Proof of funds or POF comes up in most large financial transactions, particularly in real estate. If you apply for financing, participate in an auction, or make an offer on real property or another valuable item, you’ll be asked to provide proof of funds to demonstrate you can actually afford what you’re asking for.

Here, you’ll find exactly what proof of funds is, see examples, and learn how to show it when needed.

This is what’s in store:

- What is Proof of Funds?

- How Do You Demonstrate Proof of Funds?

- What is a Proof of Funds Letter?

- How Do You Get a POF Letter for Real Estate?

- Frequently Asked Questions

- Final Takeaway

Now, let’s roll!

What is Proof of Funds?

Proof of funds (POF) is a document or evidence that shows you have the financial means to complete a transaction. It’s usually required when you buy a property, apply for a loan, or make a large purchase.

Your POF can come in several forms, including:

- Bank statements

- Letters from banks or lenders

- Investment statements

- Proof of ownership of assets

The purpose is to reassure the seller, lender, or another party that you have the necessary funds to cover the cost.

In real estate, POF is a specific document that demonstrates that you have sufficient cash to cover the purchase of a home, including the down payment, closing costs, and escrow fees.

While a POF letter is customarily required when you buy a house, there are exceptions–For instance, if a property is sold directly by the owner, or if the buyer provides other evidence in the form of cash, account balances, or printed bank statements, a POF letter might not be needed.

You might also like: How to Raise Money for Real Estate Investment: A Beginner’s Guide

How Do You Demonstrate Proof of Funds?

In short, you can demonstrate proof of funds with bank statements, letters from banks, investment statements, and proof of assets. But, it can’t just be any bank statement or letter.

Bank statements must be recent, showing your current account balance. And, letters from banks or lenders must be official letters that verify either your account balance or the sum of funds available.

Moreover, investment statements must show the value of your investments and state how quickly these funds can become available if the transaction is finalized. Likewise, proof of assets needs to come in the form of documentation of valuable assets like real estate or stocks currently owned.

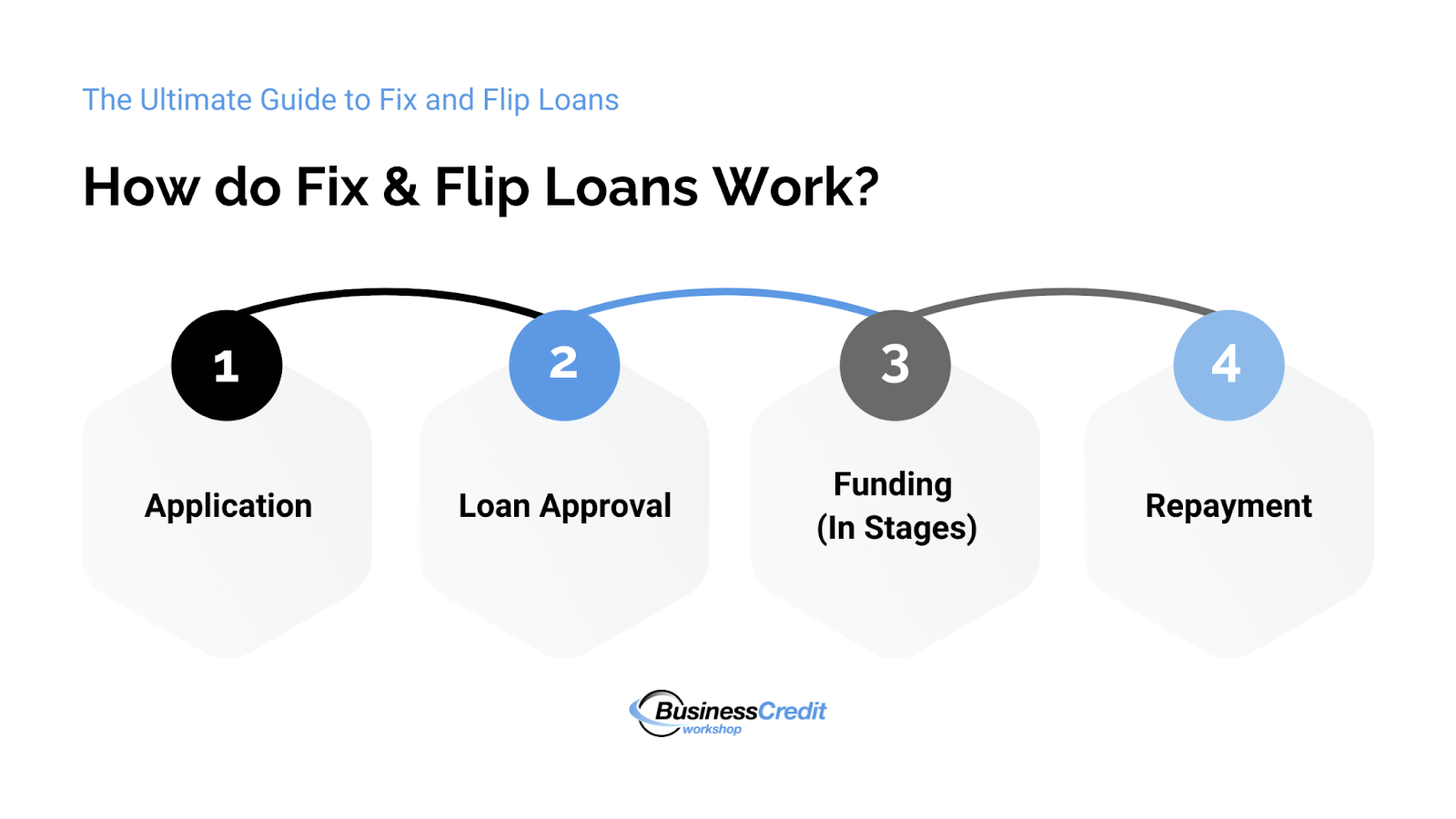

Recommended: The Ultimate Guide to Fix and Flip Loans: Fund Your Next Venture

What Qualifies as Proof of Funds?

The success of a deal usually depends on the availability of funds, including the amount you have or can get and how quickly you can provide it. Assets without liquidity (immediate cash value) typically don’t qualify as proof of funds.

The following typically don’t qualify as liquid assets:

- Life insurance

- Mutual funds

- Retirement accounts

- Automobiles

- Collectibles

Liquid assets are those that can be quickly converted into cash without significantly affecting their value.

Some examples of liquid assets include:

- Prequalification for a mortgage or loan intended to purchase the property

- Physical cash money or funds in a checking account

- Funds in savings accounts that can be accessed readily

- Money Market Accounts that offer immediate withdrawal

- Certificates of Deposit that are close to maturity or have a low penalty for early withdrawal

- Publicly traded securities that can be sold quickly on the market

- Short-term government securities that can be easily converted to cash

Usually, as long as you can get quick access to cash, your asset or account should qualify. Each party and institution may have their own terms.

Be sure to clarify with the party whether or not the type of assets you have will qualify as POF for the transaction. For example, some parties will accept crypto investments as a liquid asset and others will not.

What is a Proof of Funds Letter?

A proof of funds letter or POF letter is a document from a financial institution that verifies that you have the necessary funds available for a specific purpose. It can serve as evidence that you have the financial resources required to complete a transaction.

The letter typically includes:

- Your name and contact information

- The institution’s information including name and address

- The date the letter was issued

- Account balance and type of account

- Confirmation from the institution that funds are available

- The signature and title of the representative verifying your funds

This letter will reassure the seller or lender that you have the financial capability to proceed with the transaction.

You might also like: How to Get Money for Real Estate Investing: 18 Practical Ideas

How Do You Get a POF Letter for Real Estate?

Proof of funds doesn’t just appear out of thin air–You have to put in a little bit of footwork.

To obtain proof of funds, you generally need to:

- Reach out to your bank or financial institution where your funds are held. You can do this in person, by phone, or through their online services.

- Ask for a letter or statement verifying your available funds. Specify that you need this for a particular purpose, such as buying a home or applying for a loan.

- Be prepared to provide your account details and any specific information the bank needs to generate the letter.

- Once the bank processes your request, review the letter for accuracy. Ensure it includes all required details and is issued on official bank letterhead.

To make it easy on the institution, provide them with a list of what you need.

Here’s a basic proof of funds letter template:

[Bank’s Letterhead]

[Date]

To Whom It May Concern:

This letter is to confirm that [Your Full Name] holds an account with our institution. The details of the account are as follows:

- Account Holder: [Your Full Name]

- Account Number: [Account Number]

- Account Type: [Checking/Savings/Money Market]

- Current Balance: [Available Balance]

As of the date of this letter, the funds listed above are available and accessible to the account holder.

If you have any questions or need further information, please contact us at [Bank’s Contact Information].

Sincerely,

[Bank Representative’s Name]

[Bank Representative’s Title]

[Bank’s Name]

[Bank’s Contact Information]

Note: With two clicks, you can instantly create a copy of this proof of funds template in GDocs, then edit as you like.

How to Get a POF Letter From Your Bank

To obtain a Proof of Funds letter from your bank, reach out to your bank or financial institution—You can do this in person, online, or over the phone.

Then, just ask for a POF letter. A POF letter will confirm the amount of money you have available in your account. Be ready to give details like the amount of funds needed, your account information, and any specific requirements the seller might have.

Your bank will prepare the letter, typically including your account balance and a statement that the funds are available for the transaction.

You might also like: Should You Use a Real Estate Investor Line of Credit to Buy Property?

How to Get a POF Letter From a Hard Money Lender

If you’re using a hard money lender, the process is a bit different. First, you should look for a reputable hard money lender who specializes in short-term loans for real estate.

Before you can get proof of funds, you’ll need to apply for a loan. To do this, you typically need to provide information about the property you’re interested in and your financial situation.

Once you’re pre-approved, the hard money lender will provide a POF letter. This letter will indicate the amount they are willing to lend you and confirm that the funds are available. Keep in mind that the seller or agent could charge an additional fee or deposit for hard money transactions (since so many of these fall through).

Finally, just present your POF letter to the seller or real estate agent to show that you have the financial backing to complete the purchase.

You might also like: A Review of Alpha Funding Partners – Are Their Solutions Right for You?

Frequently Asked Questions

Do I need to show proof of funds?

To find out if you need proof of funds, review the requirements for your transaction. Then, ask the seller or lender directly if proof of funds is needed. This will help you determine if proof of funds is required.

How do you prove where money came from?

To prove where money came from, you can provide documentation like bank statements, transaction records, or a letter from your bank that details the source of the funds—This is often required for compliance with financial regulations and to verify the legitimacy of the funds.

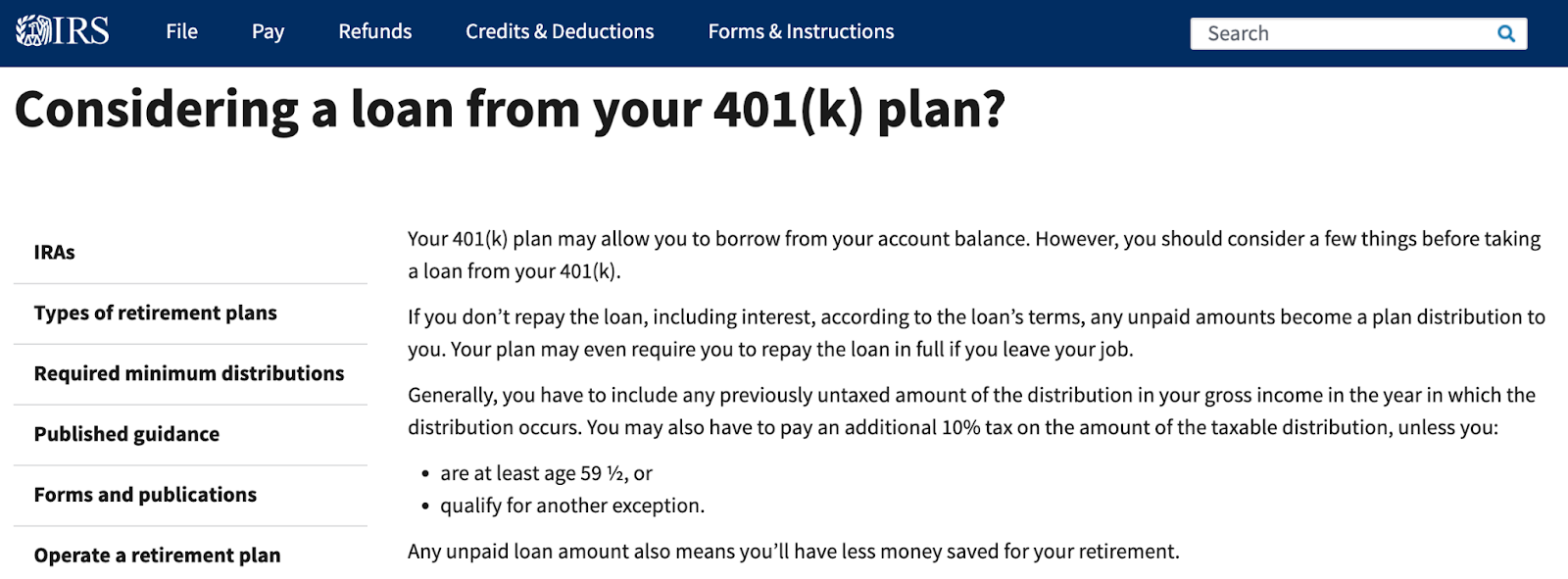

Does a 401(k) count as proof of funds?

No, a 401(k) does not count as proof of funds for transactions that require liquid assets because it is not considered liquid. Proof of funds typically needs to be in the form of cash or easily accessible accounts like checking or savings accounts.

What is a hard money proof of funds letter?

A hard money proof of funds letter is a document issued by a hard money lender confirming that they have the funds available to lend for a real estate investment. It is evidence that the lender has the financial capacity to provide the loan, often used in real estate transactions to reassure sellers or agents.

Final Takeaway

POF is a document or evidence that shows you have the financial means to complete a transaction like buying a property or applying for a loan–It includes various forms like bank statements, letters from financial institutions, and investment statements.

Liquid assets like cash and checking accounts, are acceptable for POF, while non-liquid assets, like retirement accounts and collectibles, are not. To obtain a POF letter, request it from your bank or financial institution, make sure it’s recent, detailed, and on official letterhead.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!