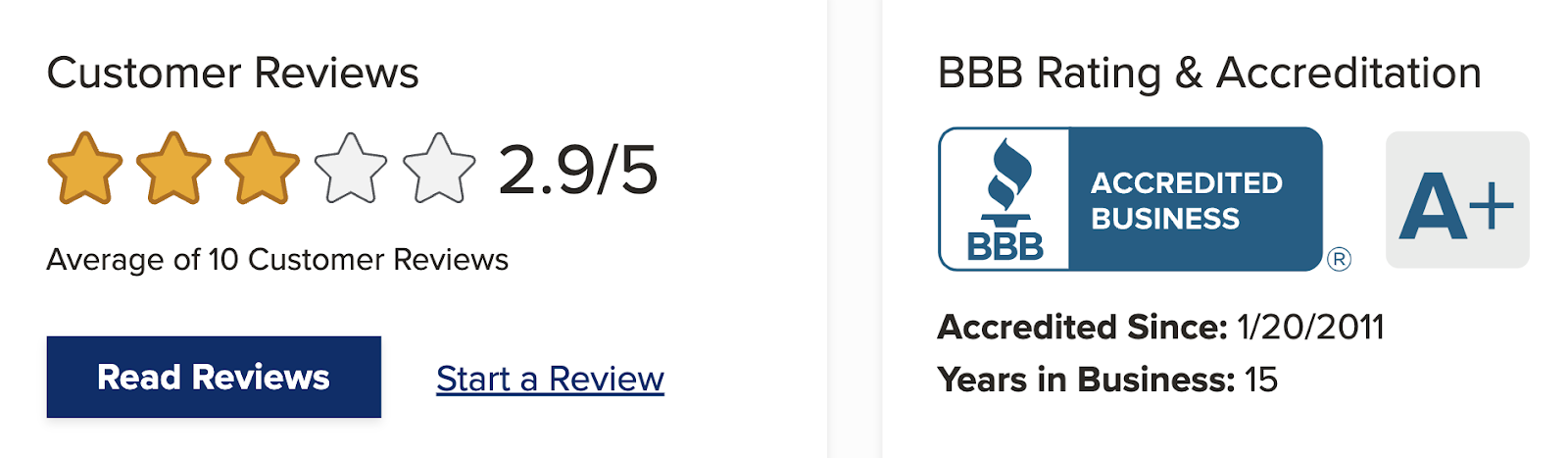

Now, when you check out Fora Financial’s standing with the Better Business Bureau, you’ll find that they are an accredited business with an A+ Rating. They have had seven customer complaints in the past three years (this is a relatively low number).

In sum, they appear to have a legit offer that could be worth checking out if you’d have trouble with approval from a more conventional lender.

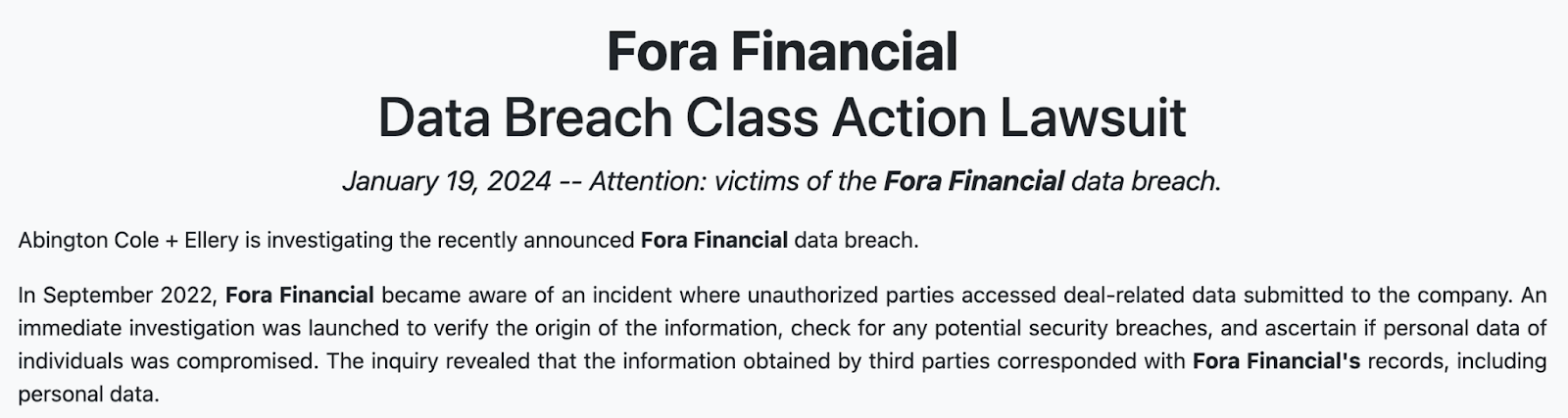

But, before you take that as a green light to go apply, you should know that – as of January 2024 – there is an open class action against Fora in which a data breach is being investigated.

In Fora’s defense, one of the world’s largest banks and even one of the three major credit bureaus have suffered data breaches.

You might also like: Is BHG Financial Legit? Personal & Business Loans, VC, & More

What Does Fora Financial Do?

In a nutshell, Fora offers small business loans and revenue advances quickly through a fast application and approval process. But, let’s take a closer look at each major facet of the offer so you can understand exactly what you’re considering signing up for.

You might also like: Torro Business Funding Review: Is This Zero Hassle Offer Legit?

1. Simple Application Process

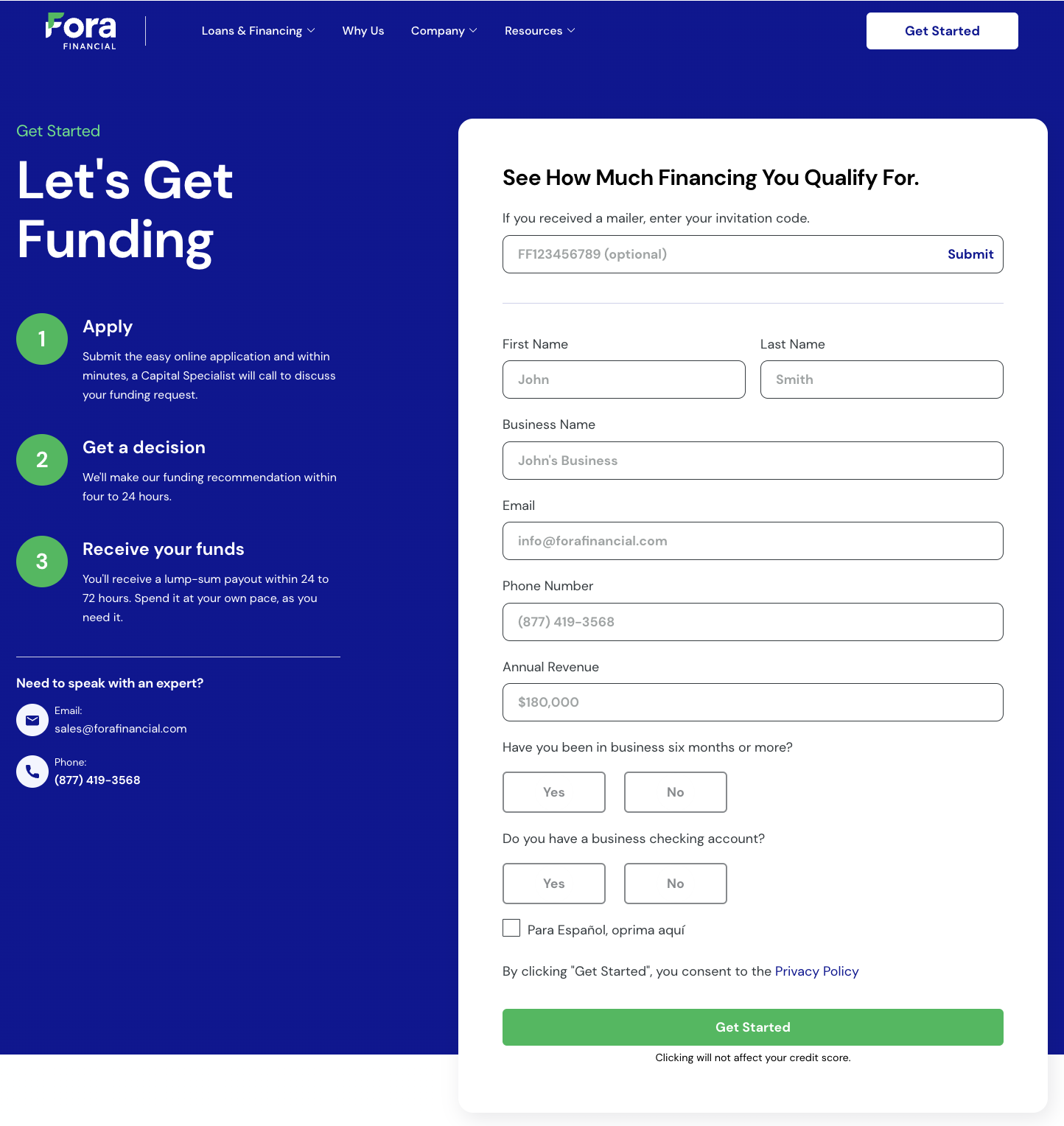

The application process with Fora Financial is straightforward and designed for convenience. First, you’ll need to fill out their easy online application form, which only takes a few minutes. Shortly after submitting your application, expect a call from one of their Capital Specialists to discuss your funding request in detail.

It’s important to note that Fora Financial will conduct a credit check as part of their review process, but only upon pre-approval.

Recommended: Free, Printable Business Credit Application Template (Plus, How to Use it Correctly)

2. Speedy Turnaround

Within four to 24 hours of your application submission, if you seem to be a good candidate, Fora Financial will provide you with a funding recommendation. Once approved, you can expect to receive your funds in a lump sum within 24 to 72 hours – This allows you to start utilizing the funds for your business needs straight away.

Be sure to read terms and conditions carefully for any offer Fora might send. You need to be sure your business has the ability to pay back the loan on-time as agreed.

Recommended: This is How to Build Business Credit Fast [Step-by-Step Guide]

3. Convenient Online Portal

When it comes to applying and repayment, Fora has a convenient online portal that you can access through their website.

An online portal is convenient for business borrowers because it offers easy access to loan information, application processes, and account management from anywhere with internet access.

This means you can apply for loans, check your account status, and manage payments without needing to visit a physical location or wait on hold for customer service. It saves time and offers flexibility.

You might also like: How to Convert Credit Cards into Cash

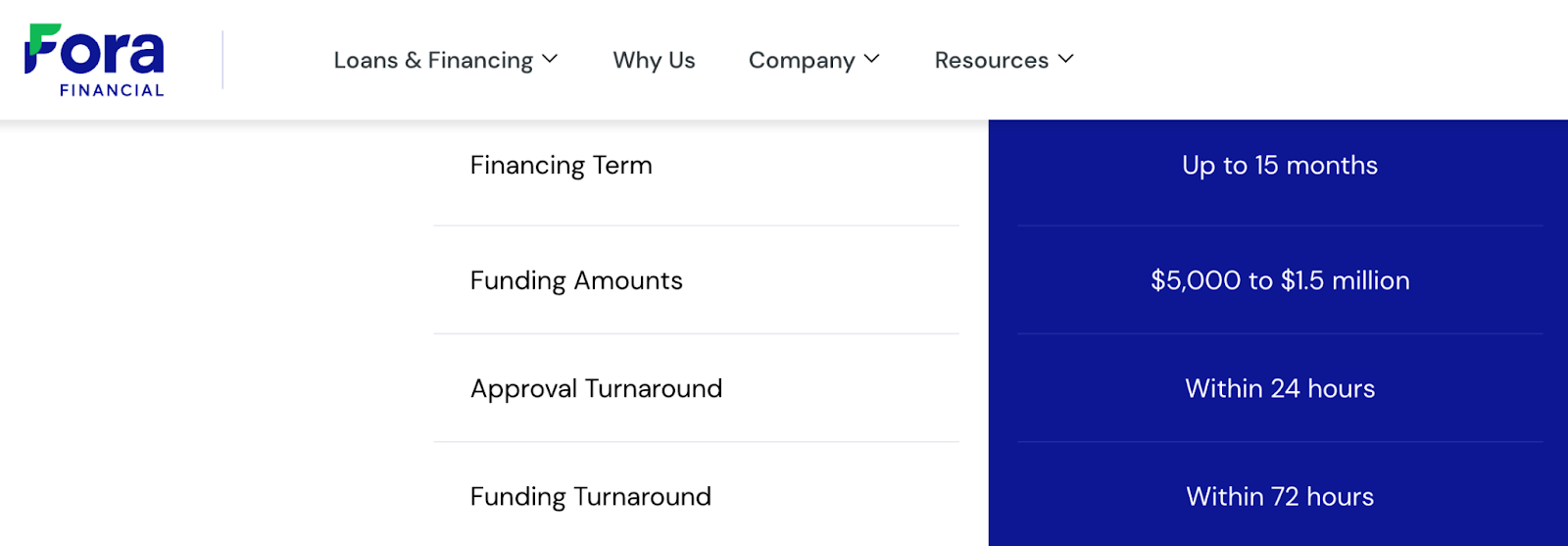

4. Repayment Terms up to 15 Months

Fora offers loans from $5K to $1.5M and repayment terms up to 15 months. This means that you will have over a year to either repay your loan or find a way to refinance it through a lower-interest lender.

And, Fora doesn’t penalize early repayment – in fact, Fora rewards responsible payment behavior. If you pay off your loan early, you’ll save money in most cases.

While this seems like a loan feature that should be standard, it’s not something you see with all online loans.

You might also like: 11 Alternate Ways for Entrepreneurs to Raise Capital with Online Lending Platforms

5. Small Business Loans

Fora Financial offers small business loans that can turn your entrepreneurial dreams into reality. With loan amounts ranging from $5K to $1.5 million in working capital, you have the financial flexibility to pursue opportunities and grow your business.

What’s great is that they don’t do hard credit pulls; just one soft inquiry when you apply, saving you from potential credit score damage. Plus, they offer pre-payment discounts and the chance to increase your borrowed amount after paying at least 60% of the original loan, providing ultimate flexibility.

And, you’re free to use the funds for almost any business expense, whether it’s expanding your operations, hiring more staff, or investing in equipment.

Recommended: How to Get an SBA Business Loan

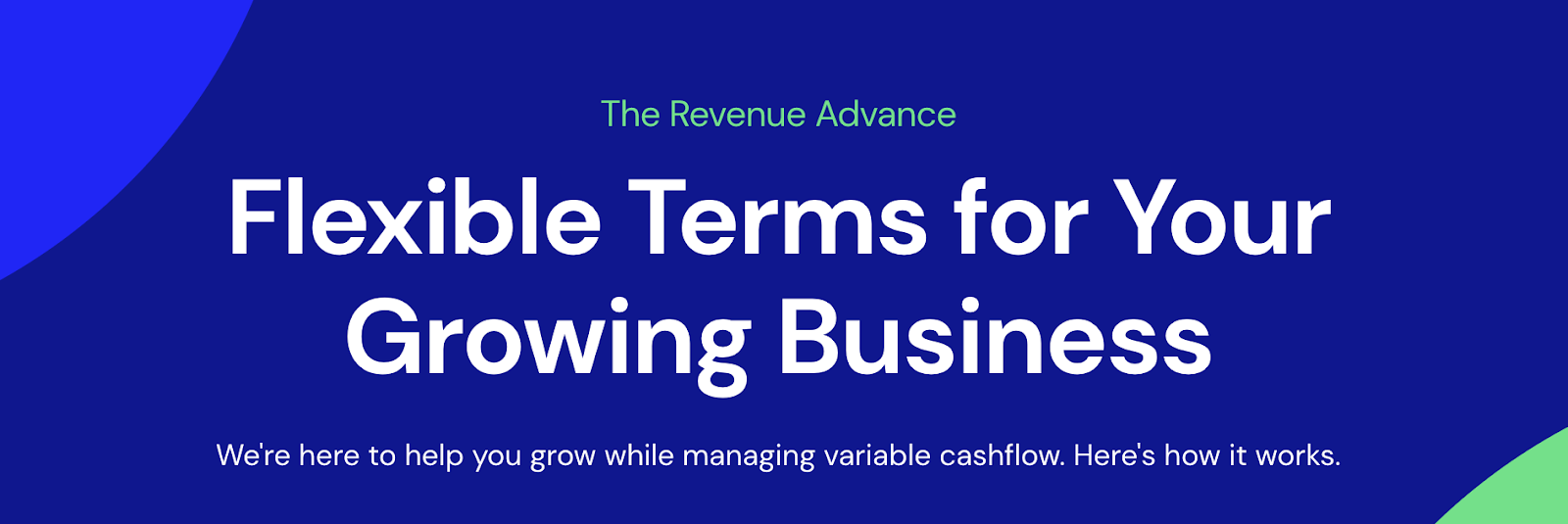

6. Revenue Advances

Fora Financial’s Revenue Advance is designed to provide flexible terms for businesses experiencing variable cash flow. With this option, you can borrow anywhere from $5K to $1.5 million against your future revenue.

The repayment structure is tailored to your business’s sales performance, making it easier to manage during both prosperous and lean times.

Here’s how it works:

- Instead of fixed monthly payments, you repay a fixed percentage of your daily or weekly sales.

- When your sales are booming, you’ll pay off your advance faster, but during slower periods, you’ll benefit from reduced payments (this gives you breathing room when you need to navigate challenging times).

In essence, this is a working capital loan or merchant cash advance. Again, I only recommend this type of financing if you have no other option.

You might also like: This is the Truth About LenCred’s Small Business Financing

Frequently Asked Questions

Does Fora Financial do credit checks?

Fora Financial conducts a soft credit inquiry when you apply for financing. This inquiry does not impact your credit score. However, they do not perform hard credit checks, so your credit score remains unaffected during the initial application process.

Is Fora Financial a direct lender?

Yes, Fora Financial is a direct lender. This means that they provide funding directly to borrowers without involving intermediaries or brokers. Working with a direct lender like Fora Financial can often streamline the loan process and offer more personalized service.

How do I get approved for financing with Fora Financial?

To get approved for financing with Fora Financial, you can start by filling out an online application on their website. Your personal credit score must be at least 500. The application process is straightforward and typically requires basic information about your business, such as revenue history and desired loan amount. Approval is based on various factors including your business’s financial health and creditworthiness.

Does Fora Financial report to credit bureaus?

No, Fora Financial does not report your payment history to major credit bureaus. This means that your loan with Fora Financial will not impact your business or consumer credit profile (unless you default on your loan).

Conclusion

As far as alternative lenders go, Fora is one of the good ones. While their rates are way too high for me to recommend the offer (I never recommend this type of loan unless the situation is so urgent and dire that there is no other choice).

This may seem like a natural benefit if you’re not versed in alternative loans, but the fact that Fora doesn’t have a prepayment penalty is fantastic – many online lenders will penalize you if you pay off your loan before the repayment date.

*Which is why it’s so important to read the terms and conditions.

Ready to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!